Battery Electrolyte Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

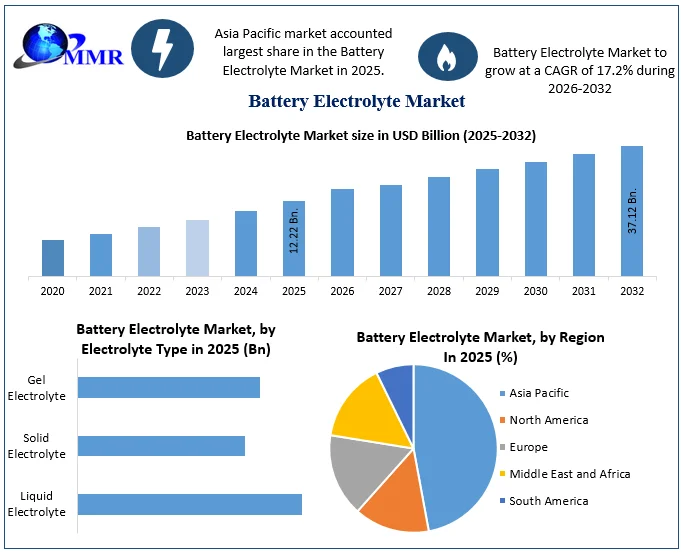

The Battery Electrolyte Market size was valued at USD 12.22 Billion in 2025 and the total Battery Electrolyte revenue is expected to grow at a CAGR of 17.2% from 2026 to 2032, reaching nearly USD 37.12 Billion.

A battery electrolyte is a solution found within batteries. It might be a liquid or a paste-like material, depending on the kind of battery. The electrolyte, however, provides the same function regardless of battery type: it transfers positively charged ions between the cathode and anode terminals. The growing need for Li-ion batteries in the automotive, consumer electronics, and energy storage systems is driving the battery electrolyte market. Li-ion batteries have seen an exponential increase in demand from the automotive sector in recent years, with sales of electric vehicles (EVs) hitting all-time highs. Furthermore, lead acid batteries are likely to see rapid technical developments and expansion in the telecom sector, which will boost the battery electrolyte business even further. As lead acid batteries are deployed in the generating grid, the requirement for energy storage will expand dramatically in tandem with the rising generation. Simultaneously, these batteries are built in substations where the generated electricity is fed onto the main grid. As a result of the increased generation, the deployment of these batteries is expected to expand dramatically. This will increase demand for lead acid battery electrolyte across the world and propel the battery electrolyte industry forward over the forecast period.

To know about the Research Methodology:-Request Free Sample Report

Rising carbon emissions, rising fossil fuel prices, increased construction of EV-charging infrastructure, and numerous national government programmes throughout the world have all aided in the global adoption of electric cars. Furthermore, numerous major automakers, including General Motors, Volvo, Ford, Volkswagen, Audi, and others, have declared plans to phase out internal combustion engine (ICE) vehicles in the next years. The increasing sales of mobile phones, tablets, laptops, Internet-of-Things (IoT) devices, and other consumer electronics have resulted in an increase in demand for battery electrolytes, since Li-ion batteries constitute a key component of consumer electronics worldwide. Because of their high energy density, greater stability and safety, and increased storage capacity, battery electrolytes have received general acceptance for use in energy storage systems. Aside from these key uses, Battery Electrolytes have also found applications in power tools and medical equipment, which are contributing to the growth of the Battery Electrolyte Industry.

Battery Electrolyte Market Dynamics

Growing Sales of Electric Vehicles to Boost Market Growth

Lithium-ion batteries are a key component of electric cars (EVs), since the majority of EVs are powered by lithium-ion (Li-ion) batteries. Depending on the cell chemistry, lithium-ion batteries employ a variety of metals in varying compositions and amounts. The increasing popularity of electric cars has resulted in an increase in demand for Li-ion batteries. With EV sales expanding at an exponential rate, manufacturers are increasing EV manufacturing. BYD, a Chinese EV maker, said in April 2022 that it will cease production of gasoline vehicles and focus only on the production of electric vehicles to fulfil rising demand. China will sell more than 3.3 million new energy vehicles in 2025, including electric vehicles and plug-in hybrid vehicles.

