Global Industrial Robotics Market– Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning / Landscape Review & Global Market Size Forecast to 2034

Overview

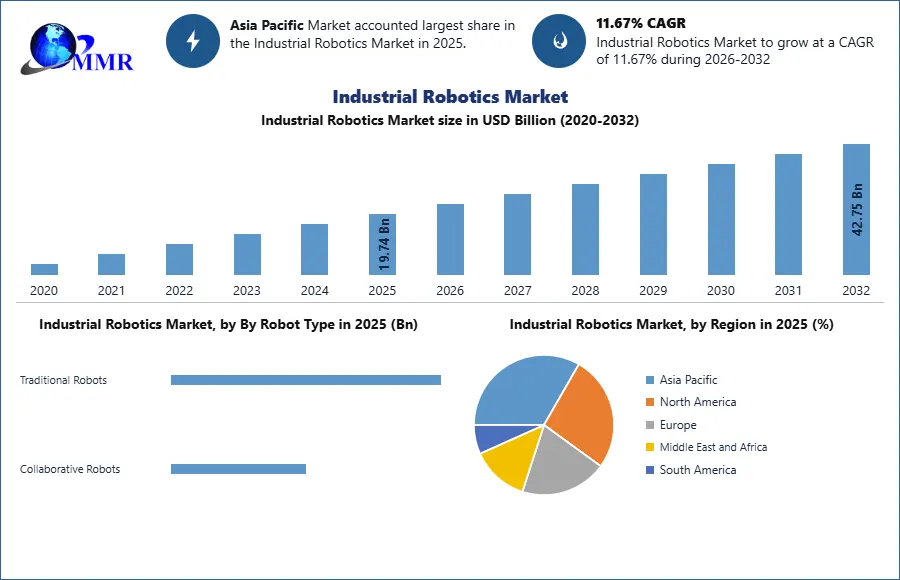

Global Industrial Robotics Market size was valued at USD 19.74 Billion in 2025, and the total Industrial Robotics Market revenue is expected to grow by 11.67% from 2026 to 2034, reaching nearly USD 53.31 Billion by 2034

Industrial Robotics Market Overview

Industrial robots are automated, programmable robotic machines designed to carry out manufacturing processes with speed, precision, and safety. These robotic systems are vital in industries such as automotive, electronics, aerospace, food & beverage, chemicals, and general manufacturing, where demand for automation continues to rise. The industrial robotics market has been expanding rapidly, driven by automation adoption, increasing labor costs, and a shortage of skilled workers. Companies are investing in robotics solutions to reduce costs, enhance product quality, and increase production efficiency. With strong R&D investment, the market is advancing toward AI-powered robots, smart automation, and collaborative robots (cobots) that work safely alongside humans in production environments.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

By type, articulated robots dominate the industrial robotics market owing to their flexibility and wide range of applications. Other types include SCARA robots, Cartesian robots, and cylindrical robots, which are used for specialized functions. Key applications include welding and soldering, material handling, assembly and disassembly, painting and dispensing, milling, and processing. Leading industrial robotics companies such as ABB Ltd (Switzerland), FANUC Corporation (Japan), KUKA AG (Germany), and Yaskawa Electric Corporation (Japan) continue to dominate the competitive landscape through OEM partnerships, direct sales, and system integrators.

Industrial Robotics Market Dynamics

High Requirement for Automation to drive the growth of the Industrial Robotics Market

The Companies have started focusing on automating operational processes to reduce costs, save time, deliver high-quality products, and increase productivity to meet the stiff competition. The report has analyzed and covered the direct positive impact of the top line of companies that have implemented industrial robotics solutions, either partially or fully. The report will give the penetration of industrial robotics in each industry in the countries covered.

High Labor Cost and Dearth of Skilled Human Workforce to drive the growth of Industrial Robotics Market

Various companies have adopted industrial robotics solutions to save costs due to the ever-increasing costs of labour in developed economies. Industrial robots enable companies to reduce wastage and eliminate the chances of faults occurring due to human errors. In the global market, the demand for delivery of improved products & services drives companies toward industrial robotics solutions, which can be operated with the help of software, thereby saving the expense incurred for training and management of labour. Unavailability of skilled labour to manage the processes and high labour costs have forced companies to adopt automation solutions, which supplement the growth of the Industrial Robotics market.

