HVDC Transmission Market Size by Component, Technology, Transmission Type, Application, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2032

Overview

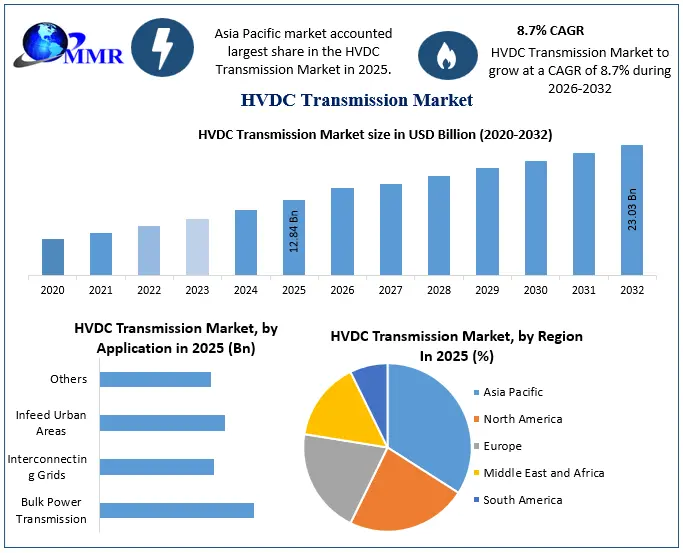

Global HVDC Transmission Market size was valued at USD 12.84 Bn in 2025 and is expected to reach USD 23.03 Bn by 2032, at a CAGR of 8.7 %.

Overview

HVDC (High-Voltage Direct Current) transmission is a method of transmitting electrical power over long distances using high-voltage direct current instead of alternating current. This approach offers several advantages over traditional AC transmission, such as reduced line losses, increased transmission capacity, and the ability to interconnect power systems and integrate renewable energy sources. Also, HVDC transmission systems are cheap for long-distance electricity transmission & they also produce lower electrical losses. High voltage direct current systems allow transmission of power generated from solar panels & wind plants which are far away.

The interconnection of High voltage direct current & the Alternative Current grid has strengthened the reliability & capacity of power grids. Rising electricity consumption is one of the main factors driving the global HVDC transmission market. The populace is rising rapidly, thereby growing electricity consumption. More & more electrically powered devices are currently being used. Fossil fuels & CO2 emissions are being replaced by new technologies which is also the reason for higher electricity consumption.

The rising need for cable-based transmission as an alternative to transmission through overhead lines is the other influence responsible for the development of the global HVDC transmission market. Overhead transmission lines are not protected & hence the threat to human safety is high. Cable-based transmission lines need insulation so that the live cables do not touch the earth & get shorted, & hence the acceptance of cable-based transmission lines is growing, thereby improving the development of the HVDC transmission Industry.

To know about the Research Methodology :- Request Free Sample Report

HVDC Transmission Market Dynamics

Interconnection of Power Grids to Boost the Market

POWERGRID is committed to operating sustainably and has been taking proactive steps for the HVDC Transmission Market as a sustainability initiative. POWERGRID has set a target for meeting 50% of its internal energy needs from renewable sources by 2025 and achieving net zero status by 2047. As of December 2023, the installation of 8.7 MWp rooftop solar PV systems at more than 110 locations is completed and about 10.1 MWp Projects are under implementation/planning. POWERGRID’s first large-scale commercial project for the establishment of an 85 MW Solar PV project at Nagda is under development and is likely to be commissioned in June 2024. Additionally, to, reduce the consumption of diesel use in the organization, diesel vehicles are replaced with Electrical Vehicles (EVs).

The interconnection of regional and international power grids is a significant factor driving the HVDC transmission market. HVDC links enable the exchange of electricity between different grids, enhancing grid stability and reliability. They allow countries to trade power, balance supply and demand, and optimize resource utilization. This interconnectivity is essential for creating a resilient and flexible global power network, capable of withstanding fluctuations in generation and consumption. As countries aim for energy security and the integration of renewables, HVDC interconnections are becoming increasingly vital.

