Hybrid Cloud Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

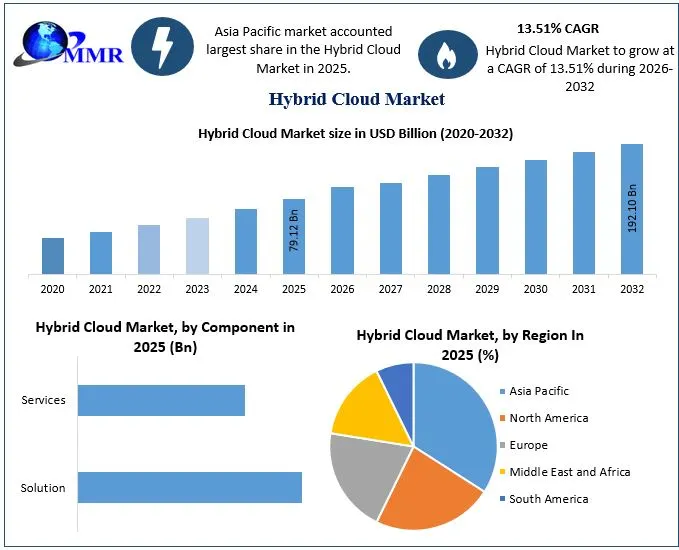

The hybrid cloud market size was valued at US$ 79.12 Bn. in 2025, and the total Hybrid Cloud revenue is expected to grow at 13.51% from 2026 to 2032, reaching nearly US$ 192.10 Bn.

Hybrid Cloud Market Overview:

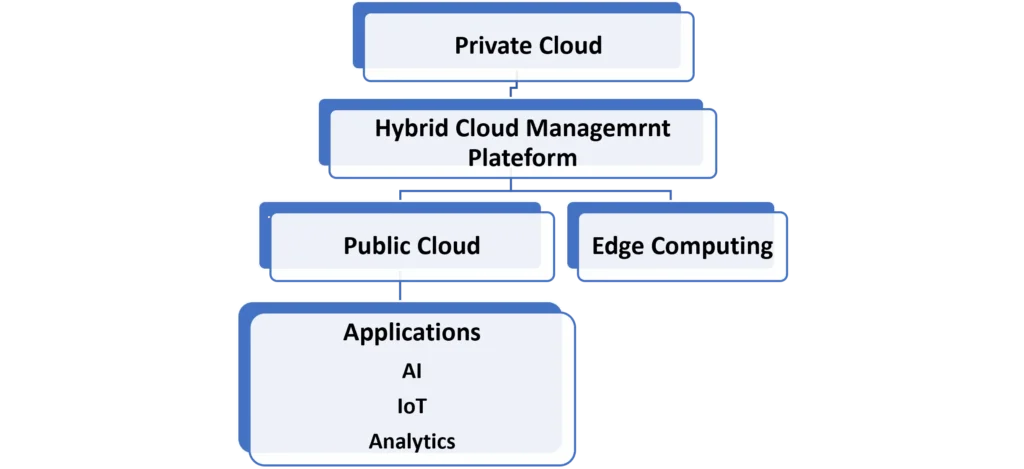

Hybrid cloud is an IT infrastructure that combines private and public cloud infrastructure to construct a setup for an organization. This architecture helps an organization to manage its workload, applications, and data across multiple environments seamlessly. This Hybrid cloud setup brings accuracy while balancing performance, scalability, and cost efficiency. The increasing adoption of digital transformation initiatives with AI-based applications, cloud computing, edge computing, and cloud native architectures is accelerating the demand for hybrid cloud services among organizations to manage their daily tasks with proficiency and efficiency.

Organizations are increasingly adopting this hybrid cloud architecture to manage their mission- critical workload, data sovereignty while complying with regulations. Organizations which operates under highly regulated environment such as banking, financial services and insurance (BFSI), healthcare, government, manufacturing, retail, and telecommunications rely on hybrid cloud infrastructure to maintain data security under highly sensitive environment while leveraging scalability and flexibility of public cloud services. The growing adoption of multi-cloud strategies, containerization technologies, Kubernetes orchestration, DevOps practices, and Infrastructure-as-a-Service (IaaS) is further strengthening the hybrid cloud ecosystem.

