1. Industrial Cybersecurity Market : Market Introduction

1.1. Executive Summary

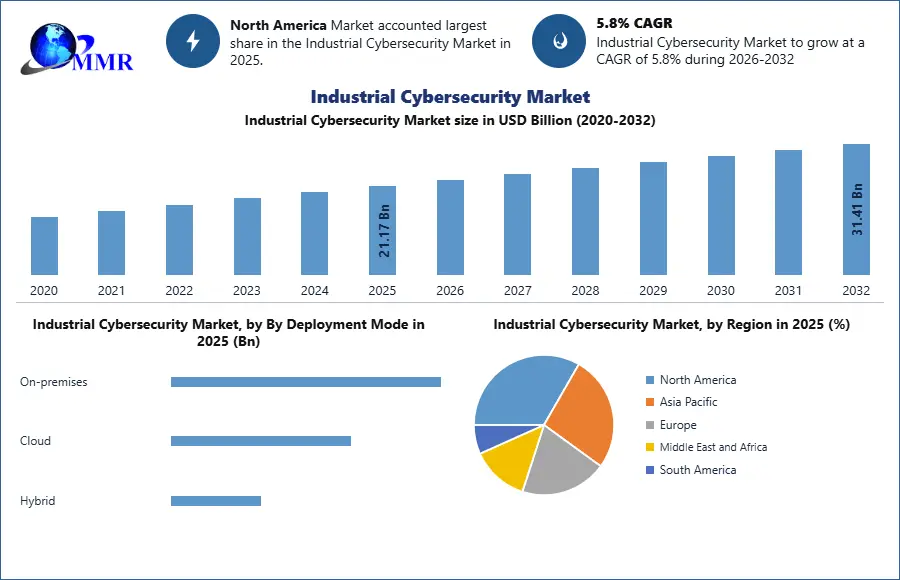

1.2. Market Size (2025) & Forecast (2026-2032)

1.3. Market Size (Value USD Billion) and Market Share (%) - By Segments, Regions, and Country

2. Industrial Cybersecurity Market Competitive Landscape

2.1. MMR Competition Matrix

2.2. Competitive Positioning of Top Key Players

2.3. Key Players Benchmarking

2.3.1 Company Name

2.3.2 Headquarters

2.3.3 Business Portfolio

2.3.4 Technology & Innovation Capability

2.3.5 Patent Portfolio Strength

2.3.6 Threat Detection Accuracy (%)

2.3.7 Consulting & Integration Capabilities

2.3.8 Customer Retention Rate (%)

2.3.9 Sustainability Initiatives

2.3.10 Certifications

2.3.11 Revenue (2025)

2.3.12 Market Share (%) 2025

2.3.13 Growth Rate (%)

2.3.14 R&D Investment (%)

2.3.15 Geographical Presence

2.4. Market Structure

2.4.1 Market Leaders

2.4.2 Market Followers

2.4.3 Emerging Players

2.5 Market Share Distribution of Leading Industrial Cybersecurity Vendors 2025

2.5.1 Market share and revenue analysis of top industrial cybersecurity companies

2.5.2 Global leaders in industrial cybersecurity: revenue scale, OT/ICS deployments, and platform capabilities

2.5.3 Vendor concentration ratio (Top 5 vs Top 10 share)

2.5.4 Market fragmentation assessment across global, niche, and OT-focused players

2.5.5 Regional market share variations among key vendors (North America, Europe, APAC)

2.5.6 Competitive intensity analysis across IT vs OT cybersecurity providers

2.5.7 Historical market share shifts driven by Industry 4.0 and IIoT adoption

2.6 Strategic Partnerships & Ecosystem Alliances

2.6.1 Strategic collaborations between cybersecurity vendors and industrial enterprises

2.6.2 Partnerships with industrial OEMs (automation, energy, manufacturing players)

2.6.3 Alliances with cloud providers for industrial cybersecurity platforms

2.6.4 Collaboration between IT security vendors and OT/ICS solution providers

2.6.5 Joint ventures supporting smart factory and critical infrastructure security

2.6.6 Ecosystem partnerships with system integrators and managed security providers

2.7 Technology Leadership & Innovation Benchmarking

2.7.1 Leadership in OT/ICS cybersecurity technologies and industrial protocols

2.7.2 AI-driven threat detection and automated incident response capabilities

2.7.3 Innovation in Zero Trust architecture for industrial environments

2.7.4 Cloud-native and edge security platform innovation benchmarking

2.7.5 Adoption of XDR, SIEM, and SOAR in industrial cybersecurity

2.7.6 R&D investment intensity among leading industrial cybersecurity providers

2.8 Competitive Differentiation & Strategic Positioning

2.8.1 Platform-based vs service-led industrial cybersecurity strategies

2.8.2 Differentiation through OT-native and ICS-specific security solutions

2.8.3 Competitive positioning based on scalability, real-time response, and reliability

2.8.4 Capability to secure multi-site industrial operations and distributed assets

2.8.5 Vendor specialization across network security, endpoint security, and OT protection

2.8.6 Long-term strategic positioning for Industry 4.0 and smart infrastructure security

3. Industrial Cybersecurity Market Dynamics

3.1. Industrial Cybersecurity Market Trends

3.2. Industrial Cybersecurity Market Dynamics

3.2.1 Drivers

3.2.2 Restraints

3.2.3 Opportunities

3.2.4 Challenges

3.3. PORTER’s Five Forces Analysis

3.4. PESTLE Analysis

3.5. Key Opinion Leader Analysis For the Global Industry

