Animal Parasiticide Market Size by Type, Animal Type, End-Users, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2034

Overview

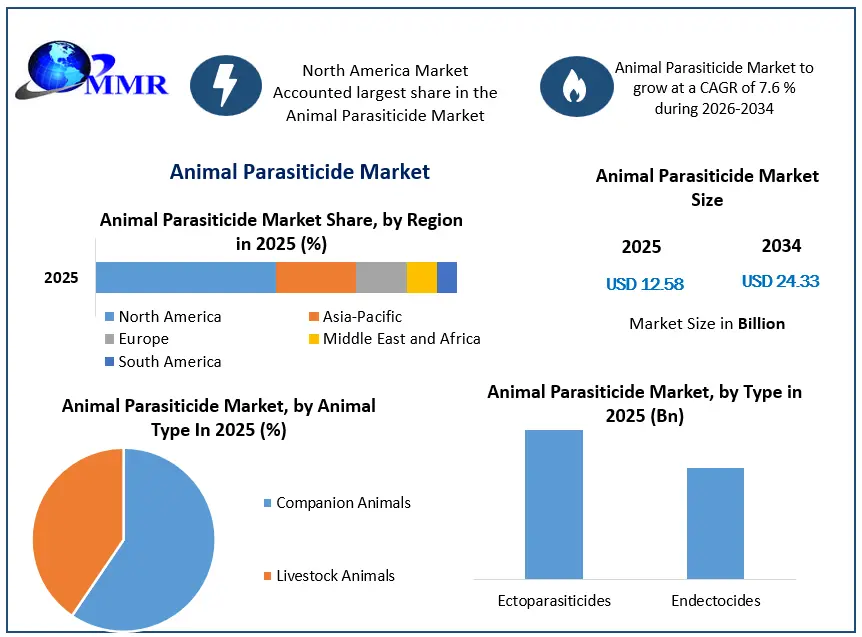

The Animal Parasiticide Market size was valued at USD 12.58 Billion in 2025 and the total Animal Parasiticide revenue is expected to grow at a CAGR of 7.6% from 2026 to 2034, reaching nearly USD 24.33 Billion.

Animal Parasiticide Market is segmented by product, type, end-users and application. Based on type, the market is segmented into ectoparasiticides, endoparasiticides, and endectocides. Based on animal type, the market is segmented into companion animals, and livestock animals. Based on end-users, the market is segmented into veterinary clinics & hospitals, animal farms, and home care settings. Based on region, the market is segmented into North America, Asia Pacific, Europe, Middle East & Africa, and South America.

The market for animal parasiticides is expanding as a result of factors like the rising demand for food products made from animals, growing private player investments, rising zoonotic disease concerns, laws aimed at preventing the spread of animal diseases, rising rates of companion animal ownership, and rising costs for animal health care. However, during the forecast period, this market's development is anticipated to be constrained by a trend toward vegetarianism and limitations on the use of parasiticides on animals used for food production.

Animal Parasiticide Market Analysis from 2025 to 2034

To know about the Research Methodology :- Request Free Sample Report

Animal Parasiticide Market Dynamics

The market for animal health has developed somewhat over the past few years, mostly due to increased knowledge of and anxiety over zoonotic illnesses. Leading market companies have made considerable expenditures in this sector, mostly as a result of the rising need for potent medications in the animal parasiticides market.

One of the main factors driving increased R&D efforts in the animal health sector is this. Many top market firms currently concentrate on R&D to create new medicines. Around 7-8 percent of each market participant's overall income is spent globally on R&D in animal healthcare.

Many top firms in the animal health sector are currently expanding their research capabilities to provide cutting-edge veterinary pharmaceutical treatments, such as antiparasitics for animal welfare. By creating R&D centres and manufacturing facilities, buying regional market participants, and entering into agreements and partnerships in these fast-growing areas, major market players are concentrating on increasing their global footprints.

For instance, Elanco paid USD 7.6 billion in August 2019 to buy Bayer's Animal Health Business. By achieving balance between its food animal and companion animal divisions, this purchase increased Elanco's companion animal business by double and improved its portfolio mix.

The cattle industry is a huge and highly dynamic global asset 330.5 million metric tonnes of beef were produced globally in 2018, up from 317.2 million metric tonnes in 2016. Globally, livestock products account for 17% of calories consumed and 33% of protein consumed; however, this differs across industrialised and developing nations.

