Esports Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

The Esports Market size was valued at USD 4.14 Billion in 2024 and the total Esports revenue is expected to grow at a CAGR of 9.04% from 2025 to 2032, reaching nearly USD 8.28 Billion.

Esports Market Overview:

Esports, short for electronic sports, transforms online gaming into an engaging spectator sport akin to traditional athletics. Viewers watch skilled video gamers compete in virtual environments, mirroring the excitement of observing top athletes like Lebron James or Steph Curry in physical sports. This industry goes beyond traditional sports-related games to include popular titles like League of Legends, Counter-Strike, and Dota. Individual players can stream their gameplay for income or join larger organizations to compete for lucrative cash prizes. Player-fan connections flourish through social media and live-streaming platforms, with fans avidly following their favourite teams in regional and global tournaments. The esports ecosystem, supported by diverse technology platforms, services, events, analytics tools, and substantial investor capital, continues to grow dynamically.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Esports Market Dynamics

Esports represents a thriving global industry where highly skilled video gamers engage in competitive play. Similar to traditional sports that encompass various competitions like baseball, basketball, and football, esports features tournaments spanning a diverse array of video games. Contrary to misconceptions, esports is not confined to basements but is a legitimate, globally expanding, and investable industry. Impressively, over 380 million people worldwide actively watch esports events, both online and in-person. Notably, the 2016 world finals of the popular esports game League of Legends drew more viewers (43 million) than the NBA Finals Game 7 in the same year (31 million). With its fragmented landscape and digital platform, the esports sector presents numerous opportunities for monetization.

2020 Most Watched Esports on Twitch

| Sr No | Title | Total Hours | Esports Hours |

| 1 | League of Legends | 87.8 Mn | 21.2 Mn |

| 2 | Dota | 34.3 Mn | 16.7 Mn |

| 3 | Counter Strike | 23.3 Mn | 9.4 Mn |

| 4 | Hearthstone | 39.4 Mn | 9.3 Mn |

| 5 | Heroes of Strom | 10.4 Mn | 2 Mn |

Current Monetization Strategies

A decade ago, packaged home-console software sales accounted for 64% of the global gaming market, but this share has dwindled to 30%. The inclusion of esports in the 2022 Asian Games marks a pivotal moment, allowing gaming companies to diversify revenue streams akin to media companies, incorporating avenues such as advertising, ticket sales, and shares of TV rights. In the coming year, esports is poised to reach approximately $700 million, reflecting a notable industry growth of 41% compared to the previous year and a significant increase from the $325 million recorded in 2015. It's crucial to note that the 2017 figure excludes data related to betting or fantasy esports. Projections indicate that revenues will further surge to $1.5 billion by 2020, indicating a robust Compound Annual Growth Rate (CAGR) of 35.6% from 2015 to 2020.

The Esports Market is witnessing a surge in engagement from renowned gaming and tech sponsors, showcasing a notable transition among lifestyle brands and non-endemic brands, previously unassociated with the gaming industry, as they shift from experimental approaches to dedicated Esports budgets. Simultaneously, local teams, leagues, and events are seizing the opportunity to leverage new marketing budgets for connecting with the Esports audience.

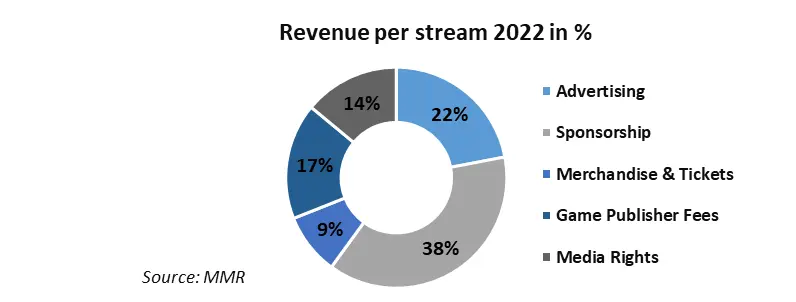

Within the Esports Market, sponsorships emerged as the dominant force, constituting a substantial 38% of the total revenue. The Esports Market experienced significant growth in sponsorship revenues, poised to reach $655 million by 2020. This surge was notably driven by the entry of new brands, particularly from lifestyle sectors, into the dynamic Esports arena. Whalen Rozelle, the former Director of Esports at Riot Games, the developer of League of Legends, underscored the evolving landscape, emphasizing, in the beginning, they used to have to explain what Esports was, and then they had sponsors and brands coming directly to audience. They also saw a shift in companies being more selective and trying to align directly with pro teams. They were always talking to different companies, and if they wanted to focus on a specific market or they had a smaller budget, they pointed them to good teams that fit their needs.