The US grid system is a complex machine consisting of several moving parts more than 3300 utilities, 7700 power plants, and 160,000 miles of high voltage transmission lines. At the local level, any grid has generators that produce energy transmission lines that transfer high-voltage energy to the distribution system. These distribution systems comprise substations that convert and distribute lower-voltage power transformers. These reduce voltage further before the electricity finally reaches our homes.

Government initiatives and investments play a crucial role in the growth of the HVDC transmission market. Many governments are investing in HVDC projects to modernize their power infrastructure, reduce transmission losses, and support renewable energy targets. Policies and incentives aimed at promoting clean energy and grid modernization are encouraging the adoption of HVDC technology. Additionally, international collaborations and funding from development banks for cross-border HVDC projects are further driving market expansion, facilitating the development of a sustainable and interconnected global power network.

Smart Grid Initiatives: US Department of Energy - ARRA Smart Grid Project, Includes Advanced Metering Infrastructure, smart meters, customer interface systems, and renewable energy integration projects. Focuses on harnessing solar power in the MENA region to meet local and European energy demands. This $10.5 billion program will assist the nation in enhancing grid flexibility and improving the resilience of the power system against growing threats of extreme weather and climate change. The goals of the GRIP program are transforming community, regional, interregional, and national resilience, particularly in consideration of future shifts in generation and load; catalyzing and leveraging the private sector and non-federal public capital for impactful technology and infrastructure deployment; and advancing community benefits.

US Government Funding Under the Program Divided across Three Subprogrammes:

| Grip Program | Total Funding (FY 2022-26) in Billion | Purpose |

| Grid Resilience Utility and Industry Grants | 2.5 | Focuses on funding comprehensive transmission and distribution technology solutions to mitigate hazards, including extreme weather events. |

| Grid Innovation Program | 5.0 | Provides financial assistance to states, tribes, local governments, and public utility commissions for collaborative projects to enhance grid resilience and reliability through innovative approaches. |

| Smart Grid Grants | 3 | Aims to increase transmission capacity through grid-enhancing technologies (GETs); mitigate wildfires; enable electrification of edge devices for better load management; and incorporate secure communications and cybersecurity. |

Other Federal Initiatives Include funds from the Inflation Reduction Act ($3 billion), fast-tracking permitting for key transmission lines, and next-generation transmission planning studies (e.g., National Transmission Planning Study, Atlantic Offshore Wind Transmission Study). Such factors are expected to boost the HVDC Transmission Market growth.

Technological Advancements in HVDC Transmission to Drive the Market Growth

Technological advancements in HVDC systems are pivotal in driving HVDC Transmission Market growth. Innovations in converter technologies, cable design, and insulation materials have significantly improved the efficiency and reliability of HVDC transmission. Modern HVDC systems offer lower transmission losses, higher capacity, and the ability to connect asynchronous power grids, making them highly attractive for long-distance and underwater power transmission. The advancements in power electronics and control systems enhance the stability and flexibility of HVDC networks, supporting the integration of renewable energy sources and facilitating the development of smart grids. For instance, total grid investments have averaged USD 450bn/year in the past decade. The expansion of renewable power leads to a steady increase in grid investments, reaching levels of USD 500bn/year in the 2030s, and growing up to USD 1.1trn/year by 2050. Measured by circuit kilometres, transmission, and distribution lines will almost triple during our forecast period.

