Gaming Market 2025–2032: Cloud Gaming Expansion, Esports Growth, and Immersive Digital Entertainment Transformation

Overview

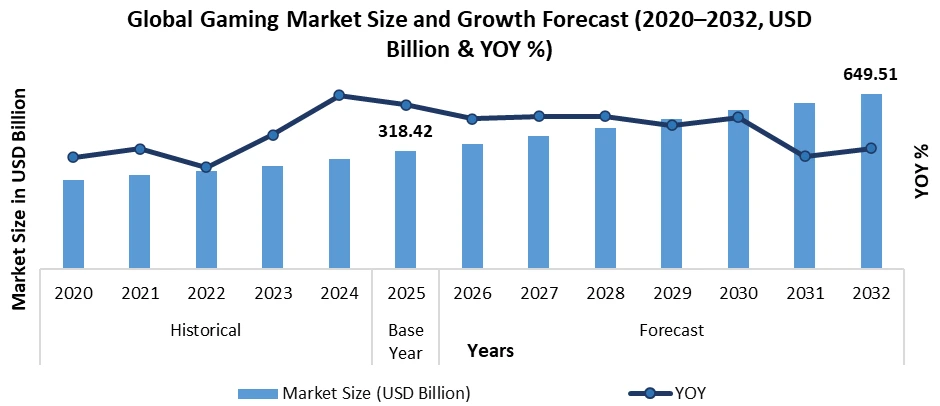

The Global Gaming Market was valued at USD 318.42 billion in 2025 and is projected to reach USD 649.51 billion by 2032, registering a CAGR of 10.72% during the forecast period. According to recent Gaming Industry Analysis, with 3.49 billion gamers worldwide and mobile gaming accounting for more than 49% of total revenue in 2025, supported by rising smartphone penetration, expanding broadband infrastructure, and increasing adoption of digital entertainment platforms.

Global Gaming Market Overview

The Gaming Market Growth is fueled by technological advancements including AI-powered game development, cloud infrastructure, blockchain integration, and immersive AR/VR environments. The Video Game Market has become the dominant segment within the broader digital entertainment ecosystem, contributing the largest revenue share across interactive media industries.

Leading companies such as Microsoft (Xbox), Sony Interactive Entertainment (PlayStation), Tencent Games, and Electronic Arts are increasingly focusing on cross-platform integration, live-service gaming models, and AI-driven personalization to enhance user engagement and maximize lifetime value across the Global market. These companies are leveraging cloud ecosystems, subscription-based gaming services, and advanced analytics to strengthen their market Share and reinforce their competitive positioning within the Gaming Industry.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Gaming Market Key Highlights:

| Market Parameter | Value / Insight | Trend |

| Global Gaming Market Size (2025) | USD 318.42 Billion | ↑ Strong Growth |

| Projected Market Size (2032) | USD 649.51 Billion | ↑ Accelerating |

| Forecast CAGR (2026–2032) | 10.72% | ↑ Expanding |

| Global Gamer Base (2025) | 3.49 Billion Players Worldwide | ↑ Rising |

| Mobile Gaming Revenue Share (2025) | 52%+ of Total Market Revenue | ↑ Dominant |

| Leading Regional Market (2025) | Asia Pacific – Largest Revenue Contributor | ↑ Market Leader |

| Console Market Performance (2025) | 5.5% Rebound Driven by Next-Gen Consoles | ↑ Recovery |

| AI in Gaming Adoption | 30%+ of new NFT/game projects integrate AI | ↑ Rapid Rise |

| Cross-Platform Engagement Boost | 45% Increase in Player Engagement | ↑ Surging |

| Game Streaming Growth | 55% Sector Growth; 20% Audience Surge | ↑ High Expansion |