Upcoming Esports Trends

Similar to the NFL, NBA, MLB, and NHL, which adhere to a franchise model with limited membership in their respective sports, the Esports Market in North America is following a comparable trajectory. A recent announcement from Riot regarding their League of Legends title has solidified a franchise model for the North American league, introducing ten spots, each carrying a hefty price tag of $10 million for entry. Activision's Overwatch is also currently undergoing the franchising process. In Europe, the Esports Market is likely to embrace a promotion and relegation model, drawing on the region's familiarity with such sporting systems observed in leagues like the UEFA Champions League.

With franchising poised to become the dominant model, elite teams and organizations within the Esports Market are set to evolve into revenue-generating machines. However, entities without franchise spots will need to explore revenue avenues in secondary leagues or establish themselves in titles yet to undergo franchising. These teams won't enjoy access to substantial revenue-sharing deals, akin to those in League of Legends, and will have to concentrate on competing in secondary leagues that offer smaller cash prizes and sponsorship opportunities. While this consolidation phase may present initial challenges, it is considered a necessary stride forward for the Esports Market's continued growth and market refinement.

The global health crisis induced by COVID-19 has left an indelible mark on various facets of human life, triggering significant disruptions across multiple business sectors, notably impacting the esports market. Leagues and tournaments, integral components of the esports market, grappled with postponements and cancellations as the pandemic unfolded, compelling a paradigm shift toward virtual platforms for event hosting due to the closure of physical stadiums. In the face of the challenges posed by COVID-19, 8% of live events within the esports market were cancelled, with 53% transitioning to virtual platforms, 26% undergoing rescheduling, and 13% proceeding as originally scheduled. Despite these disruptions, the Esports Market demonstrated moderate growth in 2020.

Prominent tournaments such as EPICENTER Major 2022, Combo Breaker, and the Pokémon Championship Series, initially slated for March to May, bore the brunt of cancellations, impacting vital revenue streams such as ticket sales and merchandising, contributing to a discernible downward trend in the first half of 2022. Additional tournaments, including ESL Americas Pro League, California Overwatch League, and ESL One Rio 2022 Counter-Strike, faced postponements. A notable trend emerged as the industry swiftly adapted to online formats, a strategic response to lockdowns and quarantine measures, resulting in a notable surge in viewership on streaming platforms. With the gradual easing of lockdowns and the lifting of restrictions, the Esports Market experienced steady growth in 2022. The ongoing influx of investments into the esports industry is poised to play a pivotal role in propelling its sustained development during the forecast period.

Esports Market Segment Analysis

The sponsorship segment has established itself as the driving force behind the esports market's global revenue, commanding a significant share exceeding 39.0% in 2024. Sponsorships provide dynamic avenues for brands to directly engage with potential customers across diverse online and offline media channels. Employing innovative approaches such as booths, interactive advertising, posters, freebies, video displays, and more allows brands to precisely target their audience. Esteemed brands like Nvidia Corporation, Red Bull, BMW AG, The Coca-Cola Company, and the U.S. Air Force have proactively entered into sponsorship deals with esports leagues and teams.

The escalating competition within the sponsorship industry has prompted brands to seek distinctiveness and authenticity through engagements in the esports and gaming realm. In response to this trend, many non-endemic brands have ventured into esports by leveraging digital extensions of their existing traditional sponsorship relationships, as exemplified by football seamlessly integrating with the esports extension of FIFA.

The media rights segment is poised to exhibit the highest Compound Annual Growth Rate (CAGR) of over 22.0% throughout the forecast period, emerging as a pivotal revenue-generating sector within the esports market. Media rights encompass the revenue disbursed to teams, leagues, and event organizers for acquiring the broadcasting rights to showcase esports content on various channels. This segment is anticipated to yield substantial revenue due to the regular occurrence of numerous individual leagues, championships, and events, which are frequently broadcasted on diverse streaming platforms. Twitch Interactive, Inc. stands out as a prominent platform for live streaming, attracting fans to witness major tournaments. Notably, Twitch experienced a surge in viewership, with fans spending 26 billion hours watching streamers in 2022, reflecting a 45% increase compared to 2021.

Furthermore, in March 2022, Rooter Sports Technologies Private Limited made a strategic move by acquiring the media rights for all intellectual properties (IPs) of Sky Esports for a one-year duration. Sky Esports, a leading esports tournament organizer in South Asia with self-owned IPs, witnessed Rooter Sports gaining the rights to stream competitions in India across multiple languages, including English, Hindi, Bengali, Kannada, Tamil, Malayalam, and Telugu. These mergers and acquisitions are expected to be instrumental in driving the growth of the media rights segment during the forecast period.

In March 2022, Rooter Sports Technologies Private Limited made a strategic move by acquiring the media rights for all intellectual properties (IPs) of Sky Esports for a one-year duration. Sky Esports, a leading esports tournament organizer in South Asia with self-owned IPs, witnessed Rooter Sports gaining the rights to stream competitions in India across multiple languages, including English, Hindi, Bengali, Kannada, Tamil, Malayalam, and Telugu. These mergers and acquisitions are expected to be instrumental in driving the growth of the media rights segment during the forecast period.

