Automotive Steel Market Size by Vehicle Type, Application, Product and Region - Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

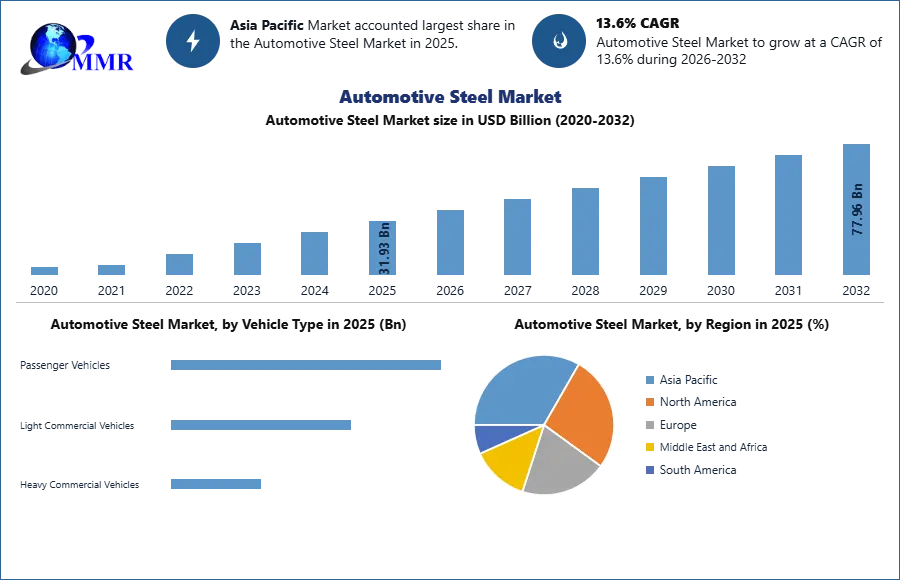

The Automotive Steel Market size was valued at USD 31.93 Billion in 2025 and the total Automotive Steel revenue is expected to grow at a CAGR of 13.6% from 2026 to 2032, reaching nearly USD 77.96 Billion.

Automotive Steel Market Overview:

The influence of steel utilization in the automobile industry has not lessened. It is a useful, economical, and long-lasting alternative since it can be machined and produced in numerous shapes using different methods. Stainless steel, high-strength steel, high-carbon steel, low-carbon steel, or galvanized steel are just a few of the steel kinds that are utilized in the automobile sector. These steel varieties are used to make a variety of engine and vehicle parts. Examples include wheel rims, exhaust pipes, bushings, bearings, exhaust systems, radiators, automobile frames, and many more. Steel has established itself as one of the most dependable materials available throughout the history of the industry.

The industry is working toward the goal of using lighter materials more frequently. The efforts related to the creation of innovative materials, forming technologies, and manufacturing processes are receiving importance. The most economical way to cut fuel use and greenhouse gas emissions is still to reduce weight. According to statistics, fuel efficiency increases by 7% for every 10% of the weight that is removed from a vehicle's overall weight. This implies that there is an about 20 kg decrease in carbon dioxide for every kilogram of weight loss in a vehicle.

The existence of multiple well-established industry players, many of which are expected to account for a significant portion of the overall market in the forecast period, makes the global automotive steel market extremely competitive. Leading automotive steel market companies may choose to focus their future growth strategies on R&D operations that result in goods of higher quality. The report covers the country-wise automotive steel market strategies by key players and their future investments.

The global Automotive Steel Market is currently grappling with a severe supply-side shock as the 2026 Middle East crisis destabilizes traditional manufacturing cost structures. The suspension of regional pricing assessments and the disruption of the Strait of Hormuz have sent crude oil prices soaring to $115–$120/bbl, directly inflating the cost of energy-intensive Electric Arc Furnace (EAF) operations. Steelmakers are facing a dual crisis: a 30% spike in overheads driven by industrial fuel shortages—specifically LNG and LPG—and 400% maritime freight surcharges that have rendered long-haul feedstock procurement economically unviable.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Automotive Steel Market Dynamic

Increases in raw material prices have a serious impact on automotive suppliers and OMEs

In India, raw material prices are becoming more rigid with the full impact of cumulative rises expected in the third and fourth quarters of this fiscal year. The primary materials used in the car industry are steel, aluminum, copper, and rubber. In the past six months, steel has increased by 30%, aluminum by 40%, and copper by 77%. However, during August and October , the cost of main raw materials increased by 9% year over year, with the price of steel and iron increasing the highest.

