Adhesive Resin Market Size by Technology, Application, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

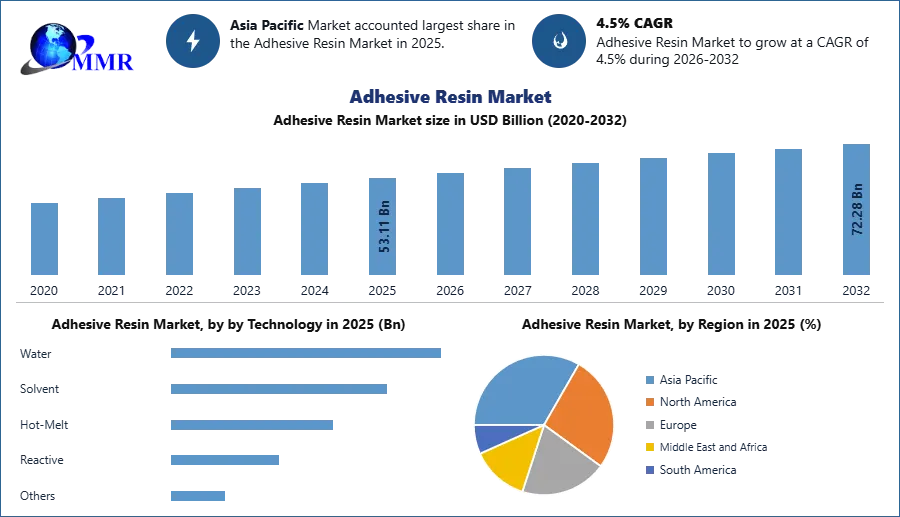

Adhesive Resin Market was valued nearly USD 53.11 Bn in 2025. Adhesive Resin Market size is estimated to grow at a CAGR of 4.5 % & is expected to reach at USD 72.28 Bn. by 2032.

Global Adhesive Resin Market Overview:

Adhesive resins are a composite material technology which has great adhesive qualities. Adhesive resin is used in a variety of applications, including woodworking, transportation, & footwear. Due to their tenacious consistency, adhesive resins like cement, glue, paste, or mucilage are in high demand in a range of applications. It promotes durability & constructs a robust composite structure because it is a diverse material efficient in dispersing stress to balance the joints & improves the cohesive strength of the product. It has a number of benefits, including flexibility & moisture resistance, as well as the potential to be used as an emulsion. To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

On the other hand adhesive resin, has limitations in terms of attaching large items with limited bonding surface area, which impacts stability at high temperatures, and difficulties in separating objects during testing, both of which act as market restraints.

Rapid expansion has been seen as a result of increasing demand & applications, and this trend is expected to continue during the forecast period. Adhesive resin demand has been driven by increased end-user awareness & increased applications, like in the automobile industry for packaging & labelling, woodworking, and footwear applications. The resin market is benefiting from the expansion of major important players as well as an increase in the number of end-users. The advantages of adhesive resin over binding techniques like welding, mechanical fastening, flexibility and cost-effectiveness have increased demand for adhesive resin.

Packaging & Labelling in Automotive industry:

Printed labels are used in the automotive industry to provide vital information, safety notifications, & cautions, including those that are immediately visible to drivers & passengers in a tiny number of circumstances. According to the MMR report study, automotive OEMs only apply a small number of labels, about 10-15 percent, the majority of which are visible to car owners, such as tyre pressure and warning labels. 'The rest are generally identification signs on the car's secret components. The majority of labelling takes place in the supply chain, before the car is assembled. Because the 'parts - metal bits' have a lot number stamped on them, the transport box must be labelled securely & precisely. Only a malfunctioning part is worse for automakers than a mislabeled part. A single digit error is dreadful, & it can cost both the manufacturer and the supplier a lot of money. Some businesses have recognized one of their main issues as the fact that they are still using older systems that necessitate such engagement.

