Aerospace Coating Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2034

Overview

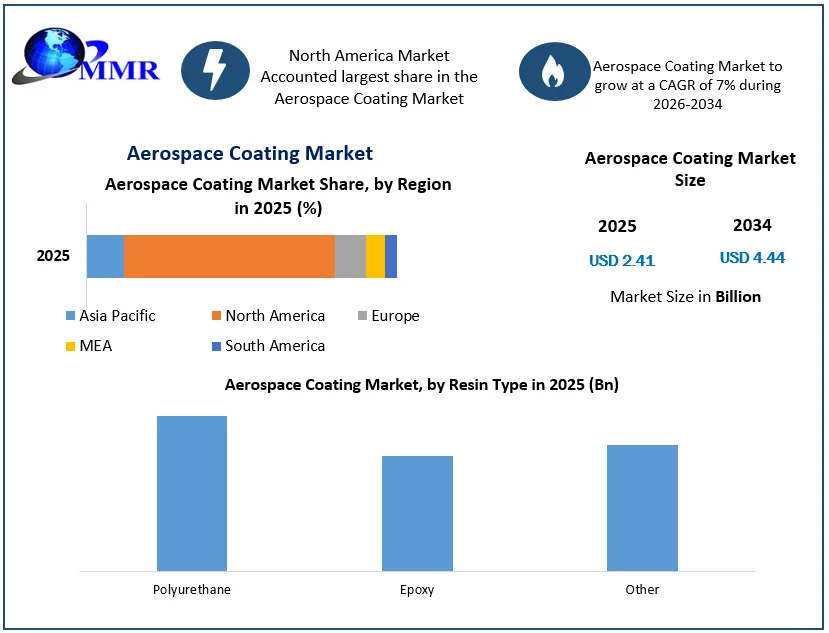

The Aerospace Coating Market size was valued at USD 2.41 Billion in 2025 and the total Aerospace Coating revenue is expected to grow at a CAGR of 7% from 2026 to 2034, reaching nearly USD 4.44 Billion.

Aerospace Coating Industry :

A coating is a covering that is put on top of an object, which is also known as a substrate. The coating may be used for practical, ornamental, or a combination of both purposes. The market for aerospace coatings is primarily driven by rising demand from a variety of end users, including general aviation, commercial aviation, and military aircraft. Nanotechnology has been adopted in aerospace manufacturing as a result of the growing trend for lighter and more efficient aircraft. Because they offer greater qualities than metals with wider grain patterns, nanostructured metals are employed in the production of aeroplanes.

Aerospace Coating Market Snapshot

To know about the Research Methodology :- Request Free Sample Report

Aerospace Coating Market Key Dynamics:

Increasing Focus on Lightweight Materials Boosts Demand for Aerospace Coatings

The burgeoning emphasis on lightweight materials stands as a pivotal force propelling the aerospace coating market forward. The intrinsic efficiency of lighter aircraft in fuel consumption presents a substantial advantage for airlines, significantly curbing operational costs. Moreover, the heightened payload capacity of these lightweight planes translates into enhanced revenue streams. As of 2022, composite materials comprised roughly 50% of the typical commercial aircraft's weight, underscoring the prevalence and relevance of these advancements. Projections estimate the global aircraft coatings market to soar to $12,923.8 million by 2028, indicative of the intensified focus on lightweight materials within the aerospace sector.

The integration of lightweight materials in aircraft construction has triggered an upsurge in demand for aerospace coatings engineered to safeguard these materials against the formidable rigors of flight environments. These coatings must demonstrate resilience against extreme temperatures, high altitudes, and pervasive UV radiation while simultaneously embodying traits of lightness and enduring strength. Within the realm of aerospace coatings, a diverse array of options exists, each boasting unique properties. Among the prevalent variants are epoxies, polyurethanes, and acrylates, catering to varied needs and specifications.

The escalating prioritization of lightweight materials constitutes a fundamental driver propelling the aerospace coating market, a trajectory anticipated to persist in the foreseeable future. Airlines' steadfast pursuit of augmented fuel efficiency and emissions reduction solidifies the trajectory towards lightweight materials integration in their aircraft. This sustained evolution necessitates the development of pioneering aerospace coatings adept at fortifying and preserving these materials, marking a pivotal juncture in the industry's trajectory.