Several countries have announced new plans and strategies to boost the country's expanding EV sales. For example, as part of its Early Adoption Initiative, Singapore launched a new EV incentive scheme in 2025. In January 2022, Singapore's Transport Minister said that the nation provided $30 million in rebates in 2024 to encourage EV adoption. Furthermore, in order to meet the Paris Agreement's ideal objective of a 1.5-degree Celsius temperature increase, electric vehicle sales must account for 75- 95% of all global passenger cars by 2032 and 100% by 2035. EV sales are expected to climb dramatically in the future years, boosting demand for Li-ion batteries and driving the growth of the lithium-ion battery metals market over the forecast period.

Rising Demand for Application in Consumer Electronics

Consumer electronics are a crucial part of daily lives, and it is impossible to fathom life without mobile phones, laptop computers, I-pads, and other devices. Due to the rechargeable nature and high energy density of Li-ion batteries, the consumer electronics sector was an early user and is currently one of the largest end-use industries for Li-ion batteries. Sony was the first manufacturer to commercialise Li-ion batteries for devices in 1991, laying the groundwork for cellphones and portable computers. Smartphone sales are now increasing rapidly all around the world. Smartphone sales have increased exponentially in some developing economies, including India, Indonesia, Vietnam, and South Africa.

Between 2011 and 2024, India's smartphone industry grew tenfold, with shipments jumping from around 14.5 million in 2011 to almost 150 million in 2021. According to IBEF, overall shipments of 5G devices in India might range from 32 million to 40 million. The rising popularity of smartphone and Internet-of-Things (IoT) devices such as Google Home, Amazon Echo Dot, and others has increased the demand for Li-ion batteries and Li-ion battery metals, pushing the growth of the Li-ion battery metals market.

High Investment in the Research and Development (R&D) & Renewable Energy Sources

Several research initiatives are being taken across the world to investigate the feasibility of utilising different metals as the principal metal in Li-ion batteries, such as manganese, copper, and aluminium. Constantly rising lithium, cobalt, and nickel prices, combined with human rights concerns associated with cobalt mining, have prompted an increase in the number of research programmes aimed at developing a cost-effective alternative for the expensive metals without compromising the energy density and capacity of Li-ion batteries. Companies are pursuing research projects to investigate the use of metals, metal alloys, metal oxides, or other metal compounds as the cathode or anode of Li-ion batteries in order to transition away from cobalt and nickel.

Renewable energy is increasing popularity and investment all around the world. Both governments and businesses are attempting to shift away from fossil fuels and toward renewable energy sources in order to cut carbon emissions and fulfil the Paris Agreement objectives, and Li-ion batteries are likely to play a significant part in this. Companies are also investigating the use of Li-ion batteries as key energy storage in off-grid renewable energy. Li-ion batteries outperform other batteries on the market in terms of energy density, specific energy, and power density. Furthermore, the high power discharge capability, improved round-trip efficiency, low self-discharge rate, and substantially longer work-life of Li-ion batteries contribute to their rising appeal as energy storage systems for renewable energy.

Limited Usage Capacity of Lead Acid Batteries

The usable capacity of lead acid batteries is expected to be limited. It is common practise to use just 30-50% of the rated capacity of a standard lead acid battery. This means that in everyday use, a 600 Ah battery bank delivers only 300 Ah of real capacity at most. If the batteries are even slightly overcharged, their life will be dramatically reduced. These batteries have a finite lifespan. Even if one is gentle with these batteries and takes special care not to overdrain them, the finest deep-cycle lead acid batteries are normally good for 500-1,000 cycles.

If the battery bank is often used, it is possible that the batteries will need to be replaced in less than two years. Furthermore, these batteries lose energy and have significant efficiency difficulties. They squander up to 15% of the energy they consume due to intrinsic charging, showing inefficiency. As a result, if 100 A of electricity is supplied, only 85 Ah is stored. This can be aggravating when utilising solar charging and attempting to squeeze as much efficiency out of every amp as possible before sunset or being obscured by clouds.

