Electric Vehicle Motor Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2032

Overview

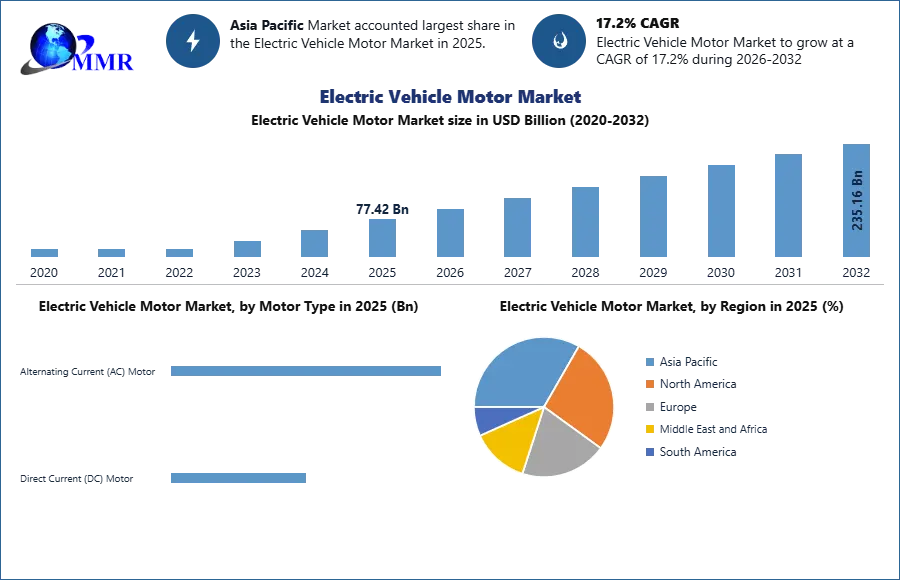

Electric Vehicle Motor Market was valued at USD 77.42 Bn in 2025. The Electric Vehicle Motor Market size is estimated to grow at a CAGR of 17.2% over the forecast period.

Electric Vehicle Motor Market Overview:

Because of the shifting consumer preference toward electric vehicles with a long range, the EV Motors market will increase steadily during the forecast period. Another significant factor positively affecting market expansion is the introduction of stringent government restrictions. To cut greenhouse gas emissions & stop global warming, the world community has established strict emissions regulations. In order to meet more stringent pollution rules, automakers now concentrate on creating zero-emission automobiles. These regulations will result in a stronger focus on the production of more effective electric vehicles during the forecast period.

To know about the Research Methodology :- Request Free Sample Report

Electric Vehicle Motor Market Dynamics:

The main factors which drive the electric vehicle motor market are growth in electric vehicle industry, & increase in government rules & regulations with respect to vehicular emission. The development in technologies, like manufacturing of energy-efficient motors, is expected to boost the market growth in the near future. In addition, rise in government initiatives related to electric vehicles is expected to provide many opportunities for the market growth.

Electric Vehicle Motor Market Segment Analysis:

The Electric Vehicle Motor Market demonstrates notable growth across multiple segments during the forecast period from 2026 to 2032, driven by rising electric vehicle adoption, technological advancements in motor efficiency, and supportive government policies promoting clean mobility.

By motor type, the Alternating Current (AC) motor segment is expected to dominate the market during the forecast period. AC motors, particularly permanent magnet synchronous motors and induction motors, offer high efficiency, better power density, and improved performance, which supports their widespread adoption in modern electric vehicles. Meanwhile, the Direct Current (DC) motor segment continues to maintain a smaller share, primarily due to its simpler control system and lower cost, though it is gradually being replaced by more efficient AC motor technologies in advanced EV platforms.

Based on vehicle type, the passenger car segment is projected to hold the largest market share between 2026 and 2032 due to the increasing production and sales of electric passenger vehicles worldwide. Strong consumer demand for sustainable transportation and expanding EV infrastructure contribute to this growth. The commercial vehicle segment is also expected to witness steady growth as logistics and public transportation sectors shift toward electrification. Additionally, two-wheelers represent a rapidly growing segment, particularly in emerging economies where electric scooters and motorcycles are gaining popularity due to lower operating costs and urban mobility needs.