R&D Focuses on Developing Sustainable Aerospace Coatings

The aerospace coatings market is poised to hit a whopping $12,923.8 million by 2029, marking a substantial growth opportunity. Sustainability has become a major focus in aviation, driving hefty investments in research and development for eco-friendly aerospace coatings. These coatings aim to minimize aircraft's environmental footprints by cutting down on hazardous materials, and waste, and boosting fuel efficiency. The push for sustainability has spurred the emergence of innovative technologies like waterborne coatings that replace solvents and nanotech-based coatings, thinner and lighter than traditional ones.

While still in the early stages, these sustainable coatings hold immense promise in significantly reducing the aerospace industry's environmental impact. With fierce competition in this sector, numerous companies are racing to develop and provide these sustainable coatings, indicating an exciting future with ongoing R&D efforts expected to fuel even more ground-breaking innovations ahead. The rising demand for military aerospace coatings in various industrial sectors involving original equipment manufacturers and maintenance repair and overhaul influence the growth rate of the military aerospace coatings market.

The expanding applications within the aerospace and defense industry stand as pivotal drivers propelling market expansion. Notably, the surge in Aerospace Coating Market demand is attributed to the need for superior coverage in inner corners, smoother surfaces, and uniform finishes, elevating the appeal of liquid-based coating technologies. This emphasis on advanced coating solutions is poised to distinctly influence and accelerate the growth rate of the military aerospace coatings market.

Expansion of Commercial Fleet Drives Demand for Aerospace Coatings

The expanding global commercial airline fleet serves as a pivotal catalyst fueling the burgeoning Aerospace Coating Market demand With the escalation in air travel, airlines are pressed to augment their aircraft count to meet the surging needs for passenger and cargo conveyance. This burgeoning fleet expansion necessitates the production of new aircraft, thereby amplifying the demand for aerospace coatings. The International Air Transport Association (IATA) projects a surge in global passenger traffic, expected to reach 4.4 billion in 2024, surpassing pre-pandemic levels.

This anticipated increase in demand is driving airlines to expand their fleets substantially, with estimations indicating a potential rise to approximately 38,000 operational commercial aircraft by 2032. Each introduction of a new aircraft into the fleet necessitates protective coatings to endure the rigorous flight conditions, including extreme temperatures, high altitudes, and UV radiation. Aerospace coatings play a pivotal role in shielding aircraft exteriors from corrosion, erosion, and other damages, thereby ensuring structural resilience and prolonged service life. This expansion of the commercial fleet creates a cyclical uptick in demand within the aerospace coatings market. As aircraft manufacturing escalates, the need for aerospace coatings proportionally increases.

This spiraling demand serves as a driving force propelling extensive research and development efforts, culminating in the creation of more sophisticated, resilient, and technologically advanced coatings. The surge in the commercial airline industry is underpinned by multiple factors such as rising disposable incomes, global connectivity trends, and ongoing advancements in aircraft technology. These factors continue to propel travel demand, reinforcing the sustained expansion of the commercial fleet and concomitant reliance on aerospace coatings in the foreseeable future.

According to the Federal Aviation Administration (FAA), the total number of aircraft in the U.S. commercial airline fleet stood at just under 7,000 at the end of 2022. These aircraft are maintained to the highest standards set by government agencies and this includes routine inspection and maintenance of their protective coatings. The aircraft coatings industry overall is an important contributor to the economy and was valued at roughly $364 million in 2021,

The aerospace industry expects coatings suppliers to develop products that reduce application times, improve performance, and increase durability. A one percent improvement in fuel efficiency in the aviation industry lowers fuel costs by $700 million a year. On average, airlines incur about $100 a minute per flight in operating costs. Therefore, even saving just one minute of flight time could reduce total operating costs by more than $1 billion a year and significantly reduce environmental emissions.

Aerospace Coating Market Restraints

The aerospace coating market faces several key restraints impacting its growth trajectory. Foremost among these challenges is the high cost associated with these coatings, stemming from the utilization of top-tier materials and intricate manufacturing procedures, which particularly burdens smaller aircraft manufacturers. Additionally, the tightening grip of environmental regulations, intended to safeguard against hazardous materials, adds both complexity and expense to the production of aerospace coatings, potentially impeding market competitiveness for some companies. Compounded by this, the scarcity of skilled labor in the specialized aerospace industry hampers production efficiency, leading to slower processes and increased operational costs.

