Humanoid Robots Market: Global Industry Analysis, Size, Share, Growth & Forecast (2025–2032): by Component, Application, End-User, and Region

Overview

| $2.92B

Market Size 2025 |

$29.57

Forecast 2032 |

39.2%

CAGR 2025–2032 |

$60T+

Long-Run Labor TAM |

Humanoid Robot Market Overview — The $60 Trillion Inflection Point

The humanoid robot market was valued at USD 2.92 billion in 2025 and is expected to reach USD 29.57 billion by 2032, growing at a CAGR of 39.2%. The market is driven by rising labor shortages, advancements in AI, and increasing automation across industries such as manufacturing, logistics, and healthcare. Humanoid robots are emerging as a key solution for workforce transformation, offering cost-efficient and scalable alternatives to human labor.

Japan loses 18% of its working-age population by 2040. South Korea, 15%. Germany, 12%. China — which built its economic identity on cheap, abundant labor — faces a 9% decline. No immigration policy, no productivity optimization, no fiscal stimulus can bridge a gap of this structural magnitude. Humanoid robots are not a preference. For these economies, they are becoming a necessity.

Humanoid robotics sits at the convergence of three unstoppable forces: the generative AI revolution, a global labour scarcity crisis, and decades of accumulated advances in precision mechanics. The result is an industry that is moving from lab curiosity to factory floor to living room faster than any prior robotics wave.

The Defining Humanoid Robot Market Insight

Humanoid robots are the only scalable interface to a $60 trillion global labor market — because the world was already built for the human form factor. NVIDIA CEO Jensen Huang stated it plainly: "The easiest robot to adapt into the world is the humanoid robot because we built the world for us." That observation is the entire investment thesis.

| $2.92B

Market Size 2025 |

$29.57

Forecast 2032 |

39.2%

CAGR 2025–2032 |

62.7Mn

US Humanoid TAM (units, 2050) |

5,688

China Patents Filed (5yr) |

| $60T+

Total Addressable Market Global Labor Displacement TAM |

$240B

US Market Revenue (2040) From ~$4B in 2030 |

7.4M

Global Units by 2035 China alone; 62M by 2050 (US) |

8% CAGR

Avg Selling Price Decline From $150K → $50K by 2040 |

To know about the Research Methodology :- Request Free Sample Report

Why This Growth Is Non-Discretionary (Highlights)

• The demographic clock cannot be paused. The 1.5 billion people who will be aged 65+ by 2050 are already alive.

• Feed-to-need economics are turning. At $20K BOM (Tesla's 2027–28 target), a humanoid delivers positive ROI vs. a $59,000/year US manufacturing worker within 18–24 months.

• Generative AI has crossed the threshold. Foundation models now enable robots to learn dexterous tasks through imitation and simulation — not years of manual programming.

• Governments are accelerating, not regulating away. Japan, Singapore, South Korea, and China are actively subsidizing deployment, not creating friction.

Humanoid Robot Market Positioning: What This Market Really Is

True Role in the Economy

The humanoid robot market is NOT a commodity market. It is a strategic infrastructure market — analogous to the introduction of electricity, the internet, or the smartphone. Each prior technology wave promised to transform labour; humanoid robotics threatens to replace it at scale. This distinction is critical for market positioning:

• Electricity automated energy delivery → freed human physical effort

• Computers automated information processing → freed cognitive effort

• Humanoid robots automate physical labour + cognitive labour simultaneously → redefines work itself

| Parameter | Commodity Market | Humanoid Robot Market |

| Pricing Power | Low / Price-Taker | HIGH — Technology Premium |

| Switching Cost | Low | Very High (ecosystem lock-in) |

| Demand Driver | Cyclical / GDP-linked | Secular / Structural |

| Margin Profile | 5–15% gross | 30–60%+ (software layer) |

| Value Capture | Distributed | Concentrated at OS/Platform Level |

| Competitive Moat | Scale only | Scale + IP + Data + Brand |

Humanoid Robot Market Segmentation — Where Value Is Creating and Where It is Migrating

By Type: Biped vs. Wheel-Drive — Not a Fair Fight

The biped segment commands the highest CAGR and strategic attention — for one structurally sound reason: the world's infrastructure was designed for two legs. Stairs, narrow aisles, hospital corridors, and home environments all assume bipedal navigation. Wheel-drive robots are cheaper and more stable, but they are permanently capped by built environment constraints.

| Parameter | Biped Humanoid | Wheel-Drive Robot |

| Mobility Environment | Stairs, slopes, uneven terrain, human spaces | Flat, structured, warehouse-optimized |

| Market CAGR | 42–45% (2025–2032) | 22–26% (2025–2032) |

| Primary Use Cases | Caregiving, manufacturing, general purpose | Retail, indoor logistics, customer service |

| BOM Complexity | High — 28–53 actuators, force sensors | Low — simplified drivetrain |

| AI Integration Level | Full multimodal — vision, touch, language | Partial — navigation + language |

| 2025 Market Share | ~61% | ~39% |

| Strategic Winner 2030 | ✓ Biped dominates premium TAM | Coexists in cost-sensitive verticals |

By Application: The Caregiving Segment is Structurally Mispriced

Most market models treat personal assistance and caregiving as one segment among six. This is an analytical error. The caregiving segment carries three advantages no industrial application can match: non-discretionary demand (1.5 billion elderly by 2050), government subsidy tailwinds, and a pricing structure where ROI is unambiguous at $20K robot vs. $60–120K/year human caregiver.

Application Segment CAGR Comparison (2025–2030)

| Personal Assist & Caregiving | ████████████████████████████████ | 4X.8% | ★ Highest |

| Logistics & Warehousing | █████████████████████████████░░░ | X1.2% | |

| Manufacturing & Industrial | ████████████████████████░░░░░░░░ | X3.1% | |

| Research & Space Exploration | █████████████████████░░░░░░░░░░░ | X9.4% | |

| Education & Entertainment | ██████████████████░░░░░░░░░░░░░░ | X5.8% | |

| Public Relations & Retail | ██████████████░░░░░░░░░░░░░░░░░░ | X0.1% | Slowest |

By Offering: Software is the Moat — Hardware Will Commoditize

Hardware constitutes the largest current share (~55% of BOM value). But the margin trajectory is clear: hardware margins will compress 30–40% by 2030 as Chinese manufacturers enter reducers, screws, and motors. Software — the AI foundation model, the motion control OS, the digital twin — will become the irreplaceable, high-margin layer. The company that owns the physical AI operating system owns the future of this market.

