Bioburden Testing Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2034

Overview

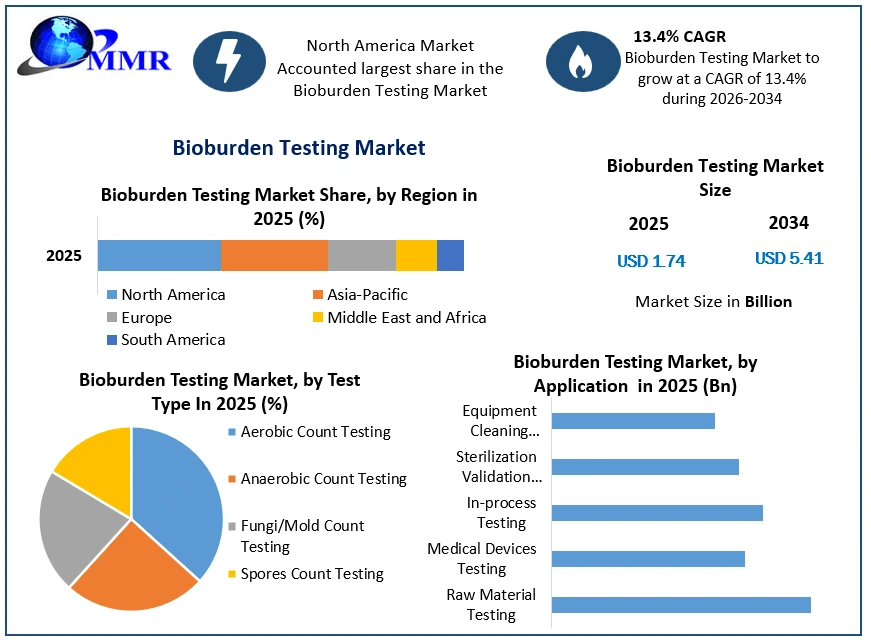

The Bioburden Testing Market size was valued at USD 1.74 Billion in 2025 and the total Bioburden Testing Market revenue is expected to grow at a CAGR of 13.4 % from 2026 to 2034, reaching nearly USD 5.41 Billion.

Bioburden testing is a critical process used to estimate the microbial contamination levels present on medical devices, raw materials, pharmaceutical products, and other items. It involves assessing the total viable microorganisms present, including bacteria, fungi, viruses, and other microorganisms, which pose a risk to product safety and patient health. The primary objective of bioburden testing is to ensure that products meet regulatory standards and are safe for use in healthcare settings by identifying and quantifying the microbial load. The bioburden testing market has been experiencing robust growth in recent years due to the increasing emphasis on product safety, stringent regulatory requirements, and rising awareness regarding microbial contamination risks.

Factors such as the growing demand for quality assurance in pharmaceutical and medical device manufacturing, technological advancements in testing methodologies, and the rising prevalence of healthcare-associated infections (HAIs) are driving market growth. The growing prevalence of chronic diseases necessitates stringent infection control measures and the rising adoption of advanced testing technologies such as rapid microbiological methods (RMMs) and molecular diagnostics. The integration of automation and robotics in bioburden testing processes is streamlining operations, reducing turnaround times, and improving accuracy.

Bioburden Testing Market Growth and Share Analysis

To know about the Research Methodology :- Request Free Sample Report

Trends in the bioburden testing market include the shift towards disposable testing kits and single-use devices to minimize the risk of cross-contamination, the adoption of novel testing methodologies such as nucleic acid amplification techniques (NAATs) for enhanced sensitivity and specificity, and the emergence of point-of-care testing solutions for rapid on-site microbial analysis. There is a growing focus on developing customizable testing protocols tailored to specific industry requirements, along with the integration of artificial intelligence (AI) and machine learning (ML) algorithms for data analysis and interpretation. With the increasing demand for quality assurance in pharmaceutical manufacturing, there is a growing need for innovative testing solutions that offer rapid, reliable, and cost-effective microbial analysis.