Over the past six months, flat steel prices have increased by 30%, driven mostly by an increase in global prices of over 25% between May and September. In the previous six months, steel prices increased by Rs 12,000 per MT, and annual steel contracts with car companies have already been amended upward. "Steel prices (hot-rolled coils) rose from Rs 36,000/MT in June to Rs 48,000/MT as of this writing in the past six to eight months.

The major steel firms have increased their H2 sales contracts with automakers by 10% to 15%. Since mid-, raw material costs have increased significantly. The cost of raw materials for an ordinary U.S. car has risen gradually over the last year, growing by 87% from a low point of nearly $2,200 per unit on April 20 to a current price of about $4,125 per unit on May 21. Average transaction prices appear to have stabilized during this raw material cost rise while remaining elevated at record-high levels.

TOKYO According to Nikkei, Toyota Motor will increase the price of steel materials it provides to its suppliers in the second half of the fiscal year by around 20,000 yen ($182) per ton, which will be the company's greatest price increase in more than ten years. Global fluctuation price of row material highly hampers the automotive steel market suppliers and OMEs. More details are covered in the report.

Challenges faced by steel OMEs in Automotive Steel Market

Analyzing the environmental effects of steel production is important. The quantity of GHGs (particularly CO2) generated by the industrial sectors has been capped by environmental safety standards implemented by a number of countries. This puts pressure on automotive steel producers to develop innovative procedures or methods that will allow them to create high-quality steel while lowering CO2 emissions and consuming less energy.

A research and development initiative called Ultra-Low CO2 Steelmaking (ULCOS), which is being carried out by a collaboration made up of 48 European enterprises and 15 European institutions, is looking for ways to create steel with CO2 emissions that are at least 50% lower and trying to solve the challenge in front of OMEs

Large volumes of solid waste are created while processing resources through numerous processes in the Automotive steel-making industry. However, what steel producers frequently forget is that these solid wastes really include a number of valuable products that, if economically recovered, may be utilized. The steel industry's players need to come up with strategies for maximizing the usage of solid waste while minimizing resource waste.

Electric Vehicles (EVs) a next opportunity for Automotive Steel Manufactureres

The automotive steel market is generally positive about its future role in the electric grid. According to a recent analysis by Tata Steels, rising demand for ultra-low emission vehicles (ULEV) would increase steel supply to the automotive sector by 4.2 million tonnes in Europe alone.

In recent years, the necessity for lighter and/or stronger goods has encouraged innovation, as well as profitability, in the automotive materials sector, allowing carmakers to reduce the mass of their ICE cars, cutting fuel consumption and carbon dioxide emissions. Lightweight materials were also important in early EVs, such as BMW's i3 and Tesla's Model S (carbon fiber-reinforced plastic (CFRP) and aluminum, respectively).

The automotive steel market will also see a significant increase in the powertrains used in ULEVs, including electric motors and battery cells. These components, which are expected to contribute to a 1.6 million tonne rise in European steel demand by 2050, will consume higher amounts of electrical and plated steel, respectively. Electrical steel is a critical component in electric motor construction, and the grades of electrical steel utilized can affect the performance of these machines. Tata thinks that as carmakers seek to differentiate their powertrains from those of their competitors, this will become increasingly significant.