Rising Prices of Raw Materials to Restraint Market Growth

The costs of battery metals have a significant impact on the prices of Li-ion batteries. Companies are continually working to cut the cost of Li-ion batteries in order to enhance their global acceptance. However, the cost of essential metals used in Li-ion batteries, such as lithium, cobalt, and nickel, are extremely volatile and fluctuate wildly. Key metal costs have risen dramatically in recent years, posing challenges for Li-ion battery makers and consumers. The US Geological Survey (USGS) reported in January 2022 that spot lithium carbonate prices in China jumped by $7,000 per tonne in January 2022 compared to November 2021 pricing. Furthermore, according to the USGS, average spot lithium carbonate prices in 2021 will be $17,000, up more than 100% from prices in 2021.

Because of the rising prices, some firms have begun to investigate the potential of joining the lithium mining sector themselves. For example, Elon Musk stated in April 2022 that due to the recent surge in lithium costs, Tesla may have to enter the lithium mining and refining sector itself. Nickel and cobalt prices have also risen dramatically in recent years, and the effects of Russia-Ukraine war is expected to drive nickel prices even higher in FY2022-FY2023. Metal price increases provide a substantial issue for enterprises involved in the manufacture of Li-ion batteries, as high metal costs impact the entire production cost of the battery. As a result, corporations may seek new and less expensive substitutes for metals such as lithium, cobalt, and nickel, such as sodium, calcium, and zinc.

Battery Electrolyte Market Segment Analysis

Based on a Battery Type, lithium-ion battery segment is estimated to be the fastest growing segment, growing at a CAGR of xx% during the forecast period. The lithium-ion battery segment accounted for the largest segment in 2025 and is expected to dominate the battery electrolyte industry during the forecast period. Lithium-ion batteries have gained popularity over the years due to their high energy and power density in terms of volume, as well as their high charge/discharge efficiency and weight. These batteries are used in a variety of applications, including electric vehicles, consumer electronics, and energy storage systems. As a result of the expansion of these industries and the fast industrialization of developing nations, demand for this segment is expected to increase during the forecast period.

Lead Acid segment is expected to grow at a CAGR of xx% and is estimated to hold a significant revenue share of the battery electrolyte industry during the forecast period. The factors driving the growth for lead acid battery segment is the rapid technological advancements and expansion in the telecom sector. On the contrary, the emergence of low-cost alternatives in the energy storage arena, as well as safety issues associated with battery usage, are expected to limit the segment's growth during the forecast period.

Based on Electrolyte Type, liquid electrolyte segment accounted for the largest segment and is estimated to grow at a CAGR of xx% during the forecast period. A liquid electrolyte is a liquid phase electrolytic solution containing at least one salt dissolved in a liquid non-aqueous polar solvent. The liquid electrolyte is mostly utilised in lead-acid batteries, which are employed in increasing areas such as vehicles and energy storage systems due to their low cost. These are some of the elements that will drive the segment's market.

The solid electrolyte segment is expected to grow at a CAGR of around xx% and hold a significant revenue share of the battery electrolyte market during the forecast period. The battery electrolyte business is likely to be driven by factors such as rising demand for energy storage systems with high energy density and extended cycle life. In the future years, the increased usage of electronic gadgets and electric vehicles is expected to expand the use of solid-state batteries and solid electrolytes. The high cost of a solid-state battery, on the other hand, is estimated to stymie the battery electrolyte sector during the forecast period.

Based on End-Use, Electric Vehicle segment is expected to hold largest market share of xx% and is estimated to grow at a significant CAGR of xx% during the forecast period. Increased demand for electric cars in places such as North America and Asia Pacific is driving the battery electrolyte market. Automobiles such as electric vehicles, e-bikes, and autonomous guided vehicles are key consumers of lithium-ion batteries, driving demand. Energy savings and pollution reduction are just a few of the factors driving consumer acceptance of electric vehicles. According to EV-Volumes, global EV sales will reach 6.75 million units in 2025, up 108% from 2025.

Consumer Electronic segment is expected to hold a significant revenue share of the battery electrolyte industry. Rechargeable lithium-ion batteries are utilised in a variety of consumer electronic products such as mobile phones, tablets, vaping devices, computers, electric toothbrushes, and hoverboards. During the forecast period, the increased demand for consumer electronics items such as smartphones, laptops, tablets, and IoT devices from emerging countries in Southeast Asia, Africa, South America, and the Middle East is likely to contribute to the growth of the battery electrolyte industry.

