Global Health Insurance Exchange Market Size by Product type, Phase, End-use and Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2029

Overview

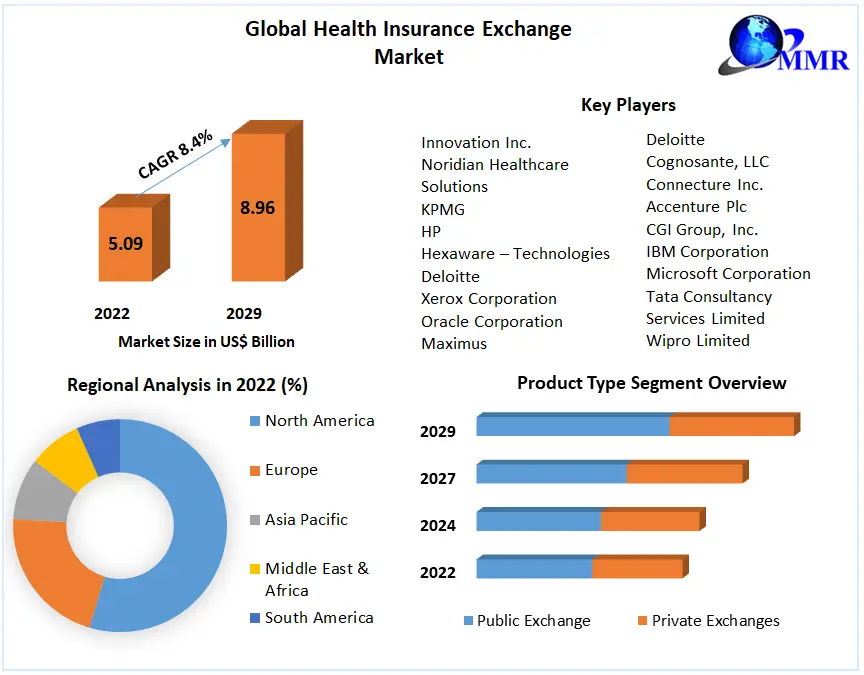

Health Insurance Exchange Market was valued at US$ 5.09 Bn. in 2022 and the total revenue is expected to grow at 8.4% of CAGR through 2023 to 2029, reaching nearly US$ 8.96 Bn.

Health Insurance Exchange Market Overview:

A health insurance exchange sometimes referred to as a health insurance market is a site where people may compare different health insurance options. Individuals use the exchange to compare health plans from private health insurance organizations that have listed their health plans and drive the health insurance exchange market.

Individual and family health insurance plans that are compliant with the ACA are purchased through public health insurance exchanges (individual and family or "individual market" refers to health insurance that people purchase on their own, as opposed to coverage obtained through an employer or through a government-run program like Medicare or Medicaid).

Additionally, only via these exchanges may individuals qualify for premium subsidies and cost-sharing exemptions, which lower premiums and out-of-pocket expenses for millions of qualified participants. During the open enrollment period for coverage in 2022, more than 14.5 million individuals nationally acquired coverage through the exchanges. Nearly 13 million of the enrolled individuals received premium assistance. Additionally, approximately 5.5 million of the 10.3 million enrollees through the federally controlled exchange HealthCare.gov (used in 33 states) were getting cost-sharing reductions in the health insurance exchange market. To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

Health Insurance Exchange Market Dynamics:

Fluctuating insurance plans and high cost hamper the health insurance exchange market

Research in behavioral economics demonstrates that when given too many options, customers choose options that are of lesser quality. When customers must choose between several health insurance plans, a situation known as “option overload” can be especially troubling for those with inadequate health literacy. Options for a variety of plans may choose not to enroll at all, or they may enroll in less-than-ideal plans.

Consumer research conducted in the early years of the ACA revealed that consumers have trouble comprehending the meaning of MOOP, coinsurance, and deductibles and hampering the health insurance exchange market growth. Many people are unaware of the meaning of coinsurance (a specific amount of expenses that the patient is accountable for), and they find it challenging to comprehend. The expenses the health plan covers and which they are in charge of. When customers select a “dominated” plan, that is, one with the highest premiums, this is a particularly clear illustration of a poor plan choice.

A plan gives less comprehensive coverage for the same or a greater cost than another plan or offers the same protection but at a greater cost, which highly hampers the health insurance exchange market. Participants in a study of University of Michigan staff % of enrollees were in a dominant plan in 2018. A similar issue surfaced in California in 2018, as a result of the discontinuation of the federal government’s cost-sharing reduction (CSR) payments to issuers, which prompted several issuers to sometimes even increase the silver plan rates above the gold plan prices.