By Primary Use Case

| Use Case Segment | 2024 Share of Unveils | Addressable TAM | First Commercial Wave | Margin Potential |

| General Purpose | 56% | Broad — all labour categories | 2027–2030 | MEDIUM (hardware-intensive) |

| Industrial / Logistics | 17% | $800B+ (global warehousing) | 2025–2028 (already starting) | MEDIUM-HIGH |

| Service (Household) | 15% | $200B+ (domestic service) | 2030–2035 | HIGH (recurring services) |

| Research Platform | 12% | N/A (enables other segments) | Ongoing | LOW (grant-funded) |

By Geography — Volume vs. Premium Markets

| Region | Role in Ecosystem | % of Confirmed Players | Competitive Advantage | Risk Factor |

| China & Taiwan | Volume + Manufacturing | 83% confirmed involvement | Cost, supply chain depth, govt support | IP protection, geopolitical |

| USA & Canada | Brain + Platform | 31% confirmed involvement | AI/software leadership, capital markets | Onshoring costs, talent |

| Rest of APAC (Japan/Korea) | Precision Components | 50% confirmed involvement | Reducer/bearing precision excellence | Domestic market size |

| EMEA | Quality + Safety Standards | 25% confirmed involvement | Regulatory expertise, brand premium | Labour protection laws, costs |

By Price Tier

| Price Tier | ASP Range | Target Segment | Example | Competition Level |

| Ultra-Premium | $200K–$300K | Specialized logistics, defense, medical | Agility Digit ($250K) | LOW (few competitors) |

| Enterprise Premium | $X0K–$X00K | Large-scale industrial automation | Figure 02, Atlas (Electric) | LOW-MEDIUM |

| Mid-Market | $X0K–$X0K | Mainstream manufacturing, food processing | Tesla Optimus (target $30–50K) | MEDIUM (growing fast) |

| Mass Market | $X0K–$X0K | General service, household, SME | Unitree G-1 ($16K) | VERY HIGH (China dominant) |

| Consumer (future) | <$X0K | Home use, personal assistant | Not yet available commercially | TBD — potential winner-take-all |

Humanoid Robot Demand Engine: Why Demand Exists & Will Persist

Core Demand Drivers — Structural, Not Cyclical

| Demand Driver | Nature | Time Horizon | Magnitude | Reversibility |

| Global Labour Shortage | Demographic | Permanent | Critical | None |

| Rising Labour Costs (China/US) | Economic | Long-term | High | Low |

| Dangerous Job Substitution | Safety/Regulatory | Medium-term | Moderate | Low |

| GenAI Model Maturation | Technological | Medium-term | Very High | None |

| Precision Manufacturing Demand | Industrial | Long-term | High | Low |

| Elderly Care Crisis (Japan/EU) | Demographic | Permanent | Very High | None |

| e-Commerce Logistics Boom | Economic | Long-term | High | Moderate |

| National Security / Sovereign AI | Geopolitical | Long-term | Moderate | Low |

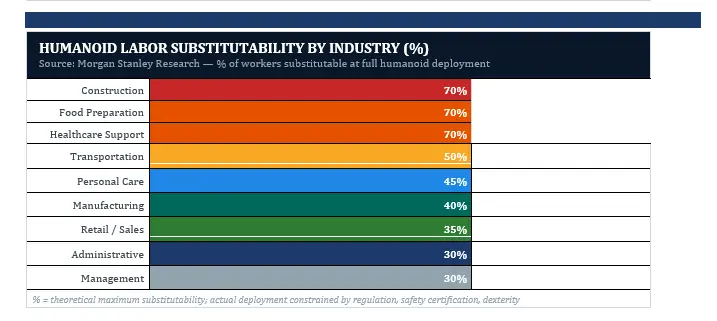

The Labour Market TAM — Humanoidability Analysis

Analysis of 831 US civilian occupations (Bureau of Labor Statistics) reveals the following substitution potential across four tiers:

| Occupation Category | Market Share / Value | Index |

| Construction & Extraction | ██████████████████████████████████ 92% humanoidable → 70% substitutable | ▲ |

| Production (Manufacturing) | ██████████████████████████████████ X1% → 70% substitutable by 2040 | ▲ |

| Food Prep & Serving | █████████████████████████████████░ X8% → 70% substitutable | ▲ |

| Healthcare Support | █████████████████████████████░░░░░ X9% → 70% substitutable | ▲ |

| Transportation & Moving | ██████████████████████████░░░░░░░░ 70% → 50% substitutable | ▲ |

| Sales & Related | █████████████████████░░░░░░░░░░░░░ X8% → 50% substitutable | ▲ |

| Healthcare Practitioners | ███████████████████░░░░░░░░░░░░░░░ 52% → 30% substitutable | ▲ |

| Management | ███████░░░░░░░░░░░░░░░░░░░░░░░░░░░ 20% → 30% substitutable (long-term) | ▲ |

| Computer & Mathematical | ██░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░ 5% → 0% (AI replaces, not humanoid) | ▼ |

Humanoid Robot Market Key Insight — Demand Inelasticity

Unlike consumer electronics (demand falls sharply with price above certain thresholds), humanoid demand is structurally INELASTIC from the employer side. When a robot replaces a $59,428/year US worker at a $50,000 purchase price + $5,000/year maintenance, the ROI is achieved in <13 months. As ASPs decline to $20K (Tesla's target), payback compresses to <5 months. This economic logic is self-reinforcing and irreversible once established.