Moreover, the growth of the healthcare sector in emerging economies presents lucrative opportunities for market penetration and growth. STEMart, a U.S.-based provider of comprehensive services for medical device development, introduced Bioburden and Sterility Testing services in April 2023. Conducted by ISO 11731 methods, these tests ensure the safety and quality of medical devices, addressing the increasing demand for sterilization validation. Redberry introduced a groundbreaking advancement in bioburden testing technology with their Red One™ technology in September 2023. This innovative solution offers rapid testing results within just 4 hours, revolutionizing the testing process and addressing the critical need for timely quality control measures in pharmaceutical manufacturing.

Bioburden Testing Market Dynamics:

Regulatory Compliance Driving Bioburden Testing Demand:

Increasing regulatory requirements for ensuring product safety and quality in pharmaceutical and medical device manufacturing drive the demand for bioburden testing. For instance, the US FDA mandates bioburden testing for medical devices to prevent contamination and ensure patient safety. The growing prevalence of HAIs in healthcare settings underscores the importance of effective bioburden testing to prevent infections. Hospitals and clinics implement rigorous testing protocols to identify and mitigate microbial contamination risks, driving market growth. The burgeoning pharmaceutical and biotech sectors fuel the demand for bioburden testing solutions to ensure product safety and compliance with regulatory standards. With the increasing production of drugs, vaccines, and biologics, there is a growing need for robust bioburden testing methods.

Innovations in bioburden testing technologies, such as rapid microbial detection systems and automated sample processing, enhance efficiency and accuracy in microbial enumeration. For example, the adoption of advanced molecular techniques like polymerase chain reaction (PCR) accelerates microbial identification, driving market growth. Industries such as medical devices, pharmaceuticals, and cosmetics prioritize sterility assurance to prevent product contamination and ensure patient safety. Bioburden testing plays a critical role in verifying sterilization processes and validating product cleanliness, driving its adoption across various sectors.

The rising trend towards decentralized testing and point-of-care diagnostics drives the demand for rapid bioburden testing methods. With the need for real-time microbial monitoring in healthcare settings, portable and easy-to-use bioburden testing devices are gaining traction, fostering market growth. Heightened awareness of infection prevention measures, particularly in healthcare facilities and pharmaceutical manufacturing, drives the adoption of stringent bioburden testing protocols. Regulatory agencies and industry associations promote best practices for microbial control, leading to greater market demand. The globalization of pharmaceutical supply chains increases the complexity of microbial contamination risks and necessitates robust bioburden testing procedures. With pharmaceutical products being sourced and distributed globally, comprehensive testing ensures product quality and compliance with international standards, driving market growth.

The development of novel therapies such as cell and gene therapies requires stringent bioburden testing to ensure product safety and efficacy. As these innovative treatments gain momentum in the biopharmaceutical industry, the demand for advanced bioburden testing methods, capable of detecting low levels of microbial contamination, grows. Rising investments in healthcare infrastructure, particularly in emerging economies, drive the adoption of advanced bioburden testing solutions. As healthcare facilities upgrade their capabilities and expand their services, there is a parallel increase in the demand for reliable microbial testing technologies to maintain quality standards.

Chart: Bioburden vs. Microbial Limit Test: Comparison Chart

| Bioburden Test | Microbial Limit Test |

| The bioburden performed microbial to test is evaluate contamination levels on or in a product. | Microbial Limits Test determines the bioburden of certain pharmaceutical manufacturing samples. |

| It is performed to measure the total number of viable microorganisms present on medical devices prior to their final sterilization for quality control purposes | It is performed to assess how many and which of viable aerobic microorganisms are present in not-sterile phar- maceutical manufacturing samples, ranging from raw materials to finished products. |

| The bioburden test is either one or both of the compendial TAMC (Total Aerobic Microbial Count) or TYMC (Total Yeast and Mold Count) methods, or an alternative. | There are four recommended methods for microbial limit testing: membrane filtration, direct plating, spread plate and serial dilution. |

