Global Engineering Plastics Market by Type (Acrylonitrile Butadiene Styrene (ABS), Polyamide (PA), Polycarbonate (PC), Thermoplastic polyesters (PET/PBT), Polyacetals (POM), Others), End User (Automotive & transportation, Electrical & electronics, Industrial & machinery, Packaging, Others) - Forecast to 2032

Overview

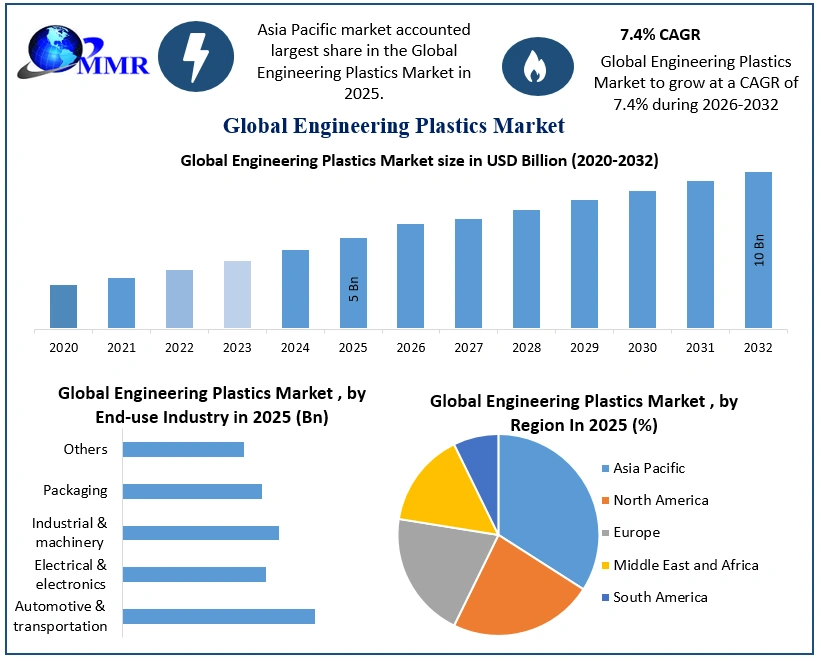

Global Engineering Plastics Market size was valued at USD 125.10 Bn. in 2025 and the total Global Engineering Plastics Market revenue is expected to grow at a CAGR of 7.4% from 2025 to 2032, reaching nearly USD 206.20 Bn. by 2032.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Global Engineering Plastics Market Segment Analysis:

Engineering Plastics Market Regional Insights:

Asia Pacific dominated the Engineering Plastics Market in 2025 and is expected to maintain its leading position throughout the forecast period, driven by its strong manufacturing base, rapid industrialization, and expanding automotive, electrical & electronics, and consumer goods industries. China, Japan, South Korea, and India account for a substantial share of regional demand due to their large-scale production of automobiles, electric vehicles, consumer electronics, industrial machinery, and electrical equipment. The region also benefits from the presence of leading engineering plastics manufacturers, abundant raw material availability, cost-effective manufacturing capabilities, and increasing investments in advanced polymer production. Furthermore, government initiatives supporting electric mobility, renewable energy, and industrial automation are accelerating the adoption of high-performance engineering plastics across multiple end-use industries.

North America is expected to register the fastest growth during the forecast period, supported by increasing demand for lightweight materials in electric vehicles, aerospace, medical devices, and industrial automation applications. Growing investments in sustainable polymers, advanced composites, and high-performance engineering plastics, coupled with continuous innovation in additive manufacturing and precision engineering, are driving regional market expansion. Europe continues to account for a significant market share owing to stringent fuel efficiency and carbon emission regulations, increasing adoption of lightweight automotive materials, and strong demand from the automotive, aerospace, and electrical & electronics sectors. Latin America is witnessing steady growth due to expanding automotive manufacturing, improving industrial infrastructure, and increasing investments in consumer goods and packaging industries. Meanwhile, the Middle East & Africa is expected to experience gradual growth, supported by industrial diversification initiatives, growing infrastructure development, rising demand for engineering plastics in construction and electrical applications, and increasing investments in manufacturing and petrochemical industries.

Global Engineering Plastics Market Recent Developments:

| Date | Recent Development |

| 26 Jun 2025 | BASF SE expanded its Ultramid® and Ultradur® engineering plastics portfolio with new sustainable grades containing recycled and renewable feedstocks to support automotive and electrical applications. |

| 14 May 2025 | SABIC introduced new high-performance engineering thermoplastics designed for electric vehicle battery systems, lightweight mobility solutions, and advanced electrical components. |

| 19 Mar 2025 | Covestro AG launched advanced polycarbonate materials with improved mechanical performance and circular content, strengthening its sustainable engineering plastics portfolio for electronics and mobility applications. |

| 11 Feb 2025 | Celanese Corporation expanded its engineered materials business by introducing next-generation thermoplastic solutions for automotive, healthcare, industrial, and consumer electronics applications. |

| 23 Oct 2024 | DuPont de Nemours, Inc. introduced new Zytel® and Crastin® engineering resin grades with enhanced flame retardancy and thermal performance for electric vehicles and electronic devices. |

| 08 Aug 2024 | LANXESS AG expanded production capacity for high-performance Durethan® and Pocan® engineering plastics to address growing global demand from the automotive and electrical industries. |

| 16 Apr 2024 | LG Chem Ltd. announced the development of sustainable engineering plastics incorporating recycled materials to support circular economy initiatives and low-carbon manufacturing. |

| 29 Jan 2024 | Toray Industries, Inc. expanded its advanced engineering plastics portfolio by developing lightweight, high-strength polymer materials for electric vehicles, aerospace, and industrial machinery applications. |

