Big Data Market – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

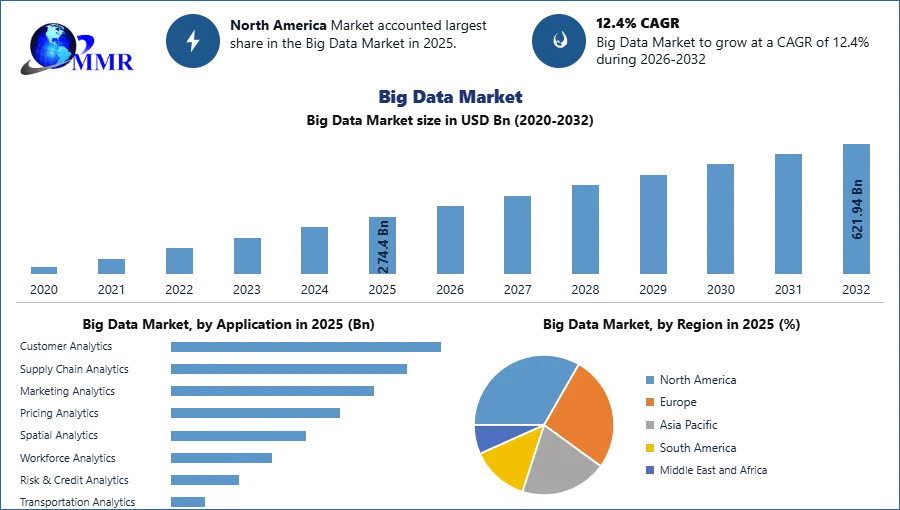

The Big Data Market size was valued at USD 244.13 Billion in 2025 and the total revenue is expected to grow at CAGR 12.4 % from 2026 to 2032, reaching nearly USD 621.94 Billion.

Big Data Market Overview:

Big Data refers to the immense volume of structured, semi-structured, and unstructured data that exceeds the capabilities of traditional data processing methods. The Big Data market focuses on harnessing the potential within this wealth of information, offering tools and technologies to extract valuable insights, patterns, and trends. The utilization of advanced analytics, machine learning, and artificial intelligence distinguishes the Big Data market as a driving force behind data-driven decision-making and innovation across various industries. In essence, the Big Data market revolves around empowering businesses to leverage their data for strategic purposes, unlocking new avenues for growth, efficiency, and competitiveness. As organizations recognize the significance of turning data into actionable intelligence, the Big Data market continues to enlarge, providing solutions that cater to the evolving needs of enterprises seeking to navigate the complexities of the digital age.

The Big Data market is a dynamic and rapidly evolving sector that plays a pivotal role in transforming the way organizations handle and derive insights from vast and complex datasets. Characterized by the continuous influx of information from diverse sources such as social media, IoT devices, and digital platforms, the Big Data market encompasses a spectrum of solutions and services tailored to manage, process, and analyze this massive volume of data. The detailed and constructive formation of key drivers, opportunities, and unique segmentation outputs structural and optimistic data. Validated using primary as well as secondary research methodology and scope of the Global Big Data Market.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Big Data Market Dynamics

Increasing Data Volume with Business Intelligence and Analytics Demand Driving Big Data Market Penetration

The exponential growth in data generation, fueled by digitalization, IoT devices, and online activities, is a significant driver for the Big Data market. Businesses are leveraging big data analytics to extract valuable insights from vast datasets, enabling informed decision-making and contributing to the overall growth of the Big Data Market. The rising demand for business intelligence and analytics solutions drives the Big Data market penetration. Organizations recognize the potential of extracting actionable insights from large datasets to gain a competitive edge, optimize operations, and identify new business opportunities, leading to increased market penetration. Technological advancements, including machine learning, artificial intelligence, and data science, contribute to the growth of the Big Data market. These technologies enhance the capabilities of big data analytics, allowing for more sophisticated analysis and predictive modeling, fostering innovation in the industry.

Industries such as finance, healthcare, and telecommunications require real-time data processing capabilities. The Big Data market addresses this demand by offering solutions that enable organizations to process and analyze data in real-time, leading to quicker and more accurate decision-making and creating new opportunities in the Big Data Market. Businesses across various sectors are placing a greater emphasis on enhancing customer experience. Big Data analytics helps organizations understand customer behavior, preferences, and trends, enabling personalized services and targeted marketing strategies, reflecting an emerging trend in the Big Data Market.