Technological advancement are also transforming a market through the integration of artificial intelligence (AI), machine learning (ML), edge computing, Internet of Things (IoT), automation, and zero-trust security frameworks. Enterprises are incorporating hybrid cloud infrastructures to gain support in real-time analytics, disaster recovery, business continuity, application modernization, and AI model training. Additionally, innovations in cloud management platforms, software-defined networking (SDN), hyperconverged infrastructure (HCI), and cloud-native application development are enabling seamless workload portability and centralized management across distributed environments.

To know about the Research Methodology: Request Free Sample Report

To know about the Research Methodology: Request Free Sample Report

Hybrid Cloud Market Segment Analysis:

Hybrid Cloud Market Recent Developments:

| Date | Recent Development |

| 19 Jun 2025 | Microsoft expanded its Azure Local and Azure Arc capabilities, which are enabling enterprises to manage on-premises, edge, and multi-cloud environments through a unified hybrid cloud platform with enhanced AI integration. |

| 08 Apr 2025 | Google Cloud introduced new Gemini AI capabilities across Google Distributed Cloud, helping organizations deploy generative AI applications securely in hybrid and air-gapped environments. |

| 20 Mar 2025 | IBM enhanced its hybrid cloud platform through expanded Red Hat OpenShift AI capabilities, enabling enterprises to deploy and manage AI workloads consistently across hybrid cloud infrastructures. |

| 03 Dec 2024 | Amazon Web Services (AWS) announced new AWS Outposts enhancements, providing improved storage, compute, and networking capabilities for customers running hybrid cloud applications with low-latency requirements. |

| 21 Nov 2024 | Oracle expanded Oracle Cloud Infrastructure (OCI) Dedicated Region and Distributed Cloud offerings, enabling organizations to deploy cloud services within customer data centers while meeting strict regulatory and data residency requirements. |

Hybrid Cloud Market Competitive Landscape:

The Global Hybrid Cloud Market is highly competitive and innovation-driven. This market is heavily depends on the presence of hyperscale cloud providers, enterprise software companies, IT infrastructure vendors, cybersecurity providers, and cloud management platform specialists. Leading market participants are focusing on expanding their hybrid cloud portfolios through strategic partnerships, acquisitions, joint ventures, and continuous investments in research and development. Companies are increasing the deployment of hybrid and multi-cloud platforms, cloud-native application environments, container orchestration solutions, edge computing infrastructure, AI-enabled cloud operations, and zero-trust security architectures to improve workload portability, operational agility, scalability, and data security. In addition, advancements in artificial intelligence (AI), machine learning (ML), Kubernetes, DevOps automation, software-defined networking (SDN), hyperconverged infrastructure (HCI), and confidential computing are enabling intelligent cloud management, predictive infrastructure optimization, automated compliance monitoring, and seamless integration across public cloud, private cloud, and on-premises environments.

Major companies including Microsoft Corporation, Amazon Web Services (AWS), Google Cloud, IBM Corporation, Oracle Corporation, Hewlett Packard Enterprise (HPE), Dell Technologies, VMware LLC (Broadcom), Cisco Systems, Inc., and Nutanix, Inc. are strengthening their market positions through technological innovation, strategic collaborations, and expansion of global cloud and edge infrastructure. These companies are investing heavily in AI-powered cloud management platforms, hybrid cloud orchestration, distributed cloud services, edge-to-cloud integration, cybersecurity solutions, and industry-specific cloud offerings. They are constantly focusing on enhancing data sovereignty, regulatory compliance, and sustainability capabilities.

Strategic collaborations with enterprises, telecom operators, system integrators, managed service providers, and government agencies are able to make faster deployment of integrated hybrid cloud environments and supporting the growing demand for secure, scalable, and intelligent digital infrastructure across industries such as BFSI, healthcare, manufacturing, retail, telecommunications, and the public sector.

