Electronics Ceramics & Electrical Ceramics Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2034

Overview

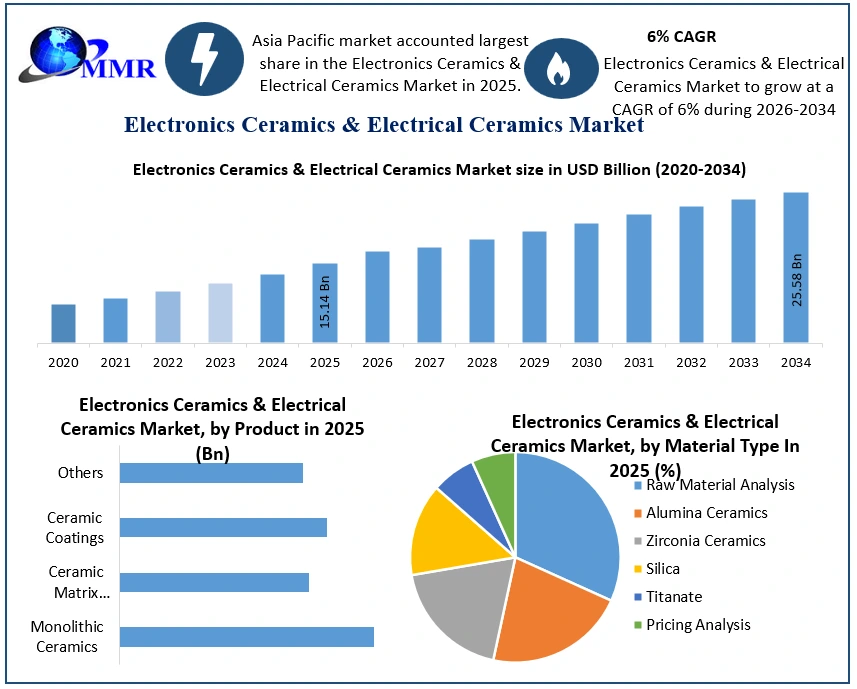

The Electronics Ceramics & Electrical Ceramics Market size was valued at USD 15.14 Billion in 2025 and the total Electronics Ceramics & Electrical Ceramics revenue is expected to grow at a CAGR of 6% from 2026 to 2034, reaching nearly USD 25.58 Billion.

Overview:

The market is expected to grow over the forecast period as a result of rising consumer appliance demand and ongoing power generation projects throughout the world. However, the market's growth is probably going to be hampered by the higher cost compared to alternative materials like metals and alloys. Over the next eight years, the market for electronics and electrical ceramics is likely to benefit from research and development in cutting-edge technologies and emerging 5G technology.

Asia-Pacific dominated the global market, with the most sales coming from China, South Korea, Japan, and India. China will surpass a valuation of US$ 2.26 billion by 2034, accounting for about 13% of the global market share. The rapid adoption of consumer electronics and medical device production is boosting market possibilities throughout the East Asian country.

Electronics Ceramics & Electrical Ceramics Market Growth and Share Analysis

To know about the Research Methodology:-Request Free Sample Report

Electronics Ceramics & Electrical Ceramics Market: Research Methodology

The entire research study was carried out in three stages: secondary research, primary research, and expert panel evaluation. The following are the major data points that enable the evaluation of the Electronics Ceramics & Electrical Ceramics market:

Manufacturers' research and development expenses, as well as government spending.

A number of end customers, the volume of consumption, price, and value.

Revenues of important market section firms.

Micro and macro environmental variables driving the Electronics Ceramics & Electrical Ceramics market today and their expected influence during the forecast period.

Geographical revenue generated by the report's countries.

Market forecasting was done using proprietary software that examines a variety of qualitative and quantitative parameters. The growth rate and CAGR were calculated using extensive secondary and primary research. Data triangulation across several data points ensures accuracy throughout the report's numerous examined market segments. The use of both a top-down and bottom-up methodology for market assessment ensures the logical, systematic, and mathematical coherence of the quantitative data.

Electronics Ceramics & Electrical Ceramics Market Dynamics

Drivers:

The electronics and electrical ceramics market is likely to be driven by advanced technologies and rising demand for electronics goods. Special ceramics may be required for electronic items such as cell phone antennas. At present, mobile phone antennas are employed in GPS applications to conserve space in handheld and portable devices. The antennas are also employed in group applications like as GPS and Bluetooth without affecting their performance. With growing income and rising living standards, demand for electronics and electrical ceramic items is expected to rise, driving the growth of the electronics ceramics & electrical ceramics market.

Application of Consumer Appliances to Dominate the Market

These ceramics are expected to find widespread use in consumer appliances. It is utilised in electronic substrates and spark plug insulators due to its strong electric and mechanical qualities as well as resistance to corrosion and wear. The most extensively utilised piezoelectric advanced ceramic material is zirconate titanate. It is less costly, chemically inert, and physically powerful. It has a unique set of features, including increased charge sensitivity, a higher working temperature, improved dielectric stability, and a fine grain structure with high density.

Sensors, antennae, capacitors, and resistors, for example, are becoming smaller and more capable as time passes on. As a result, this is a key area of research for these ceramics utilised in the electrical and electronics industries. The need for high - tech ceramics is increasing fast as the electronics industry continues to make incredible growth and development. Cell phones, portable computer devices, gaming systems, and other personal electronic gadgets will drive demand for semiconductors, capacitors, and other modern ceramics-containing electronic components.

All of the aforementioned reasons are expected to boost the electronics and electrical ceramics market during the forecast period.

