Electric Vehicle Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

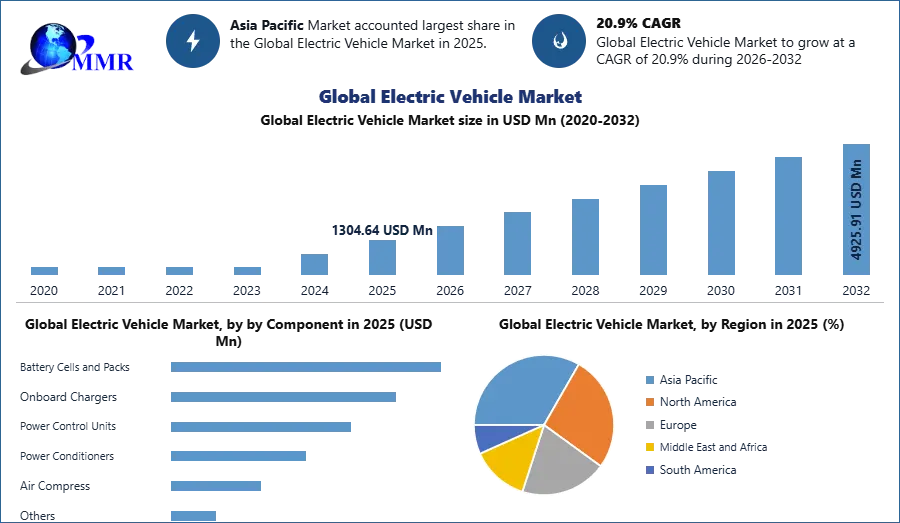

The Electric Vehicle Market size was valued at USD 1,304.64 Mn in 2025 and the total Electric Vehicle revenue is expected to grow at a CAGR of 20.90% from 2025 to 2032, reaching nearly USD 4,925.91 Mn.

Electric Vehicle Market Overview:

An electric vehicle (EV) is a vehicle that uses one or more electric motors for propulsion. Unlike traditional gasoline-powered vehicles, EVs rely on electricity stored in rechargeable batteries to power their motors. This makes them significantly more environmentally friendly as they produce zero tailpipe emissions.

MMR Global Electric Vehicle Market Report Offers

The MMR final report Global Electric Vehicle Market Outlook is a comprehensive publication that delves into recent advancements in electric mobility worldwide, crafted with the collaborative effort of members associated with the Electric Vehicles Initiative (EVI). By blending historical analyses with forecasts extending to , the report meticulously investigates crucial areas of interest, including the deployment of electric vehicles, the establishment of charging infrastructure, battery demand, electricity consumption, displacement of oil usage, greenhouse gas emissions, and pertinent policy developments. Its content incorporates a thorough analysis of insights gained from leading markets, aiming to enlighten policymakers and stakeholders about effective policy frameworks and market systems conducive to the widespread adoption of electric vehicles.

This edition specifically includes an examination of the financial performance of companies involved in the Electric Vehicle Market, venture capital investments in electric vehicle-related technologies, and the global trade of electric vehicles. Furthermore, the report offers excel sheet for electric vehicle statistics, projections, and policy measures on a global scale. By incorporating these elements, the report ensures that clients receive a comprehensive understanding of the electric vehicle market, highlighting key trends, opportunities, and challenges, thus enabling informed decision-making and strategic planning for stakeholders. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Electric Vehicle Market Dynamics:

Technological advancements and infrastructure development

The main factors driving the use of electric vehicles (EVs) in transportation and logistics are technological advancements and infrastructure. One important part of this is the rapid expansion of EV charging infrastructure, which the U.S. The Department of Energy reported more than 10,000 new charging stations in the US. all This extensive connectivity reduces accessibility concerns of EV users, making electric vehicles more practical for consumers and businesses. Governments around the world are also investing heavily in EV charging infrastructure and offering incentives for EV adoption. For example, the U.S. the government has implemented policies and subsidies to support charging station expansion and encourage EV adoption. Similarly, the EU Green Deal sets ambitious targets for EV adoption and infrastructure, which are crucial for accelerating the transition to electric mobility.

Increasing environmental awareness of consumers is also increasing the demand for environmentally friendly transportation methods, leading companies to use electric vehicles and trucks along with their fleet This combination of economic, legal and social factors is accelerating the transition to electric vehicles.

Electric vehicles are gaining momentum in transportation and logistics with the rise of global trade and e-commerce

Expansion in the transportation and logistics sectors is fueling the demand for electric vehicles (EVs). As global trade and e-commerce continue to evolve, the need for efficient and sustainable transportation solutions increases. Electric vehicles offer a promising alternative to conventional combustion engine vehicles, as they produce lower emissions and lower operating costs This shift is particularly evident in urban areas where logistics are increasing and the need to reduce air pollution is critical. As a result, logistics companies are increasingly adding electric cars and trucks to their fleets, driven by regulatory pressure and the economic benefits of lower fuel and maintenance costs.