Renewable Energy Integration to Create Opportunity for the Market

The rise of renewable energy sources such as wind, solar, and hydropower has created a significant opportunity for High Voltage Direct Current (HVDC) transmission and to boost the HVDC Transmission Market growth. HVDC technology is particularly advantageous for integrating these intermittent energy sources into the grid due to its ability to efficiently transmit power over long distances with minimal losses. This is crucial for connecting remote renewable energy farms to urban centers where the demand is highest. Also, HVDC systems help balance supply and demand by interconnecting different regions and enabling the sharing of excess renewable energy, thereby enhancing grid stability and reducing reliance on fossil fuels. HVDC is preferred for long-distance transmission due to lower line losses (around 2%).

Existing HVDC projects in India are integrated into the proposed smart grid. India's renewable energy capacity, particularly wind and solar power, is integrated into the smart grid to enhance energy sustainability. India's energy demand is rising rapidly. Despite being the world's 6th largest energy consumer, India faces significant transmission and distribution losses (15-20%). The adoption of HVDC and smart grid technologies addresses these inefficiencies. As a result, this factor is expected to increase the HVDC Transmission Market size growth. A central HVDC backbone will form the core of the Indian power network, integrating energy from conventional and renewable sources. The system will feature smart metering and two-way communication for real-time energy monitoring and control. Implementing a smart grid with HVDC transmission and renewable microgrids can significantly improve the efficiency, reliability, and stability of India's power sector.

The world’s capacity to generate renewable electricity is expanding faster than at any time in the last three decades, giving it a real chance for HVDC Transmission Market growth to achieve the goal of tripling global capacity by 2030. The amount of renewable energy capacity added to energy systems around the world grew by 50% in 2023, reaching almost 510 gigawatts (GW), with solar PV accounting for three-quarters of additions worldwide. The largest growth took place in China, which commissioned as much solar PV in 2023 as the entire world did in 2022, while China’s wind power additions rose by 66% year-on-year. The increases in renewable energy capacity in Europe, the United States, and Brazil also hit all-time highs.

Economically, HVDC systems offer cost savings over AC transmission for long-distance and high-capacity applications due to lower transmission losses and reduced infrastructure costs. The economic and environmental benefits of HVDC transmission are significant drivers of HVDC Transmission Market growth. Environmentally, HVDC transmission supports the integration of renewable energy sources, helping to reduce greenhouse gas emissions and reliance on fossil fuels. These benefits align with global efforts to combat climate change and promote sustainable development, making HVDC technology an attractive choice for utilities and governments worldwide.

Requirement of High Initial Capital Investment to Restrain the Market Growth

One of the primary restraining factors for the HVDC transmission market is the significant initial capital investment required. Establishing HVDC transmission systems involves considerable expenses in building converter stations, which are critical for converting alternating current (AC) to direct current (DC) and vice versa. These stations incorporate advanced technology and specialized equipment, leading to high costs. The development of HVDC lines, which span vast distances, requires substantial financial outlays. Such significant upfront investments are a deterrent for many stakeholders, including utility companies and governments, especially in regions with limited financial resources. This financial barrier delays project approvals and implementations, slowing down the overall HVDC Transmission Industry growth despite the long-term efficiency and cost benefits HVDC systems offer over traditional AC systems.

HVDC Transmission Market Segment Analysis

By Technology:

Based on technology, the Line Commutated Converter (LCC) segment held the largest global HVDC transmission market share in 2025. High‐voltage direct current (HVDC) systems are becoming more and more common in modern power systems. This chapter introduces line‐commutated current source converter (LCC) HVDC transmission systems and discusses AC and DC protection schemes for these systems. It focuses on the two‐terminal LCC HVDC system, consisting of two converter stations, one controlled to operate as a rectifier and the other operating as an inverter, connected by a DC transmission line. The high efficiency, reliability, and cost-effectiveness. LCCs are preferred for transmitting bulk power over larger distances. The LCC technology is advanced and has been used for many years, making it a reliable option.