Global Battery Electrolyte Market Recent Development

| Date | Company | Development | Impact |

|---|---|---|---|

| 05 January 2025 | Mitsubishi Chemical Group Corporation | The company announced a formal expansion of electrolyte production capacity at its Kurosaki plant in Japan and initiated site selection for a new North American manufacturing facility. | The strategic expansion is optimized to supply IRA-compliant battery cell manufacturers and capitalize on regional clean energy incentives. |

| 28 February 2025 | Guangzhou Tinci Materials Technology Co., Ltd. | The manufacturer signed extensive, long-term battery electrolyte supply agreements with major global battery producers CATL and BYD. | The partnerships secure high-volume chemical supply pipelines for high-performance LFP and NMC electric vehicle battery programs. |

| 15 November 2025 | Guangzhou Tinci Materials Technology Co., Ltd. | The corporation expanded its technological portfolio by successfully acquiring eight strategic invention patents regarding sulfide solid electrolytes from the National Intellectual Property Administration. | This acquisition significantly enhances their R&D framework for accelerating the production scalability of all-solid-state lithium batteries. |

| 15 December 2025 | Mitsubishi Chemical Corporation | The company entered a binding agreement to transfer its lithium-ion battery electrolyte manufacturing assets operated by its U.S. and UK subsidiaries to Green E Origin SARL. | The asset transfer optimizes the corporation's asset layout, allowing a narrower focus on specialized business development and material collaborations. |

| 20 December 2025 | Enchem Co., Ltd. | The supplier secured a major long-term contract with CATL to supply 70,000 tons of battery electrolyte annually to facilities in China from 2026 to 2030. | Valued at approximately KRW 1.5 trillion, this historic order drastically elevates the company's forward revenue visibility and global market share. |

| 05 January 2026 | Shenzhen Capchem Technology Co., Ltd. | The manufacturer announced a USD 260 million investment to build a lithium-ion battery electrolyte solvent plant in Saudi Arabia alongside a capital injection to double its Polish factory's capacity. | The capital project targets supply chain localization to satisfy soaring international demand from EV and stationary energy storage sectors. |

Battery Electrolyte Market Regional Insights

The Asia-Pacific region dominated the battery electrolyte industry in 2025 and is estimated to hold the highest revenue share of the battery electrolyte market during the forecast period. The battery electrolyte market is expected to rise significantly in the next years due to the increased usage of batteries in various industries such as autos, solar PV, electronic appliances, and data centres.

China is expected to be the dominant country in the Asia-Pacific region, accounting for the bulk of electronic appliance sales. Furthermore, the country leads the world in solar PV installations (both rooftop and ground-mounted) and automotive sales. The use of lithium-ion batteries is expected to grow during the forecast period due to the increased use of electric cars and battery energy storage systems in solar PV installations. As a result, such a circumstance may fuel the region's battery electrolyte market.

In recent years, India has experienced a substantial increase in the installation of solar and wind power. From 2010 to 2024, the country's wind power generating capacity expanded by more than 2.5 times, while solar power generation capacity increased by more than 400 times. The quality of the country's grid infrastructure remains low, making it difficult for grid providers to integrate renewable energy sources. Despite these issues, the country has relied heavily on other techniques to fulfil peak demand, such as alternate power generating sources (generators, ESS, batteries, and so on).

With the increased use of EVs and favourable government policies in China, the usage of lithium-ion batteries is estimated to rise, positively impacting market growth during the forecast period. The growing prevalence of communications services creates an opportunity for the battery electrolyte industry in China to flourish. Furthermore, Chinese producer Bslbatt Battery revealed an updated version of their home lithium-ion battery in August 2024. The gadget has a storage capacity ranging from 5.12 to 12.8 kWh and can operate continuously for up to 6,000 charge cycles. As a result of the factors mentioned above, Asia-Pacific is expected to dominate and be the fastest-growing region over the forecast period.