The global landscape of defense expenditure is experiencing a downturn primarily due to substantial reductions in funding by major nations previously dedicated to defense spending. This decline stems from the conclusion of prolonged military engagements in regions like Iraq and Afghanistan, coupled with a reconsideration of the financial sustainability of ongoing war expenditures. Despite this trend, specific regions are witnessing marginal increases in defense budgets, notably propelled by heightened investments from countries such as China, India, the Middle East, Japan, Brazil, and Russia.

These nations are directing these funds towards either modernizing their armed forces or reinforcing their national borders. Of significant note, the United States, holding the foremost position as the world's primary contributor to defense spending, accounting for approximately 40% of global defense outlay, has substantially curtailed its defense budget. This reduction has notably impacted the defense market, particularly affecting manufacturers of defense equipment, notably in the military aircraft sector, potentially influencing the demand for specialized aircraft coatings designed for military applications.

Aerospace Coating Market Opportunity

Affordable commercial air travel is gaining traction as a feasible alternative in developing nations, providing tourists with access to diverse destinations. Customers in emerging economies increasingly favor air travel due to its affordability, speed, and convenience compared to traditional transportation methods. To compete with international carriers dominating longer routes, lightweight and efficient planes are now deployed on shorter routes within emerging economies. This trend reflects the growing significance of the Texas aerospace coatings market, particularly in enhancing the efficiency and performance of these planes serving the burgeoning air travel demand in developing regions.

Extended-distance, low-cost business models are starting to take off thanks to the long-range and cheap operating costs of modern, lightweight aircraft. The connected city air travel of the carriers and the convenience of the passengers are both benefits of these business models. Therefore, it is expected that the global production of commercial aircraft will expand as a result of rising passenger traffic and the economic development of new nations.

The aerospace antimicrobial coating market is driven by the growing emphasis on passenger safety, health concerns, and the need to maintain hygienic conditions within aircraft. These coatings are engineered to withstand the unique environmental challenges of aviation, such as temperature variations, high-altitude conditions, and stringent safety regulations. Companies specializing in aerospace coatings are developing and offering antimicrobial solutions tailored to meet the specific requirements and regulations of the aviation industry. These coatings have the potential to become an integral part of aircraft interiors, contributing to a safer and more sanitary travel experience.

Aerospace Coating Market Challenges

As the Aerospace Coating Market are not permitted separately, the coated aircraft must be approved or cleared by several regulatory organizations. To show that the coated aircraft fit the requirements, design verification tests must be performed on them. To maintain a high standard, several coating producers test their products. Major coating producers on the market also have a Master File that lists all the proprietary components and manufacturing procedures used to create the product. This might enable time to be saved during approval. The approval time for different types of aircraft varies significantly.

A coated airplane must often wait many months for regulatory agencies to approve it. Additionally, any modification to the law affects the deadlines that coating producers must follow, eventually causing backlogs in the aerospace sector. Additionally, it's possible that the restrictions will get more costly and intricate. As a result, the time-consuming and strict regulatory standards provide a problem for the producers of coatings.

Aerospace Coating Market Segment Overview

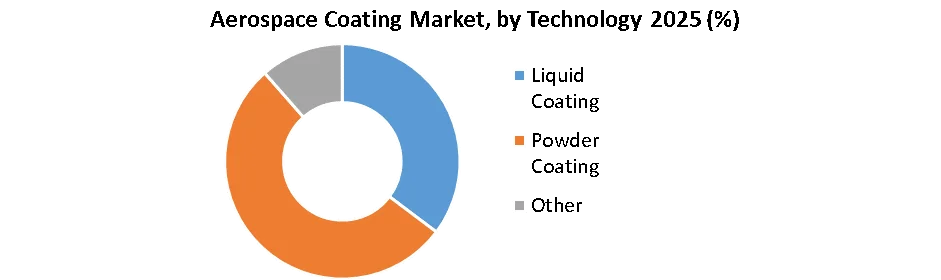

Based on Technology, The aerospace coating industry is divided into liquid coating and powder coating categories based on technology. The liquid coating market category held the largest Aerospace Coating Market revenue share in 2025. In addition to offering improved coverage on difficult-to-reach surfaces such as interior corners, liquid coating materials also produce a uniformly smooth surface. Most frequently, these coatings are applied using hand brushes, air sprays, or dip spins. They are used as corrosion inhibitors as well. There are two types of liquid coatings: solvent-based and water-based. The aircraft market uses solvent-based coatings because they are more resistant to adverse weather conditions. The demand for liquid coating materials, particularly solvent-based liquid coatings, is rising as a result of more rigorous environmental laws and government-imposed VOC emission caps.