Over the past 50 years, the world's output of beef has more than doubled while consumption has increased. 800 million tonnes of milk and more than 320 million tonnes of beef are currently produced annually throughout the globe.

The increase in demand for animal products in emerging nations is mostly to blame for this. Despite a steady and regular growth in high-income nations, emerging and developing markets' growing populations have helped similar and substantial growth.

Africa's demand for meals generated from cattle is expected to rise by an astounding 80% in only two decades (from 2010 to 2030), mostly because of the continent's growing population. Additionally, sub-Saharan Africa and South Asia's demand for cattle food products is expected to rise from 200 kcal per person per day in 2000 to around 400 kcal per person per day by 2050.

It is important to avoid the development of endoparasite infections among animals that produce food since these infections can be lethal to animals and reduce the amount of meat and milk they produce. The market for parasiticides is expected to expand in the upcoming years as a result of this as well as the rising need for animal protein on a global scale.

Numerous federal laws govern the use of parasiticides on livestock animals global. These topical parasiticides may have negative effects if used outside of the recommended dosage when applied to the skin. As a result, it is necessary to control the use of these parasiticides, particularly endoparasiticides, standardise the safe residual concentrations and withdrawal times for antiparasitics used in food-producing animals, and check slaughtered animals for any potential dangerous residues.

In order to avoid the existence of dangerous drug residues, the FDA in the US has established exact withdrawal periods for parasiticides administered to animals used for food production (the amount of time required after drug administration for drug residues to reach limits defined by the FDA). Parasiticides are also prohibited for all organic slaughter animals, according to the National Organic Program.

In order to make sure that authorised medications, including parasiticides, are not present in food above the permitted level (also referred to as the maximum residue limit), the Veterinary Medicines Directorate's non-statutory programme in the UK conducts residue analyses on imported and processed animal foods in collaboration with the National Surveillance Scheme. The Canadian Food Inspection Agency in Canada establishes standards for animal medicine withdrawal periods, including those for parasiticides.

Companion animal ownership has steadily increased over the past few years particularly in developing nations like Brazil, India, China, and other Asia Pacific and South American nations. The prevalence of pet ownership in these nations is being driven by rapid urbanisation and rising disposable incomes. In these nations, many pet owners are now prepared to pay more on their animals' care.

On the other hand, growing nations with large cattle markets include China and India. Approximately 187.7 million tonnes of milk will be produced in India in 2019, up from 165.4 million tonnes in 2017 and 146.3 million tonnes in 2015. This rise is reported by the National Dairy Development Board. In addition, India produces the most milk in the world, capturing 19% of the market.

Given that poultry animals are more susceptible to parasite infections, the huge populations of poultry and dairy animals in emerging economies are expected to propel the expansion of the veterinary health industry. Additionally, this will encourage international investors to enter these areas.

The use of animal parasiticides in veterinary offices, livestock farms, and households with pets has historically been less common in these nations than in industrialised markets. The cattle industry in South America has expanded annually at a pace (3.7 percent) faster than the average global growth rate, according to the Food and Agriculture Organization (2.1%). From 165.1 million in 2018 to 181.3 million in , the region's pet population has grown.

Obesity and other chronic diseases are becoming more commonplace on a global scale. As a result, a large number of individuals are switching from a mostly non-vegetarian diet to a vegetarian one. Google Trends reports that between and , interest in veganism surged seven-fold. Dietary recommendations are promptly released by the US Department of Agriculture.

These suggestions for food selection, weight control, and physical exercise have an impact on nutrition education, public policy, and food programmes. These recommendations also promote the intake of whole grains, low-fat dairy products, fruits, and vegetables.

Plant-based food product sales in the US reached over 4.5 billion USD in 2019, an increase of 31.3% from the previous year. According to figures from The Vegan Society, there were 600,000 vegans in the UK as of 2018 (1.16 percent of the population), a 300 percent increase from 2014. (150,000, or 0.25 percent of the population). The transition to vegetarian diets is also being fueled by evolving eating patterns and greater exposure to other cuisines.

This change has decreased consumer demand for meat, animal proteins, and eggs, which has a negative impact on the expansion of the livestock sector. Additionally, the consumption of meat has decreased as a result of the rise in bird flu cases and diseases brought on by meat eating, such as swine flu and COVID-19.