Engineering Plastics Market Competitive Landscape:

The Engineering Plastics Market is highly competitive, with leading manufacturers focusing on product innovation, capacity expansion, sustainability, and strategic collaborations to strengthen their market positions. Companies are investing significantly in the development of high-performance engineering plastics with enhanced thermal stability, chemical resistance, flame retardancy, and lightweight properties to address the evolving requirements of the automotive, electrical & electronics, healthcare, aerospace, and industrial machinery sectors. The growing demand for electric vehicles, renewable energy systems, and miniaturized electronic components is encouraging manufacturers to expand production capacities, develop bio-based and recycled engineering plastics, and enhance their global distribution networks. In addition, mergers, acquisitions, joint ventures, and long-term supply agreements remain key strategies for improving market competitiveness and expanding regional presence.

Leading companies including BASF SE, SABIC, Covestro AG, Celanese Corporation, DuPont de Nemours, Inc., LANXESS AG, Mitsubishi Engineering-Plastics Corporation, Solvay S.A., LG Chem Ltd., and Toray Industries, Inc. are continuously expanding their engineering plastics portfolios through advanced polymer technologies, specialty resin development, and sustainable material innovations. Manufacturers are increasingly introducing high-performance grades of polyamide (PA), polycarbonate (PC), polybutylene terephthalate (PBT), polyoxymethylene (POM), polyphenylene sulfide (PPS), and polyether ether ketone (PEEK) to meet the growing demand from electric mobility, industrial automation, consumer electronics, and medical applications. As sustainability regulations become more stringent, companies are also investing in circular economy initiatives, chemically recycled polymers, and low-carbon manufacturing processes to strengthen their long-term competitive advantage.

Engineering Plastics Market Scope: Inquiry Before Buying

| Engineering Plastics Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 125.10 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 7.4% | Market Size in 2032: | USD 206.20 Bn. |

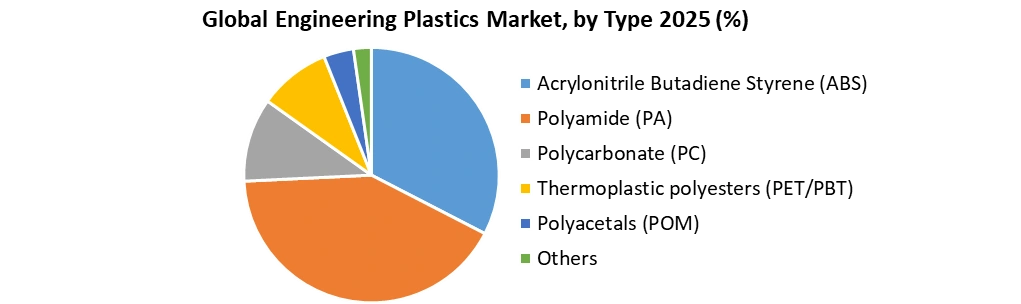

| Segments Covered: | By Type | Acrylonitrile Butadiene Styrene (ABS) Polyamide (PA) Polycarbonate (PC) Thermoplastic polyesters (PET/PBT) Polyacetals (POM) Others |

|

| By End-use Industry | Automotive & transportation Electrical & electronics Industrial & machinery Packaging Others |

||

Global Engineering Plastics Market by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Global Engineering Plastics Market Key Players

North America

- DuPont de Nemours, Inc. – United States

- Celanese Corporation – United States

- ExxonMobil Chemical – United States

- Eastman Chemical Company – United States

- RTP Company – United States

- Ensinger Inc. – United States

- Avient Corporation – United States

- Lubrizol Corporation – United States

Europe

- BASF SE – Germany

- Covestro AG – Germany

- LANXESS AG – Germany

- Arkema S.A. – France

- LyondellBasell Industries N.V. – Netherlands

- EMS-CHEMIE Holding AG – Switzerland

- Syensqo – Belgium

- Evonik Industries AG – Germany

- Victrex plc – United Kingdom

Asia Pacific

- Mitsubishi Engineering-Plastics Corporation – Japan

- Toray Industries, Inc. – Japan

- Teijin Limited – Japan

- LG Chem Ltd. – South Korea

- Sumitomo Chemical Co., Ltd. – Japan

- Idemitsu Kosan Co., Ltd. – Japan

- Formosa Plastics Corporation – Taiwan

- Chi Mei Corporation – Taiwan

- Kolon ENP, Inc. – South Korea

- Asahi Kasei Corporation – Japan

- SABIC – Saudi Arabia

Latin America

- Braskem S.A. – Brazil

Middle East & Africa

- Borouge – United Arab Emirates

- QAPCO (Qatar Petrochemical Company) – Qatar

Others

Frequently Asked Questions;

1. Which region has the largest share in the Global Engineering Plastics Market?

Ans: The Asia Pacific region held the highest share in 2024 in the Global Engineering Plastics Market.

2. What are the key factors driving the growth of the Global Engineering Plastics Market?

Ans: Rising Demand in Automotive Sector to boost the global Engineering Plastics Market growth.

3. Who are the key competitors in the Global Engineering Plastics Market?

Ans: BASF SE, SABIC, Solvay, and Covestro are the key competitors in the Global Engineering Plastics Market.

4. What are the opportunities for the Global Engineering Plastics Market?

Ans: Electric Vehicles (EVs) & Lightweighting Create Opportunities for Engineering Plastics Market Growth.

5. Which type segment dominates the Global Engineering Plastics Market?

Ans: The polyacetals segment dominated the Global Engineering Plastics Market.