Hybrid Cloud Market Scope: Inquire before buying

| Hybrid Cloud Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | US$ 79.12 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 13.51% | Market Size in 2032: | US$ 192.10 Bn. |

| Segments Covered: | By Component | Solution Services |

|

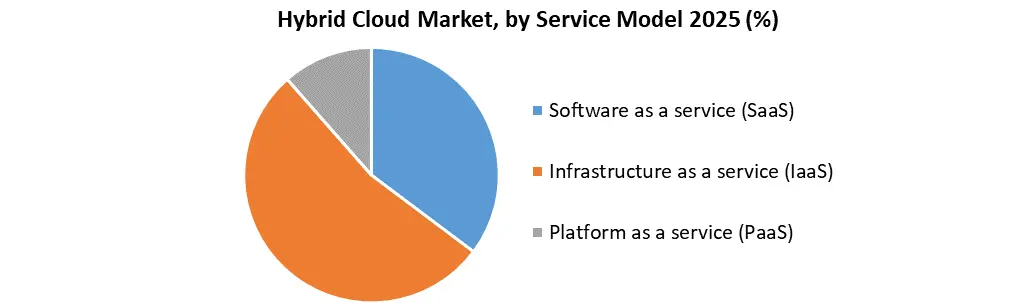

| By Service Model | Software as a service (SaaS) Infrastructure as a service (IaaS) Platform as a service (PaaS) |

||

| By Organization Size | Large enterprises Small and medium enterprises |

||

| Bby Industry Vertical | IT & Telecom Healthcare BFSI Retail Government Media & entertainment Transportation & Logistics Manufacturing Others |

||

Hybrid Cloud Market, by Region:

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

North America

- Microsoft Corporation (United States)

- Amazon Web Services (AWS) (United States)

- Google Cloud LLC (United States)

- IBM Corporation (United States)

- Oracle Corporation (United States)

- Hewlett Packard Enterprise (HPE) (United States)

- Dell Technologies Inc. (United States)

- Cisco Systems, Inc. (United States)

- Nutanix, Inc. (United States)

- NetApp, Inc. (United States)

- Equinix, Inc. (United States)

- Rackspace Technology, Inc. (United States)

- Pure Storage, Inc. (United States)

- Red Hat, Inc. (United States)

- VMware LLC (Broadcom) (United States)

Europe

- Atos SE (France)

- OVHcloud (France)

- SAP SE (Germany)

- T-Systems International GmbH (Germany)

- Deutsche Telekom AG (Germany)

- Fujitsu Services Ltd. (United Kingdom)

- Orange Business (France)

- Capgemini SE (France)

- Ericsson AB (Sweden)

- Nokia Corporation (Finland)

Asia-Pacific

- Alibaba Cloud (China)

- Huawei Technologies Co., Ltd. (China)

- Tencent Cloud (China)

- Fujitsu Limited (Japan)

- NTT DATA Group Corporation (Japan)

- NTT Communications Corporation (Japan)

- NEC Corporation (Japan)

- Hitachi Vantara (Japan)

- Samsung SDS Co., Ltd. (South Korea)

- KT Cloud Corporation (South Korea)

Middle East & Africa

- e& enterprise (United Arab Emirates)

- stc Group (Saudi Arabia)

- Ooredoo Group (Qatar)

- G42 Cloud (United Arab Emirates)

- Liquid Intelligent Technologies (South Africa)

Others

Frequently Asked Questions:

1. What is the growth rate of Hybrid Cloud Market?

Ans. The Global Hybrid Cloud Market is growing at a CAGR of 13.51% over forecast period.

2. Which region has largest share in The Global Hybrid Cloud Market?

Ans. North America holds the largest share.

3. What is the Global Hybrid Cloud Market segment based on Industry Vertical?

Ans. Based on Industry Vertical, The Global Hybrid Cloud Market is divided into IT & Telecom, Healthcare, BFSI, Retail, Government, Media & entertainment, Transportation & Logistics, Manufacturing, Others.

4. Who are the key players in the Global Hybrid Cloud Market?

Ans. The key players in the Global Hybrid Cloud Market are VMware, Inc. Rackspace Inc.,Hewlett Packard Enterprise, Dell EMC, IBM Corporation, Google LLC, Verizon Enterprise,Cisco Systems, Inc., AWS, Oracle, Alibaba, Equinix, NetApp, Atos, Fujitsu. CenturyLink