Agricultural Biologicals Market Size by Product, Crop Types, Source, Mode of Application, Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

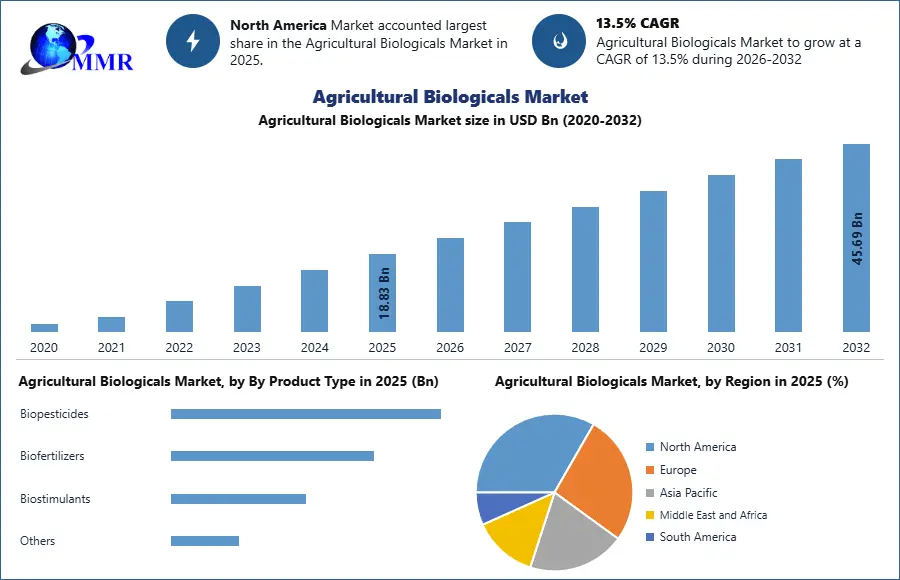

Agricultural Biologicals Market was valued at USD 18.83 Bn in 2025, and the Global Agricultural Biologicals Market is expected to reach USD 45.69 Bn by 2032, growing at a CAGR of 13.5% during the forecast period.

Agricultural Biologicals Market Overview:

Agricultural biologicals are innovative nature-based technologies that serve as an important part of many integrated crop management systems, often in the form of biocontrols and biostimulants. When complemented by leading seeds & traits, digital tools, and chemical crop protection, biologicals can help growers achieve the best results in their fields.

Agricultural biologicals market refers to the industry focused on natural, biological products used in agriculture to enhance crop health, productivity, and protection. Agricultural Biologicals Market is also recording a high growth rate, whereby the changing consumer trend towards consuming organically produced food is a major contributor.

The Agricultural Biologicals Market is rapidly expanding, fueled by the growing global demand for organically produced food, which reached approximately USD 135 billion in 2025. Consumers' preference for residue-free produce is driving adoption of bio-based inputs like biopesticides, biofertilizers, and biostimulants. Biopesticides are leading the market, offering natural alternatives to chemical pesticides. Also, foliar spray dominates the mode of application due to its high efficiency in nutrient delivery. Sustainable farming initiatives, such as the EU’s Farm to Fork Strategy and increased U.S. EPA biopesticide registrations, are accelerating market growth. The Asia Pacific region leads due to economic growth, crop protection demand, and regulatory support, with key players like Bayer and Syngenta expanding R&D efforts there. The market is highly competitive, with recent M&As such as Syngenta’s acquisition of Intrinsyx Bio and Bayer’s biological product expansions. Innovation and strategic partnerships continue to shape the market toward environmentally sustainable agriculture. To know about the Research Methodology:- Request Free Sample Report

To know about the Research Methodology:- Request Free Sample Report

Agricultural Biologicals Market Dynamics:

Increasing Consumer Trend of Organically Produced Food Drives the Agricultural Biologicals Market

The rise in consumer demand of organically grow food is a significant trend that is behind the agricultural biologicals market. Globally, the market value of organic food in 2024 was approximated to be USD 135 billion with the US alone registering USD 19.2 billion organic fresh fruits and vegetable sales in the year 2024. Sustainability and the demand of the residue-free produce are forcing farmers to apply biological pesticides, fertilizers, and biostimulants, which are included in the organic farming system as more regulated.