An example of this trend can be seen in Amazon, which in May 2025 deployed heavy-duty electric trucks across Southern California for its freight operations. The introduction of these 50 heavy duty electric trucks in the region is a significant step towards decarbonization through first, middle and final delivery. This move meets established regulatory requirements their eye towards reducing not only carbon footprints but logistics due to the lower operating costs of EVs also means there can be economic benefits in the field. The deployment of electric trucks by a major company such as Amazon highlights the increasing adoption and integration of EVs in transportation and logistics, forcing a more sustainable future in the world both trade and commerce are intensified.

Business Opportunities for Electric Vehicle globally

We have incorporated the below information for major countries and the business opportunities in those countries. This information provides insights into the expansive potential for businesses in the electric vehicle (EV) sector, mainly in India, China, Japan, South Korea, ASEAN, Germany, France, UK, Italy, Spain, US, Canada, Mexico, Brazil, Argentina. The business opportunities span across three key segments: mobility, infrastructure, and energy. These include opportunities in EV franchising, the EV Original Equipment Manufacturer (OEM) market, battery infrastructure, solar vehicle charging, and battery swapping technology, among several others.

The EV push in India opens several business opportunities in three key segments transport, infrastructure and energy These include opportunities in EV franchising, EV OEM market, battery systems, solar car charging, battery swapping technology and many others According to NITI means the Aayog will make a complete shift towards EVs, battery infrastructure and charging infrastructure A total investment of USD 267 million (Rs 19.7 lakh crore) is required.

Moreover, according to the Ministry of Skills Development and Entrepreneurship (MSDE), the EV industry could add 10 million direct jobs by , creating 50 million indirect jobs in the sector Several automotive companies are planning to participate in the EV industry as listed in the table below:

| COMPANY | EV RELATED PLANS |

| Kia | Kia plans to manufacture small SUV EVs in India for global markets in 2025. |

| Maruti Suzuki | Maruti Suzuki plans to launch its first EV model in India by 2025. |

| Tata Motors | Tata Motors bags an order worth US$ 678 million (Rs 5,000 crore) order from the government for electric buses; it plans to launch 10 more EVs in India. |

| Hyundai | Hyundai plans to launch IONIQ 5 EV in India by the second half of 2022. |

| Hopcharge | Hopcharge, a Gurgaon- based start-up has created the world’s first on-demand doorstep fast charge service. |

| MG Motors | MG Motors India has partnered with Bharath petroleum for expanding the EV charging infrastructure. |

| Mahindra & Mahindra | Mahindra and Mahindra targets to launch 16 EV models across its SUV and LCV categories by 2027. |

India’s EV industry is slowly growing, aided by various government policies and higher crude oil prices, as people look for new ways to reduce their monthly bills. However, the large-scale transition from internal combustion engine (ICE) vehicles (ICE) to EVs requires the expansion of infrastructure facilities including charging stations, and vehicles with high electric vehicle range (KM range with a single charge); for in the country Several initiatives by the government to support manufacturing and adoption can help achieve the goal of 100% EV adoption by .

Technological advances and mass production are driving down the cost of EV batteries, increasing the demand for affordable electric vehicles.

EV battery cost reduction to promote demand for low-priced EVs in the electric vehicle industry, the cost of EV batteries has decreased over the last decade as a result of technological improvements and the mass manufacture of EV batteries in enormous quantities. As EV batteries are one of the most expensive components of the car, this has resulted in a fall in the cost of electric vehicles. In , the cost of an EV battery was around USD 1,100 per kWh. However, by , the price had dropped to around USD 137 per kWh, and it was as low as USD 120 per kWh in .

In China electric vehicle market, the price of these batteries may be as low as USD 100 per kWh. This is due to lower manufacturing costs for these batteries, lower cathode material prices, increased output, and so on. The prices of EV batteries are expected to decline to around USD 60 per kWh by , considerably lowering the prices of EVs and making them cheaper than traditional ICE vehicles.

Countries during the world have set objectives to reduce automobile emissions between and . They have begun to promote the development and selling of the electric vehicle market as well as the associated charging infrastructure. For example, the United States government spent $5 million in to encourage electric car infrastructure such as charging stations. Several governments are offering different incentives to adopt EVs, such as reduced or no registration costs and exemptions from import taxes, sales taxes, and road charges. Norway and Germany are making big investments to promote EV sales.