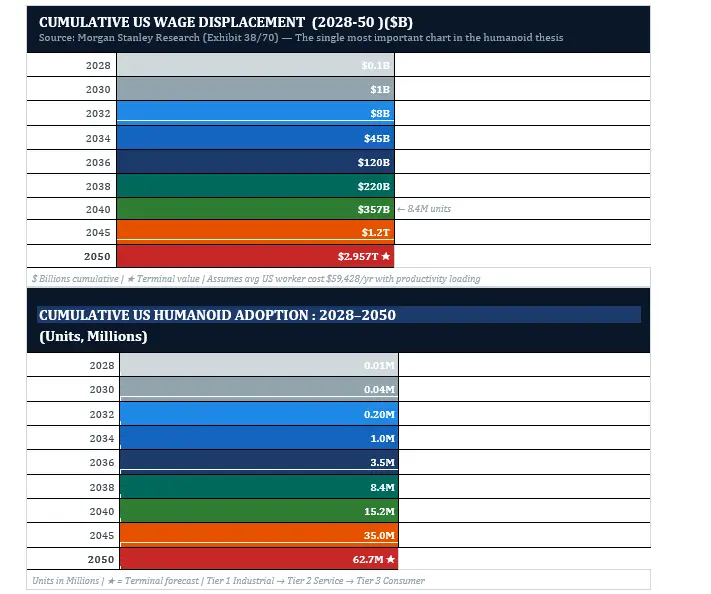

Wage Displacement Model — The $2.957 Trillion Headline

This is the most consequential data in the entire humanoid thesis. The humanoid robot is not a productivity tool — it is a wage substitution vehicle. The cumulative US wage impact reaches $357 billion by 2040 and $2.957 trillion by 2050. This is the number that makes boardrooms take notice.

Humanoid Robot Market Value Chain Intelligence — Brain, Body, and the Bill of Materials

The Brain (AI + semiconductors) captures 60–80% gross margins today. The Body (actuators, sensors, batteries) captures 20–45%. Integrators — the companies building full humanoid robots — currently operate at negative margins, investing to capture the future. This structure will invert by 2030–32 as integrators with proprietary AI operating systems extract platform-level economics.

| Value Chain Layer | Key Components | Margin Today | Margin 2032E | Power Shift |

| Brain — AI Models | Foundation models, sim, NLP | 70–80% | 60–70% | NVIDIA, Google hold; open-source pressure |

| Brain — Compute Chips | GPU, SoC, edge AI, memory | 55–70% | 50–65% | TSMC moat intact; NVIDIA dominant |

| Body — Sensors | 6-axis force/torque, vision, IMU | 45–60% | 35–50% | ATI (Novanta) dominant; China entering |

| Body — Actuators | Harmonic/planetary reducers, motors | 30–45% | 20–30% | Japan leads; China disrupting fast |

| Body — Batteries | Cylindrical Li-ion packs, BMS | 15–25% | 12–18% | CATL dominant; commoditizing |

| Integrators | Full robot + AI OS + deployment | Negative | 5–15% | Tesla, Boston Dynamics race for scale |

The Bom Compression Thesis — The Single Most Important Variable

Tesla Optimus Gen2 carries a $50–60K BOM today. Elon Musk's target: $20K by 2027–28. The path requires three simultaneous breakthroughs: (1) Chinese manufacturers enter force/torque sensors — a Western monopoly worth $20K/unit alone. (2) Planetary roller screw costs drop 60–70% via Chinese volume. (3) Frameless torque motor production scales in China. When BOM crosses $25K, the adoption curve inflects. Monitor this number quarterly.

Tesla Optimus Gen2 — Bom by Component Category ($K Per Unit)

| Force & Torque Sensors | ████████████████████████████████ | 20K |

| Ball / Roller Screws | ██████████████████░░░░░░░░░░░░░░ | 11K |

| Electric Motors | ██████████████████░░░░░░░░░░░░░░ | 11K |

| Gear Reducers | ███████████░░░░░░░░░░░░░░░░░░░░░ | 7K |

| Encoders | ███░░░░░░░░░░░░░░░░░░░░░░░░░░░░░ | 2K |

| FSD Chip + Cameras | ███░░░░░░░░░░░░░░░░░░░░░░░░░░░░░ | 2K |

| Bearings | █░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░ | 0.4K |

| Battery Pack | ░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░ | 0.3K |

Profit Pool Analysis

Value Chain Flow

Humanoid Robot Market Profit Pool Distribution

| Value Chain Stage | Gross Margin Range | Revenue Capture | Value Driver | Risk Level |

| Rare Earth Mining | 15–25% | ~2% of total | Resource scarcity (China controls 85%+) | VERY HIGH (geopolitical) |

| Component Mfg (Body) | 15–35% | ~38% of total | Precision engineering + scale | MEDIUM |

| AI/Software Layer | 50–80% | ~20% of total (growing) | IP, data moat, switching cost | LOW |

| Semiconductors (Compute) | 55–75% | ~8% of total | NVIDIA dominance, architecture lock-in | LOW-MEDIUM |

| Robot Integration (OEM) | 8–25% | ~25% of total | Brand + ecosystem + service | MEDIUM-HIGH |

| After-Market / SaaS | 70–85% | ~7% (growing to 30%) | Recurring revenue, switching cost | LOW |

Profit Pool Migration — Where Value Is Moving

Value is migrating UPWARD (to AI/software) and DOWNSTREAM (to after-market services). Hardware OEMs who fail to build a software moat will be commoditized exactly as PC manufacturers were commoditized by Microsoft and Intel. The race is not to build the best robot body — it is to own the robot operating system.

Humanoid Robot Market Competitive Landscape — Who is Winning, Who is at Risk, and Why

The humanoid competitive landscape is a three-tier war being fought simultaneously across AI software, precision hardware, and full-system integration. The company that wins all three tiers — or controls the interface between them — captures disproportionate long-term value. As of 2025, no single player has achieved this. Tesla is closest.

Full Competitor Matrix

| Company | Country | Robot | Market Segment | Backing / Partner | Key Moat |

| Tesla | USA | Optimus Gen2 | General / Industrial | In-house FSD AI | Vertical integration + proprietary AI OS |

| Boston Dynamics | USA/KR | Atlas Electric | Industrial / R&D | NVIDIA + Hyundai | Locomotion IP; 30+ years of dynamics R&D |

| Agility Robotics | USA | Digit | Logistics | Amazon + NVIDIA | Amazon warehouse deployment; first-mover logistics |

| Figure AI | USA | Figure 02 | General Purpose | NVIDIA + OpenAI + MSFT | Microsoft & BMW backing; rapid capability gains |

| UBTech | China | Walker S1 | Industrial / Service | Baidu + BYD + Nio | China OEM pipeline; BYD/DongFeng supply deals |

| Unitree | China | G-1 | General / Low-Cost | NVIDIA | Price leadership at $16K; volume strategy |

| XPeng | China | Iron | Industrial | NVIDIA + auto platform | Auto engineering synergy; China deployment scale |

| SoftBank (NAO) | Japan | Pepper / NAO | Service / Retail | In-house | Hospital + retail installed base; service brand |

| PAL Robotics | Spain | REEM-C | Research / Healthcare | EU R&D ecosystems | European healthcare regulatory positioning |

| Rainbow Robotics | Korea | RB-Y1 | Industrial | Samsung Electronics | Samsung SDI + semiconductor supply backing |

