Electronic Health Records Market by Product,End User Region - Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

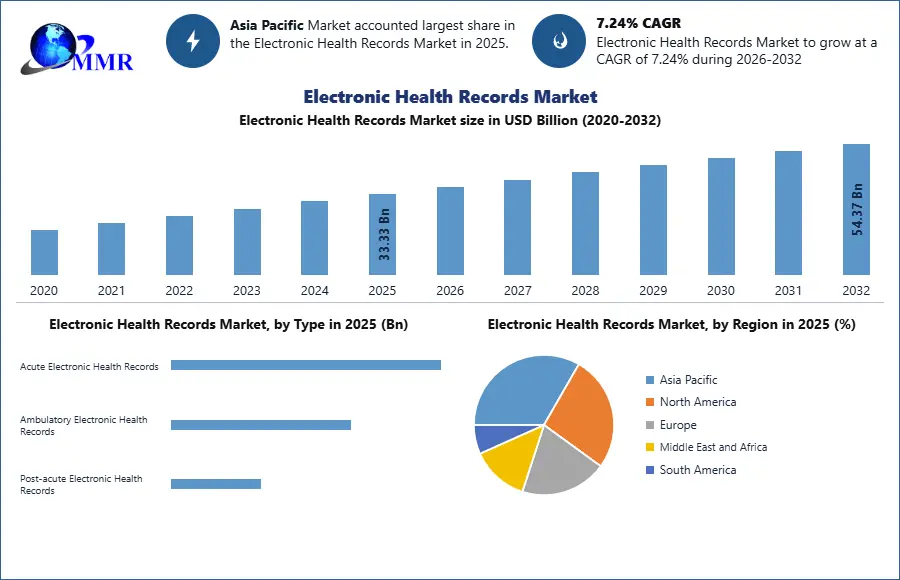

Global Electronic Health Records Market size was valued at USD 33.33 Bn in 2025 and is expected to reach USD 54.36 Bn by 2032, at a CAGR of 7.24% over 2026-2032.

Electronic Health Records Market Overview

An Electronic Health Record (EHR) aids in a digital archive housing an individual's complete medical history, systematically managed by healthcare providers. It encompasses crucial administrative and clinical data, including demographics, progress notes, medications, vital signs, immunizations, and laboratory results. EHRs automate data access, streamlining clinician workflows and supporting evidence-based decision-making, quality management, and outcomes reporting. The Electronic Health Records market, driven by technological advancements, revolutionizes healthcare, fostering patient-clinician relationships and enabling informed decision-making for optimal care outcomes. EHRs are instrumental in reducing medical errors by improving record accuracy and accessibility, and expediting treatment while minimizing test duplication. Their shared nature among diverse healthcare entities facilitates seamless information exchange, contributing to a more integrated and efficient healthcare ecosystem. With the increasing digitization of patient information, EHRs provide to the rising demand for mobile access, underlining their increasing influence in contemporary healthcare practices.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

The Electronic Health Records industry is undergoing strong growth driven by transformative advancements in healthcare digitization. The adoption of EHR systems has become imperative as healthcare providers recognize their potential to revolutionize patient care, streamline operations and improve overall healthcare delivery. The industry's growth is driven by the growing recognition of the value of comprehensive and easily accessible patient data. Governments and healthcare organizations worldwide are actively promoting EHR adoption through regulatory initiatives, incentivizing interoperability standards and investing in digital infrastructure. The Electronic Health Records market experiences growth as technological advancements, including artificial intelligence, machine learning, and data analytics, elevate healthcare quality, efficiency, and patient engagement through enhanced clinical decision support and personalized medicine.

Electronic Health Records Market Dynamics

Increasing focus on interoperability to boost Electronic Health Records Market Growth

Interoperability enables seamless sharing of patient information across different healthcare systems, providers, and organizations. This facilitates better coordination of care among healthcare professionals, leading to improved patient outcomes. When healthcare providers have access to comprehensive and up-to-date patient records, they make more informed decisions about diagnosis and treatment. Interoperability helps eliminate duplicate tests and procedures by allowing different healthcare providers to access the same patient data. This not only reduces costs but also minimizes the chances of errors and ensures that patients receive the most appropriate and timely care. It enhances the overall efficiency of the healthcare system. Interoperability empowers patients by giving them greater control over their health information. Patients access their EHRs, share them with different healthcare providers, and actively participate in their care. In the Electronic Health Records market, the integration of advanced technologies fosters a patient-centric approach, empowering individuals to proactively manage their health through improved access, engagement, and personalized care solutions.