4. Industrial Threat Landscape & Cyber Risk Exposure Analysis 2025

4.1 Evolution of cyberattacks targeting OT/ICS environments

4.2 Ransomware, ICS malware, and supply chain attack trends

4.3 Industrial Control Systems (ICS) Threat Landscape

4.3.1 Common attack vectors (malware, ransomware, phishing, insider threats)

4.3.2 Case studies (Stuxnet, Colonial Pipeline, etc.)

4.3.3 Sector-wise vulnerability assessment

4.4 Industry-wise cyber risk exposure index (manufacturing, energy, etc.)

4.5 Attack surface expansion due to IT–OT convergence

4.6 Frequency and severity of cyber incidents in industrial systems

4.7 Financial and operational impact of industrial cyber breaches

4.8 Future threat outlook for critical infrastructure

5. Regional Cyber Attack Exposure & Threat Intelligence Analysis

5.1 Average cyberattack frequency on industrial systems (2020–2025)

5.2 Data breach incidents across critical infrastructure sectors

5.3 Attack rates on OT/ICS environments by region

5.4 Emerging attack vectors targeting industrial systems (ransomware, ICS malware, IIoT exploits)

6. OT–IT Convergence & Security Architecture Complexity Analysis 2025

6.1 Differences between IT (Information Technology) and OT (Operational Technology) environments

6.2 Challenges in securing legacy industrial control systems (ICS, SCADA)

6.3 Increasing convergence and its impact on cybersecurity demand

6.4 Integration of IT and OT networks: architecture transformation

6.5 Security challenges in legacy industrial control systems (ICS)

6.6 Network segmentation vs unified architecture trade-offs

6.7 Zero Trust implementation in industrial environments

6.8 Visibility gaps across OT assets and endpoints

6.9 Impact of IIoT expansion on cybersecurity complexity

6.10 Future-ready secure architecture models for smart factories

7. Pricing, Licensing & Commercial Model Analysis 2025

7.1 Pricing models across industrial cybersecurity solutions (license vs subscription)

7.2 Price Trend of Industrial Cybersecurity by Offering by region

7.3 Tiered pricing based on asset size, plant scale, and industry complexity

7.4 Total Cost of Ownership (TCO) for industrial cybersecurity deployment

7.5 ROI and payback period across industries (manufacturing, energy, etc.)

7.6 Shift toward managed security services and subscription-based models

8. Sector-wise Cybersecurity Demand Analysis

8.1 Energy & Power (critical infrastructure protection)

8.2 Oil & Gas (pipeline and refinery security)

8.3 Manufacturing (smart factories, Industry 4.0)

8.4 Utilities, Transportation, and Water Treatment

9. Deployment Architecture & Infrastructure Strategy Analysis 2025

9.1 On-premise vs cloud vs hybrid deployment trade-offs

9.2 Cybersecurity Architecture for Industrial Environments

9.2.1 Network segmentation, zero-trust architecture, and defense-in-depth strategies

9.2.2 Role of firewalls, IDS/IPS, endpoint security, and SIEM in OT environments

9.3 Latency, uptime, and reliability requirements in industrial systems

9.4 Edge security architecture for real-time industrial environments

9.5 Cloud security adoption in critical infrastructure sectors

9.6 Scalability and redundancy planning for industrial cybersecurity

9.7 Vendor lock-in risks and platform flexibility considerations

9.8 Infrastructure readiness for next-gen industrial security frameworks

10. Industrial Enterprise Adoption & Procurement Behavior Analysis 2025

10.1 Decision-making criteria for OT cybersecurity investments