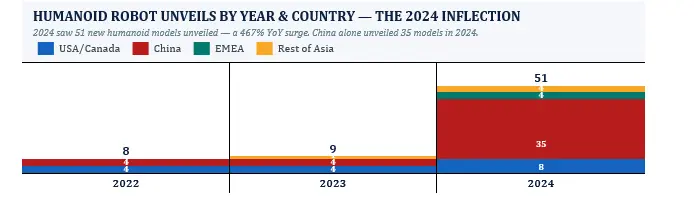

The China Threat: Accept It as Structural, Not Cyclical

73% of confirmed humanoid value chain companies are Asia-based. China filed 5,688 humanoid patents in 5 years vs. the USA's 1,483. Chinese manufacturers already supply BYD and DongFeng with Walker S1 units in production. The EV supply chain parallel is exact: the West ceded battery manufacturing by under-investing in 2015–2020. The same window for humanoid components closes in 2025–2027. Companies with procurement influence must act now.

Competitive Capability Benchmarking

| Player | AI Brain | Locomotion | Dexterity (DoF) | Production Scale | Price Competitiveness | Overall Verdict |

| Tesla (Optimus) | ★★★★★ | ★★★★ | 50 DoF | Pilot → Scale 2025 | $20K target | ★★★★★ Leader |

| Boston Dynamics | ★★★★ | ★★★★★ | 53 DoF | R&D → Industrial | Not disclosed | ★★★★ Leader |

| Agility (Digit) | ★★★ | ★★★★ | 16 DoF | Amazon Production | $250K (2024) | ★★★ Logistics niche |

| Figure AI | ★★★★ | ★★★★ | 53 DoF | Pre-production | N/A | ★★★★ Emerging |

| UBTech Walker S1 | ★★★ | ★★★ | 41 DoF | In Production | N/A | ★★★ China #1 |

| Unitree G-1 | ★★★ | ★★★ | 43 DoF | In Production | $16K | ★★★ Price leader |

P/E Ranking Vs. 3-Year Revenue CAGR — Key Humanoid 100 Names (Cons. 2025)

| Sr. No. | Company | P/E (2025) | 3yr Rev CAGR | Visual PEG Positioning | Investment Verdict |

| 1 | Rainbow Robotics | 782x | 38% | PEG: 20.6x █ | Pure-play optionality. Samsung 35% shareholder. |

| 2 | LeaderDrive | 204x | 85% | PEG: 2.4x ███████████ | Humanoid reducer >10% of Q4 2024 revenue. |

| 3 | Shanghai Beite | 129x | 80% | PEG: 1.6x █████████████ | Rmb 1.85Bn humanoid screw plant announced. |

| 4 | Tesla | 112x | 28% | PEG: 4.0x █████████ | Optimus thesis. Monitor BOM milestones quarterly. |

| 5 | Harmonic Drive | 87x | 22% | PEG: 4.0x █████████ | ~10% of rev from humanoid. 3-4 customers. |

| 6 | NVIDIA | 38x | 45% | PEG: 0.8x ██████████████ | ★ BEST PEG in universe. GR00T + Omniverse. |

| 7 | Arm Holdings | 54x | 30% | PEG: 1.8x ████████████ | SoC design for humanoid compute. |

| 8 | Alphabet (Google) | 23x | 14% | PEG: 1.6x █████████████ | DeepMind robotics. Apptronik partner. |

| 9 | TSMC | 23x | 20% | PEG: 1.1x █████████████ | Leading-edge AI chips for humanoid brain. |

| 10 | Microsoft | 31x | 15% | PEG: 2.1x ████████████ | Figure AI backer. OpenAI embedded. |

| 11 | ABB | 22x | 11% | PEG: 2.0x ████████████ | ★ ATTRACTIVE value. Full robotics stack. |

| 12 | Hyundai (w/BD) | 4x | 12% | PEG: 0.3x ███████████████ | ★★ DEEP VALUE — Boston Dynamics optionality FREE. |

| 13 | Amazon | 38x | 11% | PEG: 3.5x ██████████ | 750K+ robots. Agility Digit deployment. |

| 14 | Meta Platforms | 28x | 11% | PEG: 2.5x ███████████ | Foundation models for robotics. Llama overlap. |

| 15 | Nabtesco | 23x | 8% | PEG: 2.9x ███████████ | Used in 60%+ of global industrial robots. |

| 16 | Jiangsu Hengli | 29x | 25% | PEG: 1.2x █████████████ | Planetary roller screws sent for OEM validation. |

Competitive Landscape Heatmap

Capability Matrix — Top 20 Humanoid-Relevant Companies

| Company | AI/Software | Hardware Mfg | Supply Chain | Capital Access | China Exposure | Commercial Stage |

| NVIDIA | VH | M | VH | VH | M | VH |

| Tesla | H | VH | H | VH | L | H |

| Alphabet | VH | L | M | VH | M | M |

| Microsoft | VH | L | H | VH | M | M |

| TSMC | H | VH | VH | H | VH | VH |

| Samsung | H | VH | VH | VH | H | H |

| Foxconn | M | VH | VH | H | VH | H |

| Harmonic Drive | L | VH | H | M | M | H |

| Nabtesco | L | VH | H | M | L | H |

| CATL | M | VH | VH | H | VH | VH |

| Shenzhen Inovance | M | H | VH | M | VH | H |

| UBTech | H | H | M | M | VH | H |

| Amazon | H | M | VH | VH | M | VH |

| Hyundai/BD | M | VH | H | H | M | M |

| ABB | M | H | H | H | M | H |

| NSK | L | VH | H | M | M | H |

| Nidec | L | VH | H | M | H | H |

| Amphenol | L | H | VH | H | M | VH |

| Novanta | M | H | H | M | L | H |

| Lynas RE | L | M | M | M | L | M |

Legend: VH = Very High | H = High | M = Medium | L = Low | N = Not Applicable

Humanoid Robot Industry Technology & Innovation Landscape

The Four Technology Pillars of Humanoid Advancement

| Technology Pillar | Current State (2025) | Key Breakthroughs Needed | Timeline to Mass Market | Bottleneck Holder |