The Electronic Health Records landscape is witnessing a growing emphasis on interoperability, denoting the seamless access, integration, and utilization of electronic health data to optimize health outcomes. This emphasis is crucial sensitive nature of health data, posing a challenge to strike a balance between privacy and accessibility. Inadequate interoperability results in incomplete health information, leading to suboptimal outcomes and increased costs. To address this, governments and healthcare organizations globally are actively promoting interoperability through regulatory measures, endorsing standards such as FHIR (Fast Healthcare Interoperability Resources) and investing in digital infrastructure. As populations age, interoperability becomes increasingly critical for delivering effective healthcare. Although the adoption of EHRs has risen, challenges persist in integrating received data into individual patient records. In the Electronic Health Records market, interoperability emerges as a key driver, delivering benefits such as enhanced care coordination, optimized performance through data analysis, and an overall improved healthcare experience by reducing redundant administrative tasks. The introduction of FHIR as an open-source standards framework is revolutionizing healthcare data exchange, enabling seamless movement between systems.

Electronic Health Records Market Trend

Accelerating integration of artificial intelligence (AI) and machine learning (ML) technologies

Inherent multimodal healthcare data, encompassing Electronic Health Records (EHR), medical images, and multi-omics data, are being fused using advanced AI techniques for a profound understanding of human health and personalized healthcare. This integration workflow involves raw data feeding, multimodal fusion using conventional ML or deep learning algorithms, and subsequent evaluation through clinical outcome predictions. Within the Electronic Health Records market, multimodality fusion models excel over single-modality ones, specifically in neurological disorder diagnosis and prediction, showcasing superior performance in healthcare analytics. From an AI perspective, conventional ML models are widely used, followed closely by DL models. AI applications in EHR systems, such as data extraction, predictive analytics, clinical documentation, and decision support, are poised to revolutionize the healthcare landscape, offering flexibility, incisiveness and improved physician-friendliness.

This evolution has revolutionized healthcare, enhancing diagnostic accuracy, personalized treatments, and overall patient monitoring. AI's ability to swiftly analyze extensive clinical documentation aids in uncovering disease markers and trends that might be overlooked conventionally. From early detection through radiological image analysis to predicting outcomes based on electronic health records, the incorporation of AI and ML is reshaping healthcare delivery worldwide. Key players such as IBM, Apple, Microsoft, and Amazon are actively investing in AI technologies for healthcare. Machine Learning, Natural Language Processing and rule-based expert systems are essential components, that enable precise medical diagnoses, personalized treatments, and streamlined administrative processes. This integration not only improves patient care but also drives operational efficiency, marking a paradigm shift in the Electronic Health Records Market towards a future where AI and ML technologies play an essential in healthcare advancements.

In European countries, the adoption of Electronic Health Records (EHR) varies, with the Netherlands leading in usage. The Netherlands exhibits a higher share of clinicians embracing EHR systems. Furthermore, there is a notable trend across Europe towards the rapid integration of artificial intelligence (AI) and machine learning (ML) technologies in healthcare, enhancing diagnostic and treatment capabilities.

Electronic Health Records Market Restraints

High Implementation Costs to hamper Electronic Health Records Market Growth

Healthcare organizations need to allocate funds for the procurement of EHR software licenses, servers, computers and networking equipment. The customization and integration of EHR systems are pivotal, demanding alignment with the unique workflows and requirements of healthcare entities. The intricacies of integrating with existing systems and databases entail additional investments in software development, demanding testing, and comprehensive training. Data migration from legacy systems to EHR platforms, a critical implementation aspect is time-consuming and may necessitate specialized expertise, contributing to increased costs. Efficient Electronic Health Records market integration requires comprehensive training for healthcare staff, incurring additional costs in resources, time, and personnel to ensure a smooth transition.

