Cooling Tower Market by Type, Technology, Material,Application and Region - Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

The Cooling Tower Market size was valued at USD 5.65 Billion in 2025 and the total Cooling Tower revenue is expected to grow at a CAGR of 4.7% from 2025 to 2032, reaching nearly USD 7.79 Billion by 2032.

This growth is fueled by the rising global adoption of energy-efficient cooling solutions, increasing industrial demand for advanced thermal management systems, and the expansion of smart and eco-friendly cooling tower technologies across key sectors such as power generation, HVAC, and manufacturing.

Cooling Tower Market Overview:

The Cooling Tower Market is witnessing strong growth due to the increasing adoption of energy-efficient cooling systems across industrial, commercial, and power generation sectors. Cooling towers play a critical role in optimizing thermal performance and reducing operational costs, making them essential in HVAC systems, petrochemical plants, and manufacturing facilities. Although these systems improve energy efficiency, they often require higher water usage, creating demand for water-saving cooling tower technologies and hybrid cooling solutions.

Rapid technological advancements, such as the integration of IoT-enabled monitoring, digital control systems, and high-efficiency axial fans, are transforming the global cooling tower industry. For instance, innovations in industrial cooling tower design have allowed companies to achieve substantial energy savings—similar to how Novo Nordisk achieved nearly 5 million kWh annual savings through system optimization. Furthermore, increasing investment in eco-friendly materials, closed-circuit cooling designs, and smart cooling tower systems continues to drive market expansion.

With the ongoing push for sustainability, regulatory compliance, and industrial automation, the global cooling tower market size is expected to grow significantly from 2025 to 2032, driven by the rising focus on smart, sustainable, and cost-efficient cooling tower solutions across all major regions.

To know about the Research Methodology :- Request Free Sample Report

Global Cooling Tower Market Dynamics:

The Cooling Tower Market is witnessing strong growth driven by the rising demand for energy-efficient cooling solutions across industries such as HVAC, power generation, oil & gas, and manufacturing. Increasing industrialization in Asia-Pacific, particularly in China and India, coupled with the expansion of data centers and commercial infrastructure, is fueling the need for advanced industrial cooling tower systems. The shift toward hybrid cooling towers and water-saving cooling technologies is reshaping the market, aligning with global sustainability goals and stringent environmental regulations in Europe and North America.

Technological advancements such as IoT-based monitoring, digital performance analytics, and predictive maintenance systems are enhancing operational efficiency and driving adoption of smart cooling tower solutions. Additionally, the replacement and retrofit market is expanding as industries modernize existing systems to meet new energy standards. However, factors such as high installation costs, corrosion issues, and water scarcity challenges may limit growth in certain regions.

Despite these challenges, the global cooling tower market size is expected to grow significantly during 2025–2032, supported by eco-friendly materials, innovative design improvements, and increasing investment in sustainable industrial cooling systems. These dynamics collectively reinforce the strong growth trajectory of the cooling tower industry worldwide.

Global Cooling Tower Market Segment Analysis

The Global Cooling Tower Market is segmented by Product, and Applications.

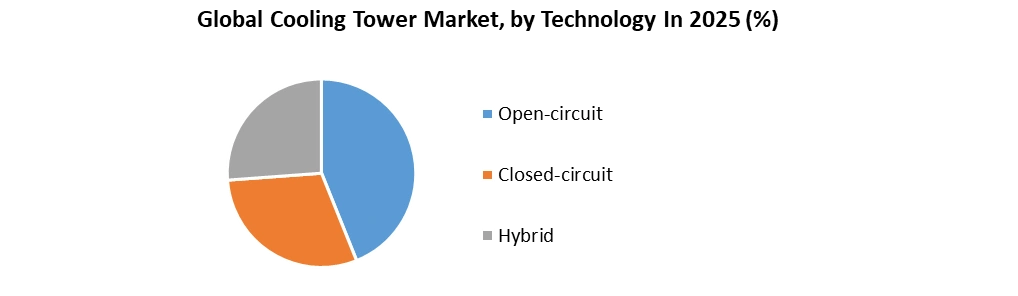

Based on the Technology, In 2025, the closed-circuit type category had the biggest market share of xx %. On the other hand, hybrid towers are predicted to take a significant part of the market throughout the forecast period. The benefits of hybrid towers, such as plume abatement, water savings, and effective cooling, are attributed to this. On the other hand, the open-circuit type resulted in a considerable share in 2025 due to the excellent cooling they give. Due to environmental issues such as drift, plume, and water contamination, the segment is likely to increase steadily throughout the forecast period.

