Global Micro-mobility Market Size by Propulsion Type, Vehicle Use, Sharing Type, Age Group, and Ownership – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Landscape & Forecast to 2032

Overview

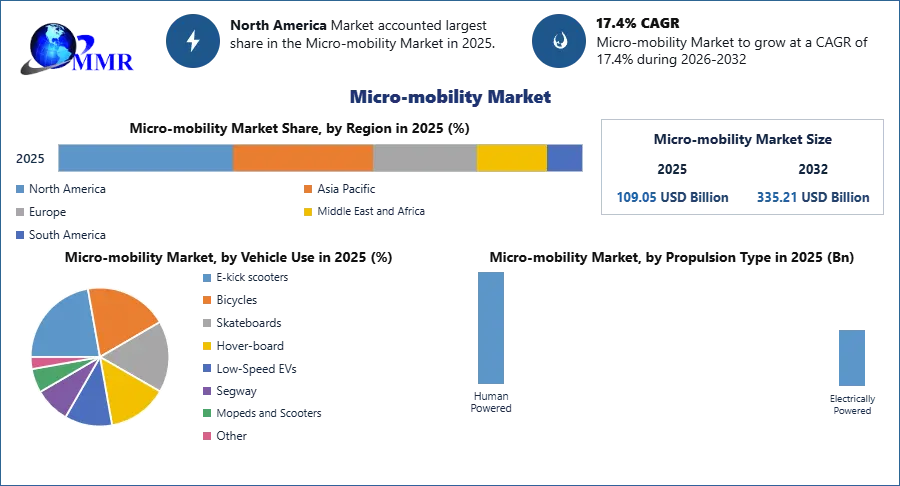

The Micro-mobility Market size was valued at USD 109.05 Billion in 2025 and the total Micro-mobility revenue is expected to grow at a CAGR of 17.4% from 2026 to 2032, reaching nearly USD 335.21 Billion.

Micro mobility encompasses small, lightweight vehicles traveling below 25 km/h (15.53 mph), providing eco-friendly alternatives to short car trips and tackling traffic congestion. It serves as a first/last mile solution, bridging the gap between travelers' origin/destination and nearby transit stops, and reducing commuter travel time. Micro-mobility has experienced significant growth and innovation over the last few years, driven by electric scooters and other last-mile transportation solutions. Companies like Lime, Bird, Grin, Yellow, Ofo, Mobike, Citi Bike, Jump Bikes, Skip, Spin, Scoot, PopScoot, Beam, Tier Mobility, Wind Mobility, Voi Technology, Vogo, Dott, and Flash have emerged as significant players in this space, attracting substantial venture capital and investor interest.

Micro-mobility solutions have been fueled by the urgent need to address congestion and pollution in megacities worldwide. Micro-mobility options, like e-scooters, electric, and pedal bikes, alleviate traffic gridlock, particularly during rush hours. While cities generally acknowledge the potential benefits of micro-mobility, they also express concerns about safety and the ability of existing infrastructure to accommodate the influx of these vehicles.

Large micro-mobility companies have been collaborating with cities, implementing measures like electronic geo-zones to regulate rider behavior and parking. Data-driven solutions offered by municipal transportation companies, such as Remix and Swiftly, further support cities in tracking and analyzing micro-mobility vehicles' movements. The demand for e-scooters and micro-mobility solutions is widespread, with riders willing to replace car trips. The success of European e-scooter startups can be attributed to Lime and Bird's achievements in Paris, Madrid, London, and Vienna. As the industry matures, the continued development of safe, data-backed, and regulated micro-mobility services is expected to garner increasing support from cities and the public.

Micro-mobility Market Scope and research methodology:

The micro-mobility market refers to the emerging sector of small, lightweight, and eco-friendly transportation solutions that operate at speeds below 25 km/h (15.53 mph). This market aims to address urban congestion, pollution, and efficient last-mile transportation options. Market size and potential qualitative and quantitative analyses are employed. Market trends, competitive landscape, and growth drivers are analyzed qualitatively, while statistical data is used to quantify market revenue, growth rates, and market share of key players. Market forecasting models also predict future market trends and opportunities.

The research methodology considers regional variations in the micro-mobility market. Different cities and countries have varying levels of adoption, regulations, and infrastructure, affecting market dynamics. The research considers these regional nuances to provide a holistic view of the micro-mobility market on a global scale. The study acknowledges the challenges faced by the micro-mobility industry. These challenges include safety concerns, parking and infrastructure issues, and competition from other transportation modes. By addressing these challenges and opportunities, the research offers insights into strategies for sustainable growth and market penetration. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Micro-mobility Market Dynamics:

Advancements in IoT and battery tech enhance micro-mobility solutions.

