Food Texture Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2034

Overview

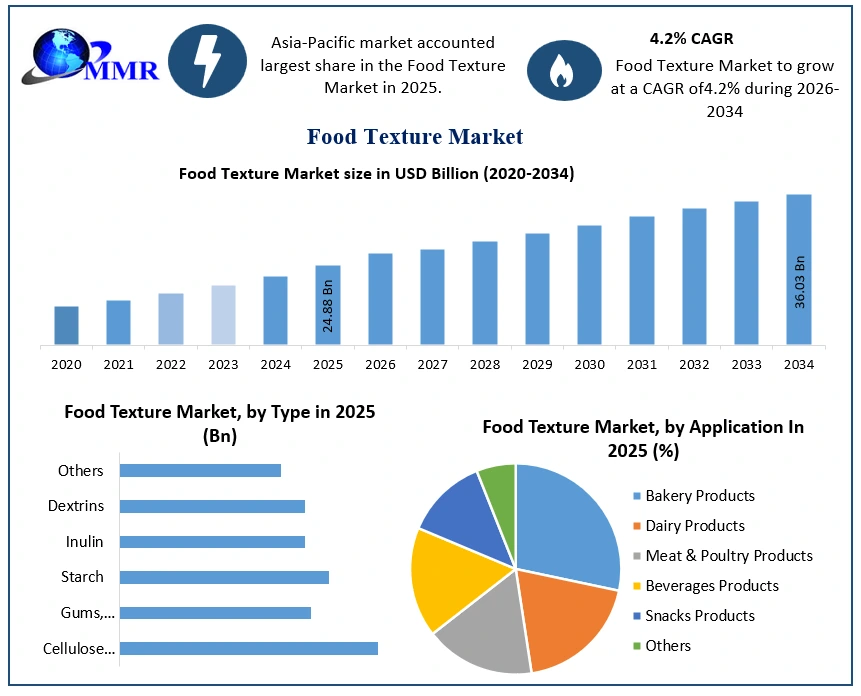

Food Texture Market size was valued at USD 24.88 Bn. in 2025 and the total Food Texture revenue is expected to grow by 4.2 % from 2026 to 2034, reaching nearly USD 36.03 Bn.

Food Texture Market Overview:

The Food Texture is a major criterion used by consumers to judge the quality and freshness of food. Texture increases the sensory experience of food and is a key component in food and beverage products across the world. Food and beverage industries are increasingly using texturizing agents in a variety of processed foods due to the advantages they provide. Food Texture assists in maintaining the product’s nutrients, preventing the growth of microbes, and increasing the product’s shelf life. It also enhances the dish’s appearance and flavour which has a good impact on food sales. The global food texture market has grown significantly in recent years and is expected to grow in the coming years. Factors such as rising customer preferences for low-fat, well-textured foods, increased innovation in the food processing industry, and cost benefits afforded by substitutes all contribute to the demand for food texture ingredients as a key food additive.

To know about the Research Methodology :- Request Free Sample Report

Report Scope:

The Food Texture market is segmented based on functionalities, application, and Region. The growth amongst these segments will help to analyze the industries and provide the users with a valuable market overview and market insights to make strategic decisions for identifying core market applications. The research study provides an in-depth analysis of the market and contains meaningful insights, facts, historical data, and statistically supported and industry-validated market statistics. It also includes estimates based on an appropriate set of assumptions and methodologies.

Bottom-up approache has been used to collect the data and analyse the market to figure out market size by volume and value by mentioned segments. Major Key Players in the Food Texture market are identified through secondary research and their market revenues are determined through primary and secondary research. Secondary research involved a study of the top manufacturers’ annual and financial reports, while primary research was done through interviews with company key persons and industry professionals such as experienced front-line staff, CEOs, and marketing executives. The study gives insight into the growth dynamics of the Food Texture market in regions such as the Middle East and Africa, Asia Pacific, Europe, North America, and Latin America. Europe is expected to witness significant growth owing to the increasing demand for jams, confectionaries, and jellies in this region.

The report contains strategic profiling of top key players in the market, a wide-ranging analysis of their core competencies, and their strategies like new product launches, growths, agreements, joint ventures, partnerships, and acquisitions which apply to the businesses. Key Players in the food texture market are increasingly offering customized solutions to the food and beverage sector due to the application-specific desirability of several texturizing functions. Product innovation is a go-to strategy for companies to stay relevant in the market. The leading players in the market are Penford Corporation, Archer Daniels Midland Co., Ajinomoto Co. Inc, Asland Inc., Cargill Inc, Cp Kelco, Estelle Chemicals, E.I. Dupont De Nemours & Company, and FMC Corporation. They are continuously strategizing on mergers & acquisitions for the expansion of their market share and growth opportunities during the forecast period.