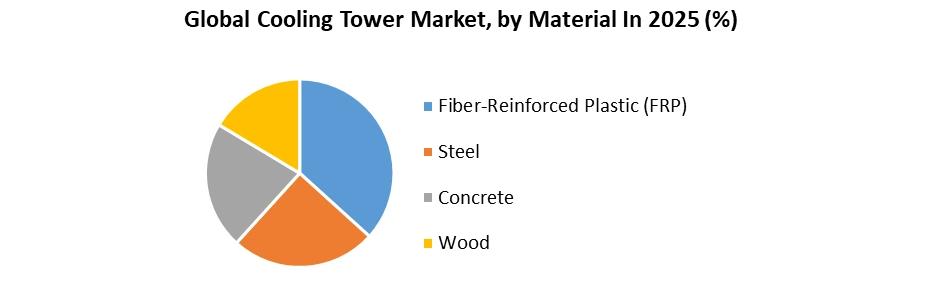

Based on the Material, Fiber-reinforced plastic (FRP), steel, concrete, wood, and High-Density Polyethylene (HDPE) are some of the materials used in cooling towers (HDPE). Due to many features such as excellent corrosion resistance, cost-effectiveness, and ease of installation, the FRP material segment accounted for the highest percentage in 2025. Steel towers, which are comprised of galvanized and stainless steel, also claimed a significant portion of the market in 2025, owing to their excellent corrosion resistance and structural strength. Following this section is the concrete material section, which is expected to develop considerably due to its extended working life.

Cooling Tower Market Regional Insights:

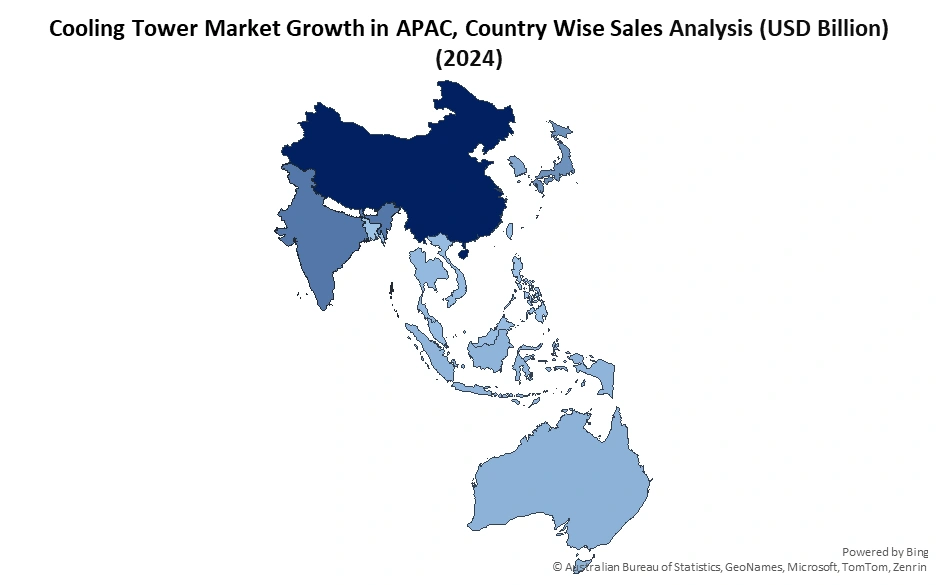

Asia Pacific had the greatest market share, accounting for more than xx% of total sales, closely followed by Europe. Furthermore, from 2025 to 2032, the region is expected to be the fastest-growing market for cooling towers, with a CAGR of over xx%. The demand for these towers in Asia Pacific is likely to be driven by the growing number of manufacturing facilities and the growth of the industrial sector.

Asia Pacific continues to lead the Cooling Tower Market in 2025, driven by the region’s expanding focus on nuclear power capacity addition and large-scale industrial development. As of 2025, the region hosts over 140 operational nuclear reactors, with more than 30 reactors under active construction and an additional 60+ reactors in various planning stages, reinforcing the demand for field-erected cooling towers across power generation projects. This surge in energy infrastructure, combined with rapid growth in manufacturing, chemicals, and HVAC installations, is expected to significantly boost cooling tower deployment in the coming years.