As a result of the strong incentives and subsidies in Europe, there is a rapid increase in the sale of electric vehicles. This has resulted in an increase in demand for EV charging components and equipment such as charging cables, connectors, adapters, and portable chargers. A new concept for a national fast-charging network is planned to be established as part of a collaboration between the US energy and transportation ministries, with potential longer-term advancements including up to 350 kW of direct current fast charging. Stringent CO2 pollution standards have boosted demand for electric automobiles. Governments are investing heavily in offering incentives and subsidies to boost the sale of electric vehicles. These initiatives by governments during the world are estimated to boost demand for electric vehicle market over the next decade.

China, Canada, and the United States have established EV laws, while all nations have established fuel economy criteria. Incentives and subsidies are also provided to EV makers and customers. The United States electric vehicle market offers incentives of up to USD 7,500 for the purchase of new electric vehicles. Most of these nations also offer incentives for the installation of EV charging stations. Europe is expected to be the first area to fully transition to EVs. Most governments in the area have declared plans to phase down ICE car sales over the next several decades. With EV sales, the UK wants to dominate the total electric vehicle market by . Norway intends to launch a similar effort and finish it by 2025. The Netherlands, Israel, Ireland, Iceland, and Denmark have made plans to adopt EVs by . China and Japan also plan to stop ICE vehicle sales by .

EV charging infrastructure standardization: Variations in charging demands have highlighted the necessity to standardize electric car charging stations. Certain voltages may be incompatible with EV charging stations. AC charging stations, for example, give a voltage of 120V AC via level 1 charging stations and 208/240V AC via level 2 charging stations, whilst DC charging stations allow rapid charging via 480V AC. Governments must standardize charging infrastructure in order to create a favorable ecology and encourage electric vehicle market sales. Distinct nations have different quick charging requirements. Japan employs CHAdeMO; Europe, the United States, and Korea employ CCS; while China employs GB/T. Since the country has not attained standardization in rapid charging technologies, the Indian government has enforced the installation of CHAdeMO and CCS systems. However, this regulation raised the cost of installing charging stations.

As a result, the government revised the requirements in July and permitted charging station developers to choose their chosen technique. Tesla, located in the United States, employs high-performance superchargers that are exclusive to Tesla and cannot be utilized by other EVs. The lack of uniformity between nations may have an influence on charging station installation and stifle the growth of the electric car charging station industry. The usage of diverse charging standards during the world is a hurdle to EV charging station harmonization. While firms are working toward the adoption of a common plug or various types of connectors in charging stations, standardization of all charging points remains a long way off. Standardization of charging stations would make charging EVs in public easier and result in quicker increase of electric vehicle market demand globally.

Insufficient EV charging infrastructure: EV charging facilities are few in several areas across the world. As a result, the availability of public EV charging for electric vehicles decreases, lowering adoption. Despite the fact that several nations are in the process of establishing EV charging infrastructure, most countries, with the exception of a few states, have not been able to install the needed number of EV charging stations.

With a well-developed global EV charging network, demand for electric vehicle market is likely to rise. The majority of countries have yet to create such charging networks. The Netherlands has the highest density of EV chargers per 100 km. The Netherlands has the greatest charging station density, with around 19-20 charging stations per 100 km. China comes in second, with around 3-4 charging stations per 100 kilometers. The UK has around 3 charge outlets per 100 km, however the government is aggressively expanding its charging stations in order to phase out ICE car sales by . Germany, the United Arab Emirates, Japan, Singapore, South Korea, Sweden, France, the United States, and Russia have also accelerated the transition to electric vehicle market by installing a huge number of charging stations.

Electric Vehicle Market Segment Analysis:

Based on the Component, the market is segmented into the Battery Cells and Packs, Onboard Chargers, Power Control Units, Power Conditioners, Air Compress and Others. Battery Cells and Packs dominated the Electric Vehicle Market in 2025. Battery systems store the energy needed to power the electric motor, directly influencing the driving experience and operational capabilities in electric Vehicles. With advancements in battery technology, particularly lithium-ion and solid-state batteries, manufacturers are continually enhancing energy density, charging speed, and overall longevity.

This evolution extends the driving range but also improves the overall appeal of electric vehicles to consumers who prioritize range anxiety and convenience. The rapid expansion of the EV market has driven significant investments in research and development aimed at optimizing battery packs, making them lighter, more efficient, and more cost-effective. The growing demand for sustainable and eco-friendly transportation solutions underscores the importance of robust battery systems, as they play a vital role in reducing carbon emissions and reliance on fossil fuels.

By Vehicle Type, the market is segmented into the Passenger Car, Commercial Vehicle and Two Wheelers and Three Wheelers. Passenger Car is expected to dominate the Electric Vehicle Market during the forecast period. Passenger cars represent the largest segment, driven by a surge in consumer awareness regarding environmental sustainability and the rising costs of fossil fuels. These vehicles are ideal for daily commuting but also offer the flexibility and convenience that modern consumers demand. Advances in battery technology have significantly enhanced the range and performance of electric passenger cars, alleviating concerns about range anxiety and making them increasingly attractive to buyers.