Esports Market Regional Analysis

North America, spearheaded by the U.S., has firmly established its dominance in the esports market, securing a significant revenue share that surpassed 29.0% in 2024. This region has consistently held a leading position in the market for several decades, and the outlook indicates expected sustained growth and increased investment. Notably, the Overwatch League and the franchised North America League of Legends Championship Series (NA LCS) are expected to be major contributors to this ongoing success. The concerted efforts of various stakeholders, including leagues, players, game developers, streaming platforms, and TV networks, have collectively transformed esports into a robust multi-million-dollar business in the U.S.

At the forefront of nurturing the esports ecosystem in North America is the North America Scholastic Esports Federation (NASEF). This organization plays a pivotal role in driving the industry's development by actively organizing tournaments tailored for students. NASEF also extends support to high schools, facilitating the establishment of esports clubs, and offers mentorship and coaching programs. Through these initiatives, NASEF contributes significantly to fostering the growth, resilience, and sustainability of the esports market in the region.

The Asia Pacific is poised to experience a remarkable growth rate of over 27.0% during the forecast period. The escalating number of internet users and the burgeoning popularity of mobile gaming have become pivotal drivers of the esports industry's growth in the region. China, having recognized esports as an official sport since 2003, has witnessed the creation of professional opportunities for esports operators in the country. South Korea, renowned as a hub for esports, provides comprehensive infrastructure for gamers, including coaches, gaming houses, analysts, and culinary staff. In April 2022, the Korean Esports Association (KeSPA) inked a three-year sponsorship deal with SK Telecom. This strategic agreement designates SK Telecom as the official sponsor of KeSPA and involves the training of the Korean esports team for the upcoming Asian Games. Such proactive initiatives and advancements are poised to fuel further growth in the esports market during the forecasted period.

Esports Market Scope: Inquire before buying

| Global Esports Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 4.14 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 9.04% | Market Size in 2032: | USD 8.28 Bn. |

| Segments Covered: | By Gender | Male Female |

|

| By Audience | Regular Viewers Occasional Viewers |

||

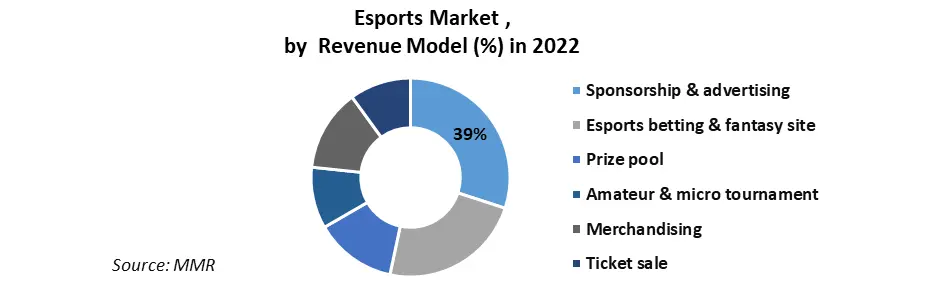

| By Revenue Model | Sponsorship & advertising Esports betting & fantasy site Prize pool Amateur & micro tournament Merchandising Ticket sale |

||

Esports Market by Region:

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Esports Market, Key Players:

North America:

1. Activision Blizzard (California, USA)

2. Electronic Arts (EA) (California, USA)

3. Take-Two Interactive Software (New York, USA)

4. Riot Games (California, USA)

5. Cloud9 (California, USA)

Europe:

6. Fnatic (United Kingdom)

7. Team Vitality (Paris, France)

8. G2 Esports (Berlin, Germany)

9. Natus Vincere (Na'Vi) (Ukraine)

10. Astralis Group (Denmark)

Asia Pacific:

1. T1 Entertainment & Sports (South Korea)

2. Gen.G Esports (South Korea)

3. Invictus Gaming (IG) (China)

4. Team Flash (Singapore)

Latin America:

1. Isurus Gaming (Argentina)

2. All Knights (Mexico)

3. Infinity Esports (Colombia)

Middle East & Africa:

1. Anubis Gaming (Egypt)

2. Nasr Esports (United Arab Emirates)

Global:

1. FaZe Clan (California)

2. Team Liquid (Netherlands )

3. 100 Thieves (California)

4. Counter Logic Gaming (CLG) (California)

FAQs:

1. Which region has the largest share in Global Esports Market?

Ans: North America region holds the highest share in 2024.

2. What was the Global Esports Market size in 2024?

Ans: The Global Esports Market size was USD 4.14 Billion in 2024.

3. What segments are covered in Global Esports market?

Ans: Global Esports Market is segmented into Gender, Audience, Revenue Model and region.

4. Who are the key players in Global Esports market?

Ans: The important key players in the Global Esports Market are – Activision Blizzard (California, USA), Electronic Arts (EA) (California, USA), Take-Two Interactive Software (New York, USA), Riot Games (California, USA), Cloud9 (California, USA) and Others.

5. What is the study period of this market?

Ans: The Global Esports Market is studied from 2024 to 2032.