Beer Market Size by Product, Type, Application, End-User, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2034

Overview

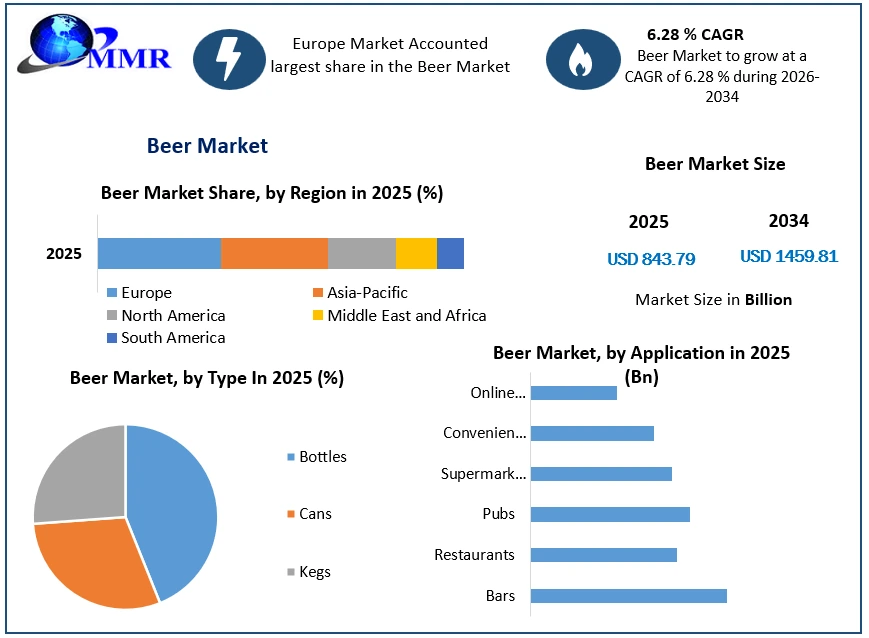

The Beer Market size was valued at USD 843.79 billion in 2025, and the total Beer revenue is expected to grow at a CAGR of 6.28% from 2026 to 2034, reaching nearly USD 1459.81 Billion.

Global Beer Market Overview and Scope

The Global Beer Market is witnessing steady growth in 2025 due to rising premium beer consumption, craft beer demand, flavored beer innovation, urbanization, and increasing online alcohol sales. Europe dominates consumption, while Asia Pacific emerges as the fastest-growing regional market driven by changing lifestyles and rising disposable income.

Key Highlights of the Global Beer Market

- The Global Beer Market was valued at USD 843.79 Billion in 2025 and is projected to reach nearly USD 1292.39 Billion by 2032

- The Beer Market is expected to grow at a CAGR of 6.28% during the 2025–2032 forecast period.

- Europe dominated the global beer consumption market in 2025.

- Asia Pacific emerged as the fastest-growing beer market in 2025 driven by urbanization and rising disposable incomes.

- China remained the world’s largest beer-consuming country by volume in 2025.

- Craft beer demand increased significan among millennials and Gen Z consumers.

- Premium and flavored beer segments witnessed strong growth due to changing consumer preferences.

- Non-alcoholic and low-alcohol beer demand expanded rapidly, owing to rising health-conscious consumption trends.

- Online alcohol retail and e-commerce beer sales accelerated globally.

- Leading players including AB InBev, Heineken, and Carlsberg focused on innovation and regional expansion strategies.

Global Beer Market Snapshot

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Global Beer Market Dynamics

A thorough analysis of the worldwide beer industry has been performed, revealing that various crucial elements are impacting its expansion and progress. The evolving preferences of consumers are having a noteworthy impact on the beer industry. Consumers are increasingly in search of distinctive and high-quality beer experiences, which has resulted in a surge in demand for craft and artisanal beers. The market is being influenced by health and wellness trends, with a growing number of consumers looking for healthier beer alternatives, including low-calorie, low-alcohol, and gluten-free options. The current trend has led manufacturers to explore new avenues and provide more nutritious options in comparison to conventional beer choices.