When determining the origin of an animal's disease, the diversity of parasite species is a significant concern. The process of creating a novel medicine to address conditions brought on by a certain species is time-consuming and follows the identification of the species. An endoparasiticide that is not intended for the identified causal endoparasite may occasionally be given to an animal.

In such circumstances, the endoparasiticide-resistant causative agent may evolve. Because of this, parasiticide producers are required to do several animal experiments to demonstrate the effectiveness of the medication created. This is a time-consuming and expensive procedure that can result in the rejection of novel medications created as parasiticides.

The market is challenged by the enormous variety of parasite species since it is challenging for producers to develop a parasiticide to combat various parasites. The fact that each parasiticide takes 5–10 years to develop further exacerbates this.

Authorities have established strict standards to guarantee that animal parasiticides are of adequate quality and efficacy, have no adverse effects on animal health, and are approved. Major regulatory agencies that approve medications used for veterinary purposes include the US FDA, Canadian Food Agency, European Medical Agency, Ministry of Agriculture, Forestry, and Fisheries (MAFF), and Australian Pesticides and Veterinary Medicines Authority (APVMA).

The US, European, and Japanese regulatory agencies are brought together by the Veterinary International Committee for Harmonization (VICH), which also harmonises the rules and technical specifications for registering veterinary goods. For the approval of veterinary pharmaceutical goods, several regulatory organisations have established strict guidelines.

Australia, Japan, and China all have highly strict regulatory requirements for the clearance of new veterinary pharmaceutical products, including antimicrobials, antibiotics, vaccinations, parasiticides, and other pharmaceutical goods.

It might take up to 11 years on average for veterinary medications to be approved for sale in the US and Europe (from product development to commercialization). Many market participants are hesitant to invest in creating new variations of veterinary medications for emerging bacteria and parasites because of how time-consuming and expensive the development and approval procedure of new veterinary pharmaceutical products is.

Animal Parasiticide Market Segment Analysis

Based on type, the animal parasiticides market is segmented into endoparasiticides, ectoparasiticides, and endectocides. The market for animal parasiticides globally in was dominated by the ectoparasiticides sector, which had a 57.9% market share.

At an estimated CAGR of 8.5%, this market is expected to grow from USD 5,703.9 million in USD 8,582.1 million in . The high adoption of ectoparasiticides relative to other products is responsible for the huge proportion of this market. The rise in pet ownership and the number of companion animals in developed nations are additional factors that are expected to promote market expansion during the forecast period.

Based on animal type, the animal parasiticides market is segmented into companion animals and livestock animals. In , companion animals made up the biggest segment of the market for animal parasiticides, with a share of 52.2%. At an estimated CAGR of 8.3%, this market is expected to grow from USD 5,130.2 million in to USD 7,633.2 million in . The significant market share of this sector is largely due to the rising costs of keeping pets and the rise in the number of people who own companion animals in industrialised nations.

Based on end users, the animal parasiticides market is segmented into veterinary clinics & hospitals, animal farms, and home care settings. Veterinary clinics & hospitals accounted for the largest share of 61.4% of the animal parasiticides market in . At a CAGR of 6.8%, it is expected that this market would grow from USD 5,952.6 million in to USD 8,252.7 million in . The increased use of animal parasiticides in medical settings, the rise in parasitic illnesses, and the rising concern over animal health in developing nations are all factors that contribute to the big proportion of this market.

Animal Parasiticide Market Regional Insights

North America held the greatest market share (40.3%) for animal parasiticides globally in . At an estimated CAGR of 5.9%, this market is expected to grow from USD 3,879.4 million in to USD 6136.6 million by . North America has a significant portion of the market because of its strong foundation in the animal health sector, the increasing adoption of companion animals, and the rising costs associated with animal health.

By , the market for animal parasiticides in the United States is expected to be worth USD 1.7 billion due to the rise in pet adoption and rising demand for animal byproducts. The usage of animal parasiticides will increase due to the high incidence of bug infestation in animals and owners' increased concern for the health of their pets. Additionally, the country's key market players' presence there and rising spending on the creation of new veterinary goods would help the veterinary healthcare market expand over the forecast period.

India's share of the Asia Pacific Animal Parasiticide Market was over USD 280 million in , and it is expected to expand significantly over the coming years. The market will expand because to the rising number of farm animals and demand for high-quality meat and animal byproducts. The adoption of companion animals is expanding, people are becoming more aware of animal healthcare goods, and key market players are investing more money in an effort to have a firm footing in the lucrative industry, all of which will spur business growth in the near future.