Rising prevalence of Healthcare-Associated Infections (HAIs):

Strict regulations in pharmaceutical and medical device manufacturing necessitate rigorous bioburden testing, offering growth opportunities. For instance, the FDA's scrutiny of medical device cleanliness drives demand for comprehensive testing solutions. The growth of healthcare infrastructure worldwide fuels demand for bioburden testing in hospitals, clinics, and diagnostic centers. As new healthcare facilities emerge and existing ones expand, there is a corresponding need for microbial contamination monitoring, creating market opportunities. The increasing incidence of HAIs drives the adoption of bioburden testing to prevent infections and ensure patient safety. For example, the rise in surgical site infections underscores the importance of thorough bioburden assessment in medical settings, presenting growth prospects for testing services. Ongoing advancements in bioburden testing technologies, such as rapid microbial detection systems and automation, enhance efficiency and accuracy. For instance, the development of automated microbial enumeration platforms streamlines testing processes, driving market growth.

The pharmaceutical industry's growth, particularly in emerging markets, increases the demand for bioburden testing. With the establishment of new manufacturing facilities and the production of biologics, there is a growing need for microbial control measures, driving market growth. Increasing adoption of sterilization methods in various industries, including healthcare, food, and cosmetics, drives demand for bioburden testing. As companies strive to ensure product sterility and compliance with regulatory standards, there is a heightened need for microbial assessment, presenting market opportunities. Heightened emphasis on product quality and safety across industries fuels the demand for bioburden testing. For example, in the food and beverage sector, ensuring microbial control is essential to prevent contamination and maintain product integrity, driving the need for testing services.

Companies outsource bioburden testing to specialized laboratories to ensure accurate and reliable results. As the outsourcing trend continues to grow, there is a corresponding increase in demand for third-party testing services, offering opportunities for testing service providers. With growing awareness of environmental contamination risks, industries invest in bioburden testing for environmental monitoring purposes. For example, in water treatment plants, bioburden testing helps ensure water quality by detecting microbial contamination, driving the market growth for testing solutions. The trend towards decentralized testing and point-of-care diagnostics creates opportunities for portable bioburden testing devices. With the need for real-time microbial assessment in various settings, such as clinics and field operations, portable testing solutions gain traction, driving market growth.

Stringent Regulatory Requirements Challenge Bioburden Testing Compliance:

The expense associated with bioburden testing is prohibitive for smaller companies or facilities, limiting their ability to perform thorough testing. For instance, advanced molecular techniques like polymerase chain reaction (PCR) are costly to implement, especially for laboratories with limited budgets. Bioburden testing involves intricate procedures and specialized equipment, requiring skilled personnel for the accurate interpretation of results. This complexity leads to errors or inconsistencies in testing outcomes, impacting reliability.

For example, the interpretation of colony-forming unit (CFU) counts in microbial enumeration requires expertise and varies between analysts, affecting test accuracy. Adhering to stringent regulatory requirements for bioburden testing, such as those set by the FDA, EMA, or other regulatory bodies, poses challenges for companies. Non-compliance results in regulatory sanctions or product recalls, leading to financial losses and damage to reputations. For instance, failure to comply with Good Manufacturing Practices (GMP) standards results in regulatory actions against pharmaceutical manufacturers.

Some product matrices, such as viscous liquids or complex formulations, interfere with microbial detection methods, affecting test accuracy. For example, antimicrobial agents present in pharmaceutical formulations inhibit microbial growth, leading to false-negative results in bioburden testing. Traditional bioburden testing methods often involve lengthy incubation periods, delaying product release and time-to-market. For instance, agar plate culture methods require incubation for several days to allow microbial colonies to grow, prolonging testing timelines and impacting production schedules. Some bioburden testing methods lack the sensitivity to detect low levels of microbial contamination, especially in products with stringent sterility requirements.