There is a noticeable trend in the market towards premiumization and flavour innovation. Consumers are showing a willingness to pay a higher price for speciality and flavoured beers that provide distinctive and thrilling taste experiences. There is a growing trend towards sustainability and environmental consciousness among consumers, which has led breweries to implement sustainable practises in order to meet this demand for eco-friendly products. The current trend of globalisation and market expansion has led breweries to explore emerging beer markets and expand their global presence. The increasing prevalence of digital platforms and e-commerce has facilitated consumer access to a diverse range of beers, thereby bolstering market expansion. By analysing these market trends and utilising the opportunities they offer, breweries can strategically position themselves for success in this ever-changing and highly competitive industry.

Global Beer Market Segment Analysis

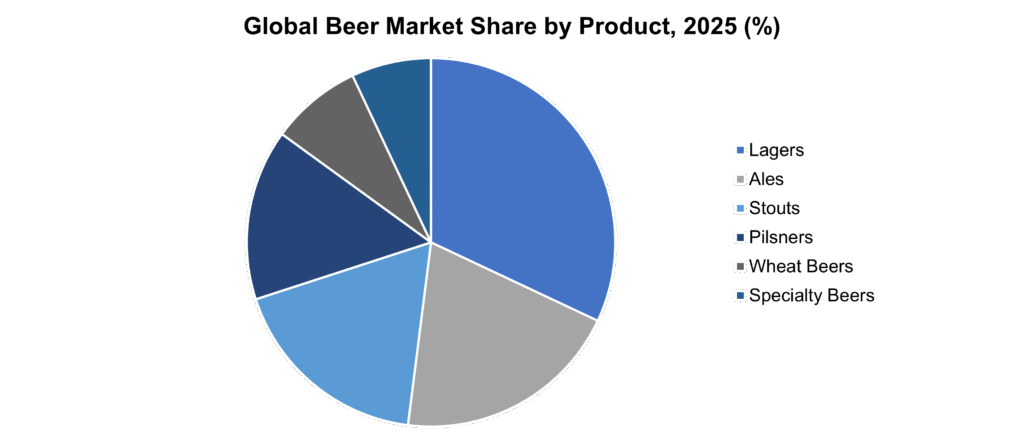

Variety, packaging, sales channels, and location characterise the beer industry. The market includes lagers, ales, stouts, pilsners, wheat beers and speciality beers. Lagers are popular and mass-produced, dominating the market. Due to customer interest in unique tastes, handcrafted brewing methods, and high-end products, the craft beer business, which includes ales, stouts, and speciality beers, is growing. Bottles, cans, and kegs contain beer.

Bottled beer dominates the market. Its convenience and availability are the main reasons. Due to its simplicity, eco-friendliness, and canning advances, canned beer is becoming more popular, especially among younger people. When assessing distribution channels, the on-trade segment—bars, restaurants, and pubs—continues to drive sales. Due to e-commerce and at-home consumption, the off-trade segment, which comprises supermarkets, convenience stores, and online platforms, has grown significantly. Regional tastes shape the beer market. Due to its high beer consumption and rich beer history, Europe dominates the beer market. Breweries can tailor their products, packaging, distribution strategies, and marketing to meet consumer preferences and regional demands by understanding the segmentation categories and their market shares. This ensures global beer market growth and competitiveness.

Beer Market Regional Analysis

Global beer market is analysed by region, considering consumption patterns, cultural preferences, and market dynamics in different parts of the world. North America has a strong beer culture & craft beer movement, making it a significant market for beer. US sees rise in craft beer demand due to unique flavours and local brewing. Europe dominates the global beer market due to its rich beer heritage. Germany, Belgium, and the Czech Republic are known for their traditional beer styles and brewing techniques. Craft beer consumption in the region is on the rise, with an emphasis on quality and variety.

Asia Pacific has great potential in the beer market. Beer consumption in China, Japan, and India is rapidly increasing due to changing lifestyles, urbanisation, and higher disposable incomes. Craft beers are gaining popularity in this region due to younger demographics and Western beer culture, despite mainstream lagers dominating the market.