Compliance with regulatory standards and the implementation of robust security features to safeguard patient data introduce additional costs to the overall implementation process. Post-implementation, ongoing maintenance and support are dynamic, involving allocations for software updates, troubleshooting and addressing potential issues that may arise over time. The transition to EHR systems leads to a temporary disruption in productivity as healthcare professionals adapt to new workflows, incurring additional costs associated with potential revenue loss during the adjustment period. Vendor lock-in, a potential limitation, restricts the flexibility of healthcare organizations in selecting alternative solutions more aligned with their evolving needs. Achieving interoperability with other healthcare systems and external partners requires supplementary investments in technologies and standards facilitating seamless data exchange.

Electronic Health Records Market Segment Analysis

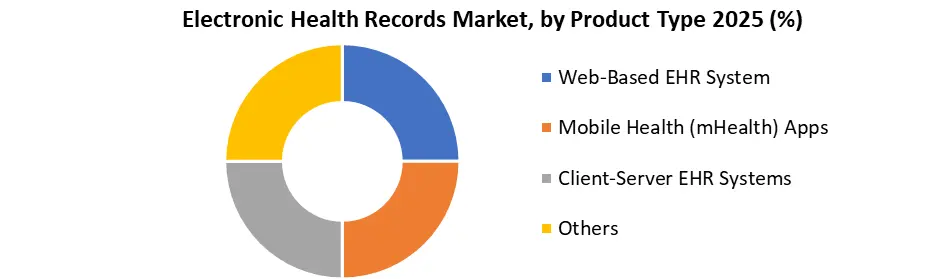

Based on the Product, the market is segmented into Web-Based EHR Systems, Mobile Health (mHealth) Apps, Client-Server EHR Systems and Others. Web-based EHR Systems dominated the largest Electronic Health Records Market share in 2025 and are expected to continue their dominance over the forecast period. Web-based EHR systems efficiently address concerns commonly encountered by independent physicians during EHR adoption. Unlike traditional server-based models, which entail substantial costs for server installation, hardware, software, and ongoing local IT maintenance, web-based EHRs, provided by Software as a Service (SaaS) providers, significantly alleviate costs and implementation timelines. The resilience of cloud-based EHR systems against system meltdowns, natural disasters, and disruptions caused by weather patterns, enhances reliability compared to their server-based counterparts. Data securely stored on the cloud remains readily accessible from any location and at any time, ensuring uninterrupted and convenient usage.

Security concerns, particularly regarding patient confidentiality, are meticulously addressed by web-based EHR systems through measures such as risk analyses and data encryption. Compliance with regulations such as the Health Insurance Portability and Accountability Act (HIPAA) ensures the secure handling of electronic protected health information (ePHI). The advantages of web-based EHRs extend beyond security, encompassing simplified operations, instant scalability, reduced costs and improved data sharing with security features. These systems provide seamless to practices of varying sizes, from single-physician clinics to large, multi-location and multi-specialty setups. Designed around specialty-specific workflows, web-based EHR systems not only streamline documentation, billing processes, and care delivery but also enhance communication, simplify administrative tasks and boost overall productivity for physicians and staff. Web-based EHR systems emerge as the preferred choice in the Electronic Health Records market, offering a holistic solution characterized by flexibility, cost-effectiveness, security and convenience tailored for the unique needs of independent physicians across diverse healthcare settings.

Electronic Health Records Market Regional Insights

North America dominated the largest Electronic Health Records Market share in 2025 and is expected to continue its dominance over the forecast period. The United States has been a developer in the early adoption of Electronic Health Record (EHR) systems. The initiatives including the Health Information Technology for Economic and Clinical Health (HITECH) Act in 2009 are boosting the adoption of the Electronic Health Records industry in the U.S. This legislation provided financial incentives to healthcare providers, catalysing widespread adoption. North America, particularly the United States, boasts a cutting-edge IT infrastructure, facilitating seamless implementation and integration of EHR systems within healthcare organizations. The region's prominence in the global healthcare market is underscored by the complete size and complexity of its healthcare sector. The demand for efficient healthcare management systems has boosted the adoption of EHR solutions across North America. Regulatory compliance has shaped the EHR landscape, with bodies such as the Centers for Medicare & Medicaid Services (CMS) and the Office of the National Coordinator for Health Information Technology (ONC) setting standards and requirements for widespread EHR adoption.