By Transmission Type:

Based on transmission type, the overhead HVDC transmission lines experience lower electricity losses compared to high voltage alternating current (HVAC) lines, particularly over long distances. This makes HVDC an ideal choice for transmitting electricity from remote power generation sources such as offshore wind farms. HVDC transmission systems typically include converter stations at each end of the line, where AC electricity is converted to DC for transmission and then back to AC at the receiving end. These converter stations are often situated near the overhead transmission lines. Such factors are expected to drive the segment growth in HVDC Transmission Market.

HVDC Transmission Market Regional Analysis

Asia Pacific held the largest HVDC Transmission Market share in 2023. The regional growth is driven by rapid urbanization, a key factor in the region's socioeconomic landscape. Massive population growth and migration to cities demand a shift in energy infrastructure planning. As urban centers expand, the need for dependable, high-capacity power transmission drives the adoption of HVDC technology, which is essential for modern urban development. The rapid development of both conventional and renewable power plants highlights Asia-Pacific's pivotal role in expanding the global HVDC transmission industry. Rising energy demands due to urbanization, industrialization, and improved living standards push governments and utilities to boost and diversify power production.

HVDC transmission efficiently connects remote generation facilities, such as hydroelectric dams, solar farms, and wind parks, to urban and industrial centers, overcoming traditional AC line limitations. Thus, Asia-Pacific is set to lead the HVDC transmission industry, driven by urbanization, smart city proliferation, industrialization, and power generation growth. This region’s demand for HVDC systems will confirm its role in energy transmission innovation and growth.

HVDC Transmission Market Scope: Inquire before buying

| HVDC Transmission Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 12.84 USD Billion |

| Forecast Period 2026-2032 CAGR: | 8.7% | Market Size in 2032: | 23.03 USD Billion |

| Segments Covered: | by Component | Converter Stations Transmission Cables Others |

|

| by Technology | Capacitor Commutated Converter Voltage Source Converter Line Commutated Converter Others |

||

| by Transmission Type | Submarine Overhead Underground |

||

| by Project Type | Point-to-Point Transmission Back-to-Back Stations Multi-Terminal Systems |

||

| by Application | Bulk Power Transmission Interconnecting Grids Infeed Urban Areas Others |

||

HVDC Transmission Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

HVDC Transmission Key players

1. Siemens Energy

2. ABB Ltd.

3. General Electric (GE Vernova)

0. Hitachi Energy

5. Mitsubishi Electric

6. Toshiba Corporation

7. Nexans

8. NKT A/S

9. Prysmian Group

10.Sumitomo Electric

11.Schneider Electric

12.TBEA Co., Ltd.

13.LS Cable & System Ltd.

14.ZTT Group

15.Furukawa Electric Co., Ltd.

16.Hyosung Heavy Industries

17.Bharat Heavy Electricals Ltd. (BHEL)

18.CG Power and Industrial Solutions

19.Taihan Cable & Solution Co., Ltd.

20.XD Group

21.Hydro‑Québec

22.Xu Ji Group Co., Ltd.

23.KEI Industries Ltd.

24.Polycab India Ltd.

25.Brugg Kabel AG

26.Southwire Company

Frequently Asked Questions:

1] What is the growth rate of the Global HVDC Transmission Market?

Ans. The Global HVDC Transmission Market is growing at a significant rate of 8.7 % during the forecast period.

2] Which region is expected to dominate the Global HVDC Transmission Market?

Ans. APAC is expected to dominate the HVDC Transmission Market during the forecast period.

3] What is the expected Global HVDC Transmission Market size by 2032?

Ans. The HVDC Transmission Market size is expected to reach USD 23.03 Bn by 2032.

4] Which are the top players in the Global HVDC Transmission Market?

Ans. The major top players in the Global HVDC Transmission Market are ABB, Siemens, General Electric and others.

5] What are the factors driving the Global HVDC Transmission Market growth?

Ans. The growth of smart grid and renewable energy projects is expected to drive the HVDC Transmission Market growth.

6] Which country held the largest Global HVDC Transmission Market share in 2025?

Ans. China held the largest HVDC Transmission Market share in 2025.