Data Privacy and Security Concerns Impacting Big Data Market Fluctuation

As the volume of data collected and processed increases, concerns about data privacy and security become more pronounced. Stringent regulations and the need for robust security measures pose challenges for organizations utilizing Big Data solutions, contributing to fluctuations in the Big Data Market. The implementation of Big Data solutions often involves substantial upfront costs for hardware, software, and skilled personnel. This cost barrier be a restraint for smaller organizations or those with budget constraints, necessitating a thorough pricing analysis in the Big Data Market. The shortage of skilled professionals in the field of big data analytics poses a challenge for organizations seeking to fully capitalize on their data. The complex nature of big data technologies requires expertise in data science, machine learning, and related domains, impacting the overall share in the Big Data Market.

Integrating big data solutions with existing IT infrastructure is challenging. Compatibility issues, data migration complexities, and the need for seamless integration with other enterprise systems hinder the adoption of Big Data technologies, affecting the industry dynamics in the Big Data Market. The quality of data is crucial for accurate analysis and decision-making. Incomplete, inaccurate, or inconsistent data lead to erroneous insights, impacting the overall share in the Big Data Market. Maintaining data quality remains a challenge, especially when dealing with large and diverse datasets.

Big Data Market Segment Analysis

Based on the Components, In 2025, the Software segment dominates the Big Data Market and holds the largest market share. This is driven by the increasing demand for advanced analytics, predictive modeling, and data visualization tools that help organizations derive actionable insights from vast datasets. The Hardware segment, which includes high-performance servers, storage solutions, and networking equipment, supports the infrastructure needed for data processing and storage. Meanwhile, the Services segment, covering consulting, system integration, training, support, and managed services, provides essential guidance and operational efficiency for organizations adopting Big Data solutions, contributing significantly to market growth.

Based on the Deployment Mode, In 2025, Cloud-Based solutions are expected to dominate the market due to their scalability, flexibility, and cost-effectiveness, making them the preferred choice for industries like retail, healthcare, and finance that require agility and rapid data processing. The Big Data Market is segmented into On-premise and Cloud-Based solutions, each serving specific organizational needs. Cloud solutions offer businesses the ability to store and analyze vast amounts of data without the heavy upfront costs of on-premise infrastructure. On the other hand, On-premise solutions are gaining traction in industries with stringent data security, privacy, and compliance requirements, such as government and defense. While on-premise systems come with higher initial investments and maintenance costs, they provide organizations with greater control over their data and operations, making them ideal for sectors where security and customization are paramount. Both deployment modes reflect the increasing demand for reliable and efficient Big Data solutions, with Cloud-Based solutions leading the way due to their scalability and ease of integration, while On-premise solutions cater to more specific, security-focused applications.

Based on the Application, In 2025, the Customer Analytics segment leads the Big Data Market, driven by the need for organizations to enhance customer experiences and optimize segmentation. Supply Chain Analytics improves inventory management and logistics, while Marketing Analytics helps businesses tailor strategies to boost engagement and ROI. Pricing Analytics aids in determining optimal pricing strategies, and Spatial Analytics leverages geographic data for insights in urban planning and retail expansion. Workforce Analytics optimizes talent management, and Risk & Credit Analytics enhances financial risk assessment and fraud detection. Transportation Analytics focuses on optimizing routes and predictive maintenance, improving efficiency in logistics and transit industries. These application segments collectively drive significant growth in the Big Data Market.

Manufacturing is a major segment in the Big Data Market, contributing to the industry's growth and innovation. Retailers benefit from Big Data in areas like inventory management, demand forecasting, and personalized marketing, making the retail and consumer goods segment a key player in the Big Data Market.

Big Data enhances content recommendation, audience analysis, and marketing strategies in the media and entertainment industry. The media and entertainment segment contributes significantly to the Big Data Market's share with its innovative applications. Big Data aids in smart grid management, predictive maintenance, and energy consumption optimization in the energy and utility sector. The energy and utility segment represent a major player in the Big Data Market, driving innovation and efficiency. The transportation industry utilizes Big Data for route optimization, predictive maintenance, and demand forecasting. Transportation is a significant regional segment with unique challenges and opportunities in the Big Data Market.