In terms of power, the up to 100 kW segment is anticipated to account for a significant share of the market, largely driven by its extensive use in compact electric vehicles and two-wheelers. The 101–250 kW segment is projected to experience strong growth as mid-range passenger EVs increasingly require higher power output for improved performance. The above 250 kW segment, although smaller in volume, is expected to grow steadily due to its use in high-performance electric vehicles and heavy commercial EVs that demand greater power and torque.

By assembly, the central power train segment is expected to dominate the electric vehicle motor market throughout the forecast period. This configuration remains widely used due to its reliability, efficiency, and compatibility with existing drivetrain architectures. In contrast, the wheel hub motor segment is projected to grow at a notable pace as automakers explore advanced EV designs that improve space utilization, vehicle efficiency, and drivetrain simplification.

Electric Vehicle Motor Market Regional Analysis:

The Electric Vehicle Motor Market is projected to experience significant regional growth during the 2026–2032 period, with Asia Pacific leading the market due to strong electric vehicle production, expanding EV infrastructure, and supportive government initiatives in countries such as China, Japan, and South Korea. North America is expected to witness substantial growth driven by increasing EV adoption, technological advancements in electric powertrain systems, and supportive regulatory policies in the United States and Canada. Europe continues to hold a significant market share owing to strict emission regulations, strong sustainability targets, and rising investments in electric mobility across countries including Germany, France, and the United Kingdom. Meanwhile, the Middle East and Africa market is projected to grow at a moderate pace as governments gradually promote clean transportation and develop EV infrastructure, particularly in the UAE and South Africa. South America is anticipated to observe steady growth supported by rising environmental awareness, government initiatives encouraging electric mobility, and increasing adoption of EVs in countries such as Brazil and Chile, contributing to overall market expansion during the forecast period.

Trends Affecting the Market for EV Motors:

EV manufacturers are incorporating AC synchronous motors with brushed current excitation more frequently. This type of motor was not utilised in EVs until recently because it was commonly accepted that brushless motors were the only viable option for an EV. BMW defied the trend by incorporating brushed current-excited AC synchronous motors in the new i4 & iX. The RMF of the stator is affected by this sort of rotor in a similar manner to a permanent-magnet rotor, but without the use of permanent magnets. Instead, it has six sizable copper lobes that, when powered by a DC battery, produce the required EMF. The system's capability to change the strength of the magnetic field on the rotor also enables optimization.

Manufacturers of EV motors face difficulties:

Lower replacement rates have an effect on the aftermarket. An electric car motor normally lasts 15 to 20 years, but certain motors have long working lives & don't require replacement as often. In cases of accidents, EV motors are routinely replaced. One of the key things keeping aftermarket sales down is this. The market for electric cars is also being restricted in developing & price-sensitive countries by factors like high electric vehicle prices and a lack of infrastructure, such as charging and repair facilities.

Sales of electric vehicle motors will be fueled by strict vehicle emission standards.

In the year 2022, the U.S. accounted for almost 91% of the North American electric car motor market. By the end of 2032, the market, which holds 89.7% of the market share, is expected to lose 162 BPS points. The U.S. EV market is lagging behind other industrialized countries with significant economies like China & Europe, where sales are just a third and a half as high, respectively. The governors of eight western states, including Colorado, Arizona, Idaho, Nevada, Montana, New Mexico, Wyoming, & Utah, signed a memorandum of understanding in 2019 to make it possible to travel in an EV across significant transportation corridors in the states. The sales of electric car motors will increase as a result.

Sales of Electric Car Motor Kits in China will grow as they increase.

A growing number of people can now afford to buy their autos thanks to China's recent robust economic progress. Mobility has increased as a result, and the global car market has expanded considerably. But this has also resulted in significant urban air pollution, high greenhouse gas emissions, and a growing dependency on foreign energy. To counteract these disconcerting trends, the Chinese government has created policies that encourage the usage of plug-in electric automobiles. Because buying an electric vehicle (EV) is more expensive than buying an internal combustion engine (ICE) vehicle, the government began providing significant subsidies for EV purchases. This is anticipated to drive the Chinese market for electric car motors.

As the impact of COVID-19 related lockdowns spread during the first quarter of 2020, global electric vehicle sales in major markets, including Europe and the US, are expected to fall significantly. Falling consumer demand, disruption to upstream & downstream supply chains, and government guidelines have now resulted in the suspension and curtailment of production at major automotive OEMs and battery manufacturers. European and US automakers have delayed Asian Li-ion battery shipments initially scheduled for Q2 2020 amid the growing uncertainty for automotive demand.