Technology for adhesion:

S8049 rubber-hybridized acrylic adhesive from Avery Dennison is designed for strong low surface energy polymers in automotive applications. It is possible to combine good peel adhesion to highly challenging materials with robust resistance with this adhesive technique.' This adhesive technique will be used to expand the product line with a variety of adhesives that are suitable for a wide range of automotive applications and can achieve similar results on smooth low energy lacquered or plastic parts.

Adhesive resins as composite materials have two main features that are expected to fuel market growth during the forecast period: chemical and moisture resistance. The market for an adhesive resin is expected to increase throughout the forecast period, owing to the increased need for ecologically friendly products. Toughness, ageing, & temperature resistance, as well as the capacity to give long-term adhesiveness, are projected to move the global market forward over the forecast period.

The building and construction category is likely to account for a greater share of the global market over the forecast period. A high-performance adhesive glue is used to laminate wood for decks, walls, & roofs. It's also used in other things that require high adhesion to a range of substrates. High-performance adhesive resin is widely used in the building & construction industry, from flooring and countertops to structural adhesives and paints. As a result, the building and construction industry is expected to drive the adhesive resin market over the forecast period.

Building & Construction Industry:

Green construction approaches are increasingly being used by building construction businesses to create energy efficient structures and lower construction costs. Green construction is the technique of creating energy-efficient structures with low environmental impact by employing sustainable building materials and construction procedures. According to the World Green Building Trends Survey 2015, green construction projects were undertaken by roughly 51% of construction businesses in the United Kingdom. Leadership in Energy and Environmental Design (LEED) certifications assist construction companies in developing high-performance, sustainable residential and commercial buildings, as well as providing a variety of benefits ranging from tax breaks to marketing opportunities.

The cost of building construction has risen gradually over time due to rising material costs. With rising prices of resources such as crude oil, a fundamental component of asphalt, which grew by 49 %, and softwood lumber, a major component used in building construction, which rose by 23 % over the historic period, companies in the industry witnessed restrained growth in earnings. In the United States, cement costs grew by 2.5 percent in the year 2018, while plumbing and fixtures prices increased by 3%. During the historic period, high material prices had a negative impact on the building construction sector.

The objective of the report is to present a comprehensive analysis of the Adhesive Resin Market to the stakeholders in the Application. The past and current status of the Application with the forecasted Market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the Application with a dedicated study of key players which include Market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the Market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the Application to the decision-makers.

The report also helps in understanding the Adhesive Resin Market dynamics, structure by analyzing the Market segments and project the Adhesive Resin Market size. Clear representation of competitive analysis of key players by Technology, price, financial position, Technology portfolio, growth strategies, and regional presence in the Adhesive Resin Market make the report investor’s guide.

Adhesive Resin Market Scope: Inquiry Before Buying

| Adhesive Resin Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 53.11 USD Billion |

| Forecast Period 2026-2032 CAGR: | 4.5% | Market Size in 2032: | 72.28 USD Billion |

| Segments Covered: | by Technology | Water Solvent Hot-Melt Reactive Others |

|

| by Application | Paper & Packaging Building & Construction Transportation Leather & Footwear Others |

||

| By End User | Aerospace Consumer Goods Industrial Medical Transportation |

||

Adhesive Resin Market, by Region

• North America (United States, Canada and Mexico)

• Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

• Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

• Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

• South America (Brazil, Argentina Rest of South America)

E.I. du Pont de Nemours and Company (U.S.)

ExxonMobil Chemical (U.S.)

Eastman Chemical (U.S.)

Dow Chemical (U.S.)

Lawter (U.S.)

Mitsui Chemicals America, Inc. (U.S.)

Mitsubishi Chemical (Japan)

Georgia-Pacific Chemicals (U.S.)

Ashland Inc. (U.S.)

BASF SE

Henkel AG & Co. KGaA

H.B. Fuller Company

Sika AG

Arkema S.A.

Huntsman Corporation

Evonik Industries AG

Wacker Chemie AG

Momentive Performance Materials Inc.

3M Company

Avery Dennison Corporation

Mapei S.p.A.

DIC Corporation

Kolon Industries Inc.

Synthomer plc

Others