10.2 Adoption rates by enterprise size (SMEs vs Large Enterprises)

10.3 Industry-wise adoption of industrial cybersecurity solutions

10.4 Integration with existing IT–OT infrastructure in industrial environments

10.5 Budget allocation trends across IT vs OT security

10.6 Preference for integrated platforms vs best-of-breed solutions

10.7 Role of OEMs, system integrators, and cybersecurity vendors

10.8 Buy vs build vs outsource security strategy decisions

10.9 Contract structures, SLAs, and managed service adoption

10.10 Adoption barriers among SMEs vs large industrial enterprises

11. Smart Manufacturing & IIoT Security Demand Analysis 2025

11.1 Cybersecurity demand driven by Industry 4.0 adoption

11.2 Security requirements for connected factories and automation

11.3 Risks associated with IIoT device proliferation

11.4 Integration of cybersecurity in digital twin environments

11.5 Role of edge computing in industrial security frameworks

11.6 Future demand outlook for smart factory cybersecurity

12. Industrial Cybersecurity Technology & Innovation Landscape 2025

12.1 Evolution of Industrial Cybersecurity Technologies

12.2 Core Technology Stack & Architecture Innovation

12.3 AI, Machine Learning & Automation in Cybersecurity

12.4 ICS, SCADA & OT-Specific Security Innovations

12.5 Cloud, Edge & Hybrid Security Advancements

12.6 Device-Level, Firmware & Embedded Security Innovation

12.7 Emerging Technologies Shaping Industrial Cybersecurity

13. Industrial Data Flow & Asset Connectivity Analysis 2025

13.1 End-to-end data flow across industrial control systems

13.2 Connectivity between SCADA, PLCs, IoT devices, and cloud platforms

13.3 Average number of connected assets per industrial facility

13.4 Data exchange bottlenecks and security vulnerabilities

13.5 Real-time vs batch data processing requirements

13.6 Impact of IIoT and smart manufacturing on data traffic growth

13.7 Infrastructure scaling requirements for secure data exchange

14. Industrial Cybersecurity Maturity Index Assessment 2025

14.1 Cybersecurity maturity scoring model for industrial enterprises

14.2 Adoption levels across industries and regions

14.3 Gap analysis between current and required security levels

14.4 Maturity models for industrial enterprises

14.5 Benchmarking companies by security capability level

14.6 Maturity comparison: SMEs vs large industrial enterprises

14.7 Correlation between digitalization and cybersecurity maturity

14.8 Regional variation in industrial cybersecurity readiness

14.9 Maturity roadmap for industrial organizations

15. Cyber Incident Response & Recovery Performance Analysis

15.1 Average detection and response time benchmarks

15.2 Incident containment and recovery timelines

15.3 Effectiveness of automated vs manual response systems

15.4 Role of SOC (Security Operations Centers) in industrial security

15.5 Post-incident operational stabilization metrics

15.6 Lessons learned from major industrial cyber incidents

16. Industrial Cybersecurity Platform Performance Benchmarking 2025

16.1 Threat detection accuracy and false positive rates

16.2 System uptime and availability benchmarking

16.3 Latency in threat detection and response

16.4 Scalability under high data and device loads

16.5 Comparative benchmarking of leading cybersecurity platforms

16.6 Performance under real-time industrial environments

17. Intellectual Property & Patent Landscape Analysis 2025

17.1 Patent filing trends in industrial cybersecurity technologies

17.2 Key innovation areas (AI security, ICS protection, encryption)