| GenAI Foundation Models for Robotics | Early stage; models trained on limited physical data | Multi-modal models trained on 10B+ robot-hours of data | 2026–2029 | NVIDIA (GR00T), Physical Intelligence (π0) |

| Actuator Precision & Reliability | 50 DoF achievable; coreless motors still expensive | Planetary roller screws at <$100/unit; coreless at <$20 | 2028–2032 | Japanese/German precision mfg; Chinese ramp-up |

| Battery Energy Density | 2.3 KWh, 52v; 2–4 hour operational life | 4–6 hour operational life; fast-charge <30 min | 2028–2033 | CATL, Samsung SDI, solid-state pioneers |

| Real-Time Simulation (Digital Twins) | NVIDIA Omniverse + Isaac Sim functional but compute-heavy | 1000x simulation speed-up; photo-realistic physics | 2025–2027 | NVIDIA (Omniverse Isaac) |

| Dexterous Manipulation | 20–22 DoF hands; can fold laundry, open doors | Near-human dexterity (27 DoF); tactile feedback integration | 2028–2035 | Tesla (Optimus hands), Physical Intelligence |

| Human-Robot Natural Language Interface | Basic NLP via LLMs; voice commands functional | Real-time natural conversation + context memory | 2025–2027 (near solved via LLMs) | OpenAI, Anthropic, Google |

Drive System Comparison — Electric vs. Hydraulic vs. Pneumatic

| Drive Type | Leading Companies | Pros | Cons | Humanoid Market Share (2025) |

| Electric Drive | Tesla, UBTech, Unitree, Figure, 1X | High precision, fast response, complex motion capable | Power consumption, weight, thermal management | ~85% of all development |

| Hydraulic Drive | Boston Dynamics (legacy) | High torque, fast, handles heavy loads | Complex maintenance, noise, fluid leaks | ~10% (declining) |

| Pneumatic Drive | FESTO, research labs | Clean, low-cost, easy to maintain | Limited torque, not suitable for complex motion | ~5% (niche research) |

Patent Filing Trends — Competitive Intelligence

| Patent Office | 5-Year Count | % Global Share | Trend | Implication |

| China (CNIPA) | 5,688 | 53% | Accelerating strongly | China is building the broadest IP portfolio in body components |

| United States (USPTO) | 1,483 | 14% | Stable + growing | US focused on AI/software patents (higher value) |

| Japan (JPO) | 1,195 | 11% | Stable | Japan protecting precision mechanics heritage |

| WIPO (International) | 1,123 | 10% | Growing | Global companies filing for multi-market protection |

| South Korea (KIPO) | 368 | 3% | Growing | Samsung + Hyundai driving Korean IP buildup |

| EPO (Europe) | 237 | 2% | Slow growth | Europe behind; risk of technology dependence |

Humanoid Robot Market Risk Assessment

Structural Risk Matrix

| Risk Category | Specific Risk | Probability | Impact | Mitigation | Timeline |

| Technology | GenAI models fail to achieve sufficient embodied intelligence | Medium | Very High | Continued R&D; simulation-first approach | 2025–2028 critical window |

| Geopolitical | US-China decoupling severs humanoid supply chains | Medium-High | Very High | Supply chain regionalization; dual sourcing | Ongoing; escalating |

| Regulatory | Safety regulations delay commercial deployment | High | High | Geo-fenced initial deployments; industry standards body | 2026–2030 |

| Economic | High ASP prevents mass-market adoption in critical early phase | Medium | High | Cost reduction roadmap; lease/RaaS models | 2025–2030 |

| Social | Labour displacement backlash creates political headwinds | High | Medium | Upskilling narrative; job creation in new sectors | 2028–2035 |

| Competitive | China wins global market before West builds supply chain | Medium-High | High | Onshoring investment; CHIPS Act equivalents for humanoids | Ongoing |

| Technical | Battery life limits commercial viability for 8-hour shifts | Medium | High | Battery swap stations; energy-dense cell development | 2026–2032 |

| Market | Enterprise customers slow to adopt unproven technology | Medium | Medium | Pilot programs; ROI demonstration; insurance products | 2025–2030 |

Bear Case — What Could Go Wrong

The single biggest risk to the humanoid thesis is not technology — it is timing. If GenAI model accuracy for physical tasks stagnates below 95%+ reliability, enterprise customers will not deploy at scale regardless of unit economics. A 5% error rate translates to roughly one failure per 20 tasks — unacceptable for manufacturing quality control or patient care. The window between 'impressive demo' and 'reliable production tool' is where most robotics companies have historically failed.

Bull Case — What Accelerates the Timeline

The key bull case catalyst is NVIDIA's Project GR00T combined with OpenAI's entry into physical AI. If foundation models for robotics follow the same scaling laws as language models (capabilities doubling every 6–12 months of training compute), we could see commercially viable general-purpose robots by 2027 — 3 years ahead of base case. Tesla's Optimus reaching 10,000 units in 2025 would provide a critical data flywheel that no startup can replicate.

Humanoid Robot Market Regional Strategy Framework

| Region | Role in Ecosystem | Government Policy | Labour Context | Investment Theme | Top Companies |

| United States | AI Brain + Platform + Capital Markets | CHIPS Act, DOD investment in robotics, DARPA | Highest labour costs globally; strong ROI case | AI/software layer; capital allocation to startups | NVIDIA, Tesla, Alphabet, Microsoft, Amazon |

| China & Taiwan | Manufacturing + Volume + Supply Chain | 14th/15th Five Year Plan; local content requirements | Rising costs + massive labour force rebalancing needed | Component manufacturing; vertically integrated OEMs | CATL, Foxconn, Shenzhen Inovance, UBTech, Unitree |

| Japan | Precision Components + Legacy Robotics | Society 5.0; aging population drives demand urgency | Severe aging + labour shortage; most acute globally | Precision parts + reducer/bearing dominance | Harmonic Drive, Nabtesco, NSK, Nidec, Toyota |

| South Korea | Memory + Consumer Electronics + Autos | K-Robotics Strategy 2030 | High labour costs; tech-savvy workforce | Memory chips for AI + autos-to-humanoid crossover | Samsung, SK Hynix, Hyundai, LG Energy, Rainbow |

| Europe (EMEA) | Premium Brands + Safety Standards + Capital | EU AI Act; €2B Horizon Europe robotics funding | Strong labour protection laws; slower adoption curve | Safety/regulatory compliance; precision manufacturing | Siemens, ABB, Schaeffler, Valeo, STMicro, Infineon |

| India | Emerging Demand + Software Talent Pool | National Robotics Mission 2023 | Low labour costs = slower ROI, but massive scale potential | Software development + deployment partner | Addverb (private); potential large market ~2035+ |