Due to high awareness of animal healthcare and high healthcare spending for animal welfare, the Europe market currently leads the world in terms of revenue produced in the animal parasiticides market and is expected to grow at a CAGR of 6.2 % during the forecast period.

Among the few nations that lead the market for animal parasiticides in Europe in terms of income are Germany, France, and the United Kingdom. During the forecast period, the market in South America is estimated to grow at the highest CAGR of 8.8%. This can be ascribed to the rising adoption of pets as well as the expanding populations of livestock animals and consumers of food items generated from animals.

The objective of the report is to present a comprehensive analysis of the global Animal Parasiticide Market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The reports also help in understanding the Animal Parasiticide Market dynamic, structure by analyzing the market segments and projecting the Animal Parasiticide Market size. Clear representation of competitive analysis of key players by Vehicle type, price, financial position, product portfolio, growth strategies, and regional presence in the Animal Parasiticide Market make the report investor’s guide.

Animal Parasiticide Market Recent Development

| Date | Company | Development | Impact |

|---|---|---|---|

| 01 November 2025 | Merck & Co., Inc. | Received regulatory approval for Bravecto Quantum, a long-acting injectable providing up to 12 months of parasite protection in dogs. | Significantly improves treatment compliance and reduces dosing frequency for pet owners. |

| 01 November 2025 | Zoetis Inc. | Secured additional international approvals and label expansions for its broad-spectrum parasiticide, Simparica Trio. | Expands the product's geographic footprint and market reach for comprehensive internal and external parasite control. |

| 15 September 2025 | Elanco Animal Health | Reported that Credelio Quattro™ reached over $100 million in net sales within eight months of its initial rollout. | Establishes the drug as the company's fastest-growing pet health product, validating demand for combination therapies. |

| 01 August 2025 | Merck & Co., Inc. | Presented the Bravecto fluralaner portfolio at the 2025 World Association for the Advancement of Veterinary Parasitology (WAAVP) Congress. | Reinforces the company's technical leadership and commitment to advancing parasite prevention standards globally. |

| 01 April 2025 | Zoetis Inc. | Announced FDA approval of a new label indication for Simparica Trio to prevent flea tapeworm infections. | Positions the product as the only canine combination treatment capable of killing vector fleas before parasite transmission occurs. |

| 01 March 2025 | NOAH (National Office of Animal Health) | Launched the “Use It Right, Treat Them Right” national campaign to promote responsible usage of anti-parasitic medicines. | Aims to mitigate the growing threat of parasitic resistance through improved veterinary and pet owner education. |

Animal Parasiticide Market Scope: Inquire before buying

| Global Animal Parasiticide Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 12.58 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 7.6% | Market Size in 2034: | USD 24.33 Bn. |

| Segments Covered: | by Type | Ectoparasiticides Endectocides |

|

| by Animal Type | Companion Animals Livestock Animals |

||

| by End-Users | Veterinary Clinics & Hospitals Animal Farms Home Care Settings |

||

Animal Parasiticide Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Key Players

1.Zoetis Inc.

2.Virbac

3.PetIQ, Inc.

4.Norbrook

5.Vetoquinol S.A.

6.Merck & Co., Inc.

7.Ceva Santé Animale

8.Bimeda Animal Health

9.Boehringer Ingelheim GmbH

10.Elanco Animal Health Incorporated

11.Sanofi S.A. (Merial)

12.Virbac SA

13.Eli Lilly and Company

14.Bayer AG

15.Perrigo Co. plc

Frequently Asked Questions:

1. Which region has the largest share in Global Animal Parasiticide Market?

Ans: North America region held the highest share in 2025.

2. What is the growth rate of Global Animal Parasiticide Market?

Ans: The Global Animal Parasiticide Market is growing at a CAGR of 7.6% during forecasting period 2026-2034.

3. What is scope of the Global Animal Parasiticide Market report?

Ans: Global Animal Parasiticide Market report helps with the PESTEL, PORTER, COVID-19 Impact analysis, Recommendations for Investors & Leaders, and market estimation of the forecast period.

4. What was the Global Animal Parasiticide Market size in 2025?

Ans: The Global Animal Parasiticide Market size was USD 12.58 Billion in 2025.