In Europe, market growth in 2025 is primarily supported by stringent environmental regulations, energy-efficiency mandates, and the modernization of aging industrial infrastructure. The rise of heavy industries, along with a strong shift toward sustainable cooling technologies, continues to create new opportunities for cooling tower manufacturers and service providers.

Meanwhile, the Middle East & Africa (MEA) region is witnessing steady growth fueled by the expanding oil & gas sector, petrochemical investments, and increasing installation of high-capacity cooling systems in power and desalination plants. These developments collectively position MEA as a promising market for advanced cooling towers during the forecast period.

Asia Pacific dominates the global Cooling Tower Market, driven by rapid industrialization, expanding power generation capacity, and large-scale infrastructure development.

Asia Pacific dominates the global Cooling Tower Market, driven by rapid industrialization, expanding power generation capacity, and large-scale infrastructure development.

Cooling Tower Market Scope: Inquire before buying

| Cooling Tower Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 5.65 USD Bn |

| Forecast Period 2026-2032 CAGR: | 4.7% | Market Size in 2032: | 7.79 USD Bn |

| Segments Covered: | By Type | Evaporative Dry Hybrid |

|

| By Technology | Open-Circuit Closed-Circuit Hybrid-Circuit |

||

| By Material | Fiber-Reinforced Plastic (FRP) Steel Concrete Wood High-Density Polyethylene (HDPE) |

||

| By Application | HVAC Power Generation Oil & Gas Chemicals & Petrochemicals Food & Beverage Paper & Pulp Mills Others |

||

Cooling Tower Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Cooling Tower Market, Key Players

1. B&W SPIG (Babcock & Wilcox)

2. Baltimore Aircoil Company (BAC)

3. Cenk Industrial Plants Manufacturing and Contracting

4. Cooling Towers Systems; Inc.

5. Delta Cooling Towers

6. Engie Refrigeration GmbH

7. Hamon & CIE SA

8. Johnson Controls Inc

9. Mesan Cooling Towers Ltd

10. Bell Cooling Tower

11. Brentwood Industries Inc.

12. Enexio

13. Hamon & Cie International SA

14. Paharpur Cooling Towers

15. SPIG S.p.A

16. Star Cooling Towers Private Ltd

17. EVAPCO Inc.

18. SPX Cooling Technologies, Inc.

19. Thermax Limited

20. Mitsubishi Heavy Industries, Ltd.

21. Kelvion Holding GmbH

22. Reymsa Cooling Towers, Inc.

23. Tashin Industry Co., Ltd.

24. Composite Cooling Solutions, L.P. (CCS)

25. Whaley Products, Inc.

26. Advance Cooling Towers Pvt. Ltd.

27. SPX Thermal Product Solutions

28. Superchill Cooling Towers Pvt. Ltd.

29. Torrex Cooling Tower

30. Aeron Cooling Towers Pvt. Ltd.

31. Laxmi Engineering

32. Ceramica Cleia

33. Marley Cooling Technologies

34. Delta T Systems, Inc.

35. Pinnacle Industries Ltd.

36. Towertech Cooling System Pvt. Ltd.

Frequently Asked Questions:

1. Which region has the largest share in the Global Cooling Tower Market?

Ans: Asia Pacific region held the highest share in 2025.

2. What is the growth rate of the Global Cooling Tower Market?

Ans: The Global Cooling Tower Market is expected to grow at a CAGR of 4.7% during the forecast period 2026-2032.

3. What is the scope of the Global Cooling Tower market report?

Ans: Global Cooling Tower Market report helps with the PESTEL, PORTER, Recommendations for Investors & Leaders, and market estimation of the forecast period.

4. Who are the key players in the Global Cooling Tower market?

Ans: The important key players in the Global Cooling Tower Market are – B&W SPIG (Babcock & Wilcox), Baltimore Aircoil Company (BAC), Cenk Industrial Plants Manufacturing and Contracting, Cooling Towers Systems; Inc.

5. What is the study period of this market?

Ans: The Global Cooling Tower Market is studied from 2025 to 2032.