Based on the End User, The aerospace coating market is divided into three categories based on end-users: general aviation, commercial aviation, and military aviation. The commercial aviation sector held the largest market share in 2025. Commercial aviation has developed into a lucrative market in recent years for aerospace coatings. Commercial aviation is seen as a subset of civil aviation and is mostly used for the transportation of people and commodities. Aerospace Coating Market Growth is being fueled by the rise in air travel, growth of global trade, and surge in freight traffic, which have all sparked new advances in the commercial aviation sector.

The demand for passenger air travel is rising due to rising tourism and falling travel costs, which is driving an increase in the number of commercial aircraft globally. The need for air freight is increasing as a result of expanding trade between nations like China and India. The military end-user market is expected to expand significantly over the course of the forecast period as a result of the rising demand for premium coatings with increased durability. Military aircraft, which are frequently made of aluminum alloys, need to be coated with materials that have greater corrosion resistance.

Aerospace Coating Market Regional Insights:

The North American region dominated the Aerospace Coating Market with a 36.1 % share in 2025. The region is expected to dominate the market through 2034 due to the U.S. aerospace market's growth and the introduction of significant aerospace businesses in Mexico. Due to strict controls by governing agencies, products with lower VOC and hydroxyapatite (HAp), such as polyurethane aerospace coatings, are predominantly used in this region.

The Asia Pacific region is expected to witness significant growth at a CAGR of 6.8% through the forecast period. It is expected that both production and sales of aerospace coatings increase significantly during the forecast period due to the promising prognosis for the aircraft sector in China, and India. The Asia Pacific is expected to become the most promising regional Market during the forecast period. Some of the main drivers of the region's growth are an increase in air travel and rising Defense market investments. The growth in air passenger traffic brought on by rapid urbanization in various nations has increased demand for aircraft and, consequently, Aerospace Coating Market. Another significant rising nation in the market for aerospace coatings is Sweden. Aerospace coatings business supplier products for a new long-distance tanker aircraft Airbus Defence and Space a global leader in designing, developing, and manufacturing military aircraft. It is considered the benchmark for new generations

The objective of the report is to present a comprehensive analysis of the global Aerospace Coating Market to the stakeholders in the market. The past and current status of the market with the forecast market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the market with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the market to the decision-makers

The reports also help in understanding the Aerospace Coating Market dynamic, and structure by analyzing the market segments and projecting the Aerospace Coating Market size. Clear representation of competitive analysis of key players by Vehicle type, price, financial position, product portfolio, growth strategies, and regional presence in the Aerospace Coating Market make the report an investor’s guide.

Aerospace Coating Market Competitive Analysis

The aerospace coating market is a highly competitive arena, characterized by a multitude of key players striving for innovation and market dominance. Leaders like PPG Industries, Sherwin-Williams, AkzoNobel, Hentzen Coatings, and LORD Corporation continuously drive the industry forward with their distinct contributions. PPG Industries excels in corrosion protection, while Sherwin-Williams focuses on extending aircraft lifespans. AkzoNobel leads in developing coatings to reduce aircraft weight, while Hentzen Coatings specializes in repairing aircraft surfaces. LORD Corporation stands out with its emphasis on noise-reduction coatings for aircraft.

This dynamic market, marked by rapid growth, used different type of market strategies to drive the Aerospace market demand, and rewards companies that innovate sustainable coatings meeting industry demands for durability, weight reduction, maintenance efficiency, and environmental impact. Continuous innovation and adaptability are pivotal for success in this evolving landscape, where companies offering multifaceted solutions hold a distinct advantage. Tiger Infrastructure Partners, a middle market growth infrastructure investor, has announced the acquisition of International Aerospace Coatings (“IAC”), a market-leading aviation services provider headquartered in Shannon, Ireland and Irvine, California.