17.3 Company-wise patent leadership analysis

17.4 Collaboration between industry and research institutions

17.5 Technology commercialization trends

18. Human Factor & Cybersecurity Workforce Readiness Analysis 2025

18.1 Skill gap analysis in industrial cybersecurity workforce

18.2 Training and awareness programs across industrial enterprises

18.3 Role of human error in industrial cyber incidents (%)

18.4 Cybersecurity talent demand vs supply gap

18.5 Impact of workforce readiness on security posture

19. Industrial Cybersecurity Investment Landscape 2025

19.1 Global investment trends in industrial cybersecurity solutions

19.2 Venture capital and private equity funding in OT security startups

19.3 Mergers, acquisitions, and strategic partnerships

19.4 Investment focus areas: AI security, ICS protection, cloud security

19.5 Spending distribution across industries and regions

19.6 Future funding outlook for critical infrastructure protection

20. ROI & Cost-Benefit Analysis of Industrial Cybersecurity 2025

20.1 Cost of cyberattack vs cost of prevention (comparative analysis)

20.2 ROI on industrial cybersecurity investments (%)

20.3 Payback period and long-term cost savings

20.4 Productivity gains from secure and automated operations

20.5 Cyber insurance and risk mitigation cost modeling

20.6 Sensitivity analysis of investment vs risk exposure reduction

21. Industrial Cybersecurity Ecosystem & Value Chain Analysis 2025

21.1 Value chain mapping: OEMs, cybersecurity vendors, integrators, end-users

21.2 Role of industrial OEMs vs pure-play cybersecurity providers

21.3 Cloud, edge, and platform providers in industrial security ecosystem

21.4 Startups and niche players driving OT cybersecurity innovation

21.5 Strategic collaborations and partnerships across the ecosystem

22. Industrial Operations Impact & Downtime Risk Analysis 2025

22.1 Cost of downtime due to cyber incidents (USD/hour analysis)

22.2 Production loss and operational disruption case analysis

22.3 Impact on safety-critical systems and human risk factors

22.4 Cybersecurity role in maintaining operational continuity

22.5 Incident response time vs operational recovery metrics

22.6 Business continuity planning and disaster recovery readiness

22.7 Quantifiable benefits of proactive cybersecurity deployment

23. Industrial Cybersecurity Sustainability Landscape 2025

23.1 Role of cybersecurity in enabling sustainable and energy-efficient industrial operations

23.2 Energy consumption and carbon footprint analysis of cybersecurity infrastructure

23.3 Adoption of green IT practices in industrial cybersecurity

23.4 Cybersecurity’s role in preventing environmental and operational risks

23.5 Integration of cybersecurity within ESG frameworks

23.6 Sustainable supply chain and vendor risk management

23.7 Lifecycle management and e-waste reduction

24. Data Security, Compliance & Regulatory Impact Analysis 2025

24.1 Industrial cybersecurity regulations across key regions

24.2 Compliance requirements for critical infrastructure sectors

24.3 Data protection, encryption, and access control mandates

24.4 Impact of regulatory frameworks on solution adoption

24.5 Cost of compliance vs non-compliance risk analysis

24.6 Role of cybersecurity in audit readiness and reporting

24.7 Future regulatory trends shaping industrial cybersecurity

25. Industrial Cybersecurity Market : Global Industrial Cybersecurity Market Size and Forecast by Segmentation (by Value in USD Billion) (2025-2032)