| Indie Game Market Expansion | 35% Market Share Growth | ↑ Emerging Strength |

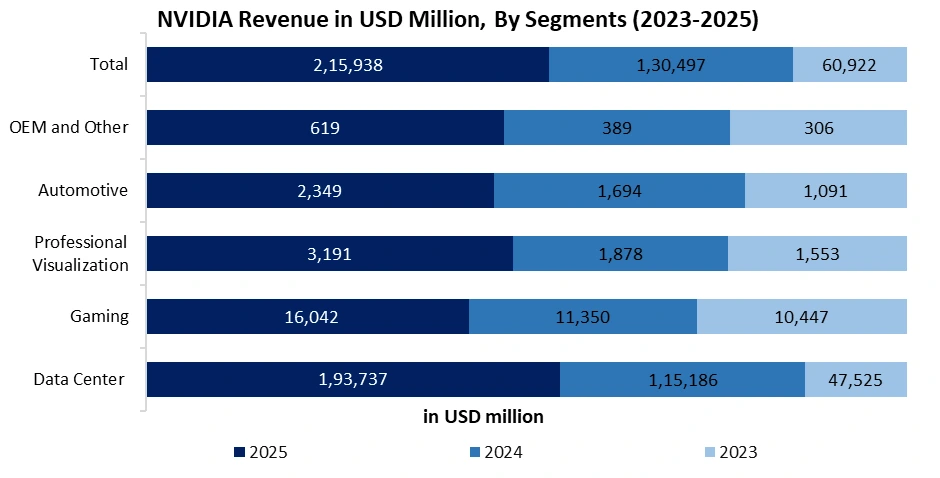

| NVIDIA Gaming Segment Revenue (2025) | USD 16,042 Billion | ↑ Strategic Technology Leader |

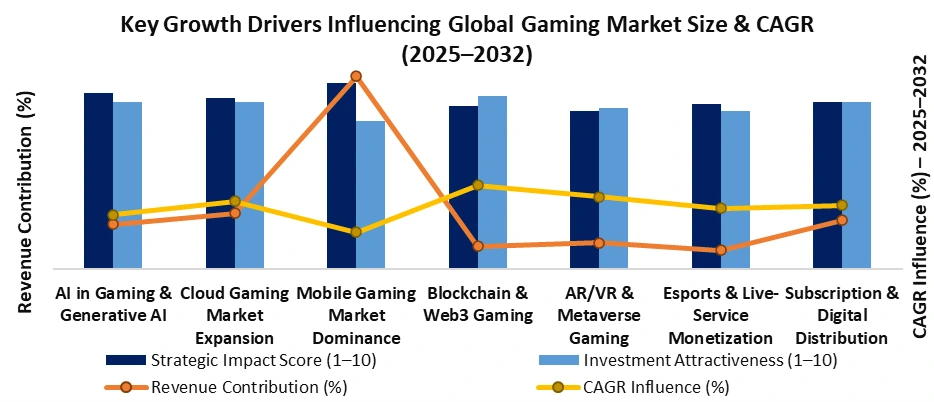

Key Market Drivers for the Gaming Market

• AI in Gaming & Generative AI Revolution

The AI in Gaming Market is transforming content creation, NPC intelligence, real-time personalization, and predictive analytics. Generative AI enables procedural world-building and adaptive gameplay, significantly improving engagement metrics and lifetime value. AI-driven automation is reducing development cycles while enhancing profitability across the Gaming Industry Value Chain.

• Rapid Expansion of the Cloud Gaming

The Cloud Gaming is experiencing exponential growth due to 5G deployment and low-latency streaming capabilities. Cloud-based platforms eliminate high-end hardware dependency, making gaming more accessible and expanding the Online Gaming globally. This shift is a core contributor to the Gaming Industry Growth Rate CAGR.

• Mobile Gaming Market Dominance

The Mobile Gaming accounts for over 50% of total Global market Revenue, driven by freemium models, microtransactions, and in-app purchases. Emerging economies across Asia-Pacific are witnessing strong adoption, making mobile the largest revenue-generating segment within the market Share Analysis.