Increase in Investments in R&D Activities to drive the growth of Industrial Robotics Market

Heavy investment in various industries for R&D activities on robotics technology has encouraged the use of new and advanced technologies for the development of industrial robots. Industrial robots can be customized to serve specific requirements, such as cloud-based operation and remote monitoring, along with effective physical stature for improved compatibility with the human workforce by using innovative technologies. Rapid changes in the supporting factors, such as disposable income, consumer preference, wireless technologies, and others, have resulted into continuous improvements in specifications and features of industrial robots.

High Initial Investment and Installation Costs to restrain the growth of the Industrial Robotics Market

High installation cost and integration capabilities required for the initial setup of industrial robots restrain their adoption. Initial investment and maintenance costs of employing robotics systems are high due to the integration of high-quality hardware coupled with an efficient software control system. The need for high initial investment limits the use of industrial robotics in the professional and personal use segments. Industrial robotic systems are predominantly used in manufacturing, automotive, infrastructure, agriculture, food & beverage, metals, and chemical, rubber & plastics industries.

Increase in Application Areas to Create Lucrative Opportunities for Industrial Robotics Market Growth

Earlier, the use of industrial robots was restricted to the automotive and manufacturing industries; however, industries such as food & beverage, metals, chemical & material industries, aerospace, and electronics have deployed industrial robots. Increase in demand from the food & beverages sector for raw material handling, packing finished products, and logistics has increased the sales of industrial robots. The precision & optics sectors use robots for analysis of a variety of food products on the basis of quality, composition, and authenticity. In the future, the adoption of robotics technology is expected to increase further, leading to the Industrial Robotics Market growth.

Growth in Emerging Economies to Create Lucrative Opportunity for Industrial Robotics Market Growth

Emerging economies in Asia-Pacific and South America and Middle East and Africa have adopted industrial robotics solutions for various professional uses, and this is expected to facilitate faster growth in terms of efficiency. For instance, India has taken an initiative to support the growth of industrial robotics by introduction of Robotics 2 under Make in India campaign. Moreover, the robot revolution program is being implemented by Japan for expansion of robotics. The implementation of industrial robotics in agriculture, construction, and logistics sectors is also expected to strengthen the infrastructure of these economies.

Industrial Robotics Market Segment Analysis

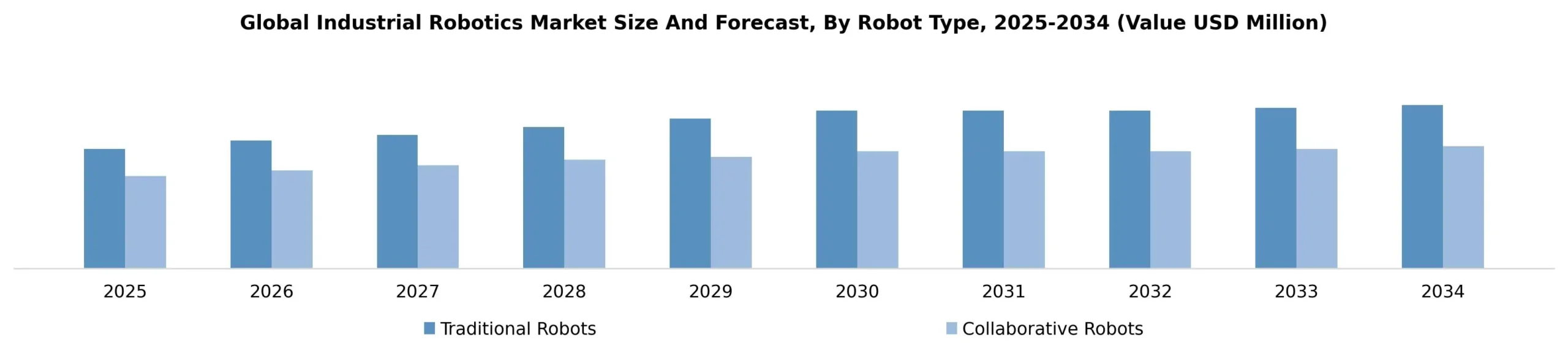

Based on Type, the Industrial Robotics Market is segmented into articulated, Cartesian, SCARA, cylindrical, and other types of industrial robots. The articulated robot’s segment is expected to hold the major Industrial Robotics Market share during the forecast period, owing to technological innovation, which has increased its flexibility to perform multiple functions and payload capability. Articulated robots are based on three rotary joints, thereby resembling movements similar to the human hand, and can be fixed or moving as per requirement.