Electronics Ceramics & Electrical Ceramics Market: Restraints

Though the global electronics ceramics and electrical ceramics market is growing rapidly, a few factors such as high raw material prices, a change in the end-use market from developed to emerging countries, and rising manufacturing costs are hampering market growth. Furthermore, electronics and electrical ceramics have a very high dielectric constant, which hinders signal transmission, as well as limited thermal conductivity, making them ineffective heat absorbers. As a result, producers are attempting to create ceramics comprised of more durable materials.

Electronics Ceramics & Electrical Ceramics Market Segment Analysis

By Material Type, Alumina ceramics sales are expected to grow at a rate of 5% CAGR to reach US$ 5.25 Bn by 2034, according to report on electronics and electrical ceramics. Thanks to the high mechanical strength, improved wear resistance, increased thermal stability, and strong corrosion resistance, alumina ceramics are widely used in the production of medical devices and household appliances.

By End Use, sales of electronics and electrical ceramics for medical devices are expected to grow the fastest, with a CAGR of 5% through 2034. The increasing demand for devices such as pacemakers, defibrillators, and endoscope forceps is driving adoption in the global market of electronics and electrical ceramics.

Electronics Ceramics & Electrical Ceramics Market Regional Insights

Asia Pacific Dominates the Electronics Ceramics & Electrical Ceramics Market:

Since the electrical and electronics industries are well-established in the Asia-Pacific region, the region is expected to dominate the market. The primary consumers of electronic and electrical ceramics in the area include countries like China, Japan, India, South Korea, and Vietnam.

The greatest electronics manufacturing base in the world is China, which is dominated by electronic devices including smartphones, OLED TVs, tablets, and so on. One of the biggest and fastest-growing sectors in India is electronics. Many firms are moving from China to India to satisfy domestic demand due to growing labour costs. In addition, government programmes like Digital India are promoting the growth of the country's electronics manufacturing industry.

Making ensuring that all government services are available to residents electronically is the key objective of this effort. India sold US$ 11 Bn worth of consumer electronics in 2019, but China sold more than US$ 100 Bn. China now holds a 2/5 worldwide market share in the technical ceramics industry. This also applies to electrical ceramics and electronics. Consumers are purchasing smartphones and laptops due to an increase in digital literacy, which is encouraging the use of premium ceramics in interior parts of these devices.

Japan has one of the world's largest electrical and electronic industries and is a key rival to the United States in terms of semiconductor manufacture. It is also home to Sony and Toshiba, two global leaders in the electronics industry. According to the Japan Electronics and Information Technology Industries Association (JEITA), display, server, storage, electro-medical, and electronic measurement equipment manufacturing is increasing steadily. During the forecast period, such a well-established electronics sector base is likely to add to the demand for electronics and electrical ceramics.

In 2023, the United States is one of the largest markets in North America for electronics and electrical ceramics, accounting USD 3 Bn market share. Because of the presence of significant manufacturers in this industry, especially in the United States and Canada, end-user industries such as household appliances and medical equipment have grown. According to SelectUSA, the United States continues to have the world's largest medical device market, which is expected to reach US$ 208 billion by 2024. Hospitalization rates are rising as growing population pool suffering from numerous chronic conditions are growing, inspiring investments in high-quality medical equipment constructed of high-quality ceramics.

Scope of the Report

This research evaluates current activities and developments in each sub-sector, as well as revenue growth at the global, regional, and global levels (2026-2034). For this analysis, MMR divided the Electronics Ceramics & Electrical Ceramics market into Material Type, Product, End-Use, and geographic locations. The market analysis also contains expected market estimates and trends for 17 countries spread throughout the world's primary geographic zones. The value for the aforementioned categories is provided in the report (in USD million).

The research also aids in understanding the Electronics Ceramics & Electrical Ceramics Market trends, structure, and size projections by evaluating market segments. The research serves as an investor's guide by providing a clear depiction of competition analysis of major competitors in the Electronics Ceramics & Electrical Ceramics Market by financial situation, product portfolio, growth plans, and geographical presence.

Scope of Global Electronics Ceramics & Electrical Ceramics Market :Inquire before buying

| Global Electronics Ceramics & Electrical Ceramics Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | US 15.14 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 6% | Market Size in 2034: | USD 25.58 Bn. |

| Segments Covered: | by Product | Monolithic Ceramics Ceramic Matrix Composites Ceramic Coatings Others |

|

| by Material Type | Raw Material Analysis Alumina Ceramics Zirconia Ceramics Silica Titanate Pricing Analysis |

||

| by End Use Industry | Home Appliances Power Grid Medical Devices Mobile Phones Others |

||

Electronics Ceramics & Electrical Ceramics Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Electronics Ceramics & Electrical Ceramics Market, Key Players are

1. Coorstek Inc.

2. Ceramtec GmbH

3. Kyocera Corporation

4. Morgan Advanced Materials

5. Ceradyne Inc. (3M Company)

6. NGK Spark Plug Co., Ltd.

7. Rauschert Steinbach GmbH

8. Murata Manufacturing Co., Ltd.

9. ENRG Inc.

10. Mantec Technical Ceramics Ltd.

Frequently Asked Questions:

1] What segments are covered in the Global market report?

Ans. The segments covered in the Market report are based on Material Type, Product, End-Use, and Region.

2] Which region is expected to hold the highest share in the Global market?

Ans. The Asia Pacific region is expected to hold the highest share in the Market.

3] What is the market size of the Global Market by 2034?

Ans. The market size of the Market by 2034 is expected to reach USD 25.58 Bn.

4] What is the forecast period for the Global Market?

Ans. The forecast period for the Market is 2026-2034.

5] What was the Global Electronics Ceramics & Electrical Ceramics Market size in 2025?

Ans. The Global Electronics Ceramics & Electrical Ceramics Market size was USD 15.14 Billion in 2025.