• Blockchain & Web3 Gaming Industry Growth

The Blockchain Gaming Market and Web3 Gaming Industry are introducing decentralized asset ownership, NFT marketplaces, and play-to-earn ecosystems. Digital asset monetization is creating new income streams within the broader Digital Gaming Market, attracting venture capital and institutional investment.

• AR/VR & Metaverse Gaming Integration

The AR/VR Gaming Market is redefining immersive digital experiences. Metaverse-based gaming platforms enable real-time social interaction, digital commerce, and interoperable gaming environments. These innovations are shaping long-term Gaming Industry Trends 2025–2032.

• Esports Market & Live-Service Monetization

The Esports Market continues to expand through sponsorships, media rights, tournament revenues, and streaming platforms. Battle passes, downloadable content (DLC), and seasonal updates are strengthening recurring revenue models and boosting overall market Growth Rate.

• Subscription & Digital Distribution Models

Gaming subscription ecosystems and digital storefronts are transforming traditional sales models into recurring revenue streams. Subscription-based gaming significantly enhances predictable cash flows and contributes to the Gaming Market Forecast 2032.

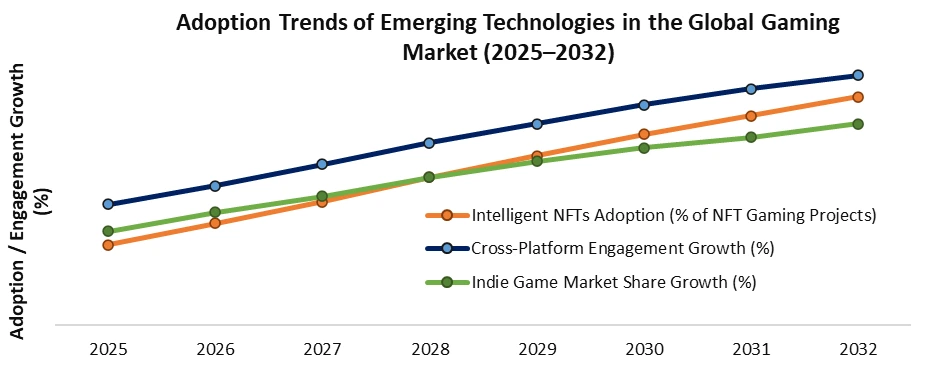

Emerging Trends Shaping the Gaming Market

• Intelligent NFTs (iNFTs): Around 30% of new NFT projects in 2025 incorporate AI, forming a new category of programmable digital assets — making static collectibles obsolete and creating "living assets" that evolve with user interactions.

• Nintendo Switch 2 & Next-Gen Console Surge: The release of Nintendo Switch 2 drove a 5.5% rebound in console sales in 2025, helping halt declines across the gaming hardware category.

• Cross-Platform Gaming: Cross-platform gaming support has boosted player engagement by 45%, ensuring seamless gameplay across consoles, PCs, and mobile devices.

• Indie Gaming Expansion: Indie gaming's market share has expanded by 35%, fueled by accessible development platforms and lower production barriers.

• Game Streaming Growth: The game streaming sector has observed 55% growth, with platforms like Twitch and YouTube Gaming recording a 20% surge in audience size.

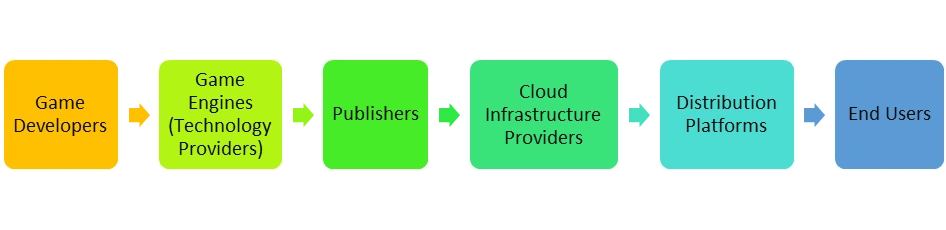

Gaming Market Value Chain Analysis

The Gaming Industry Value Chain plays a critical role in determining profitability, cost structure, revenue flow, and overall market Growth. A structured Gaming Market Ecosystem Analysis includes the following components:

