Helicopter Market Size by Type, Weight, Number of Engine, Application, Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

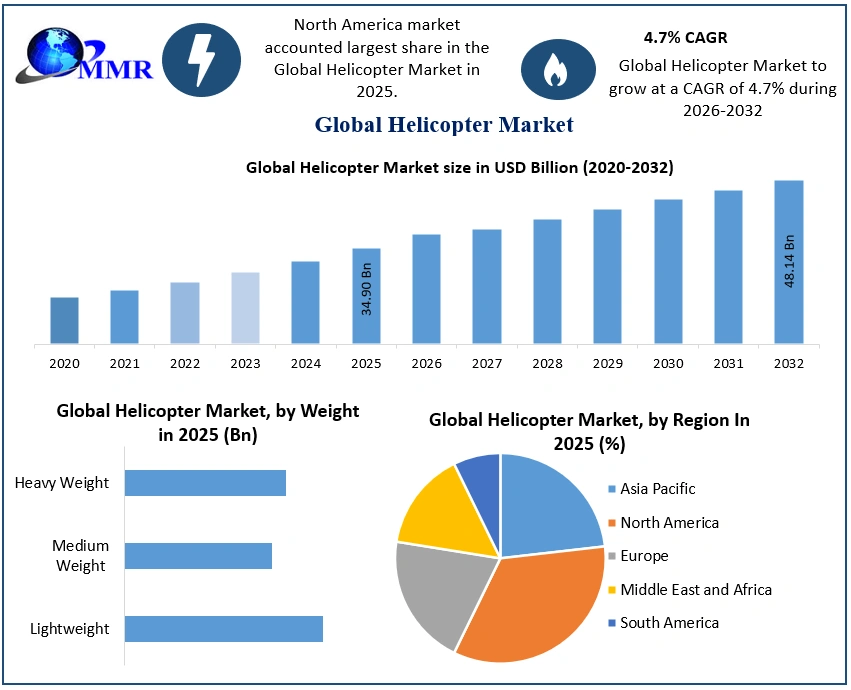

The Helicopter Market size was valued at USD 34.90 Billion in 2025 and the total Helicopter revenue is expected to grow at a CAGR of 4.7% from 2025 to 2032, reaching nearly USD 48.14 Billion by 2032.

Helicopter Market Overview:

Looking ahead, the Helicopter Market is expected to continue consistent performance in, with stable deliveries hovering nearby the 500-unit mark. Despite continuing resolutions, supply chain issues may persist into 2024. Preceding the leased helicopter operations are North America and Europe, among a focus on offshore oil & gas, emergency medical services (EMS), and search and rescue roles. South America and Asia are also playing substantial roles in catering to this demand.

Helicopters are required for air ambulance services owing to their ability to reach remote areas faster than conventional automobiles and traditional aircraft. They can access distant, inaccessible places, like military bases deep in forests or oil rigs in the middle of the sea, within a short period. The early medical treatment of patients, permitted by quick emergency transport by helicopters, significantly increases the survival rate in serious cases. For example, MH-60 Jayhawks based at USCG Station Kodiak play a crucial role in fishing operations in the remote and treacherous Bering Sea with lifting crewmembers in distress off boats and transporting them to the nearest healthcare centre in Dutch Harbor.

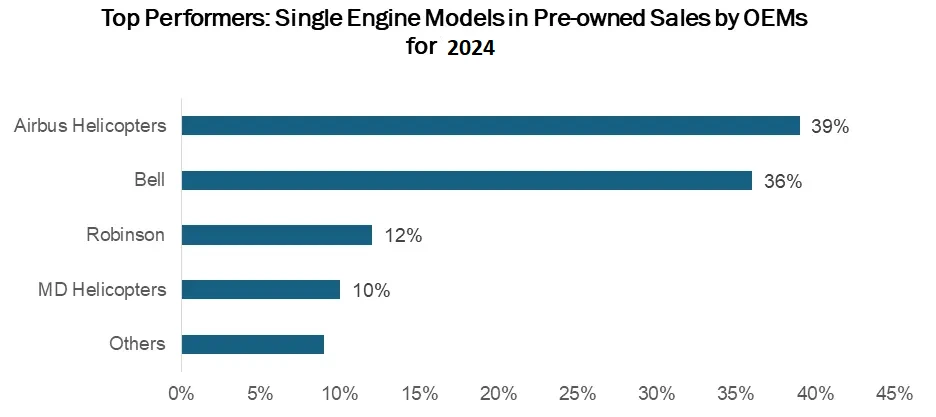

| Airbus Helicopter: A Record Year of Orders and Deliveries in 2024 | |||

|---|---|---|---|

| Airbus Helicopter Gross Orders | 410 | ||

| Airbus Helicopter Deliveries | 346 | ||

| Market Share | 54% | ||

Airbus Helicopters Reports Robust Sales Growth in 2024:

Airbus Helicopters recorded 410 gross orders (net: 393), highlighting a steady recovery in the Helicopter Market with a strong performance for light twin and medium twin helicopters in . Orders were placed by 179 buyers across 47 countries. The company brought 346 helicopters in , resulting in a beginning 54% share of the civil and parapublic market.