North America has an abundance of natural resources and has become one of the world's most developed areas. According to the US Department of Energy, the region has a robust charging infrastructure that is expected to support the region's EV development, which is expected to increase to 224 GWh by 2032 from roughly 59 GWh in 2024. LG Chem and Panasonic Corporation, among others, are prominent makers of lithium-ion batteries in the region. Tesla is a significant manufacturer of electric automobiles and solar panels, with aspirations to sell 20 million electric vehicles annually by 2032 and deploy 1,500 GWh of energy storage utilising Li-ion batteries. The presence of prominent firms at each stage of the Li-ion battery supply chain has aided the expansion of the region's battery electrolyte market, and it is estimated to be one of the primary drivers of the region's battery electrolyte industry in the future years.

Scope of the Report

Product classification, product application, product technology, industry overview, competitive landscape, industrial chain structure, national policy and planning analysis of the industry, development trend, the most recent dynamic analysis are included in the Battery Electrolyte Market report. The report examines the influence of market drivers, trends, opportunities, challenges, and restraints on global demand during the forecast period. The Battery Electrolyte Market competitive landscape includes information about each competitor, such as company overview, market potential, company financials, revenue generated, new market initiatives, investment in R&D, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, and application dominance. The research uses an objective and fair way to conduct an in-depth analysis of the development trend of the industry, providing support and evidence for customer competition analysis, development planning, and investment decision-making.

Battery Electrolyte Market Scope: Inquire before buying

| Global Battery Electrolyte Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 12.22 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 17.2% | Market Size in 2032: | USD 37.12 Bn. |

| Segments Covered: | by Product | Lead-Acid Battery Lithium-Ion Battery |

|

| by Electrolyte Type | Liquid Electrolyte Solid Electrolyte Gel Electrolyte |

||

| by End-User | Electric Vehicle Consumer Electronics Energy Storage Others |

||

Battery Electrolyte Market Key Players

The Battery Electrolyte Market is experiencing significant growth with the increasing demand for electric vehicles (EVs), energy storage systems, renewable energy integration, advancements in battery technologies, cost optimization, and environmental regulations. The competitive landscape features key players such as 3M, NEI Corporation, Guangzhou Tinci Materials Technology Co. Ltd, and Mitsubishi Chemical Holdings Corporation, among others, leveraging advanced technologies, customization, and strategic alliances to maintain a competitive edge. Companies are focused on innovative product development, such as solid-state electrolytes and advanced additives, to meet the demands of next-generation batteries.

1. Capchem

2. Kunlun

3. Smooth Way

4. Shida Shinghwa

5. Yongtai

6. 3M Company

7. Central Glass Co., Ltd.

8. American Elements

9. Lanxess AG

10. Mitsui & Co., Ltd.

11. UBE Corporation

12. Dongwha Electrolyte

13. Xiamen Tob New Energy Technology Co., Ltd.

14. Umicore

15. Mitsubishi Chemical Corporation

16. Sumitomo Chemical Co., Ltd.

17. Tomiyama Pure Chemical Industries Ltd.

18. Targray Industries Inc.

19. Hitachi Chemical

20. Gelest Inc

21. Daikin America Inc.

22. Amara Raja Batteries

23. Exide Industries

24. SunGarner

25. Guangzhou Tinci Materials Technology Co., Ltd

26. Others

Frequently Asked Questions:

1] What segments are covered in the Global Battery Electrolyte Market report?

Ans. The segments covered in the Battery Electrolyte Market report are based on Battery Type, Electrolyte Type, End-User.

2] Which region is expected to hold the highest share in the Global Battery Electrolyte Market?

Ans. The Asia Pacific region is expected to hold the highest share in the Battery Electrolyte Market.

3] What is the market size of the Global Battery Electrolyte Market by 2032?

Ans. The market size of the Battery Electrolyte Market by 2032 is expected to reach USD 37.12 Bn.

4] What is the forecast period for the Global Battery Electrolyte Market?

Ans. The forecast period for the Battery Electrolyte Market is 2026-2032.

5] What was the Global Battery Electrolyte Market size in 2025?

Ans: The Global Battery Electrolyte Market size was USD 12.22 Billion in 2025.