These robots are able to operate in spherical space. These robots are highly advantageous in manufacturing industry for pick & assembly operations. An articulated robot can be used for various applications such as welding, material handling, & dispensing, among others. These robots can optimize warehouse operations through improved speed and accuracy, and are popular for their longevity.

Based on Payload, the Industrial Robotics Market is segmented into Up to 16 kg, 16 to 60 kg, 61 to 225 kg, and Above 225 kg. The 16 to 60 kg segment held the largest Industrial Robotics Market share in 2025 due to its versatility across a broad range of manufacturing applications. Robots within this payload range provide an optimal balance between lifting capacity, speed, and precision, making them suitable for assembly, machine tending, welding, packaging, and material handling operations. They are widely adopted across automotive, electronics, food & beverages, and metal fabrication industries where medium-duty automation is required. Increasing investments in flexible manufacturing systems and smart factories continue to drive demand for this payload category.

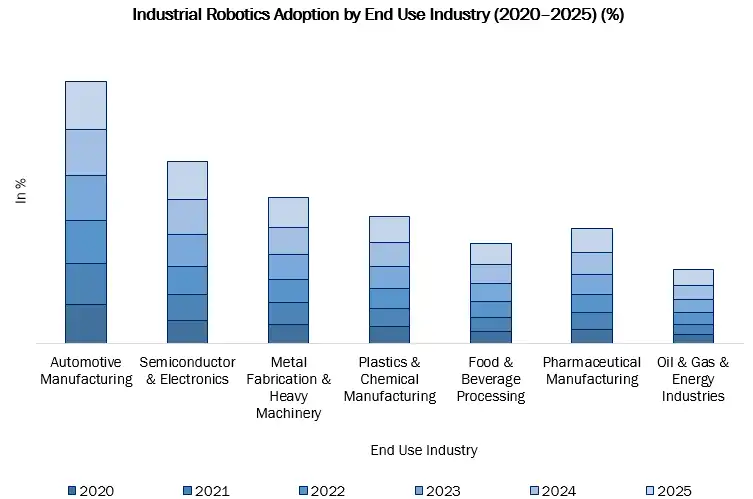

Based on Function, the industrial Robotics Market is segmented into soldering & welding; material handling, assembling & disassembling; painting & dispensing; milling, cutting, and processing; and others. Material handling was the largest segment by function, in terms of revenue, in the industrial robotics market in 2024. Currently, it accounts for over one-third of the global industrial Robotics Market and is expected to remain the largest segment during the forecast period, thanks to an increase in demand for industrial robots in the materials handling function.

All types of goods, including small, medium, and large, are stored in warehouses & manufacturing units in massive volumes. These goods are placed in large racks with heights and are navigated through the warehouse management system (WMS). To place and sort these goods, material handling is performed by robots. This has made the functioning faster, safer, and more productive. These factors drive the growth of this segment in the industrial robotics market.

Based on Offering, the Industrial Robotics Market is segmented into Hardware, System Engineering, Software & Programming, and Others. Hardware held the largest Industrial Robotics Market share in 2025, driven by the substantial investment required for robotic arms, end effectors, controllers, drive units, vision systems, sensors, and safety components. Hardware forms the foundation of every industrial robotic installation and represents the largest share of capital expenditure in automation projects. Growing adoption of advanced robotic systems across manufacturing facilities, coupled with continuous innovation in servo drives, machine vision, and end-of-arm tooling, continues to support the dominance of the hardware segment.