The government incentives and supportive policies aimed at promoting electric mobility have further accelerated the transition to electric passenger vehicles. The burgeoning availability of models from a wide range of manufacturers, including both established automakers and innovative startups, has expanded choices for consumers, making EVs more accessible than ever. The enhanced features such as smart connectivity, advanced safety systems, and lower operational costs have made electric passenger cars not just a sustainable alternative but also a desirable choice.

Electric Vehicle Market Regional Insights:

The Asia Pacific region is poised to exert significant dominance over the global electric vehicle market, with three major markets spearheading global sales. According to the 2025 International Energy Agency Report, China, in particular, played a pivotal role, contributing to over 70% of global electric car sales. This surge is attributed to substantial government investments directed towards electrification and sustainable transportation. In the context of Asia Pacific, electric vehicles play a crucial role in achieving net-zero emission targets, driven notably by government support and initiatives aimed at decarbonizing society. By , the Indian government aims for 30% of all vehicles on its roads to be electric, underscoring its commitment to reducing carbon emissions and curbing air pollution. This ambitious target is part of broader efforts to promote sustainable transportation and decrease reliance on fossil fuels.

Electric Vehicle Market Recent Developments:

1. Nissan has committed to to expand its EV lineup, with the Aria electric SUV being a recent addition. The company is also working to expand its global EV footprint to create more efficient batteries.

2. Hyundai and Kia launched several new EV models, including the Hyundai Ionic 5 and Kia EV6, which received positive market reception and international awards for their design and innovative technologies.

3. South Korea is aggressively expanding its EV charging network. The government aims to install 500,000 charging stations by to support the growing demand for electric vehicles.

Electric Vehicle Industry Ecosystem

Electric Vehicle Market Scope: Inquire before buying

| Global Electric Vehicle Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 1,304.64USD Million |

| Forecast Period 2026-2032 CAGR: | 20.90% | Market Size in 2032: | 4,925.91 USD Million |

| Segments Covered: | by Component | Battery Cells and Packs Onboard Chargers Power Control Units Power Conditioners Air Compress Others |

|

| by Vehicle Type | Passenger Car Commercial Vehicle Two Wheelers and Three Wheelers |

||

| by Drive Type | All Wheel Drive Front Wheel Drive Rear Wheel Drive |

||

| by EV Charging Point Type | Normal Charging Super Charging Inductive Charging |

||

| by Range | Up to 150 Miles 151-300 Miles Above 300 Miles |

||

| by Propulsion Type | Battery Electric Vehicle (BEV) Hybrid Electric Vehicle (HEV) Fuel Cell Electric Vehicle (FCEV) |

||

Electric Vehicle Market, by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key players / competitors profiles covered in the Global Electric Vehicle Market report in strategic perspective

1. Tesla - (United States)

2. Rivian - (United States)

3. Chevrolet - (United States)

4. Lucid Motors - (United States)

5. Ford - (United States)

6. Fisker - (United States)

7. Nikola - (United States)

8. Proterra - (United States)

9. Canoo - (United States)

10. Lion Electric - (Canada)

11. Hyliion - (United States)

12. Hyzon Motors - (United States)

13. Faraday Future - (United States)

14. Lordstown Motors - (United States)

15. BMW - (Germany)

16. Stellantis - (Netherlands)

17. Arrival - (United Kingdom)

18. Volkswagen - (Germany)

19. Polestar - (Sweden)

20. NIO - (China)

21. BYD - (China)

22. SAIC Motors - (China)

23. GAC Motors- (China)

24. NIU - (China)

25. Tata Motors- (India)

26. Geely- (China)

27. Wuling Hong Guang MINI EV- (China)

28. Kia - (South Korea)

29. Gogoro - (Taiwan)

30. XPeng - (China)

31. Toyota - (Japan)

32. Li Auto - (China)

33. Nissan - (Japan)

FAQs:

1. Which region has the largest Global Electric Vehicle Market share?

Ans: The Asia Pacific region holds the highest share in 2025.

2. What is the growth rate of Global Electric Vehicle Market?

Ans: The Global Electric Vehicle Market is growing at a CAGR of 4.5% during the forecasting period 2026-2032.

3. What segments are covered in the Global Electric Vehicle market?

Ans: Global Electric Vehicle Market is segmented into Component, Vehicle Type, Drive Type, EV Charging Point Type, Range, Propulsion Type and Region.

4. Who are the key players in the Global Electric Vehicle market?

Ans: The important key players in the Global Electric Vehicle Market are Tesla - (United States), Rivian - (United States), Chevrolet - (United States), Lucid Motors - (United States), Ford - (United States), Fisker - (United States) and others.

5. What is the study period of this market?

Ans: The Global Electric Vehicle Market is studied from 2025 to 2032.