Private sector investments have significantly contributed to the growth of the EHR market in North America. The presence of a strong private sector, characterized by substantial investments in healthcare technology, has fostered innovation and the development of EHR solutions. Simultaneously, efforts to enhance interoperability among healthcare systems have become a driving force behind EHR adoption. The imperative for a seamless exchange of patient information between different healthcare entities has elevated the importance of EHRs in the region. Concerted initiatives in awareness and education have garnered acceptance and utilization of electronic health records among healthcare professionals. Training programs and awareness campaigns have contributed to enhancing the understanding of the benefits associated with EHR systems. The competitive landscape in North America has been ongoing innovations and improvements in EHR technologies. The presence of many vendors and service providers has created a dynamic Electronic Health Records Market, offering a multitude of options for healthcare organizations seeking effective EHR solutions.

Recent Industry Developments

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 09 March 2026 | athenahealth | Showcased Intelligent Interoperability and advanced AI capabilities at HIMSS 2026 to streamline clinical data exchange. | Strengthens its competitive position in automated data sharing across fragmented healthcare networks. |

| 19 February 2026 | athenahealth | Launched Agentic Patient Communication Tools across its provider network to offer 24/7 AI-driven scheduling and engagement. | Reduces administrative burden for practices while improving patient access to EHR-integrated services. |

| 09 February 2026 | athenahealth | Partnered with b.well to introduce patient-controlled digital health data sharing at the point of care. | Advances CMS interoperability goals by placing data control directly in the hands of the patient. |

| 01 January 2026 | Oracle Health | Released a 2026 product roadmap detailing the integration of Clinical AI Agents for inpatient and emergency care. | Accelerates the shift toward ambient AI documentation within high-acuity hospital environments. |

| 15 December 2025 | Epic Systems | Selected by Saint Peter’s Healthcare System as the centralized EHR partner to integrate inpatient and outpatient records. | Consolidates market share in the acute care segment by replacing legacy multi-vendor environments. |

| 22 October 2025 | WellSky | Launched AI-powered ambient listening enabled by Suki for behavioral health and long-term acute care EHRs. | Enhances efficiency in specialty care settings, specifically targeting clinician burnout in post-acute workflows. |

Electronic Health Records Market Scope: Inquire before buying

| Electronic Health Records Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 33.33 USD Billion |

| Forecast Period 2026-2032 CAGR: | 7.24% | Market Size in 2032: | 54.37 USD Billion |

| Segments Covered: | by Type | Acute Electronic Health Records Ambulatory Electronic Health Records Post-acute Electronic Health Records |

|

| By System | Web-based EHR Systems Client-based EHR Systems |

||

| By Business Model | Licensed Software Technology Resale Subscriptions Professional Services Others |

||

| By Deployment | On-Premise Cloud-Based Hybrid |

||

| By Application | Administrative Task and Billing Clinical Records Physician Support Others |

||

| By End-users | Hospitals and Clinics Ambulatory Care Others |

||

Electronic Health Records Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players / Competitors Profiles Covered in Brief in Global Electronic Health Records Market Report in Strategic Perspective:

- AdvancedMD, Inc.

- athenahealth, Inc.

- Altera Digital Health (a Harris Company)

- Azalea Health

- CareCloud, Inc.

- ChipSoft

- CompuGroup Medical SE & Co. KGaA

- CureMD Healthcare

- DrChrono (EverHealth Solutions Inc.)

- eClinicalWorks LLC

- Epic Systems Corporation

- Dedalus Group

- Greenway Health, LLC

- InterSystems Corporation

- McKesson Corporation

- Medical Information Technology, Inc. (MEDITECH)

- SimplePractice

- Microwize Technology

- Modernizing Medicine (ModMed)

- Netsmart Technologies

- NextGen Healthcare, Inc.

- Oracle Corporation (Oracle Health / Cerner)

- Praxis EMR

- Practice Fusion

- PracticeSuite

- RXNT

- Tebra Technologies, Inc.

- TruBridge, Inc.

- Valant

- Veradigm LLC

- WRS Health

- Dell Technologies Inc.

- GE HealthCare Technologies Inc.

- EverCommerce Inc.

- KareXpert Technologies Pvt. Ltd.

Others