Based on End-Use Industry, the Industrial Robotics Market is segmented into Automotive, Electrical & Electronics, Metals & Machinery, Plastics, Rubber & Chemicals, Food & Beverages, Precision Engineering & Optics, Pharmaceuticals & Cosmetics, Oil & Gas, and Others. The Automotive segment held the largest Industrial Robotics Market share in 2025 due to its long-standing leadership in manufacturing automation. Automotive manufacturers extensively deploy industrial robots for welding, painting, assembly, machine tending, inspection, and material handling to improve production efficiency, product quality, and worker safety. The increasing production of electric vehicles, growing adoption of flexible manufacturing systems, and continuous investments in smart factories further reinforce the automotive industry's position as the largest consumer of industrial robotics globally.

Based on Application, the Industrial Robotics Market is segmented into Handling, Assembling & Disassembling, Welding & Soldering, Dispensing, Processing, Cleanroom, and Others. Handling held the largest Industrial Robotics Market share in 2025 owing to the growing automation of material movement across manufacturing and warehouse environments. Handling applications, including pick-and-place, material handling, packaging, and palletizing, require high-speed and repetitive operations that industrial robots perform with exceptional precision and consistency. Rising e-commerce activities, increasing warehouse automation, and the need to improve production efficiency while reducing labor costs continue to accelerate demand for robotic handling systems worldwide.

Industrial Robotics Market Regional Insights

Technological advancements, particularly in the developing regions of Asia-Pacific and South America, and Middle East, and Africa, coupled with increased investments in education and research infrastructure across the regions, propel the industrial robotics market.

In addition, the increase in demand for renewed and optimized robots, especially in North America and Europe, and rapid growth in the food and beverage industry, thanks to lifestyle changes worldwide, promote the development of the industrial robotics market. The Asia-Pacific dominance in the Industrial Robotics Market is expected to continue in the forecast period, followed by North America and Europe. Asia-Pacific is the most populous region, including countries such as China, India, Japan, Taiwan, and Australia, and has invested heavily in R&D activities, promoting the growth of the industrial robotics market. The end-user Asia-Pacific Industrial Robotics promotes the demand for plastic products and plastic materials in the market, and technological growth promotes development. Increase in adoption of automated systems in the growing food & beverage, logistics, pharmaceutical, and other sectors; improved & safe working conditions; and technological advancements foster the demand for packaging robots in this region. The Indian government emphasizes safety and security on the production floor, which accelerates the growth of the packaging robots market.