According to the company, higher-performing electrical steels can enhance motor efficiency, which will assist in either extending the range or raising the dynamic performance of the automobile. Although steel offers an outstanding property profile, materials competition will still be difficult. As a result, steel producers must always look for new and better solutions. At ThyssenKrupp, for example, they are focusing on the possibilities for cold forming provided by new ultrahigh-strength dual-phase steels in the 1200 class to help bridge the gap between hot and cold forming. Additionally, they have created a technique that, specifically for ultra-high-strength steels, prevents spring-back in the pressing plant, uses less material and increases process reliability these are expected to boost the automotive steel market growth during the forecast period.

Automotive Steel Market Segment Analysis:

Based on Vehicle Type, the Automotive Steel Market is segmented into Passenger Vehicles, Light Commercial Vehicles, and Heavy Commercial Vehicles. a rise in the number of passenger automobiles sold is expected that the Asia Pacific area would help the business flourish. According to OICA figures, India, Thailand, Indonesia, and Malaysia saw overall increases in car manufacturing of 2.6%, 7.2%, 7.5%, and 13.7%, respectively, in. Passenger vehicles dominate the market during the forecast period. The typical passenger vehicle utilizes 15 to 22 kilograms of stainless steel. Stainless is mostly prevalent in exhaust systems but is also present in several minor pieces. Since stainless steel has been utilized in commuter and long-distance trains. High-speed trains in the US or Sweden's X2000 are stunning nowadays.

Stainless steel is used in rail transportation. Additionally, the stainless steel used to coat some tram fleets and bus bodies is becoming more common. Transport applications are expected to grow in importance as major, new automobile applications come online. The ability to use galvanized steel for the automobile body is a skill that all Indian automakers have mastered. They possess the know-how and tools necessary to switch their whole output from uncoated steel to galvanized steel at their stamping facilities, auto assembly lines, and painting facilities.

Based on the Application, the Automotive Steel Market is segmented into Body Structure, Power Train, Suspension, and Others. Body structure held the largest market share in 2025. The primary factors in material selection, particularly for the body, encompass a wide range of qualities including durability, production effectiveness, and thermal, chemical, or mechanical resistance. Steel is the material of choice for producers since it has all the necessary qualities.

Steel is now stronger, lighter, and more rigid than it was in the past thanks to advancements achieved in the steel industry. Steel is used for various automotive components, including the engine, chassis, wheels, and car bodywork. Iron and steel are low-cost materials that generate the essential structural elements for the mass production of cars.

To provide car parts more strength, automotive structural steel is employed. Steel may be made extremely strong by combining alloy components and cooling at low temperatures. Automobile structural steel also offers outstanding cold-formingcapabilities.

As a result, it is utilized to create booms, truck arms, and trailer frames. Due to its excellent surface finishing and admirable corrosion resistance, stainless steel is primarily utilized to construct automobile exhaust systems. Stainless steel is a high-value steel product that doesn't require any special processing and may be utilized in a variety of applications. Around 34% of automotive structural steel is used for body structures, panels, doors, and trunk closures; 23% is used for drive train components, engine components, and gears; 12% is used for suspension units; and the remaining percentage is used for tires, wheels, steering, breaking systems, and fuel tanks.

Automotive Steel Market Regional Insights:

The Asia Pacific region dominated the market with a 65 % share in 2025. Steel consumption in Asia and Oceania increased by 3.5% to 1,303 mmt in , according to worldsteel. This was thanks to China's robust recovery, where consumption increased by 9.1%. (worldsteel, ). China's construction sector recovered significantly beginning in April , boosted by infrastructure spending. Furthermore, according to the National Bureau of Statistics, real estate investment will expand by 7% to around USD 2.2 trillion in . According to the China Association of Automobile Manufacturers, car sales in the manufacturing sector declined 1.9% to 25.3 million units.

Although passenger car sales dropped by 6%, commercial vehicle sales increased by 19% as a result of government infrastructure expenditure and as customers modified their vehicles to meet with stricter emissions rules. Other manufacturing industries grew as a result of strong export demand. Steel consumption in India fell by 13.7% to 88.5 mmt in , from about 100 mmt. This was due to a longer duration of strict lockdown, which halted most industrial and building activity.