Regional Intelligence — Asia Humanoid Robot Market Leads, West Must Respond

| Region | Market Role | CAGR 2025–32 | Key Countries | Government Stance | Strategic Advantage |

| Asia Pacific | Manufacturing + Integration hub | 42–45% | China, Japan, S. Korea, India | Active subsidy; Ministry-level priority | Supply chain depth; labor need; volume |

| North America | AI Brain + Integrator leader | 35–38% | USA, Canada | CHIPS-adjacent; DoD interest | NVIDIA, Google, Tesla; AI model dominance |

| Europe | Component + Regulatory shaper | 28–32% | Germany, Spain, Sweden | EU AI Act; cautious but supportive | ABB, Siemens, SKF; industrial automation base |

| Rest of World | Emerging adopter | 22–26% | India, Middle East, Brazil | Policy frameworks developing | Labor cost crossover driving adoption |

Asia Pacific's CAGR leadership is not simply about manufacturing cost. China alone filed 55% of all global humanoid patents over the past 5 years — a leading indicator of where deployment scale will originate. Japan brings 30 years of precision robotics manufacturing heritage. South Korea's Hyundai, now the majority owner of Boston Dynamics, is the only company in the world that combines automotive scale manufacturing with cutting-edge humanoid locomotion IP.

North America's Strategic Paradox

North America dominates the Brain layer — NVIDIA, Google DeepMind, OpenAI, TSMC's US fabs — which carries 60–80% gross margins. But it imports virtually all Body components from Asia. This is not a 2030 problem. It is a 2025 problem. The company or government that closes this gap first captures the entire value stack.

Humanoid Robot Market Dynamics — Droct Framework

| Dimension | Factor | Market Impact | Intensity |

| Drivers | Generative AI — LLMs now power dexterous manipulation | Collapses R&D cycles from years to months via digital twin training | VERY HIGH ▲▲▲ |

| Demographic decline in key economies (Japan −18%, Korea −15% by 2040) | Creates non-discretionary, sustained demand for labor substitution | VERY HIGH ▲▲▲ | |

| Restraint | BOM at $50–60K blocks mass adoption; $20K target not yet achieved | Limits deployment to institutional buyers; mass consumer market frozen | HIGH ▼▼ |

| Safety standards and liability frameworks lag deployment readiness | Slows healthcare + public space deployment by 2–3 years minimum | HIGH ▼▼ | |

| Opportunity | Eldercare deficit: 1.5Bn people over 65 by 2050; caregiver shortage acute | Opens $3T+ caregiving TAM; government subsidies in Japan, Korea, SG | VERY HIGH ▲▲▲ |

| Logistics e-commerce scale: Amazon, GXO deploying Digit now | First commercial validation at scale; proves enterprise ROI case | HIGH ▲▲ | |

| Challenge | Safety incident risk could trigger regulatory overreach | One publicized injury sets adoption back 18–24 months | MEDIUM ▼ |

| China supply chain concentration creates single-point geopolitical risk | US-China decoupling would disrupt 70%+ of global humanoid BOM | HIGH ▼▼ |

Humanoid Robot Market Strategic Takeaways — Five Verdicts for the Boardroom

| 01. |

| Buy the Brain, Monitor the Body — The AI infrastructure layer (NVIDIA, TSMC, ARM, Google DeepMind) has the highest conviction and lowest execution risk today. Hardware margins will compress 30–40% by 2030. Do not confuse the Body's volume share with its margin future. |

| 02. |

| The $20k Bom Is the Adoption Trigger — When Tesla Optimus BOM crosses below $25K, the consumer and mid-market adoption curve inflects. This is the single most important number in this entire market. Monitor quarterly disclosures. |

| 03. |

| Caregiving is the Killer App — Most models underweight this segment. The demand is non-discretionary, government-subsidized, and demographically locked in. The highest sustained CAGR over a 20-year horizon sits here — not in manufacturing. |

| 04. |

| China Has Already Won the Supply Chain — 73% of the humanoid value chain is Asia-based; 55% of global patents are Chinese. The strategic window to build China-independent component supply is 2025–2027. After that, dependency is structural. |

| 05. |

| This Is A 30-Year Infrastructure Story — Investors who size this as a 5-year market will take profits too early. The correct mental model is the internet (1994–present). Position sizing must account for non-linear adoption curves and extreme inter-year volatility. |

Humanoid Robot Market Key Player Ecosystem:

Brain Companies (Semis + Software)

Foundational AI Models

| Company | Country | Key Product/Initiative |

| NVIDIA | USA | Project GR00T, Omniverse, Jetson |

| Alphabet | USA | DeepMind robotics, partnered Apptronik |

| Microsoft | USA | Azure AI, funded Figure AI |

| Meta | USA | Llama for robotics, tactile sensors |

| Baidu | China | Robotics R&D group, partnered UBTech |

Semiconductor — Compute & Vision

| Company | Country | Primary Role | Competitive Moat |

| NVIDIA | USA | Compute SoC | CUDA ecosystem, GR00T exclusivity |

| Intel | USA | Vision + Compute + Fab | Manufacturing capacity (if restored) |

| Qualcomm | USA | Vision SoC | Mobile architecture reuse |

| Ambarella | USA | Vision SoC | ADAS → humanoid crossover |

| Mobileye | USA | Vision Semis | EyeQ chip + dataset |

| Arm Holdings | UK | SoC Design | Ubiquitous ISA; royalty model |

| TSMC | Taiwan | Fabrication | 2nm process leadership |

| Samsung Electronics | Korea | Memory + Fab + Integration | Vertical integration |

| SK Hynix | Korea | HBM Memory | HBM3 leadership |

| Micron | USA | DRAM + NAND | US-based; CHIPS Act beneficiary |

| Horizon Robotics | China | Vision SoC (China) | China market access |

Simulation & Software

| Company | Role | Competitive Advantage |

| NVIDIA (Omniverse) | Simulation Platform | Photorealistic physics sim; GPU-native |

| Siemens | Industrial Simulation | Full automation stack; digital factory |

| Dassault Systèmes | Digital Twin / PLM | 3DExperience platform; widely used |

| Hexagon | Reality Capture + Sim | Optical sensors + digital sim; Unitree partner |

| Palantir | Data Analytics | AIP platform; Sarcos partnership |

| Oracle | Data + Cloud | Stargate consortium (OpenAI + NVIDIA) |

| Microsoft | Cloud + Dev Tools | Azure AI; GitHub Copilot for robotics dev |

Body Companies (Industrial Components)