For instance, conventional plate count methods fail to detect low levels of viable microorganisms, posing a risk of undetected contamination in pharmaceutical products or medical devices. Testing laboratories face limitations in throughput capacity, especially during peak demand periods or in response to urgent testing requirements. This constraint leads to backlogs in testing schedules and delays in result reporting, affecting product release timelines. For example, during public health emergencies or outbreaks, laboratories struggle to accommodate increased testing volumes, resulting in delays in identifying microbial contaminants.

Bioburden Testing Market Segment Analysis:

Based on Test Type, Aerobic Count Testing emerges as the dominant segment, primarily due to its relevance in assessing the total aerobic microbial load in various products and environments. This method is widely adopted across industries such as pharmaceuticals, medical devices, and food processing, where aerobic microbes pose significant contamination risks. Anaerobic Count Testing, while important for assessing anaerobic microbial populations, holds a smaller share compared to aerobic testing, reflecting its limited application in certain industries. Fungi/Mold Count Testing occupies a significant portion of the market, driven by the increasing awareness of fungal contamination risks in healthcare settings and pharmaceutical manufacturing.

Spores Count Testing stands out as a niche segment with specialized applications, particularly in assessing the presence of bacterial endospores in sterilization validation processes. Looking ahead, Aerobic Count Testing is expected to maintain its dominance, driven by stringent regulatory requirements and the growing emphasis on product safety and quality across industries. Fungi/Mold Count Testing is anticipated to witness growth due to rising concerns about fungal infections and product spoilage, while Anaerobic Count Testing and Spores Count Testing are expected to remain relatively stable, catering to specific niche applications in the market.

Bioburden Testing Market Regional Insights:

North America currently holds a prominent position in the market, attributed to stringent regulatory requirements, advanced healthcare infrastructure, and a robust pharmaceutical industry. The region boasts several key players such as Charles River Laboratories International Inc., Sigma-Aldrich Corporation, and Merck & Co. Inc., driving market growth through innovative testing solutions. Europe follows closely, characterized by a well-established healthcare system, increasing investments in research and development, and a growing emphasis on quality control measures. Companies like SGS S.A. and Becton, Dickinson, and Company are prominent players in this region, contributing to market dominance. Asia Pacific emerges as a region with significant growth potential, fueled by expanding pharmaceutical and biotechnology sectors, increasing healthcare expenditure, and rising awareness about infection prevention. With headquarters in Asia, companies like Wuxi Pharmatech (CAYMAN) Inc. and Pacific Biolabs are leading players driving market growth.

The Middle East and Africa region exhibits steady growth, supported by improving healthcare infrastructure and a growing demand for quality assurance in pharmaceutical manufacturing. Notable players in this region include Nelson Laboratories Inc. and ATS Labs Inc., contributing to market development. South America presents opportunities for market growth, driven by increasing investments in healthcare infrastructure and a burgeoning pharmaceutical industry.

Market dominance in this region is still evolving, with companies like North American Science Associates Inc. playing a role in shaping market dynamics. Asia Pacific is expected to witness the fastest growth rate, supported by favorable government initiatives, expanding research capabilities, and a growing focus on product safety and quality across industries. As regulatory standards become more stringent globally, all regions are poised to experience steady market growth, with Asia Pacific leading the way in terms of growth and innovation.

Bioburden Testing Market Competitive Landscape

Recent advancements in bioburden testing technology by Redberry and STEMart's introduction of Bioburden and Sterility Testing services are poised to drive significant market growth and create opportunities in the forecast period. Redberry's Red One™ technology, offering rapid testing results in just 4 hours, addresses the critical need for timely quality control measures in pharmaceutical manufacturing, enhancing efficiency and ensuring compliance with regulatory standards. Similarly, STEMart's comprehensive testing services cater to the increasing demand for sterilization and validation in medical device development, thereby bolstering market growth by providing essential solutions for ensuring product safety and regulatory compliance. These innovations are expected to fuel market expansion by meeting industry needs efficiently and effectively.