The Society of Indian Automobile Manufacturers reports that domestic passenger car sales between April and March decreased 2.2% from the same period the previous year . Steel usage in Japan fell by 16.8% to 52.6 mmt in . Steel consumption from the automobile sector fell considerably in Q2 , whereas steel demand from industrial machinery fell in the same quarter Steel consumption in Korea fell 8.0% to 49.0 mmt in .

According to worldsteel's April SRO, steel consumption in the ASEAN-5 area (Indonesia, Malaysia, the Philippines, Thailand, and Vietnam) fell by 11.9% to 68.7 mmt in . According to the South East Asia Iron and Steel Institute, apparent steel consumption in the Association of Southeast Asian Nations (ASEAN-6, which includes Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Vietnam) would fall by 12% year on year to 70.6 mmt in . Malaysia (-38%) and the Philippines (-15.5%) were the hardest afflicted countries. In comparison, Vietnam (-4%) and Indonesia (-5.3%) had very minor losses in steel production.

Stratergic collaboration by key players

ArcelorMittal, TATA Steel, China Steel, Hyundai Steel, United States Steel Corporation, JSW Group, POSCO, Nippon Steel & Sumitomo Metal Corporation, JFE Steel Corporation, NUCOR Corporation, Jindal Steel & Power, Grow Ever Steel, HBIS Group, Outokumpu OYJ, and Kobe Steel are some of the major players in the market.

The strategic landscape will be shaped by various acquisition options and constant research and development to increase product reliability. In addition, corporations will benefit from growing efforts to reduce the automotive industry's carbon impact. As an illustration, in July , Tata Steel and BHP, a significant global resource company, inked an MoU to work together to research low carbon iron and steelmaking technologies. The businesses agreed to cooperate in order to discover strategies for reducing emissions produced by the blast furnace steel route as part of the agreement.

Competitive Landscape

The global automotive steel market is highly competitive, with the presence of several well-established market players, many of whom are expected to account for a large share of the overall market, in the coming years. Research and development activities to produce an improved quality of products could be a key growth strategy for leading automotive steel market players, in the future.

Collaboration with smaller players could help prominent automotive steel market players expand their presence and increase their revenue shares. Smaller competitors in the automotive steel sector will seek funding from private investors, which might aid in their long-term growth. For example china account China now has 1.2 billion tons of steel manufacturing capacity per year, with annual consumption averaging around 1 billion tons.

According to the China Iron and Steel Association, around 95% of China's steel output is used domestically (CISA). China Baowu Steel Group 120 million tonnes of automotive steel manufactures in the year 2022 key automotive steel manufacturer in the world. Ansteel Group (55.65 million tonnes ), Jiangsu Shagang (44.23 million tonnes), Hesteel Group (41.64 million tonnes), and Jianlong Steel (36.71 million tonnes) are some of the key companies in china.

India will be the second-largest manufacturer, with output increasing by 17.8 percent to 118.1 million tons. In December, India's crude steel output increased by 0.9% to 10.4 million tons. The country's total steel manufacturing capacity is at 143.91 million tonnes. Details on steel production plants in both the public and private sectors. Tata Steel (30.6 million tonnes), JSW Steel (18.6 million tonnes), Steel Authority of India Limited (17.3 million tones), Essar Steel (10 million tonnes), Mahindra Ugine Steel (30,000 metric tons). Japan was the third-largest producer, with output climbing nearly 15% to 96.3 mt . In December, its output grew by 5.4% to 7.9 million tons.

Recent Industry Developments

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 26 March 2026 | ArcelorMittal | The company announced a major leadership transition with Amit Harlalka appointed as the new CEO to lead future green steel initiatives. | This strategic shift is expected to accelerate decarbonization efforts across their global automotive steel supply chains. |

| 23 March 2026 | AM/NS India | A foundation stone was laid for a massive greenfield steel plant in Andhra Pradesh to boost regional production capacity. | The expansion strengthens the domestic supply of high-grade steel for the rapidly growing Indian automotive manufacturing sector. |