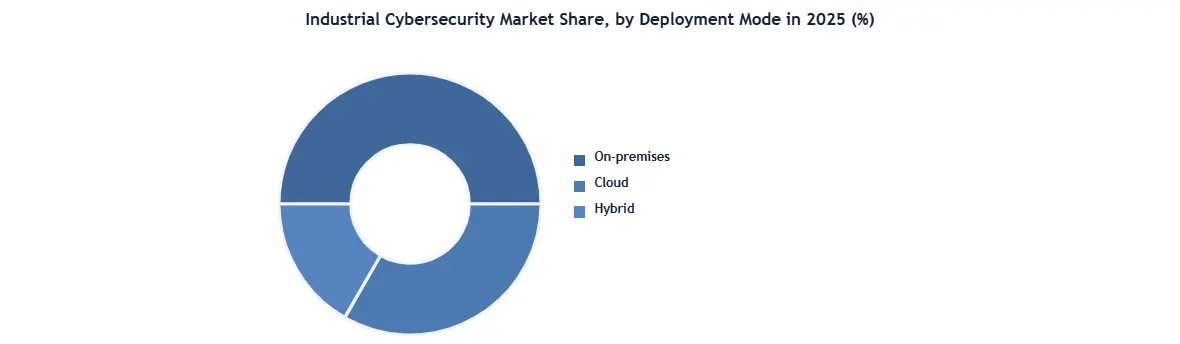

25.1. Global Industrial Cybersecurity Market Size and Forecast, By Deployment Mode

25.1.1 Cloud

25.1.2 On-premises

25.1.3 Hybrid

25.2. Global Industrial Cybersecurity Market Size and Forecast, By Security

25.2.1 Network Security

25.2.2 Endpoint Security

25.2.3 Application Security

25.2.4 Cloud Security

25.2.5 Wireless Security

25.2.6 Others

25.3. Global Industrial Cybersecurity Market Size and Forecast, By Solution Type

25.3.1 Antivirus/Malware Solutions

25.3.2 Firewall Solutions

25.3.3 Proxy Firewall

25.3.4 Packet-Filtering Firewall

25.3.5 Stateful Inspection Firewall

25.3.6 Next-Generation Firewall (NGFW)

25.3.7 Data Loss Prevention (DLP)

25.3.8 Security Information and Event Management (SIEM)

25.3.9 Intrusion Detection and Prevention Systems (IDS/IPS)

25.3.10 Identity and Access Management (IAM)

25.3.11 Others

25.4. Global Industrial Cybersecurity Market Size and Forecast, By Offering

25.4.1 Hardware

25.4.2 Gateways

25.4.3 Networking Devices

25.4.4 Hardware Security Modules (HSM)

25.4.5 Encryption Storage Devices

25.4.6 Network Encryption Appliances

25.4.7 Secure USB Drives

25.4.8 Hardware Tokens

25.4.9 Network Access Control Devices

25.4.10 Software

25.4.11 Antivirus and Malware Protection Software

25.4.12 SCADA Security Software

25.4.13 SIEM Software

25.4.14 Encryption Software

25.4.15 Services

25.4.16 Managed Services

25.4.17 Network Monitoring

25.4.18 Threat Intelligence & Incident Response

25.4.19 Professional Services

25.4.20 Consulting

25.4.21 Integration & Deployment

25.4.22 Training & Support

25.5. Global Industrial Cybersecurity Market Size and Forecast, By Enterprise Size

25.5.1 Small & Medium Enterprises

25.5.2 Large Enterprises

25.6. Global Industrial Cybersecurity Market Size and Forecast, By Vertical

25.6.1 Healthcare & Life Sciences

25.6.2 Hospitals

25.6.3 Medical Device Manufacturers

25.6.4 Pharmaceutical Companies

25.6.5 Aerospace & Defense

25.6.6 Military Systems

25.6.7 Aviation Manufacturing

25.6.8 Defense Contractors

25.6.9 Manufacturing

25.6.10 Automotive

25.6.11 Machine Manufacturing

25.6.12 Semiconductor & Electronics

25.6.13 Others

25.6.14 Energy & Utilities

25.6.15 Power Generation Plants

25.6.16 Nuclear Power Plants

25.6.17 Thermal & Hydropower Plants

25.6.18 Renewable Energy Power Plants