Big Data applications in this sector include network optimization, customer experience enhancement, and predictive analytics. The IT and telecommunication segment showcase fluctuation and responsiveness to emerging trends in the Big Data Market. Academic and research institutions leverage Big Data for scientific research, data-driven insights, and collaborative projects. The academia and research segment represent a regional focus on knowledge creation and innovation in the Big Data Market. This category encompasses various industries adopting Big Data for specific applications tailored to their needs. The "others" segment showcases diversity and niche opportunities within the Big Data Market.

Big Data Market Regional Analysis

North America, particularly the United States, exhibits robust regional growth in the Big Data Market. The U.S. leads the way with substantial market potential, driven by its advanced technological infrastructure and early adoption of Big Data solutions. In this region, the Big Data Market shares are significant, with key players in the U.S., Canada, and Mexico actively contributing to the industry's growth. Factors such as the widespread application of analytics in finance, healthcare, and IT industries contribute to North America's position as a major player in the global Big Data Market. The emphasis on emerging trends and innovation further strengthens the region's foothold in the industry.

Asia Pacific emerges as a dynamic and rapidly growing region in the Big Data Market, showcasing immense potential for market penetration and expansion. Key economies like China, India, and Japan contribute significantly to the region's growth. The adoption of digital technologies and the widespread availability of smartphones and internet connectivity fuel the demand for Big Data solutions. Industries in Asia Pacific, including manufacturing, healthcare, and telecommunications, actively invest in analytics to enhance operational efficiency. The region presents lucrative opportunities for Big Data Market share in countries like China and South Korea, making it a focal point for industry growth.

Europe holds a major share in the Big Data Market, driven by a well-established IT landscape and a focus on technological innovation. Key players in Germany, the United Kingdom, and France contribute significantly to the region's Big Data market share. European industries, spanning finance, healthcare, and manufacturing, leverage data analytics for decision-making and optimization. The region's commitment to data privacy and security aligns with the challenges posed by Big Data analytics. Strategic investments in research and development further strengthen Europe's position as a dominant player in the global Big Data Market, with notable regional growth in Germany and France.

The Middle East and Africa are witnessing a growing Big Data Market, fueled by increased digitization and a focus on data-driven decision-making. Governments and businesses in the region recognize the potential of Big Data solutions for enhancing efficiency and competitiveness. Industries such as finance, energy, and healthcare actively invest in analytics applications, contributing to regional growth. As an emerging market with untapped potential, the Middle East and Africa present opportunities for Big Data Market share expansion. The region's unique challenges and opportunities, coupled with strategic initiatives, contribute to its significance in the global Big Data landscape.

Big Data Market Competitive Landscape

Deloitte, a major Big Data market share holder, has entered into a global collaboration with IBM to enhance sustainability outcomes for organizations universal. The collaboration integrates IBM’s Envizi ESG Suite with Deloitte’s GreenLight Solution, aiming to streamline data, elevate insights, and accelerate transformation for end-to-end environmental needs. The collaboration emphasizes helping clients achieve improved sustainability outcomes by leveraging multiple IBM solutions and integrating data from the IBM Envizi ESG Suite with Deloitte’s GreenLight Solution.

Deloitte’s GreenLight Solution, a global Big Data market player, contributes to sustainability performance improvements, providing analysis on global credits, incentives, abatement strategies, and tools for planning and managing net-zero goals. On the other hand, IBM Envizi, a prominent manufacturer in the Big Data market, consolidates environmental, social, and governance (ESG) data into a single system, supporting emissions calculations, ESG reporting, and providing insights for decarbonization projects. The collaboration allows clients to transform organizations, drawing insights from Envizi while leveraging Deloitte’s extensive experience in sustainability and climate client service. The integration with IBM Envizi aims to streamline capabilities in data-driven insights and strategic action, helping organizations set strategies, embed sustainability, and address disclosure and regulatory requirements. The collaboration focuses on providing organizations with rapid access to data, enhancing insights, and understanding options for accelerated action toward climate and sustainability goals.