Food Texture Market Dynamics:

The growing population and rising demand for textured food in urban areas

Increasing urban population and changing lifestyles of individuals because of the rising disposable incomes are the key factors that are boosting the Food Texture market growth. In recent years, growth in the number of employees at work has resulted in less time for meal preparation, which necessitates the consumption of high-quality foods for better health. Furthermore, Convenience food is becoming increasingly significant to consumers in developed countries. These products are becoming popular, particularly among students and working professionals. Consumers in developed nations are increasingly preferring convenience or ready-to-eat products over fresh foods, which is boosting the frozen food production sector. 56% of consumers in the US are willing to pay more for clean-label ready-to-eat meals. As a result, the rise in demand for convenience and ready-to-eat foods is expected to increase the growth of the worldwide food texture market during the forecast period.

Innovation in Food Texture

Consumers throughout the world want more naturalness and want to reduce their sugar consumption. In North America, Consumer interest in clean labels continues to impact texture replacement choices when it comes to sugar reduction, as well as protein enhancement. Texture techniques can improve the sensory experience as brands seek to minimize costs and make their products more affordable to everybody. Food texture plays a pivotal role in how consumers experience food and beverages. As per research, 81 % of consumers in France choose their ice creams which have a different texture. Furthermore, the Emulsifiers are used to combine two components to create a stable and homogeneous result. It is widely utilised in the making of bakery goods, chocolates, and margarine. Emulsifying agents provide the proper amount of stability and flavour.

Modified Food texture provides cost benefits

Modifying food texture while delivering an extra special experience to consumers saves money and provides cost benefits to manufacturers. For example, internal experts in India note how adding a little texture has allowed some manufacturers to reduce the actual fruit pulp content in their fruit drinks and provide a satisfying mouthfeel without compromising flavours. This can be accomplished by adding pectin or citrus fibre. Fluffy, foamy, and creme textures may also give a luxurious, dessert-like feel to beverages. This is done by adding additional air to a recipe. A great example of an effective texture alteration is Dalgona coffee. The drink, which originated in South Korea and spread through social media, is now popular worldwide. It has produced a whipped foam texture trend that can rival coffee shop baristas, but consumers may enjoy it anywhere. The same concept may be used to make dessert-style yoghurts, either dairy or plant-based, which are becoming increasingly popular. Food texture will continue to be a big theme and will provide significant market growth over the forecast period.

The negative effects of food texture are hampering market growth:

Different textures can make food look more or less sweet or salty, even if the sugar or salt content stays the same. This effect can have a direct impact on food texture. The high-calorie content, energy loss, and greater allergenic content are only a few of the disadvantages. Furthermore, the side effects associated with food texture are hampering the growth of the market during the forecast period. Key Players in the global food texture market are increasingly shifting towards the development of safe synthetic chemicals. This will very likely open up significant growth opportunities for the food texture market.

Food Texture Market Segment Analysis:

By functionalities, the Emulsifying agent segment had the largest market share of more than 40% in 2023. Emulsifying agents are substances that are added to liquid materials to stabilise the mixture. Emulsification is used to make food more aesthetically attractive while also improving flavour and texture. According to Understanding FoodAdditives.org, monoglycerides are one of the most popular forms of emulsifying agents. Lecithin, a monoglyceride present in egg yolks, is a common emulsifier. It is widely utilised in the manufacturing of baked products, chocolates, and margarine.

The Thickening Agents segment is expected to grow at a significant growth rate during the forecast period. A thickening agent or thickener is a substance that may raise the viscosity of a liquid without significantly altering its other properties. Edible thickeners are often used to thicken sauces, soups, and puddings without affecting their taste.

By application, the dairy products segment had 32.1 % of the food texture market in 2025. Demand for Food textures for Manufacturing Dairy products rise by 2.6 % during the forecast period owing to the growing demand for creamy and crystal-free liquid or frozen items made with milk. Consumers want dairy products to be smooth, creamy, and devoid of standing moisture, whether liquid or frozen.

However, the Processed Foods segment is expected to develop at a CAGR of 3.8 % throughout the forecast period. Food Texture demand for Meat Products increased by 2.7 % in 2025. This is due to increased demand for processed meat products and a preference for the palatability of the products while eating.

Food Texture Market Regional Insights

Asia’s preferences for food texture have boosted the market growth over the forecast period. Emerging countries in the region such as India and China will experience a surge in the demand for texturizing agents owing to the increasing consumption of processed foods. 78.6 % of consumers in India and 72 % of Chinese consumers surveyed said that texture claims in food and drinks influence their purchase decision. Economic conditions provide a profitable market for food texture. Other elements propelling the region’s growth include the abundant supply of raw materials and cheap labour, a rising retail sector, and a growing food and beverage industry.