| 16 February 2026 | AM/NS India | The joint venture expanded its value-added steel portfolio by launching the Vibrance and Optima brands for industrial use. | This development diversifies competitive offerings for automotive OEMs requiring specialized, high-performance coated steel. |

| 05 February 2026 | AM/NS India | The company became the first integrated producer to receive Green Steel certification under the Ministry of Steel's new taxonomy. | It establishes a new industry benchmark for sustainable manufacturing, appealing to environmentally conscious vehicle manufacturers. |

| 17 December 2025 | AM/NS India | The company secured a top innovation award at NECA 2025 for its advancements in energy leadership and decarbonization. | Recognition of these R&D milestones enhances brand equity as a preferred partner for future "zero-emission" vehicle projects. |

| 16 July 2025 | AM/NS India | A state-of-the-art Continuous Galvanising Line (CGL) was commissioned to produce the highest strength automotive steel. | The facility reduces import dependency for advanced high-strength steel (AHSS) used in modern vehicle body structures. |

Automotive Steel Market Scope: Inquire before buying

| Automotive Steel Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 31.93 USD Billion |

| Forecast Period 2026-2032 CAGR: | 13.6% | Market Size in 2032: | 77.96 USD Billion |

| Segments Covered: | by Vehicle Type | Passenger Vehicles Light Commercial Vehicles Heavy Commercial Vehicles |

|

| by Application | Body Structure Powertrain Suspension Others |

||

| by Product | Transformation Induced Plasticity (TRIP) Steel Dual Phase Steel Complex Phase (CP) Steel Others |

||

Automotive Steel Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Key Players / Competitors Profiles Covered in Brief in Global Automotive Steel Market Report in Strategic Perspective:

- JSW Steel

- Steel Authority of India Limited

- Tata Steel

- Nippon Steel Corporation

- JFE Holdings, Inc.

- POSCO

- Hyundai Steel Co., Ltd

- China Baowu Steel Group Corp., Ltd.

- ArcelorMittal

- United States Steel Corporation

- Nucor Corporation

- China Steel Corporation

- Jindal Steel & Power

- HBIS Group

- Outokumpu OYJ

- Kobe Steel

- SSAB

- ThyssenKrupp AG

- Shougang Group

- Angang Steel Company Limited

- Voestalpine AG

- Tenaris

- Gerdau S.A.

- BlueScope Steel Limited

Frequently Asked Questions

1.What is the projected valuation and growth rate for the Automotive Steel Market through 2032?

Ans. The market reached USD 31.93 Billion in 2025. It is expanding at a 13.6% CAGR, reaching a forecasted USD 77.96 Billion valuation by year-end 2032.

2. Which region currently leads the Automotive Steel Market share analysis and why?

Ans. Asia Pacific dominates with a 65% share, driven by massive production in China and India, infrastructure investments, and a rapid shift toward localized automotive manufacturing.

3. How is the shift toward Electric Vehicles influencing Automotive Steel Market trends 2026?

Ans. EV growth drives demand for high-performance electrical steel for motors and advanced high-strength steel for battery enclosures, ensuring vehicle safety while extending driving range.

4. What are the primary industry growth drivers for lightweight materials in vehicle manufacturing?

Ans. Weight reduction remains the most economical strategy to boost fuel efficiency and meet strict global emission standards, prompting innovations in ultra-high-strength dual-phase steel grades.

5. How are rising raw material costs impacting the global Automotive Steel Market supply chain?

Ans. Surging prices for iron and energy force OMEs to renegotiate contracts, leading to increased vehicle transaction prices and a strategic focus on high-margin specialized steel.

6. What decarbonization strategies are leading players adopting for sustainable green steel production?

Ans. Top manufacturers are investing in ULCOS technologies and hydrogen-based steelmaking to reduce carbon footprints, securing Green Steel certifications to meet evolving environmental safety standards.

7. Which application segment is expected to maintain the highest Automotive Steel Market revenue?

Ans. Body structure remains the leading segment, utilizing advanced high-strength steel to balance crash safety and structural integrity while optimizing overall vehicle weight for better performance.