Urbanization has led to severe traffic congestion and pollution in many cities worldwide. Micro-mobility solutions offer a sustainable and eco-friendly alternative to cars, reducing traffic and carbon emissions. Micro-mobility provides convenient first/last mile solutions, bridging the gap between public transportation stops and travelers' final destinations. This convenience attracts commuters looking for efficient ways to travel. Micro-mobility devices, such as e-scooters and shared bikes, offer affordable transportation options compared to personal vehicles. Cost-effectiveness appeals to budget-conscious consumers and encourages adoption. A city with heavy traffic congestion and limited parking spaces implements a dockless e-scooter sharing program, allowing residents and visitors to easily move around the city center without private cars.

As smart cities develop, micro-mobility can be seamlessly integrated into urban transportation systems, creating a comprehensive mobility ecosystem. Continuous innovation in IoT devices, battery technology, and wireless connectivity can improve micro-mobility offerings, enhancing user experience and efficiency. Collaborations between municipal governments and micro-mobility operators can lead to better infrastructure and regulations, fostering a more sustainable and user-friendly micro-mobility environment. A city leverages IoT technology to implement a comprehensive micro-mobility network. This allows users to access shared e-scooters, bikes, and other devices seamlessly through a smart city app. Public and private sector collaborations support micro-mobility market growth and regulation.

The lack of dedicated lanes, parking, and charging stations hinders efficient micro-mobility services in cities.

Micro-mobility vehicles, particularly e-scooters, have faced safety issues, increasing accidents and injuries. The rapid growth of micro-mobility has caught many cities off-guard, leading to challenges in implementing and enforcing regulations to manage the influx of vehicles. Conflicts with existing transportation infrastructure and laws create barriers to smooth adoption. Cities are adequately equipped to handle the sudden surge in micro-mobility devices. The lack of dedicated bike lanes, parking spaces, and charging stations can hinder these services' efficiency. A city introduces an e-scooter sharing program without sufficient regulations, leading to irresponsible riding behavior and accidents.

The city faces difficulties enforcing rules and ensuring safety. Managing a large fleet of shared micro-mobility devices requires effective asset tracking, maintenance, and servicing. Companies must invest in systems to monitor vehicle health, location, and availability to ensure smooth operations. Shared micro-mobility devices are susceptible to misuse, vandalism, and theft. Companies must implement security measures and anti-theft technologies to protect their assets and maintain profitability. Operating a micro-mobility network involves deploying and redistributing devices strategically, considering demand patterns and charging needs. Logistics are essential to optimize fleet utilization and meet user demands. A shared e-bike company faces challenges managing and distributing its bikes across the city to meet user demand while ensuring they are regularly charged and maintained.

Micro-mobility Market Segmental Insights:

Based on Vehicle Use, In the Micro-mobility Market, E-kick scooters dominate the market in 2025 and are expected to grow during the forecast period. The micro-mobility market is analyzed based on the types of vehicles used for transportation. Among the listed vehicle types, e-kick scooters and bicycles dominate the micro-mobility market. E-Kick scooters or electric scooters have gained significant popularity in urban areas due to their convenience and ease of use. These scooters offer throttle or pedal assist, allowing users to move effortlessly without physical effort. The rise of dockless e-scooter sharing programs has made them readily available to the public, making short trips within cities more accessible. The micro-mobility market has been dominated by traditional bicycles and electric bikes.

Bicycles offer a sustainable and eco-friendly mode of transportation, and e-bikes with electric motor assistance provide an easier and faster cycling experience. Many cities have invested in infrastructure like protected bike lanes and cycling superhighways to promote bike usage and increase safety.

E-kick scooters and bicycles are leading the way for micro-mobility vehicles such as skateboards, hoverboards, and electric vehicles. E-scooters have quickly gained popularity in the past few years, especially with dockless sharing programs in various cities. They offer a solution to short-distance trips, often replacing short car rides and reducing traffic congestion. Bicycles, both traditional and e-bikes, remain a strong contender in the micro-mobility market. Their long-standing presence and established infrastructure, coupled with increasing interest in sustainable transportation, contribute to their dominance. Bike-sharing programs in many cities have made bicycle access easier. Bicycles and E-kick scooters are currently the dominant segments in the micro-mobility market, with e-scooters experiencing rapid growth in recent years, thanks to dockless sharing programs, while bicycles continue to be a reliable and eco-friendly option for urban transportation.

Micro-mobility Market Regional Insights:

North America dominates the micro-mobility revolution in the United States. It has seen a significant influx of e-scooters and bike-sharing services. The region's tech-savvy population, urban density, and growing demand for sustainable transportation are driving factors in micro-vehicle adoption. North America has been the birthplace of several prominent micro-mobility companies like Lime and Bird, which have played a pivotal role in popularizing e-scooters. The region also faced challenges related to safety concerns, regulatory issues, and conflicts with local municipalities.