Two insurers in California provided silver plans with higher rates than their gold plans, but roughly 20% of customers still selected the more expensive and less comprehensive silver plans, which cost them $460 more in premiums annually on average. Plans with a higher individual deductible of $2,500 or a higher family deductible of $5,000 in comparison to the matching gold plans. One potential remedy for the issues of option overload and inadequate information is standardized planning. Information by reducing the complexity of cost-sharing arrangements and enhancing the comparability of plans, which customers should pay attention to other aspects like premium, provider network, and plan quality.

The ideal amount of plan options to make enrolling easier may change according to age and other factors. In addition, women, people of lower wealth, and those with chronic health concerns are all likely to make nrolment more difficult for older persons than for younger ones when faced with a big choice set these are expected to hamper the market growth globally. Selections with greater expected expenses and a choice of fewer plans are linked to better health in older persons.

Whereas a choice of more than 30 options resulted in lower enrolment. In the uninsured Individuals’ understanding of health insurance decreased when given the option of nine options as opposed to three choices. This was connected to selecting a plan with annual expenses of at least $500 more costly. So choosing Significant plans is a major problem hampering the health insurance exchange market growth during the forecast period.

Health Insurance Exchange Market growth trend

Private exchanges may provide a wider array of retail items, including dental and life insurance. both insurance and no insurance items than can open health insurance exchange markets. There are two private exchange models: to continue playing a role in decision-making both the insurance company and the strategy design. According to how complex Employers desire to participate in benefits design, negotiation, and goods may be priced and modified for the employee collective or particulars.

Various provider and plan design alternatives will be offered by brokers or benefits consultants, which will encourage employers should play a more passive role. Multi-carrier for payors Exchanges that feature specific items on a menu of options run the danger of commoditization, which might lead to price pressure payment margins and drive health insurance exchange market demand globally and drive health insurance exchange market.

Strategic planning of key market players

The frequent changes in coverage witnessed indicated that these organizations have a chance to enhance their retention and financial performance strategies. If there are interruptions in coverage that undermine care continuity, lapses in coverage and subsequent re-enrollment may result in greater expenses and utilization as well as harm to members' health. Payers may take the following steps to enhance customer loyalty and financial performance.

PAPC health plans drive the health insurance exchange market growth

The managed Medicaid market saw the biggest enrollment growth in absolute terms, increasing from around a 7.1million lives in 2020 to 9.8 million lives in 2022 (a CAGR of more than 9%). From 43, there are now 51 providers who provide Medicaid programs. Although PLHPs already have a considerable market share in managed Medicaid (covering around 22% of the population), a number of variables indicate that there is still tremendous opportunity for market share expansion.

For instance, state-by-state Medicaid expansion is still ongoing. (By November 2015, 60% of all Medicaid members were located in the 27 states that have extended Medicaid.) The demand for population health management expertise is also increasing as a result of the switch to value-based payments, and state laws for managed Medicaid programs are favorable for PLHPs.and drive the health insurance exchange market.

Given the favorable circumstances, enrollment in Medicare Advantage plans sponsored by providers is expected to rise (e.g., the adoption of risk-bearing and other innovative payment models and the heightened focus on reducing inpatient utilization rates). However, compared to the individual or Medicaid markets, many providers tend to believe that the Medicare Advantage market offers fewer opportunities for growth.

Medicare Advantage enrollees are few (in comparison to the scale of the individual and Medicaid markets), and payors often provide good service to these customers, giving PLHPs little opportunity for health insurance exchange market plyers.

Health Insurance Exchange Market Segment Analysis:

Based on Type, the Health Insurance Exchange Market is segmented into Public Exchange, Private Exchanges. private insurance exchanges held the largest market share in 2022. Employer health insurance is available through private insurance exchanges that combine internet purchasing, more plan options, benefits administration, and cost-cutting techniques.

A private health exchange commonly referred to as a health insurance market is a tool that enables users to look through and buy health insurance policies. This kind of online exchange or marketplace, which is run by a private corporation, often offers a range of health insurance alternatives accessible in regions and drives the health insurance exchange market.

Any time of the year, as a small company owner, you may utilize a private health exchange to get group health insurance for both you and your staff. You can have a greater chance of finding the ideal small market leader health insurance plan for the particular requirements of customer organization if they use quotes to compare various plan types. Users might be able to find out more about healthcare tax credit alternatives (if any are available) for small businesses through a private health exchange for employers. These tax credits can be available to some companies that employ less than 25 people.

Through eHealth, a well-known private health exchange with the greatest online range of small company health insurance policies, customers may get group health insurance. To make getting private exchange health insurance as quick, convenient, and educational as possible, eHealth provides a number of tools also some health insurance market driving resones that as Free quotes - small market players homepage, simply enter your ZIP code and the number of employees to quickly receive free, customized, no-obligation quotations for small business.