20 million investment has been announced by AkzoNobel to increase and improve production at two of its sites in France A total of €15 million spent on the company’s aerospace coatings facility in Pamiers, which was taken over following the Mapaero acquisition in 2019. Production capacity is being boosted by 50%, while the funds will also be used to reduce environmental impact and improve safety processes and working conditions. These investments underline our growth ambitions and confirm our commitment to supporting economic development in France, the aerospace industry is increasing the supply of high-performance products that are more respectful of the environment.

The project will also enable the company to relocate the production of exterior polyurethane paints for aircraft widely used in Europe from its Waukegan plant in the US. Building work is expected to start by the end of 2024, with the new installations at both locations due to be operational in early 2025. AkzoNobel employs nearly 1,500 people in France and operates four production facilities, in Montataire (decorative paints), Dourdan (powder coatings), Limoges (adhesive markings), and Pamiers (aerospace coatings).

Aerospace Coating Market Recent Development

| Date | Company | Development | Impact |

|---|---|---|---|

| 08 May 2025 | PPG Industries | The company announced a $380 million investment to construct a new 198,000-square-foot manufacturing and warehousing facility in Shelby, North Carolina, dedicated entirely to aerospace coatings and sealants. | This facility will substantially expand production capacity and streamline supply chain logistics through modernized, digitized operations to meet surging global aerospace demand. |

| 18 November 2025 | AkzoNobel | AkzoNobel and Axalta Coating Systems announced a definitive agreement to combine in an all-stock merger of equals, creating a premier global coatings leader. | The transaction unites highly complementary portfolios in the aerospace coatings sector, driving customer-centric innovation backed by a joint $400 million annual R&D expenditure. |

| 18 December 2025 | AkzoNobel | The company committed a €50 million investment to upgrade its Waukegan, Illinois plant, which stands as its largest aerospace coatings production facility globally. | The multi-phase optimization project will deploy high-speed machinery and advanced automation to expand North American production scale and shorten color development lead times. |

| 29 January 2026 | AkzoNobel Aerospace Coatings | The company revealed plans to launch a brand new color blending and distribution hub in Dubai, United Arab Emirates, to support regional market expansion. | The automated facility will provide localized blending of advanced paint lines like Aerobase and Aerodur 3001, drastically reducing material procurement lead times for Middle Eastern MRO providers. |

| 20 May 2026 | H.I.G. Capital | The global alternative investment firm completed its acquisition of International Aerospace Coatings (IAC), a leading specialist in commercial and military aircraft painting. | With the financial backing of H.I.G. Capital, IAC intends to accelerate its international fleet maintenance growth strategy and expand its portfolio of dedicated aviation hangars. |

Aerospace Coating Market Scope: Inquire before buying

| Aerospace Coating Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 2.41 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 7% | Market Size in 2034: | USD 4.44 Bn. |

| Segments Covered: | by Resin Type | Polyurethane Epoxy Other |

|

| by Application | Exterior Interior |

||

| by End User | Commercial Military General Other |

||

| by Technology | Liquid Coating Powder Coating Other |

||

Aerospace Coating Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Leading Companies in the Aerospace Coating Industry

1. AkzoNobel N.V

2. PPG Industries Inc

3. Sherwin Williams

4. Mankiewicz Gebr.& Co.

5. Axalta Coating Systems

6. Saint-Gobain S.A.

7. Henkel Corporation

8. LORD Corporation

9. Asahi Kinzoku Kogyo

10.IHI Ionbond AG

11.Zircotec Ltd

12.Basf Se

13.Hentzen Coatings, Inc

14.Mapaero

15.Zircotec Ltd

16.Brycoat

17.Argosy

18.Axalta

Frequently Asked Questions:

1] What segments are covered in the Global Aerospace Coating Market report?

Ans. The segments covered in the Aerospace Coating Market report are based on Resin Type, Technology, Application and End User.

2] Which region is expected to hold the highest share in the Global Aerospace Coating Market?

Ans. The North America region is expected to hold the highest share in the Aerospace Coating Market.

3] What is the market size of the Global Aerospace Coating Market by 2034?

Ans. The market size of the Aerospace Coating Market by 2034 is expected to reach USD 4.44 Bn.

4] What is the forecast period for the Global Aerospace Coating Market?

Ans. The forecast period for the Aerospace Coating Market is 2026-2034.

5] What was the Global Aerospace Coating Market size in 2025?

Ans: The Global Aerospace Coating Market size was USD 2.41 Billion in 2025.