Sustainable Farming Driving the Agricultural Biologicals Market Growth

Agricultural biologicals market undoubtedly is increasing on account of sustainable farming practices. To give an example, the European Union initiates the Farm to Fork Strategy, which aims at reducing the consumption of chemical pesticides by half as soon as by 2030, the demand in biological alternatives, in its turn, is induced. Similarly, 40 percent increases in the speed of biopesticide registrations was introduced in 2024 by the U.S. EPA. Environmental needs and the regulations by the government that have resulted to transition of global farming into environmentally sensitive farming makes the biologicals a must-have to the growers.

Unpredictable Performance Restraints the Agricultural Biologicals Market

The resultant instability of agricultural biologicals makes a considerable limitation. They may be highly effective or ineffective depending on sensitivity to such environmental factors as soil type, temperature, and moisture levels. It has also been reported that 30-40 percent of the biological products lose their efficacy in 6-12 months of storage using the standard storage conditions. Retailers also can report fluctuating performance, with only about 45 percent of the time resulting in retailers reporting a good to excellent rating, causing farmers reluctance and lack of adoption by others.

Agricultural Biologicals Market Segmentation Analysis:

In 2025, the Product Type segment is dominated by Biopesticides, driven by increasing demand for eco-friendly crop protection solutions and the rising restrictions on chemical pesticides. Within this category, microbial-based biopesticides hold a significant share due to their effectiveness against a wide range of pests. Biostimulants are the fastest-growing segment, particularly seaweed extracts and acid-based products, as they enhance plant growth, stress tolerance, and yield quality. Biofertilizers, especially nitrogen-fixing and phosphate-solubilizing types, are gaining steady traction due to their role in improving soil fertility and reducing dependency on synthetic fertilizers.

Based on Form, the Liquid segment holds the highest demand in 2025 due to its ease of application, better absorption, and compatibility with modern irrigation systems such as drip and fertigation. Liquid formulations are widely preferred for foliar sprays and soil applications. However, the Solid segment continues to maintain relevance, particularly in seed treatment and traditional farming practices, due to its longer shelf life and ease of storage.

Based on Crop Types, Fruits and Vegetables dominate the market in 2025 owing to the increasing consumer preference for organic and residue-free produce. The demand for high-quality yield and improved shelf life further drives the adoption of agricultural biologicals in this segment. Plantation & Specialty Crops also represent a significant share due to export-oriented farming practices. Meanwhile, Floriculture & Ornamentals are witnessing rapid growth as growers increasingly adopt biological inputs to maintain aesthetic quality and sustainability standards.

| Agricultural Biologicals Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 18.83 USD Bn |

| Forecast Period 2026-2032 CAGR: | 13.5% | Market Size in 2032: | 45.69 USD Bn |

| Segments Covered: | By Product Type | Biopesticides Biochemicals Microbials Others Biofertilizers Nitrogen Fixation Phosphate Solubilizing Others Biostimulants Acid Based Seaweed Extract Others Others |

|

| By Form | Solid Liquid |

||

| By Crop Types | Fruits Vegetables Floriculture & Ornamentals Plantation & Specialty Crops Others |

||

| By Source | Microbial-Based Plant Extracts Others |

||

| By Mode of Application | Foliar Application Soil Treatment Seed Treatment Root Dip / Transplant Treatment Drip Irrigation / Fertigation Others |

||

Agricultural Biologicals Market Regional Insights:

Significant Growth in Demand, R&D, and Sustainable Practices creates an Asia-Pacific Dominated Agricultural Biologicals Market

The Asia Pacific is expected to witness significant growth in the global agricultural biologicals market during the forecast period. The growth in the market can be attributed to the growing demand for crop protection and crop nutrition products in the regional market, in line with the rising economic growth conditions. Some of the key players like Bayer, Monsanto, and Syngenta are focusing on tapping this potential market and also expanding their R&D centers across the region. Strict regulations on chemical usage have been limited in the agriculture industry across major countries and governments have been endorsing sustainable practices in developing countries like China and India.

Agricultural Biologicals Market Competitive Landscape:

Agricultural Biologicals Market Top key players include Bayer AG, Syngenta AG, BASF SE, Corteva Agriscience, and UPL Ltd.