25.6.19 Power Grids

25.6.20 Oil & Gas Pipelines

25.6.21 Electric Power Transmission

25.6.22 Water Treatment and Distribution

25.6.23 Wastewater Collection and Treatment

25.6.24 Telecommunications

25.6.25 Network Operators

25.6.26 Data Centers

25.6.27 Internet Service Providers

25.6.28 Others

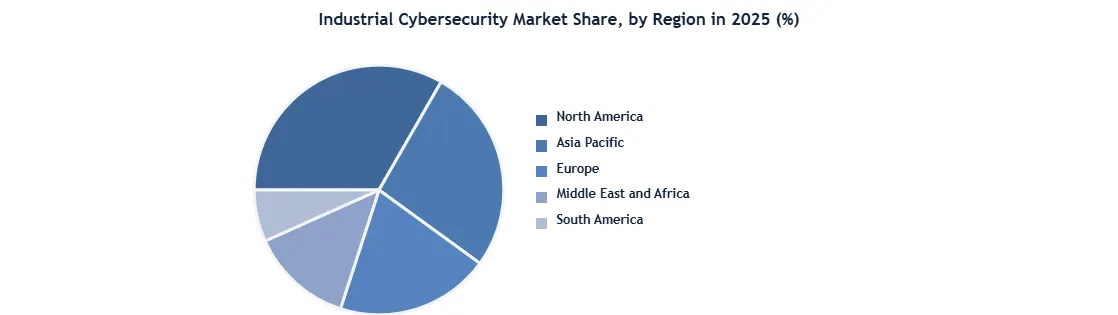

25.7. Global Industrial Cybersecurity Market Size and Forecast, by Region

25.7.1 North America

25.7.2 United States

25.7.3 Mexico

25.7.4 Canada

25.7.5 Europe

25.7.6 United Kingdom

25.7.7 France

25.7.8 Germany

25.7.9 Italy

25.7.10 Spain

25.7.11 Sweden

25.7.12 Russia

25.7.13 Rest of Europe

25.7.14 Asia Pacific

25.7.15 China

25.7.16 South Korea

25.7.17 Japan

25.7.18 India

25.7.19 Australia

25.7.20 Indonesia

25.7.21 Philippines

25.7.22 Malaysia

25.7.23 Vietnam

25.7.24 Thailand

25.7.25 Rest of Asia Pacific

25.7.26 Middle East and Africa

25.7.27 South Africa

25.7.28 GCC

25.7.29 Egypt

25.7.30 Nigeria

25.7.31 Rest of ME&A

25.7.32 South America

25.7.33 Brazil

25.7.34 Argentina

25.7.35 Colombia

25.7.36 Chile

25.7.37 Peru

25.7.38 Rest Of South America

26. Company Profile: Key Players

26.01.Cisco Systems, Inc.

26.01.1 Company Overview

26.01.2 Business Portfolio

26.01.3 Financial Overview

26.01.4 SWOT Analysis

26.01.5 Strategic Analysis

26.01.6 Recent Developments

26.02.Microsoft Corporation

26.03.IBM Corporation

26.04.Palo Alto Networks, Inc.

26.05.Fortinet, Inc.

26.06.Thales Group

26.07.NTT Data Corporation

26.08.Honeywell International Inc.

26.09.Siemens AG

26.10.Schneider Electric SE

26.11.ABB Ltd.

26.12.Rockwell Automation, Inc.

26.13.Broadcom Inc. (Symantec)

26.14.AO Kaspersky Lab

26.15.Trend Micro Incorporated

26.16.Dragos, Inc.

26.17.Claroty Ltd.

26.18.Nozomi Networks Inc.

26.19.OPSWAT Inc.

26.20.Musarubra US LLC (Trellix)

26.21.Dell Inc.

26.22.Accenture plc

26.23.BAE Systems plc

26.24.Forescout Technologies Inc.

26.25.Wipro Limited

26.26.General Electric Company

26.27.HCL Technologies Limited

26.28.Tata Consultancy Services (TCS)

26.29.Check Point Software Technologies Ltd.

26.30.CyberArk Software Ltd.

26.30.1 Others

27. Key Findings

28. Future Outlook & Analyst Recommendations

29. Industrial Cybersecurity Market : Research Methodology

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report