Europe appears to dominate the micro-mobility market. European cities have a well-established cycling culture, and favorable government policies and investments encourage micro-mobility solutions. Europe has several successful e-scooter companies that have expanded across the region. With a focus on sustainability and efficient urban transportation, Europe is leading the way in embracing micro-mobility as a mainstream mode of transportation. Favorable government policies and investments in cycling infrastructure have further bolstered micro-mobility options. The region has also witnessed the rise of several successful e-scooter companies like Voi, Tier, and Dott, which have expanded their operations across various European countries.

Asia-Pacific has also seen rapid growth in the micro-mobility market, fueled by its high population density and need for efficient urban transportation solutions. Chinese companies like Ofo and Mobike, which started as docked bike-sharing services, have expanded into e-scooters and electric bikes. The Asia-Pacific region has witnessed fierce competition among micro-mobility companies, leading to significant investments and rapid expansion. Micro-mobility companies face regulatory challenges and issues related to parking and vehicle maintenance in some cities.

Competitive Landscape

Key Players of the Micro-mobility Market profiled in the report include Accell Group, AGC Inc., Airwheel Holding Limited, and Beam Mobility Holdings PTE. Ltd, Bird Global, Inc, Bolt Mobility, Boosted USA, Derby Cycle, DOTT, Electric feel, Helbiz, Hellotracks LLC, JIANGSU XINRI E-VEHICLE CO., LTD., Joyride, Jugnoo, Lime Micro-mobility, Luna Systems, Lyft, Inc., SWAGTRON, Velvioo LLC, VOI, Vulog. This provides huge opportunities to serve many End-uses & customers and expand the Micro-mobility Market.

Recent Industry Developments

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 15 January 2026 | Neuron and Beam | The two Singapore-based rivals completed a strategic merger to create the largest shared micro-mobility operator in the Asia-Pacific region. | This consolidation strengthens market dominance across 100+ cities by streamlining fleet operations and reducing overhead costs. |

| 22 October 2025 | Cooltra Group | The company acquired Kleta Mobility’s urban bike-subscription business unit in Barcelona, adding a fleet of over 2,000 active subscriptions. | The acquisition expands Cooltra's subscription-based revenue stream and solidifies its leadership in the Spanish B2C micro-mobility sector. |

| 14 August 2025 | Lyft | Lyft finalized the acquisition of FreeNow for approximately €197 million to integrate taxis and micro-mobility into a single multimodal app. | This move provides instant access to 150 European cities, significantly challenging Uber’s regional dominance in shared transportation. |

| 28 May 2025 | Uber and WeRide | The companies announced a global partnership to deploy autonomous robotaxis and advanced AI-managed micro-mobility fleets in 15 global cities. | The collaboration utilizes AI-driven predictive demand to optimize fleet distribution and enhance safety for urban commuters. |

| 11 March 2025 | VisionEdgeOne | Backed by GCM Grosvenor, the firm purchased Inurba Mobility, acquiring a fleet of roughly 18,000 bicycles. | The deal secures long-term municipal contracts and establishes a heavy-asset foothold in the European public bike-share market. |

Micro-mobility Market Scope: Inquiry Before Buying

| Micro-mobility Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 109.05 USD Billion |

| Forecast Period 2026-2032 CAGR: | 17.4% | Market Size in 2032: | 335.21 USD Billion |

| Segments Covered: | by Propulsion Type | Human Powered Electrically Powered |

|

| by Vehicle Use | E-kick scooters Bicycles Skateboards Hover-board Low-Speed EVs Segway Mopeds and Scooters Other |

||

| by Sharing Type | Docked Dock-less |

||

| by Age Group | 15-34 35-54 55 and above |

||

| by Ownership | Business to Business Business to Consumer |

||

Micro-mobility Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (razil, Argentina Rest of South America)

Key Players / Competitors Profiles Covered in Brief in Global Micro-mobility Market Report in Strategic Perspective:

- Yadea Technology Group Co. Ltd.

- Jiangsu Xinri E-Vehicle Co. Ltd.

- AGC Inc.

- Segway Inc.

- Swagtron

- Airwheel Holding Limited

- Yamaha Motor Co. Ltd.

- Accell Group N.V.

- Derby Cycle AG

- Neutron Holdings Inc.

- Bird Rides Inc.

- ElectricFeel AG

- Beam Mobility Holdings Pte. Ltd.

- Dott B.V.

- Yulu Bikes Pvt. Ltd.

- Voi Technology AB

- Tier Mobility GmbH

- Dynamic

- Hellotracks LLC

- Veo Technologies Inc.

- Razor USA LLC

- Ninebot Inc.

- Gogoro Inc.

- Superpedestrian

- VanMoof