Actuators & Actuator Parts — Complete Overview

| Company | Country | Primary Product | Humanoid Involvement |

| NSK | Japan | Bearings + Screws | Linear actuators + bearings for robotics |

| THK | Japan | Screws + Linear Guides | SEED linear actuators for humanoid hands |

| Hiwin Technologies | Taiwan | Ball Screws + Linear Guides | Confirmed Boston Dynamics supplier |

| Jiangsu Hengli | China | Planetary Roller Screws | Screws for humanoid linear actuators (overseas validation) |

| Harmonic Drive Systems | Japan | Harmonic Reducers | ~10% revenue from humanoids; 3–4 humanoid customers |

| Nabtesco | Japan | RV / Precision Reducers | 60%+ of industrial robot reducers globally |

| LeaderDrive | China | Harmonic Reducers | Humanoid >10% of revenue (Q4 2024) |

| Shuanghuan Driveline | China | Gear Reducers | Active humanoid production |

| Hota Industrial | Taiwan | Gears / Reducers | Reportedly pursuing Tesla supply chain |

| Nidec | Japan | Motors + Encoders | Motors for commercial + industrial robots |

| Regal Rexnord | USA | Motors + Gears + Actuators | Full-stack US industrial automation supplier |

| Estun Automation | China | Motors + Own Humanoid | In-house humanoid (Codriod 01) + precision motors |

| Moons' Electric | China | Coreless Motors | Super-hollow shaft stepper for humanoid hands |

| Zhaowei | China | Micro Motors | Humanoid hand motors/actuators |

| Shenzhen Inovance | China | Complete Actuators + Motors | Motor+actuator launch for humanoids 2025 |

| Sanhua | China | Complete Actuators + Thermal | Humanoid-specific actuator business + Tesla auto supplier |

| Tuopu Group | China | Complete Actuators + Thermal | Rmb 1.85M revenue from humanoid samples (2023) |

| Timken | USA | Bearings + Reducers | 'TwinSpin' + 'DriveSpin' actuators for industrial robots |

| RBC Bearings | USA | Precision Bearings | Variety of robot-grade bearings |

| Schaeffler | Germany | Bearings + Linear Guides | Investor + partner of Agility Robotics |

| SKF | Sweden | Bearings + Screws + Seals | Broad industrial bearing portfolio |

Sensors

| Company | Country | Sensor Type | Humanoid Application |

| Novanta (ATI) | USA | 6-Axis Force Sensors | Humanoid wrist/ankle — industry standard |

| Keli Sensing | China | 6-Axis Force/Torque | Showcased at 2024 China Weighing Fair for humanoids |

| Sensata | USA | Multi-sensor | Pressure, position, temperature + motor drivers |

| TE Connectivity | USA | Optical + Force Sensors + Wiring | Full wiring + sensor harness for humanoids |

| Analog Devices | USA | Analog / Motion Control | Motion control + advanced sensing chips |

| Melexis | Belgium | Magnetic Sensors | Designed Tractaxis specifically for industrial humanoid robots |

| Allegro Microsystems | USA | Magnetic + Motor Sensors | Humanoid hand touch sensing + motor control |

| Keyence | Japan | Machine Vision + Optical | Vision + temperature sensors for robotics QC |

| Sony Group | Japan | Cameras + Image Sensors | Image sensors for humanoid vision; QRIO prototype |

| Robosense | China | Lidar + Vision + Controllers | Lidar + cameras designed for humanoids |

| Valeo | France | ADAS / Radar / Lidar | Ultrasonic + radar from automotive ADAS |

| Intel | USA | RealSense Cameras | Depth cameras used on Unitree high-end models |

| Hexagon | Sweden | Optical + Reality Capture | Digital twin + sensor systems; Unitree Series B investor |

| Will Semiconductor | China | CMOS / Vision Sensors | Oct 2024 launched 2MP global shutter sensor for humanoids |

Batteries

| Company | Country | Battery Type | Humanoid Application |

| CATL | China | Cylindrical Li-Ion Cells | Battery packs for humanoid torso (standard reference) |

| EVE Energy | China | Li-Ion Cells | Global supplier; humanoid battery packs |

| Samsung SDI | Korea | Prismatic + Cylindrical Cells | Humanoid battery cells; broad robotics supply |

| LG Energy Solution | Korea | Cylindrical Li-Ion | Supplies Bear Robotics and other robotics cos. |

Body, Wiring, Thermal & Analog Semis

| Company | Country | Primary Product | Humanoid Role |

| Amphenol | USA | Wires + Connectors | Connector harness throughout humanoid body |

| TE Connectivity | USA | Wires + Connectors + Sensors | Full wiring harness + force/optical sensors |

| Aptiv | USA | Wiring + ADAS Sensors | High-voltage distribution from autos → humanoids |

| Magna International | Canada | Aluminum Castings + ADAS | Structural casting + Waymo sensor supply |

| Xusheng | China | Aluminum Castings | Casts Tesla EV parts → potential humanoid body parts |

| Sanhua | China | Thermal + Actuators | Pumps + battery cooling + humanoid thermal mgmt |

| Texas Instruments | USA | Analog Semis | Motor drivers + sensors explicitly for humanoids (marketed) |

| Infineon | Germany | Power + MCU | Motion control ICs + power management |

| NXP Semiconductor | Netherlands | Auto + Robotics MCU | Motion controllers from autos → humanoids |

| STMicroelectronics | Switzerland | Power + Motor Control | Power + motor control in industrial robots |

| Renesas | Japan | MCU / SoC | MCU supply for robotics applications |

| Onsemi | USA | Power + Imaging | Power/sensing for AMRs → humanoids |

| Honeywell | USA | Diversified Automation | AMRs + vision tech + industrial sensing |

| Rockwell Automation | USA | Diversified Automation | Factory integration of humanoid robots |

| Foxconn / Hon Hai | Taiwan | Electronic Components + Mfg | NVIDIA partnership for humanoid development + EMS potential |

| Siemens | Germany | Full Automation Stack | Factory-wide humanoid integration + simulation |

