Heat Exchanger Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Market Size Forecast to 2032

Overview

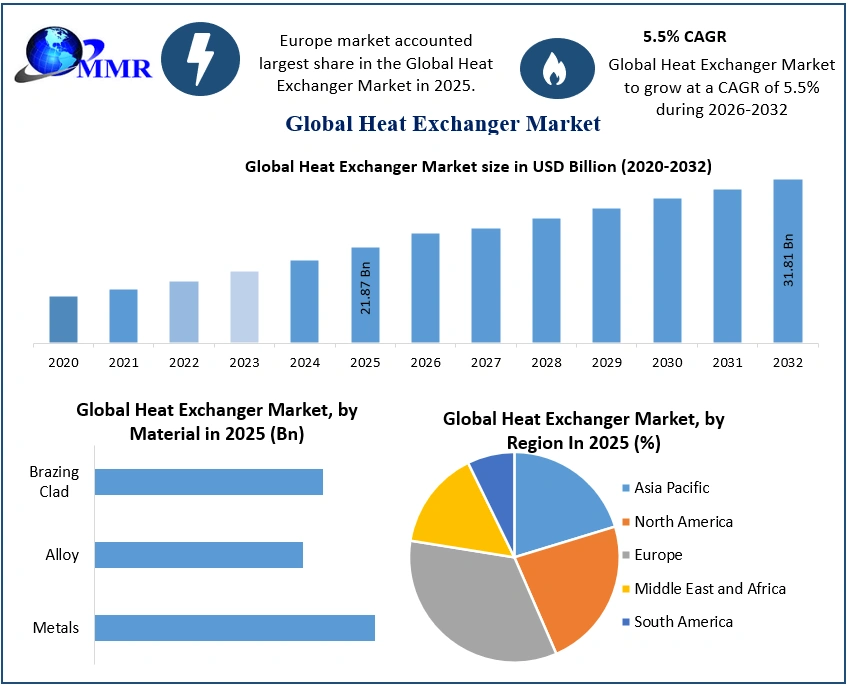

The Heat Exchanger Market size was valued at USD 21.87 Billion in 2025 and the total Heat Exchanger revenue is expected to grow at a CAGR of 5.5% from 2025 to 2032, reaching nearly USD 31.81 Billion by 2032.

Global Heat Exchanger Market Overview:

Heat exchangers are devices used for transfer of heat from one medium to another without mixing the two mediums. The heat exchanger either heats or cools processes by transfer of heat energy through the process of conduction. The heat exchanger market growth is fueled by the demand for energy efficient operations across industries as heat exchangers play a critical role in facilitating transfer of heat between fluids and other medium. The heat exchangers are vital for temperature control and waste heat recovery in chemical and power generation industries. The region of Europe has accounted largest heat exchanger market share for in 2025 due to investments in industrial sectors and demand from end user industries.

The booming chemical processing, oil & gas, power generation, food and beverages and many more are reasons for growth of the region. The demand from HVAC, refrigeration, automobile are other factors driving the growth of the market. The rise of industrial activities in China and India are creating increased demand in the Asia-Pacific region over the forecast period. The adoption of eco-friendly practices, developments in design are some of the trends of heat exchanger market. The metal type of material used for manufacturing of heat exchangers are widely used by manufacturers due to their thermal properties.

The chemical industries held largest market share of end users for heat exchanger market in 2025. The energy & power generation, oil & gas, food & beverage, HVAC are major industries driving the market. Sourcing of raw material, environmental regulations and pricing are some of the challenges faced by heat exchanger market. With promising growth prospects, the market has a good growth over the forecast period. Companies like Alfa Laval, Danfoss, Boyd, SPX Flow and many more are key players that are leveraging their capabilities in the market.