IBM, a leading key player in the Big Data market, and Meta have jointly launched the AI Alliance, an international community of leading technology developers, researchers, and adopters collaborating to advance open, safe, and responsible AI. The alliance includes over 50 founding members and collaborators globally, such as AMD, CERN, Dell Technologies, Linux Foundation, Oracle, Sony Group, and many others. The AI Alliance aims to support open innovation and open science in AI, fostering collaboration among various institutions to shape AI evolution. The AI Alliance focuses on creating opportunities for AI researchers, builders, and adopters to empower them with information and tools for harnessing advancements in ways that prioritize safety, diversity, economic opportunity, and benefits to all. The alliance aims to accelerate responsible innovation in AI by enabling developers and researchers to work collaboratively on open initiatives that address safety concerns and provide a platform for sharing and developing solutions.

Informatica, a global Big Data market player, and Oracle have strengthened their strategic collaboration, enhancing the partnership with the creation of an Oracle Cloud Infrastructure (OCI) point of delivery for thousands of joint customers in North America. The collaboration includes new integrations and capabilities for Informatica’s Intelligent Data Management Cloud (IDMC) across Oracle’s Modern Data Platform. IDMC offers an integrated suite of capabilities, providing clean, secure, and trusted data to empower AI/ML utilization and accelerate modernization journeys. As a cloud-native, AI-powered data management platform, IDMC offers shared Informatica-Oracle customers a common data management experience with consistent governance across cloud and on-premises architectures. The collaboration is designed to deliver a seamless and integrated experience for customers, simplifying the entire data lifecycle and ensuring data governance across various environments.

Microsoft, a major Big Data market share holder, has prolonged its partnership with Oracle to bring customers' mission-critical database workloads to Azure. This expansion enables Oracle's 430,000 customers to apply Microsoft cloud services to Oracle's mission-critical databases. Azure becomes the only cloud provider, aside from Oracle Cloud Infrastructure, hosting Oracle services, including Oracle Exadata Database Service and Oracle Autonomous Database on Oracle Cloud Infrastructure in Azure data centers.

This collaboration addresses the needs of customers moving critical data environments to the cloud, offering seamless connectivity to new and massive-scale cloud services. The joint effort aims to reduce common hurdles faced by customers during workload migrations to the public cloud. The new offering, Oracle Database Azure, allows customers to migrate Oracle databases "as is" to Oracle Cloud Infrastructure and deploy them in Azure alongside their current workloads in the Microsoft Cloud. Customers, including Fidelity, PepsiCo, Vodafone, and Voya Financial, have expressed interest in this solution, highlighting its relevance across various industries

Global Big Data Market Scope: Inquire before buying

| Big Data Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 274.4 USD Bn |

| Forecast Period 2026-2032 CAGR: | 12.4% | Market Size in 2032: | 621.94 USD Bn |

| Segments Covered: | By Component | Hardware Software Services |

|

| by Deployment Mode | On-premise Cloud-Based |

||

| by Industry Vertical | BFSI Manufacturing Healthcare Government Energy & Utilities Transportation Retail & E-commerce IT & Telecom Education Others |

||

| by Application | Customer Analytics Supply Chain Analytics Marketing Analytics Pricing Analytics Spatial Analytics Workforce Analytics Risk & Credit Analytics Transportation Analytics |

||

Global Big Data Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Big Data Market, Key Players:

1. SAP SE (Germany)

2. Microsoft Corporation (United States)

3. Oracle Corporation (United States)

4. IBM Corporation (United States)

5. Amazon Web Services, Inc. (United States)

6. Google LLC (United States)

7. Hewlett Packard Enterprise Development LP (United States)

8. TIBCO Software Inc. (United States)

9. Teradata Corporation (United States)

10. Fair Isaac Corporation (United States)

11. Atos SE (France)

12. Capgemini SE (France)

13. Software AG (Germany)

14. Cloudera, Inc. (United Kingdom)

15. Alibaba Group Holding Limited (China)

16. Tata Consultancy Services Limited ( (TCS) (India)

17. Huawei Technologies Co., Ltd. (China)

18. Baidu, Inc. (China)

19. NEC Corporation (Japan)

20. SAS Institute Inc. (United Arab Emirates)

21. Teradata Corporation (South Africa)

22. Cloudera, Inc. (Brazil)

23. KSOLVES

24. Databricks, Inc. (United States)

25. Palantir Technologies (United States)

26. Qlik Technologies Inc. (United States)

27. Splunk Inc. (United States)

28. MongoDB, Inc. (United States)

29. Domo, Inc. (United States)

30. Others