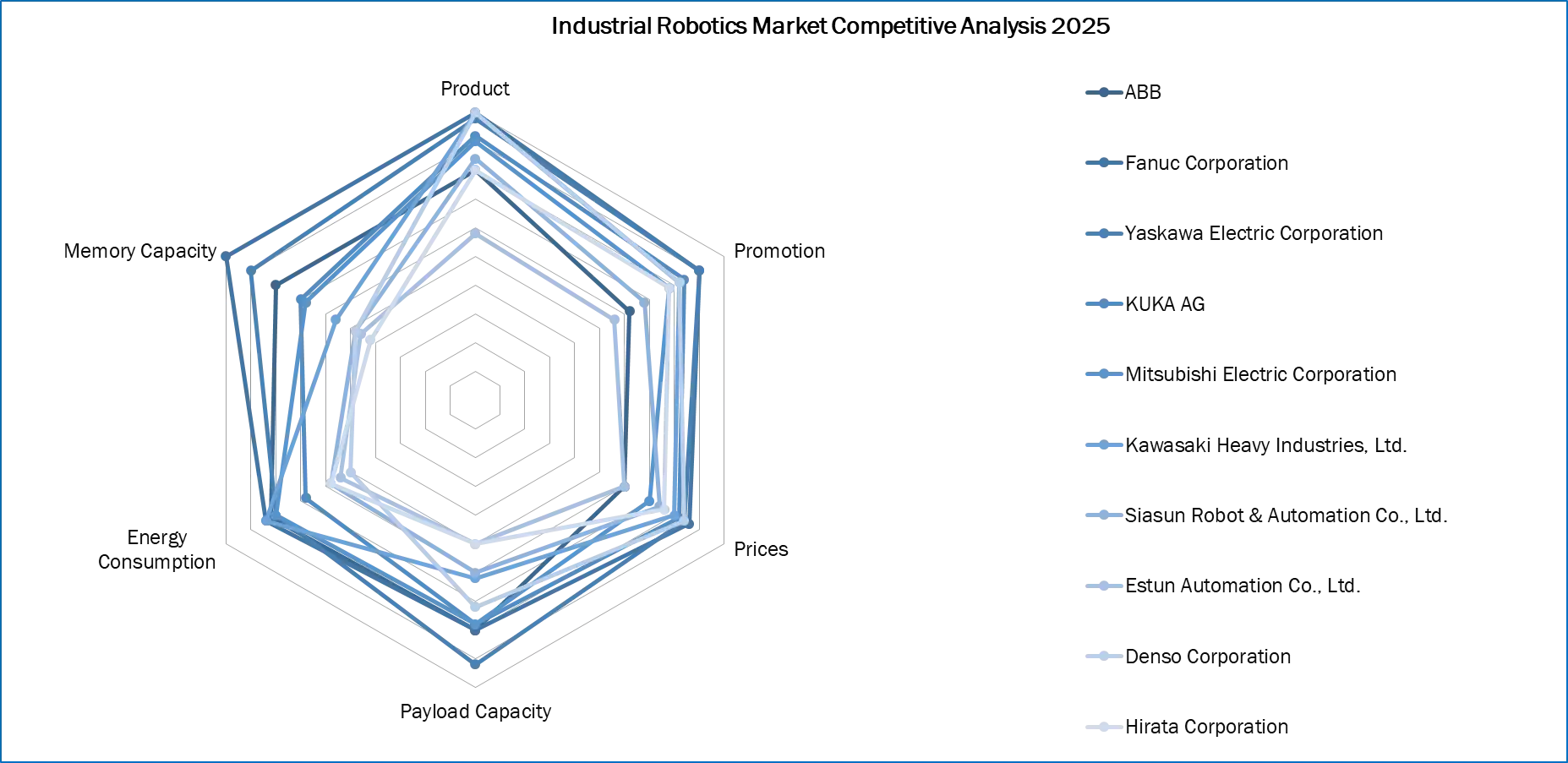

Industrial Robotics Market Competitive Landscape:

The industrial robots market consists of a mix of global industrial manufacturing corporations and automation specialists, with each manufacturer offering technological and innovative advantages. Many large companies have engineering expertise and market share, such as ABB Ltd. (Europe), and FANUC Corporation (Asia-Pacific). These two companies have very different ideas about how best to utilize robotics technology, and each offers a unique value proposition; ABB focuses on integrated automation systems and smart robotics, while FANUC offers the highest performance manufacturing robots with the broadest global reach.

ABB Ltd. is a dominant multinational player in industrial robots and a globally known company based in Switzerland that provides state-of-the-art automation solutions. ABB, with its heavy range of robots, has industry-best-in-class hardware equipment for nearly every global industry, including automotive, electronics, and logistics. A considerable point of differentiation for ABB is the global all-in-one automation ecosystem, since they are selling their hardware robotics equipment with their complete packaged software and digital services. ABB is still investing in the R&D of collaborative robots (cobots) that are AI-powered autonomous robots and integrated control systems. ABB partners closely with OEMs and system integrators to provide fully customizable automation solutions that can enhance both productivity and flexibility on the factory floor across a variety of sectors and is firmly established in Germany, North America, and Asia.

Industrial Robotics Market Key Developments:

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 16 March 2026 | Universal Robots A/S | Launched the UR AI Trainer at GTC 2026, an imitation learning system developed in collaboration with Scale AI. | This shifts robots from pre-programmed routines to fully AI-driven tasks, bridging the gap between laboratory research and factory-floor deployment. |

| 07 February 2026 | ABB Ltd. | Unveiled Autonomous Versatile Robotics (AVR™) solutions at SLAS 2026 to automate complex laboratory workflows. | The AI-powered systems enable seamless multi-vendor connectivity, allowing researchers to automate high-throughput tasks like pipetting and vial handling. |

| 01 December 2025 | Fanuc Corporation | Released a dedicated ROS 2 driver and Python support as open-source software to accelerate Physical AI implementation. | This facilitates the integration of NVIDIA Isaac Sim digital twins, enabling developers to perform accurate photorealistic simulations for robots up to 2.3 tons. |