To know about the Research Methodology:- Request Free Sample Report

Global Heat Exchanger Market Dynamics:

Heat Exchangers are incorporated components in heat pumps which enable exchange of heat between the system and external environment. Heat pumps solely rely on heat exchangers and increased uptake of heat pumps are facilitating growth of the market. Heat exchangers are characterized by high innovation with rapid technological advancements. Industries are focusing on methods to reduce energy consumption, hence heat exchangers are being used to exchange heat in the production processes. The major factor driving the growth of the market is the chemical industry with expansion of domestic end use sectors. The demand is higher from chemical industry due to various uses in production processes and cooling of industrial equipment. The growth in chemical, oil& gas industries are driving the heat exchanger market over the forecast period, as these industries rely heavily on heat exchangers. Additionally, European Union promotes renovation and enhanced energy efficiency which are contributing to adoption of heat exchangers in the present year. The growth of power generation industries in US, India, Russia are anticipated to boost the heat exchanger market growth over the forecast period.

As the heat exchangers require stable metals for designing of outer body, manufacturers often face risk of sourcing raw material and changing prices of metals. The volatility of prices is hampering profit margin and operational efficiency of manufacturers in the heat exchanger market. The HFC gas emitted from heat exchangers is curbing the use of heat exchangers due to regulations on emission of hazardous gases. As a result, European Union has adopted several ways to limit fluorinated gas emissions into the air. These are some of the factors that are limiting the growth of market.

The market holds opportunities for existing and new market entrants by focusing on sustainable practices and use of advanced materials that are making heat exchangers more attractive to industries. The development of heat exchangers that utilize eco-friendly refrigerators can cater the demand for sustainable solutions in the market in the upcoming years. Various infrastructure and oil field development projects across the globe provide potential opportunities in the heat exchanger market.

Global Heat Exchanger Market Segmentation:

The global heat exchanger market is segmented by product type, material and its application in the end-user industry. By product type, Shell and Tube heat exchangers are versatile exchangers used by many industries for effective heat transfer system. The construction of shell and tube heat exchangers with carbon, steel, copper alloys provide mechanical strength and also guarantee reliability and performance in diverse conditions. Thus, the segment holds largest growth in the heat exchanger market. However, the requirement of large spaces for shell and tube heat exchangers is likely to affect the demand over the forecast period. The Plate & Frame heat exchanger segment is expected to increase steadily in the heat exchanger market over the forecast period. Also, air cooled exchangers are used in gas stations, power plants, refineries as these can be installed at different angles. Hence, air cooled exchanger is the second fastest growing segment in the heat exchanger industry over the forecast period.

By material type, the metals like aluminum, stainless steel, copper, are widely used by manufacturers for designing of heat exchangers, as these metals have high thermal conductivity with efficient transfer of heat, hence are preferable for heat exchanger manufactures. These metals provide mechanical strength, durability which ensures the longevity of the heat exchanger system. These metals are also cost effective over other materials hence, are widely preferred by manufacturers over the past years.

By end user industry, chemical sector is witnessing highest growth in heat exchanger market due to application of heat exchangers in various processes such as cooling, condensing, heating, evaporation and many other areas. The chemical industry is highly using heat exchanger on account of their characteristics, flexible design, anti-corrosive property and ability to handle varying level of solids. For handling hazardous agents in chemical industries, heat exchangers with specific design are used to fulfil the demand of that sector. Secondly, heat exchangers are widely used in HVAC systems, energy power plants, oil and gas industries for temperature control in production processes. These industries require efficient heat control, power generation and facilitate energy conversion processes.

Overall, the heat exchanger market segment analysis gives an outlook of the characteristics, demand, material, types of heat exchangers and the end user industries which are using heat exchangers for temperature control and production processes and many other applications.