Vibrant beer market in South America, led by Brazil and Argentina. Regions prefer light and refreshing beers for social and festive occasions. Craft beer is growing in popularity in South America, appealing to a niche market looking for distinct flavours and premium quality beer. Middle East and Africa beer market encounters cultural and regulatory hurdles. Growing demand for beer in South Africa and Nigeria due to urbanisation, population growth, and westernisation of consumer preferences. Non-alcoholic and low-alcohol beer are growing in this region due to cultural and religious reasons.

Regional variations and preferences in the global market are crucial for breweries to develop effective marketing strategies, product portfolios, and distribution networks. Analysing regional trends, cultural nuances, and consumer demands helps industry stakeholders identify growth opportunities and tailor their offerings to establish a strong presence in each market, contributing to the overall success of the global beer industry.

Global Beer Market Recent Industry Developments (2025–2026)

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 06 May 2026 | Carlsberg Breweries | The company issued a €1.8 billion dual-tranche euro hybrid bond to manage its capital structure following recent major acquisitions. | The issuance is designed to accelerate deleveraging and strengthen the balance sheet after the multi-billion pound integration of its beverage portfolio. |

| 03 April 2026 | Constellation Brands | The company completed the acquisition of HopWtr, a prominent brand in the non-alcoholic, hop-infused sparkling water segment. | The deal expands the company's alcohol-adjacent portfolio and leverages its extensive retail network to drive the distribution of functional beer alternatives. |

| 11 February 2026 | Heineken N.V. | The brewer finalized the acquisition of FIFCO’s beverage and retail businesses in Central America to solidify its regional footprint. | This strategic move is expected to be immediately accretive to earnings per share and positions the company for high-growth opportunities in the Latin American market. |

| 01 September 2025 | Ironhill India | The brand officially launched “Zero Gravity AF,” its first non-alcoholic wheat beer featuring less than 0.5% ABV. | The launch targets the health-conscious consumer segment in emerging markets, addressing the rising demand for low-alcohol alternatives. |

| 14 August 2025 | United Breweries | The company inaugurated a new ₹90 Crore canned beer production facility at its Nizam Brewery in Telangana. | The expansion significantly boosts the production capacity for Kingfisher and Heineken brands to meet localized consumer demand for canned formats. |

Global Beer Market Competitive Analysis

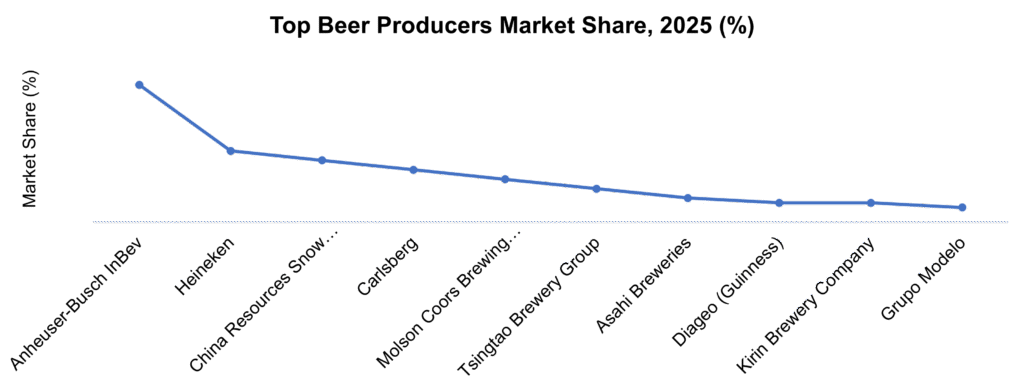

Multinationals, regional breweries, and craft beer makers have a strong competition in the global beer industry. Anheuser-Busch InBev, Heineken N.V., and China Resources Snow Breweries lead the market with their wide product lines and global distribution networks. Brand recognition, economies of scale, and product innovation keep these enterprises competitive.