In the recent news, Syngenta acquired Intrinsyx Bio (May 2025) to strengthen nutrient use efficiency, and Bayer concentrated on the existing biological (e.g., Serenade) expansion and creation of new ones (e.g., Ibisio) (June 2025). The former organization is leading the way to use artificial intelligence to speed up the process of biological discovery (June 2025), and the latter is positioning its ag business to go public in 2027, setting its sights on growth in Asia. UPL, via UPL-SAS, is betting big on tech and climate (Dec 2024), a move that would see it transform to a holistic solution provider. This competition injects innovation, M&A, and strategic business alliances, which are interested in effective and sustainable agricultural processes to address the increased demand and need of clean, safe agriculture.

Agricultural Biologicals Market Key Trends:

• Convergence with Digital and Precision Agriculture

Digital and precision farming the intersection of agricultural biologicals and advanced digital and precision farming technology is a significant shift. It includes AI-powered platforms, satellite and aerial images, drones and GPS-driven equipment to maximize timing, dose rates and the localized application of biologicals. Such synergy promotes effectiveness, eliminates wastage, and enables evidence-based predictions about plant responses and the dynamics of the soil microbiome, which increases farmer ROI significantly.

• Focus on Novel Bio-Nematicides and Post-Harvest Biocontrols

Biofertilizer, biostimulants and biopesticide have already emerged, but there is also emerging and distinct focus on specialized segments. Bio- nematicides are a fast-growing segment and are used to fight the microscopic worms that lead to huge crop losses. Moreover, use of beneficial microorganisms in post-harvest biocontrols is also emerging to increase the shelf life and limit spoilage of produce, addressing the much-needed food security issue

• Agrochemical giants Strategy on Brand Launches and Portfolio Integration

Large agrochemical firms no longer view biologicals as a niche but are positioning dedicated biological brands and coupling them within their core portfolios. This is an indication of moving towards offering full-chain solutions which incorporates the combination of conventional and biological inputs. Such strategic hug gave the biologicals industry legitimacy and hastened the acceleration of their use by distribution channel and farmer credibility.

Recent Industry Developments

| Year | Company Name | Key Development |

| May 13, 2025 | Bayer AG | Announced a $100 million expansion of its biologicals R&D facility in California, focusing on next-generation microbial products, and committed to over €3.5 billion incremental sales from innovation by 2029. |

| Feb 26, 2025 | Syngenta AG | Strengthened global leadership in agricultural biologicals by acquiring natural product and genetic strain assets from Novartis and inaugurating a cutting-edge production facility in South Carolina, USA. |

| Mar 5, 2024 | BASF SE | Expanded its BioSolutions offering by incorporating seaweed biostimulants through a partnership with Acadian Plant Health™, and invested in a new fermentation plant for biological crop protection products in Ludwigshafen. |

| Dec 21, 2023 | Corteva Agriscience | Launched "Corteva Biologics" to provide farmers with a comprehensive portfolio covering the entire planting cycle, signaling an expanded and dedicated biologicals business. |

| May 12, 2025 | UPL Ltd. | Highlighted a strategic shift towards a comprehensive solution provider model, with significant investment in technology and climate solutions, emphasizing leadership in biosolutions and sustainable farming. |

Agricultural Biologicals Market Scope: Inquire before buying

Agricultural Biologicals Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players / Competitors Profiles Covered in Brief in Global Agricultural Biologicals Market Report in Strategic Perspective:

- Bayer AG

- BASF SE

- Corteva Agriscience

- Syngenta

- UPL

- Novozymes

- Certis Biologicals

- Isagro SpA

- Koppert Biological Systems

- Valent BioSciences

- Agricen

- Lallemand Inc.

- Bioceres Crop Solutions

- Rizobacter S.A.

- Sigma Agri-Science LLC

- Agrinos Inc.

- Biomaxnaturals

- Andermatt Group AG

- Atlántica Agrícola

- Gujarat State Fertilizers & Chemicals Ltd

- IPL Biologicals Ltd.

- T.Stanes & Company Ltd

- Som Phytopharma Biotech

- Biobest Group NV

- Others