Through eHealth, a well-known private health exchange with the greatest online range of small company health insurance policies, customers may get group health insurance. To make getting private exchange health insurance as quick, convenient, and educational as possible, eHealth provides a number of tools also some health insurance market driving resones that as Free quotes - small market players homepage, simply enter your ZIP code and the number of employees to quickly receive free, customized, no-obligation quotations for small business.

Simple comparisons - You can simply locate the best coverage choice for your company by comparing the costs of a variety of health insurance plans offered by various insurance providers and provider networks in your area, all in one handy location. Expert guidance - When you use eHealth, customers have access to our qualified health insurance agents, who can assist with your unique queries, offer objective expert advice, and walk you through each stage of our simplified shopping, enrollment, and implementation process are some of the health insurance exchange market driving resonates for small market players.

Health Insurance Exchange Market Regional Insights:

The North American region dominated the market with a 45 % share in 2022. The market for health insurance exchanges has been divided geographically into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. A large portion of the global market for health insurance exchanges is accounted for by North America, with the U.S. making a considerable contribution due to the country's highly developed healthcare system and rising IT use.

Health insurance exchanges are essential for achieving improved healthcare results because they provide a market where different insurance options may be gathered and given to the public for potential sickness coverage. It may be privately held or subject to governmental regulation. Government-controlled markets are often safer and more secure in their objectives, but they also provide fewer advantages and are marginally less profitable than privately managed exchanges. (California, Connecticut, the District of Columbia, Maine, Maryland, Massachusetts, New Jersey, New York, Vermont, and the state of Washington) and one SBM utilizing HealthCare.gov (Oregon) has put some type of standardized plans into place.

In the Year 2022, Maine started enforcing standardized plans. Colorado will put its standard plan policy into effect for Fy 2023. and drive health insurance market demand in North American countries.

Regarding the amount of non-standardized offers that are allowed or restricted, as well as the form of cost-sharing arrangements, these states' rules change greatly. The "value plans" in Maryland and the "standard plans" in New Jersey have lower deductibles, but they don't demand the same amounts in money or percentages for each cost-sharing value. Non-standard layouts are permitted in Maryland. Only non-standard designs are permitted in New Jersey for catastrophe insurance.

The other nine states demand that issuers provide plans with comprehensive standard policies. designs for AV, MOOP, deductibles, and cost-sharing by metal level. These nine states—California, Washington, Oregon, The number of non-standard plans are limited to Connecticut, Maine, Massachusetts, New York, and Oregon all these regions are creating a huge demand in the health insurance exchange market. More details about each region are covered in the report.

Health Insurance Exchange Market Scope: Inquire before buying

| Health Insurance Exchange Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2022 | Forecast Period: | 2023-2029 |

| Historical Data: | 2017 to 2022 | Market Size in 2022: | US $ 5.09 Bn. |

| Forecast Period 2023 to 2029 CAGR: | 8.4% | Market Size in 2029: | US $ 8.96 Bn. |

| Segments Covered: | by Product Type | Public Exchange Private Exchanges |

|

| by Phase | Pre-Implementation Services Implementation/Exchange Infrastructure Delivery Program Management and Independent Verification and Validation (IV&V)/Quality Assurance (QA) Operations & Maintenance |

||

| by End-use | Government Agencies Third Party Administrators Brokerage Firms, & Consultancies |

||

Health Insurance Exchange Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Health Insurance Exchange Market, Key Players are

1. Innovation Inc.

2. Noridian Healthcare Solutions

3. KPMG

4. HP

5. Hexaware – Technologies

6. Deloitte

7. Xerox Corporation

8. Oracle Corporation

9. Maximus

10. Infosys

11. Hcentive, Inc.

12. Deloitte

13. Cognosante, LLC

14. Connecture Inc.

15. Accenture Plc

16. CGI Group, Inc.

17. IBM Corporation

18. Microsoft Corporation

19. Tata Consultancy Services Limited

20. Wipro Limited

21. Hewlett-Packard Enterprise Development LP

Frequently Asked Questions:

1] What segments are covered in the Global Health Insurance Exchange Market report?

Ans. The segments covered in the Health Insurance Exchange Market report are based on Product Type and End User.

2] Which region is expected to hold the highest share in the Global Health Insurance Exchange Market?

Ans. The North America region is expected to hold the highest share in the Health Insurance Exchange Market.

3] What is the market size of the Global Health Insurance Exchange Market by 2029?

Ans. The market size of the Health Insurance Exchange Market by 2029 is expected to reach US$ 8.96 Bn.

4] What is the forecast period for the Global Market?

Ans. The forecast period for the Market is 2023-2029.

5] What was the market size of the Global Market in 2022?

Ans. The market size of the Market in 2022 was valued at US$ 5.09 Bn.