In “Airbus Helicopter’ order intake with an increase nearby 10% in units compared to , focuses its stable growth despite the ongoing global context of inflation and geopolitical instability, The was a year of many firsts for Airbus Helicopters, counting the first flight of the DisruptiveLab demonstrator featuring a new aerodynamic architecture pointed at reducing fuel feasting and the first flight of the NH90 Sea Tiger, a state-of-the-art anti-submarine warfare helicopter for the German Navy. Furthermore, the company welcomed a new member to the Airbus family with the Spanish Navy taking delivery of their first H135 helicopters.

Helicopter Market Dynamics:

Helicopter Utilization in Military Applications on the Rise:

Military helicopters are most used to transport personnel, nonetheless they can also be modified for many additional duties, with being armed with weaponry to strike ground targets, conducting medical removal (MEDEVAC), serving as airborne command posts, or performing combat search & rescue (CSAR) missions. Governments of both developed and developing nations are enhancing investments in their military forces to found battlefield dominance and perform rescue missions with enhanced helicopters.

Such as, in June , Poland stated plans to purchase several AW149 military helicopters, joined by the Italian company Leonardo.

Moreover, in December , the French Armament General Directorate (DGA) signed a contract with Airbus Helicopters, a France-based company and one of the foremost helicopter manufacturers, for the growth and obtaining of the H160M as part of the Light Joint Helicopter Program (HIL). The contract contains the development of several prototypes and the delivery of the first batch of 30 aircraft, with 21 for the army, 8 for the navy, and 1 for the air force. The rise in adoption of helicopters by military forces is expected to drive the growth of the Helicopter Market.

Demand for Customized and Luxurious Helicopters in the Transportation Sector is Growing:

In recent years, helicopter air transportation has risen, with updated, expanded, and increased services. Speed is fundamental in helicopter air travel, driving heightened demand thanks to its efficiency and convenience. This growing demand is fueling growth in the Helicopter Market within the transportation sector.

Helicopters boast simpler take-off and landing operations compared to conventional aircraft, and they are unchanged by geographical constraints, making them ideal for short-distance travel and transportation. Furthermore, the introduction of luxurious helicopters by industry leaders for public transportation is poised to further stimulate Helicopter Market growth. Such as, Airbus launched the ACH160, a $14 million luxury helicopter devised for business or private use, helping up to 10 passengers in sept . The mounting demand for customized and luxurious helicopters, coupled with current innovations, is expected to drive robust growth in the global Helicopter Market during forecast period.

To know about the Research Methodology :- Request Free Sample Report

Helicopter Market Trends:

The integration of developed AI systems and automation capabilities in helicopters is a pivotal trend driving the growth of the Helicopter Market globally. Modern helicopters are now equipped with advanced sensors that increase accuracy and precision across various tasks. These advanced control systems confirm safe and reliable operation of these aerial vehicles.

Manufacturers have also started combining advanced features aimed at improving safety, efficiency, and versatility. Modern helicopter designs incorporate advanced automation capabilities, significantly reducing the need for manual labour and allowing personnel to focus on more critical tasks. Automation not only enhances efficiency but also minimizes errors, leading to quicker turnaround times at construction sites. Furthermore, helicopters consume less energy and produce fewer emissions compared to traditional ground-based cranes, making them an ecologically friendly choice for construction projects. The introduction of advanced technologies and automation capabilities has made helicopters more efficient, precise, and dependable, driving growth in the Helicopter Market throughout the forecast period.

Helicopter Market Segmentation Insight:

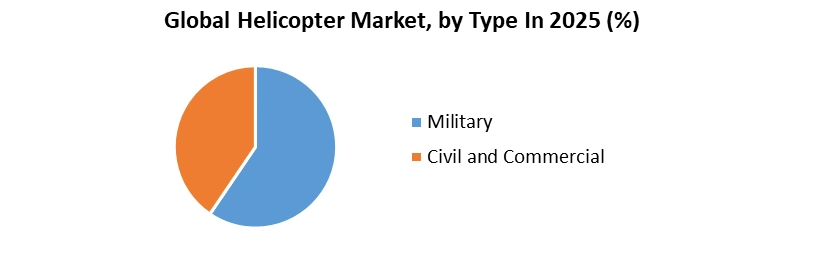

By Type, the Civil and Commercial segment held the largest Helicopter Market share of about 65% for the Helicopter Market in 2025 and is expected to dominate the market at the end of the forecast period. The growth is driven by growing need for emergency services and a rising need for air transportation. The demand for quick transportation and efficient grows as the population raises and urban areas expand.