Gaming Market Segmentation Analysis

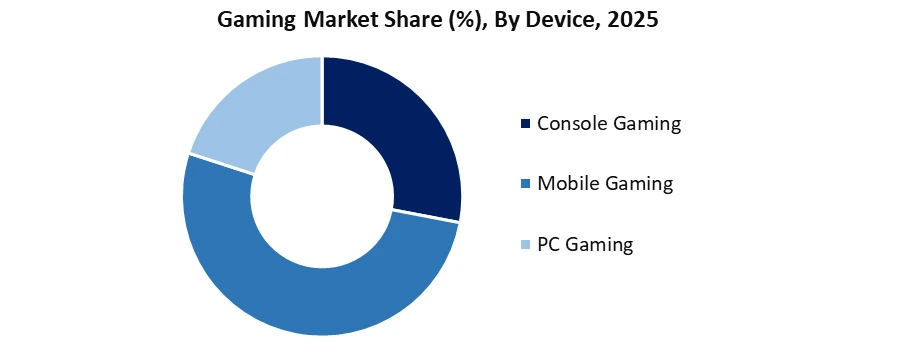

The Mobile Gaming segment dominated the Global Gaming Market, accounting for over 52% of the total Gaming Market Share, driven by smartphone penetration, freemium models, and in-app purchases. Console Gaming ranked second, supported by premium titles and subscription ecosystems, while PC Gaming sustained by esports and digital distribution growth.

Gaming Market Regional Insights

Gaming Market Regional Insights

• Asia Pacific Gaming Market – Market Leader

The Asia Pacific Gaming Market dominates the Global Gaming Market Share, accounting for the largest revenue contribution due to strong performance in the Mobile Gaming Market, esports expansion, and high user penetration in China, Japan, and South Korea. The region remains a core growth engine in the market Forecast 2032.

• North America Gaming Market – Revenue & Innovation Hub

The North America Gaming Market leads in premium console sales, cloud adoption, and the Esports Market. Strong investment in the AI in Gaming Market and the Cloud Gaming Market supports the steady Gaming Industry Growth Rate (CAGR) across the United States and Canada.

• Europe Gaming Market – Regulatory & Console-Driven Growth

The Europe Gaming Industry shows stable expansion driven by console demand, digital downloads, and subscription ecosystems. Regulatory developments around monetization models influence overall market Revenue and competitive dynamics.

• South America Gaming Market – Emerging Growth Opportunity

The South America Gaming Industry is witnessing rapid expansion in the Online Gaming, supported by rising smartphone penetration and affordable internet access. The region presents strong market Investment Opportunities.

• Middle East & Africa Gaming Market – High Future Potential

The Middle East & Africa Gaming Market is emerging as a fast-growing region, driven by government-backed esports initiatives, youth demographics, and digital transformation strategies, strengthening long-term Gaming Industry Future Outlook.

Regulatory Landscape in the Global Gaming Market

• Monetization & Loot Box Regulations

Stricter EU and US regulations on loot boxes are reshaping revenue models within the In-Game Purchases Market, directly impacting Gaming Market Revenue, particularly in the Mobile Gaming Market and Console Gaming Market.

• NFT & Web3 Gaming Restrictions

Compliance measures around digital assets and crypto transactions are influencing growth in the Blockchain Gaming Market and Web3 Gaming Industry, affecting overall Gaming Market Investment Opportunities.

• Data Protection & Cybersecurity Laws

Privacy regulations are transforming operations within the Online Gaming Market and Cloud Gaming Market, increasing compliance costs while strengthening long-term Gaming Industry Growth Rate (CAGR).

• App Store Commission Policies

Revenue-sharing models in the Digital Game Distribution Market significantly impact profitability and Gaming Market Share, especially within the dominant Global market Size driven by mobile platforms.