| 06 October 2025 | Universal Robots A/S | Expanded the UR Series with the launch of the UR18, an industrial collaborative robot designed for high payload in a compact form. | The UR18 enhances productivity in heavy-duty tasks such as palletizing and machine tending without requiring extensive safety guarding. |

| 24 June 2025 | Comau S.p.A. | Unveiled the MyCo family of collaborative robots and the MyMR Autonomous Mobile Robot (AMR) platform at Automatica 2025. | These modular solutions target modern intralogistics and additive manufacturing, offering payload capacities from 3 kg to 1,500 kg for flexible production. |

| 17 April 2025 | ABB Ltd. | Announced a strategic proposal for a 100 percent spin-off of its Robotics division to become a separately listed company. | The move is intended to optimize capital allocation and allow the pure-play robotics business to focus on high-growth sectors like AMRs and AI-enabled software. |

Industrial Robotics Market Key Trends:

• AI-enabled Autonomy and Modular Robotics Platforms

Organizations, such as ABB, are producing significantly capable AI-enabled autonomy platforms (e.g., OBniCore) as well as autonomous versatile robots that can execute a number of tasks in a standalone fashion. This shows that there is a persistent pattern of significant advancements in intelligent, multi-use, adaptable, and energy-efficient robotic systems that can easily serve numerous industries that offer flexibility in application.

• Collaborating Growth in Humanoid and Specialized Robotics

The callback to launching investments in humanoid and specialized robots is seen in the rise of projects like Kawasaki’s AI-based robotic horse and the K-Humanoid Alliance in South Korea. This is yet another opportunity to launch collaboration that shows the interests of not only industry, but also, governments and academia to help accelerate innovation in humanlike and task-specific robots while expanding globally (i.e., Doosan robotics expanding to the growing European market).

Industrial Robotics Market Scope: Inquire before buying

| Industrial Robotics Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 19.74 USD Billion |

| Forecast Period 2026-2034 CAGR: | 11.67% | Market Size in 2034: | 53.31 USD Billion |

| Segments Covered: | By Robot Type | Traditional Robots Articulated Robots SCARA Robots Parallel Robots Cartesian Robots Cylindrical Robots Others Collaborative Robots |

|

| By Payload | Up to 16 kg 16 to 60 kg 61 to 225 kg Above 225 kg |

||

| By Offering | Hardware End Effectors Welding guns Grippers Tool changers Clamps Suction cups Others Controllers Drive Units Hydraulic Electric Pneumatic Vision Systems Sensors Power Supply Accessories Safety Fencing Hardware Fixtures & Tools Conveyor Hardware Others System Engineering Software & Programming Others |

||

| By Application | Handling Pick & Place Material Handling Packaging & Palletizing Assembling & Disassembling Welding & Soldering Dispensing Gluing Painting Food Dispensing Processing Grinding & Polishing Milling Cutting Cleanroom Others |

||

| By End-Use Industry | Automotive Electrical & Electronics Metals & Machinery Plastics, Rubber & Chemicals Food & Beverages Precision Engineering & Optics Pharmaceuticals & Cosmetics Oil & Gas Others |

||

Industrial Robotics Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Industrial Robotics Market, Key Players

- ABB Ltd.

- Fanuc Corporation

- Yaskawa Electric Corporation

- KUKA AG

- Mitsubishi Electric Corporation

- Kawasaki Heavy Industries, Ltd.

- Siasun Robot & Automation Co., Ltd.

- Estun Automation Co., Ltd.

- Denso Corporation

- Hirata Corporation

- Nachi-Fujikoshi Corp.

- Seiko Epson Corporation

- Omron Corporation

- Universal Robots A/S

- Stäubli International AG

- Comau S.p.A.

- Delta Electronics, Inc.

- Dürr AG

- Yamaha Motor Co., Ltd.

- Techman Robot Inc.

- Franka Robotics GmbH

- HD Hyundai Robotics

- Shibaura Machine Co., Ltd.

- Daihen Corporation

- Doosan Robotics

- Hanwha Robotics

- IGM Robotersysteme AG

- CMA Robotics S.p.A.

- STEP Electric Corporation

- Elite Robots

Other