The military segment is expected to grow moderately over 2025-2032. The Helicopter Market is growing as an aging fleet is replaced and modernized, including increased use in disaster relief and humanitarian missions.

By Weight, in 2025, the lightweight segment dominated the Helicopter Market with Helicopter Market share nearly 55%. This growth is driven by growing demand for civil and commercial helicopters used for activities like sightseeing, aerial photography, and transporting small groups and cargo. Lightweight rotorcraft, depicted by a maximum take-off weight of less than 6,000 pounds, are noted for their agility, ease of operation, and suitability for various tasks.

Helicopter Market Regional Insight:

Geographically, North America held the largest market share of about xx% in 2025 for the Helicopter Market and is expected to dominate the market at the end of the forecast period. This dominance is attributed to the U.S. having the largest helicopter fleet and a raising reliance on helicopters for air ambulance services. The U.S. presently operates a fleet of nearly 7,014 helicopters, with over 1,000 dedicated to air ambulance duties. The increase in demand for helicopter services is further propelled by the developing offshore wind farm projects across the country, driven by developing demands for cleaner and more viable energy sources. This has led to a surge in new contracts and partnerships, substantially boosting Helicopter Market value.

For example, Orsted and Eversource awarded HeliService International Inc. a contract for helicopter crew changes operations for their joint offshore wind projects in the Northeast United States in . Using Leonardo AW169 helicopters, this agreement underscores the industry's response to developing offshore activity. Furthermore, the uptick in revenue from the oil & gas sector has directly correlated with enhanced demand for helicopter services in offshore operations. Conversely, the influx of private equity investors into the air ambulance industry, aimed at improving service quality, also poses challenges like potential increases in operational costs passed on to customers. Also, across Canada, rising demands for helicopters span various applications with emergency medical services, search and rescue operations, leisure charters, and more, contributing to regional Helicopter Market growth.

Developments in the Helicopter Market by Key Industry Players:

1. Vertical Aerospace and Rolls-Royce: Signed a partnership agreement in July 2023 to jointly develop and certify an electric vertical takeoff and landing (eVTOL) aircraft for urban air mobility applications.

2. Cicare USA: Announced in July 2023 that its Cicare 8 helicopter had received certification under the LTF-ULH regulations for ultralight helicopters, applicable to helicopters with a maximum take-off weight under 600 kg or 1320 lbs.

3. Leonardo Helicopters and Collins Aerospace: Collaborated on a digital solutions project for helicopter health and usage monitoring, enhancing maintenance efficiency and safety, announced in August 2023.

Helicopter Market Scope: Inquiry Before Buying

| Helicopter Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 34.90 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 4.7% | Market Size in 2032: | USD 48.14 Bn. |

| Segments Covered: | by Type | Military Civil and Commercial |

|

| by Weight | Lightweight Medium Weight Heavy Weight |

||

| by Number of Engine | Twin Engine Single Engine |

||

| by Application | Emergency Medical Service Oil and Gas Defense Homeland Security Others |

||

Helicopter Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Helicopter Market, Key Players:

1. Airbus Helicopter Inc. (France and Germany)

2. AgustaWestland (Italy) (part of Leonardo S.p.A.)

3. Bell Helicopter (United States)

4. Korea Aerospace Industries (KAI) (South Korea)

5. Avicopter (China)

6. PZL Swidnik (Poland) (part of Leonardo S.p.A.)

7. Enstrom Helicopter Corporation (United States)

8. Kaman Aerospace (United States)

9. Sikorsky Aircraft Corporation (United States) (part of Lockheed Martin)

10. Columbia Helicopters (United States)

11. Leonardo S.p.A. (Italy)

12. MD Helicopters Inc. (United States)

13. Boeing Rotorcraft Systems (United States)

14. Jiangxi Changhe Aviation Industry Co., Ltd. (China)

15. Robinson Helicopter Company (United States)

16. Russian Helicopters, JSC (Russia)

FAQs:

1] What segments are covered in the Global Helicopter Market report?

Ans. The segments covered in the Helicopter Market report are based on Type, Wight, Number of Engine, Application and Region.

2] Which region is expected to hold the highest share in the Global Helicopter Market?

Ans. North America region is expected to hold the highest share of the Helicopter Market.

3] What is the market size of the Global Helicopter Market by 2032?

Ans. The market size of the Helicopter Market by 2032 is expected to reach USD 48.14 Bn.

4] What is the forecast period for the Global Helicopter Market?

Ans. The forecast period for the Helicopter Market is 2026-2032.

5] What was the Global Helicopter Market size in 2025?

Ans: The Global Helicopter Market size was USD 34.90 Billion in 2025.