In India, a highly thick and creamy mouthfeel in beverages such as lassi, mango cocktails, and flavoured milk is seen as healthier and contains more of the desired protein or fruit. Mouthfeel preferences may differ in China to fulfil the demands of different consumers.

North America Food Texture Market is expected to grow at a rapid rate over the forecast period. owing to the increase in innovations in food solutions, and the demand for ingredients providing textures to food. North America is a land of opportunity for food texture, and manufacturers are experimenting with it. In North America, the demand for food texture is growing in many traditional vegetarian foods, especially in the frozen food section. Furthermore, the presence of large food packaging companies in this region is accelerating the Food Texture market growth during the forecast period.

The objective of the report is to present a comprehensive analysis of the Food Texture market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The report also helps in understanding the Food Texture market dynamics, and structure by analyzing the market segments and projecting the Food Texture market size. Clear representation of competitive analysis of key players by product, price, financial position, product portfolio, growth strategies, and regional presence in the Food Texture market make the report investor’s guide.

Food Texture Market Recent Industry Development

| Date | Company | Development | Impact |

|---|---|---|---|

| 02 June 2026 | Cargill | The company executed a €25 million modernization project at its Baupte, France facility, introducing Mechanical Vapor Recompression technology for hydrocolloid processing. | The upgrade improves supply reliability and process efficiency while cutting localized site emissions by approximately 45% annually. |

| 06 February 2026 | Ingredion Incorporated | The company reported a 16% operating income surge within its Texture & Healthful Solutions division, heavily supported by infrastructure investments like its modernized Indianapolis specialty starch facility. | The financial outperformance validates a strategic corporate pivot toward high-value texture innovation and clean-label portfolios over traditional sweetener lines. |

| 31 October 2025 | Roquette | The company introduced AMYSTA™ L 123, a next-generation thermally soluble pea starch developed using a patented, chemical-free processing method. | The launch enables food brands to achieve improved process control, stable texturizing performance, and cleaner ingredient labels across ready-to-mix products. |

| 30 October 2025 | Ingredion Incorporated | The developer entered into a strategic commercialization partnership with biotechnology startup Cosaic focused on a novel fermentation-derived texturizer. | The alliance yields a specialized emulsion ingredient capable of introducing dairy-like creaminess and smooth mouthfeel to plant-based formulations without animal components. |

Food Texture Market Scope: Inquire before buying

| Global Food Texture Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 24.88 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 4.2 % | Market Size in 203:4 | USD 36.03 Bn. |

| Segments Covered: | by Product | Natural Synthetic |

|

| by Type | Cellulose Derivatives Gums, Pectins, Gelatins Starch Inulin Dextrins Others |

||

| by Application | Bakery Products Dairy Products Meat & Poultry Products Beverages Products Snacks Products Others |

||

| by functionalities | Thickening Agents Gelling Agents Emulsifying Agents Stabilizing Agents Other Agents |

||

Food Texture Market, by Region

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

North America (United States, Canada and Mexico)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players

1. CP Kelco (U.S.)

2. Tate and Lyle PLC (U.K.)

3. Ingredion Inc (U.S.)

4. DuPont (U.S.)

5. Kerry Group (Ireland)

6. JELU-WERK (Germany)

7. Cargill, Inc (Wayzata, MN)

8. Ajinomoto Co., Inc. (Japan)

9. Archer Daniels Midland Company (U.S.)

10. Penford Corp. (U.S.)

11. Fiberstar Inc. (River Falls, Wisconsin)

12. SELECTAROME (Grasse)

13. Willy Benecke GmbH (Germany)

14. Jost Chemicals GmbH (U.S.A)

15. SM-Service Ltd. (U.S.)

FAQs:

1. Which is the potential market for Food Texture in terms of the region?

Ans. In the Asia Pacific region, the increasing consumption of processed foods is expected to drive the market.

2. What is expected to drive the growth of the Food Texture market in the forecast period?

Ans. The growing population and rising demand for textured food in urban areas will fuel the market’s growth over the forecast period.

3. What is the projected market size & growth rate of the Food Texture Market?

Ans. The Food Texture Market size was valued at USD 24.88 Bn. in 2025 and the total Food Texture revenue is expected to grow by 4.2 % from 2026 to 2034, reaching nearly USD 36.03 Bn.

4. What segments are covered in the Food Texture Market report?

Ans. The segments covered are functionalities, application, Product, Type and Region.