United Breweries Ltd. (UBL), renowned for Kingfisher, dominates the Indian beer market. UBL offers a variety of beer for diverse tastes. Anheuser-Busch InBev India Pvt. Ltd. is another key player. Budweiser and Corona are strong brands in premium and super-premium beer. Carlsberg India Pvt. Ltd., which makes Carlsberg and Tuborg, is another major Indian beer company. Craft and microbreweries are growing in the Indian beer market alongside these major names. Smaller breweries make specialty beers for specific markets and local markets. Bira 91, White Owl Brewery, and Gateway Brewery are Indian craft beer brands.

Brand recognition, quality, pricing, distribution, and marketing drive worldwide beer market competition. Diverse beer styles, flavours, and packaging help breweries stand out. They also address consumer demands for healthier, low-alcohol, and ecologically friendly beer. Breweries engage in R&D to create new recipes, enhance brewing methods, and try novel ingredients to stay competitive. Collaborations with other breweries, suppliers, and distributors are frequent ways to reach new markets. Breweries use traditional and digital venues to promote brand awareness and loyalty.

Competitive analysis in the global market entails studying market trends, key player performance, product innovations, and customer preferences. This analysis helps organizations identify market opportunities, implement targeted strategies, and stay ahead in the fast-paced global beer industry.

Beer Market Scope: Inquire before buying

| Global Beer Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 843.79 Billion |

| Forecast Period 2026-2034 CAGR: | 6.28% | Market Size in 2034: | USD 1459.81 Billion |

| Segments Covered: | by Product | Lagers Ales Stouts Pilsners Wheat Beers Specialty Beers |

|

| by Type | Bottles Cans Kegs |

||

| by Application | Bars Restaurants Pubs Supermarkets Convenience Stores Online Platforms |

||

| by Category | Premium Beer Mainstream Beer Super Premium Beer Economy Beer |

||

| by Alcohol Content | Low-Alcohol Beer Standard-Strength Beer High-Alcohol Beer |

||

| by Distribution Channel | On-Trade Off-Trade |

||

| by Consumer Group | Millennials Gen Z Consumers Female Consumers Premium Consumers |

||

Beer Market, Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Beer Market, Key Players

The captured list of leading manufacturers of Beer industry has been compiled after an analysis of multiple factors. It is not an exhaustive list based only on market share ranking. After a regional analysis, a competitive analysis and other such considerations, the company profiles were selected based on a variety of factors. The comprehensive report contains information on the position of each company in the market from local and global perspective.

1. Anheuser-Busch InBev

2. SABMiller

3. Molson Coors Brewing Company

4. Heineken

5. Carlsberg

6. China Resources Snow Breweries

7. Tsingtao Brewery

8. Yanjing Brewery

9. Grupo Modelo

10. Kirin Brewery Company

11. Asahi Breweries

12. Mahou San Miguel

13. Estrella Galicia

14. Fuller's

15. Diageo

16. AB InBev Efes

17. Boston Beer Company

18. Sierra Nevada Brewing Company

19. New Belgium Brewing

20. Oskar Blues Brewery

21. Stone Brewing

22. Deschutes Brewery

23. Lagunitas Brewing Company

24. Founders Brewing Company

25. Ballast Point Brewing Company

FAQs

1. What was the Global Beer Market size in 2025?

Ans: The Global Beer Market size was USD 843.79 Billion in 2025.

2. What is the projected growth rate of the global market?

Ans: The forecasted CAGR of the global market is 6.28% during the forecast period.

3. What are the different types of beers available in the market?

Ans: The Global Beer Market includes lagers, ales, stouts, pilsners, wheat beers, craft beers, non-alcoholic beers, and specialty beers.

4. Which regions are the major consumers of beer?

Ans: Europe dominated the Global Beer Market in 2025, while Asia Pacific emerged as the fastest-growing regional market due to rising urbanization and disposable income.

5. What are the key factors driving the growth of the global beer market?

Ans: Rising craft beer demand, premiumization trends, flavored beer innovation, non-alcoholic beer consumption, sustainable brewing practices, and growth in online alcohol retail are driving the Global Beer Market growth.