Rare Earths & Magnets

| Company | Country | Product | Humanoid Application |

| JL Mag Rare-Earth | China | NdFeB Permanent Magnets | Motors + actuators in every humanoid |

| Lynas Rare Earths | Australia | Rare Earth Materials | Permanent magnets for high-efficiency motors |

| MP Materials | USA | NdFeB Magnets | Motor magnets; CEO cites humanoid demand explicitly |

| Northern Rare Earths | China | Rare Earth Materials | Motor magnets for Chinese humanoid supply chain |

Integrators (Full Humanoid Developers)

Automotive OEMs Developing Humanoids

| Company | Country | Robot Name | Competitive Advantage |

| Tesla | USA | Optimus Gen 1 & 2 | FSD brain reuse, massive manufacturing scale, Musk's vision |

| Hyundai / Boston Dynamics | Korea | Atlas (Electric) | Boston Dynamics' 30-yr robotics heritage + Hyundai mfg scale |

| XPENG | China | Iron Humanoid | EV AI architecture reuse, strong China government support |

| BYD | China | Yao Shun Yu (internal) | World's largest EV maker; vertical integration masters |

| Toyota | Japan | T-HR3 / Punyo | 100+ years manufacturing expertise, deep robotics research |

| GAC Group | China | GoMate | Chinese govt support, EV supply chain leverage |

Consumer Electronics & Tech Integrators

| Company | Country | Robot / Initiative |

| Apple | USA | Undisclosed (Carnegie Mellon partnership) |

| Xiaomi | China | CyberOne Humanoid |

| Samsung Electronics | Korea | Rainbow Robotics (35% owner) |

| LG Electronics | Korea | Household Humanoid (reported) |

| Sony Group | Japan | QRIO prototype; image sensor supply |

| Foxconn / Hon Hai | Taiwan | NVIDIA partnership for humanoid EMS |

E-Commerce, Internet & Legacy Robotics

| Company | Role | Humanoid Initiative |

| Amazon | E-Commerce + Cloud | 750K+ robots; invested in Agility Robotics (Digit) |

| Alibaba | E-Commerce + Cloud | Invested in Beijing Xingtong Era (humanoid dev co.) |

| Tencent | Internet | Internal robotics lab working on humanoids |

| Naver | Internet | Ambidex Humanoid + robotics division |

| ABB | Legacy Robotics | Full cobot + industrial robot stack |

| Midea / KUKA | Legacy Robotics | KUKA acquisition + embodied R&D |

| Teradyne | Testing Equipment + Cobots | Universal Robots cobot business |

| UBTech | Humanoid Pure Play | Walker series; BYD, DongFeng, NIO partnerships |

| Rainbow Robotics | Humanoid Pure Play | RB-Y1; Samsung 35% shareholder |

Private Humanoid Startups: The Unlisted Universe

The vast majority of pure-play humanoid developers remain private. Investors must track this space for acquisition targets, supply chain disruption, and competitive context.

| Company | Country | Key Robot | Last Valuation | Key Investors | Commercial Status | Key Differentiator |

| Figure AI | USA | Figure 01 / 02 | $2.6B (2024) | OpenAI, Microsoft, NVIDIA, Bezos | Prototype; BMW testing | Fastest-funded US startup; OpenAI AI integration |

| Agility Robotics | USA | Digit | $1.2B (2024) | Amazon (customer+investor) | Limited production ($250K ASP) | Only commercially deployed bipedal robot (Amazon) |

| Physical Intelligence (π) | USA | Software-only (π0 model) | $1.5B (2024) | Bezos, Tiger Global, Khosla | Research + licensing | Foundation model for physical AI — the 'OpenAI of robots' |

| Boston Dynamics | USA | Atlas (Electric) | Part of Hyundai | Hyundai (owns majority) | Prototype; customer testing | 30-year robotics heritage; best motion control |

| 1X Technologies | Norway | EVE / NEO | Undisclosed | OpenAI, Tiger Global | Limited production (EVE for Everon) | European humanoid leader; home robot focus (NEO) |

| Apptronik | USA | Apollo | Undisclosed | Google (DeepMind partner) | Prototype; Mercedes-Benz testing | Google DeepMind partnership for brain |

| Sanctuary AI | Canada | Phoenix | Undisclosed | Magna International investor | In production (general purpose) | Highest DoF (75); cognitive AI focus |

| Fourier Intelligence | China | GR-1 / GR-2 | Undisclosed | Strategic investors | In production | Research-grade + commercial; global distribution |

| Unitree Robotics | China | G-1 / H-1 | Undisclosed | Hexagon (Series B partner) | In production ($16K G-1) | Lowest ASP in market; democratizing humanoids |

| UBTech (partial public) | China | Walker S / S1 | HKEx listed (9880-HK) | BYD, DongFeng, NIO partnerships | In production (industrial) | Only Chinese listed near-pure-play |

Investor Watch — The Acquisition Wave is Coming

As the market matures 2026–2030, we expect a significant M&A wave as large tech companies (Alphabet, Microsoft, Amazon) and industrial conglomerates (Siemens, ABB, Honeywell) acquire private humanoid startups. The most likely targets: Agility Robotics (Amazon already invested), Physical Intelligence (AI-first model is uniquely valuable), and Apptronik (Google partnership suggests acquisition optionality). Investors should monitor Series C/D funding rounds as acquisition precursors.

FAQs:

Q1. What is the size of the humanoid robot market?

Ans: The humanoid robot market was valued at USD 2.92 billion in 2025 and is projected to reach USD 29.57 billion by 2032, driven by AI advancements, automation demand, and global labor shortages.

Q2. What is the CAGR of humanoid robot market?

The humanoid robot market is expected to grow at a CAGR of 39.2% during 2025–2032 due to increasing adoption across manufacturing, logistics, healthcare, and personal assistance applications.

Q3. Which region dominates humanoid robot market?

Asia Pacific dominates the humanoid robot market because of strong manufacturing ecosystems, government support, high patent activity, and rapid adoption in China, Japan, and South Korea.

Q4. Who are key players in humanoid robot market?

Key players in the humanoid robot market include Tesla, Boston Dynamics, Figure AI, Agility Robotics, UBTech, Unitree Robotics, NVIDIA, Samsung Electronics, Hyundai, and XPeng.