Gaming Market Competitive Landscape

The Global market Competitive Landscape is highly consolidated, with leading players driving innovation across console, mobile, cloud, and AI-powered ecosystems. Sony Interactive Entertainment and Microsoft dominate the console and subscription segments, strengthening their Gaming Market Share through exclusive titles and cloud integration. Tencent Holdings leads the Mobile Gaming Market and holds strategic stakes in global studios. Nintendo maintains strong brand equity in hardware-software integration. Electronic Arts focuses on live-service monetization and esports expansion. Meanwhile, NVIDIA Gaming segment had a revenue of USD 16,042 Billion in 2025, plays a critical role in the Cloud Gaming Market and AI in Gaming Market by providing advanced GPUs and real-time rendering technologies, strengthening the overall Gaming Industry Growth Rate.

Recent Key Development

| Date | Company | Development | Impact |

| March 2025 | Government of Morocco & Government of France | Launched the “Video Game Incubator” program supporting nine startups with structured training in business, production, branding, and financial planning. | Accelerated regional game development capabilities, fostering innovation and strengthening the European and North African gaming ecosystem. |

| November 2024 | Apple Inc. | Launched five new titles including Skate City: New York, Talking Tom Blast Park, and FINAL FANTASY IV (3D Remake) to expand its family-focused gaming portfolio across Apple devices. | Strengthened Apple Arcade’s value proposition with ad-free, in-app purchase–free experiences, enhancing user retention and ecosystem stickiness. |

| May 2024 | Rovio Entertainment Corporation | Introduced Angry Birds for Automotive, enabling gameplay in vehicles with Google built-in such as the Volvo EX90, integrated with cloud-save functionality. | Expanded gaming into automotive infotainment systems, enhancing cross-device engagement and reinforcing omnichannel gaming experiences. |

| May 2024 | Microsoft Corporation | Announced plans to launch an online store for mobile-game consumables, creating an alternative distribution channel outside traditional app stores. | Challenged existing app store commission models, potentially improving publisher margins and reshaping digital game distribution economics. |

| November 2023 | Activision Blizzard | Officially launched Warcraft Rumble, a free-to-play mobile action strategy game, globally on Android and iOS following earlier regional soft launches. | Strengthened mobile gaming presence and diversified franchise monetization within the competitive free-to-play ecosystem. |

Gaming Market Scope: Inquire before buying

| Gaming Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 318.42 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 10.72% | Market Size in 2032: | USD 649.51 Bn. |

| Segments Covered: | by Device | Console Gaming Mobile Gaming PC Gaming |

|

| by Game Type | Action Shooter Role-Playing Sports & Racing Others |

||

| by Platform | Online Gaming Offline Gaming |

||

| by Technology | Cloud Gaming AR/VR Gaming AI-Powered Gaming Blockchain/Web3 Gaming |

||

| by Revenue Model | Free-to-Play (F2P) Subscription-Based Gaming In-Game Purchases & Microtransactions Premium / Pay-to-Play |

||

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and Rest of ME&A)

South America (Brazil, Argentina, and Rest of South America)

Key Players/Competitors Profiles Covered in the Gaming Market Report in Strategic Perspective

1. Sony Interactive Entertainment

2. Microsoft Corporation

3. Nintendo Co., Ltd.

4. Activision Blizzard

5. Electronic Arts (EA)

6. Ubisoft Entertainment

7. Tencent Holdings Limited

8. NVIDIA

9. NetEase, Inc.

10. Take-Two Interactive Software

11. Valve Corporation

12. Epic Games

13. Square Enix Holdings Co., Ltd.

14. Capcom Co., Ltd.

15. CD Projekt S.A.

16. Bandai Namco Entertainment Inc.

17. Krafton, Inc.

18. Sega Enterprises, Inc.

19. Apple, Inc.

20. The Walt Disney Company

21. Rovio Entertainment Corporation

22. Roblox Corporation

23. MiHoYo

24. Supercell

25. Embracer Group

26. Amazon