Global Heat Exchanger Market, Regional Insights:

The region of Europe accounted the largest market share in the heat exchanger market in 2025. The rising investments in European countries in leading to growth of heat exchangers in the region. The demand from several end use industries for heat exchangers in Germany, France, UK are expected to drive the growth in the European region. The rising use of refrigeration and power generation are further expanding the growth of heat exchanger market over the forecast period. The increasing energy demand from commercial and residential sectors are positively impacting the market growth in Europe. The developments in US and Canada in oil & gas industries are driving the market growth in North America. The Asia-Pacific is a rapid growing region due to industrialization, investments in commercial and manufacturing sectors in China and India with adoption of sustainable practices. The government of these nations is focusing more on reducing greenhouse gases which are driving the uptake of heat exchangers in Asia-Pacific. In 2023, LU-VE Group (Tianmen, China) announced its expansion of production plant which is a key factor driving the growth of heat exchanger market in Asia-Pacific.

Global Heat Exchanger Market, Competitive Landscape:

Global market players are focusing on manufacturing energy-efficient designs and mergers and acquisitions to sustain the market competition.

In 2023, Alfa Laval partnered with Outokumpu, global steel manufacturer, to reduce carbon emissions by utilizing the green stainless steel in production of heat exchangers. The partnership emphasizes to decrease the carbon footprint to half level than original level.

In 2023, Danfoss Heat Exchangers signed an agreement with Danfoss Commercial Compressors, to establish an in-house facility for testing of plate heat exchangers from 10-150 kW capacity.

In 2023, Kelvion Holding GmbH invested $4.3 million to expand its production capacities in order to meet increasing demand for heat exchangers for diverse end users. The expansion enables the facility to manufacture 1,50,000 heat exchangers annually, with expanding its presence in US market.

In 2023, Kelvion launched its air cooler series for natural refrigerators. The CDF & CDH ranges are dual discharge air coolers that highlight a proficient tube system.

In 2023, SPX Flows introduced the new Plate Heat Exchanger Frame which has improved usability and durability to reduce costs for food and beverage operators.

Heat Exchanger Industry Ecosystem:

Heat Exchangers Market Scope: Inquire before buying

| Heat Exchangers Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 21.87 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 5.5% | Market Size in 2032: | USD 31.81 Bn. |

| Segments Covered: | by Product Type | Plate & Frame Shell &Tube Air Cooled Others |

|

| by Material | Metals Alloy Brazing Clad |

||

| by End-Use Industry | Chemicals Oil & Gas Power Generation HVAC Automobile Food & Beverages Others |

||

Heat Exchangers Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Heat Exchangers Market, Key Players:

1. Alfa Laval (Sweden)

2. Kelvion Holding GmbH (Germany)

3. Danfoss (Denmark)

4. Mersen (France)

5. API Heat Transfer (United States)

6. Boyd (United States)

7. Johnson Controls (Ireland)

8. Wabtech Corporation (United States)

9. Xylem (United States)

10. SPX Flow (United States)

11. LU-VE Group (Italy)

12. Lennox International Inc (United States)

13. Modine Manufacturing Company (United States)

14. Koch Heat Transfer Company (United States)

15. Southern Heat Exchanger (United States)

16. Hisaka Works Ltd (Malaysia)

17. Chart Industries (United States)

18. Radiant Heat Exchangers (India)

19. Glacier Energy (United Kingdom)

Frequently Asked Questions FAQ’s

1) What segments are covered in Global Heat Exchanger Market report?

Ans. The segments covered in Global Heat Exchanger Market report are based on Product Type, Material, and End User Industry.

2) Which region held the largest Heat Exchanger Market share in 2025?

Ans. Europe is expected to hold the largest Heat Exchanger Market share in 2025.

3) Who are the top players in the Global Heat Exchanger Market?

Ans. Danfoss, SPX Flow, Alfa Laval, Kelvion Holdings, Mersen and many more are the top players in the Global Heat Exchanger Market.

4) Which segment is expected to hold the largest Market share by 2032?

Ans. Shell and Tube exchanger segment is expected to hold the largest Market share by 2032.

5) What is the expected Global Heat Exchanger Market size by 2032?

Ans. The expected Global Heat Exchanger Market size is USD 31.81 Bn by 2032.