The market for AC motors will increase:

The AC motor industry is expected to generate an absolute incremental opportunity of more than USD 286 Bn between 2026 & 2032, depending on the kind of product. When it comes to performance and efficiency, electric vehicles with AC motors have an advantage, especially on uneven roads. They have a faster acceleration and can be used for harsher, longer excursions.

Battery electric vehicles are adopting EV motors:

Battery Electric Vehicles (BEVs) are a specific category of vehicle that is predicted to hold more than 45% of the market in the year 2025. Sales of BEVs have dramatically increased in the last few years, exceeding earlier expectations for their ultimate impact on the automobile industry. Now, almost all manufacturers hope to make BEVs their main offering in the upcoming years. Most OEMs had plans to deploy BEVs three years ago, but few expected or expected BEV dominance before the late 2030s, at the earliest. The rapid decline in battery prices, which will eventually bring their costs to level with those of ICE vehicles, is a significant factor in the rise in interest in BEVs.

Recent Industry Developments (2025–2026)

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 08 September 2025 | Vedanta Limited | Invested USD 1.42 billion to expand production capacity for aluminium and zinc alloys essential for lightweight EV motor housings. | Increased raw material availability lowers production costs for motor manufacturers and supports vehicle range extension through weight reduction. |

| 14 August 2025 | Ola Electric | Unveiled an indigenously developed ferrite motor that eliminates the need for expensive rare-earth magnets. | This innovation ensures supply chain independence from rare-earth volatility and significantly reduces the environmental footprint of motor production. |

| 29 July 2025 | DPIIT & Ather Energy | Signed a Memorandum of Understanding to boost the manufacturing startup ecosystem with a focus on deep-tech battery and motor integration. | The partnership fosters R&D innovation, enabling smaller players to compete in the high-efficiency traction motor segment. |

The report's objective is to provide key industry players with a thorough insight of the global Electric Vehicle Motor Market. The research analyses complex data in plain terms & presents the historical & current state of the industry together with expected market size and trends. The analysis analyses important companies, including market leaders, followers, and new entries, in detail and covers all areas of the industry. The research includes a PORTER, PESTEL analysis with the probable influence of market micro-economic aspects. Analysis of both internal & external variables that are thought to have an impact on the company either favorably or unfavorably has been done in order to provide decision-makers with a clear futuristic vision of the sector.

The reports also help in understanding the Electric Vehicle Motor Market dynamic, & structure by analyzing the market segments and projecting the Electric Vehicle Motor Market size. Clear representation of competitive analysis of key players by Design, price, financial position, Motor Type portfolio, growth strategies, and regional presence in the Electric Vehicle Motor Market make the report investor’s guide.

Electric Vehicle Motor Market Scope: Inquire before buying

| Electric Vehicle Motor Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 77.42 USD Billion |

| Forecast Period 2026-2032 CAGR: | 17.2% | Market Size in 2032: | 235.16 USD Billion |

| Segments Covered: | by Motor Type | Alternating Current (AC) Motor Direct Current (DC) Motor |

|

| by Vehicle Type | Passenger Car Commercial Vehicle Two-wheelers |

||

| by Power | Up to 100 kW 101-250 kW Above 250 kW |

||

| by Assembly | Wheel Hub Central Power Train |

||

Electric Vehicle Motor Market, by Region:

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players / Competitors Profiles Covered in Brief in Global Electric Vehicle Motor Market Report in Strategic Perspective:

- Robert Bosch GmbH

- Continental AG

- Nidec Corporation

- Denso Corporation

- ZF Friedrichshafen AG

- Mitsubishi Electric Corporation

- Magna International Inc.

- BorgWarner Inc.

- Aisin Corporation

- Toshiba Corporation

- Siemens AG

- ABB Ltd.

- Hitachi Astemo, Ltd.

- Valeo S.A.

- Mahle GmbH

- Hyundai Mobis Co., Ltd.

- Dana Incorporated

- GKN Automotive

- Allison Transmission

- Meidensha Corporation

- Jatco Ltd.

- Yasa Limited

- BYD Company Ltd.

- Tesla, Inc.

- XPT (NIO)