On September 25th, 2023, Redberry introduced a groundbreaking advancement in bioburden testing with their Red One technology, offering rapid bioburden testing results within just 4 hours, along with sterility confirmation in a mere 4 days. This innovation revolutionizes the testing process, significantly reducing the time required for microbial analysis of pharmaceutical products. By providing quicker and more efficient testing solutions, Redberry addresses the critical need for timely quality control measures in pharmaceutical manufacturing, ensuring product safety and compliance with regulatory standards.

In April 2023, STEMart, a U.S.-based provider of comprehensive services for medical device development, launched Bioburden and Sterility Testing services. Conducted by the ISO 11731 method, these tests ensure the safety and quality of medical devices. In response to FDA and other regulatory requirements, the validation of sterilization processes becomes imperative, making Bioburden and Sterility Testing indispensable. These tests detect and quantify microorganisms, with Bioburden Testing assessing microbial levels on device surfaces and Sterility Testing validating sterilization efficacy. This recent development enhances medical device manufacturing by ensuring compliance with stringent regulatory standards and maintaining product safety.

Bioburden Testing Market Scope: Inquire before buying

| Bioburden Testing Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | US $ 1.74 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 13.4% | Market Size in 2034: | US $ 5.41 Bn. |

| Segments Covered: | by Product | Consumables Culture Media and Reagents & Kits Other Consumables Instruments Automated Microbial Identification Systems PCR Microscopes Other Instruments |

|

| by Test Type | Aerobic Count Testing Anaerobic Count Testing Fungi/Mold Count Testing Spores Count Testing |

||

| by Application | Raw Material Testing Medical Devices Testing In-process Testing Sterilization Validation Testing Equipment Cleaning Validation |

||

| by End-User | Pharmaceutical and Biotechnology Companies Medical Device Manufacturers Contract Manufacturing Organizations (CMOs) Food & Beverage and Agricultural Products Microbial Testing Laboratories |

||

Bioburden Testing Market by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Bioburden Testing Market Key Players:

Key Players in North America:

1. Charles River Laboratories International Inc. (Massachusetts, USA)

2. Sigma-Aldrich Corporation (Missouri, USA)

3. Merck & Co. Inc. (New Jersey, USA)

4. Becton, Dickinson, and Company (New Jersey, USA)

5. Nelson Laboratories Inc. (Utah, USA)

6. Pacific Biolabs (California, United States)

Key Players in Europe:

7. SGS S.A. (Geneva, Switzerland)

8. Merck & Co. Inc.(Darmstadt, Germany)

9. Becton, Dickinson, and Company (Eysins, Switzerland)

10. North American Science Associates Inc. (Liverpool, United Kingdom)

11. ATS Labs Inc. (Ede, Netherlands)

Key Players in Asia Pacific:

12. Wuxi Pharmatech (CAYMAN) Inc. (Jiangsu, China)

13. Pacific Biolabs (China)

14. Charles River Laboratories International Inc. (China)

15. Nelson Laboratories Inc. (Japan)

Frequently Asked Questions:

1. What are the growth drivers for the Bioburden Testing Market?

Ans. Regulatory Compliance Driving Bioburden Testing Demand expected to be the major driver for the Bioburden Testing Market.

2. What are the major Opportunity for the Bioburden Testing Market growth?

Ans. Rising prevalence of Healthcare-Associated Infections (HAIs) is the major opportunity for the Bioburden Testing market.

3. Which country is expected to lead the global Bioburden Testing Market during the forecast period?

Ans. North America is expected to lead the Bioburden Testing Market during the forecast period.

4. What is the projected market size and growth rate of the Bioburden Testing Market?

Ans. The Bioburden Testing Market size was valued at USD 1.74 Billion in 2025 and the total Bioburden Testing Market revenue is expected to grow at a CAGR of 13.4 % from 2026 to 2034, reaching nearly USD 5.41 Billion.

5. What segments are covered in the Bioburden Testing Market report?

Ans. The segments covered in the Bioburden Testing Market report are by Product, Test Type, Application, End User, and Region.