Fluid Loss Control Additives Market Size by Type of Additives, Fluid Types, Application, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2032

Overview

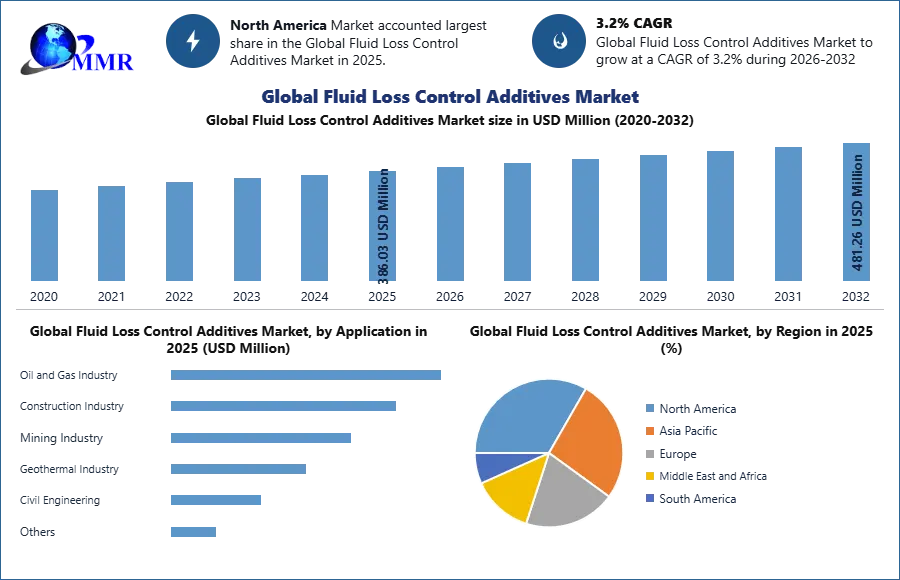

Global Fluid Loss Control Additives Market Size was valued at USD 386.03 Mn in 2025 and is expected to reach USD 481.26 Mn by 2032 at a CAGR of 3.2 % over the forecast period.

Fluid Loss Control Additives Market Overview

Fluid Loss Control Additives are chemical substances used in the oil and gas drilling industry, as well as other industries such as construction, geothermal drilling, and mining. These additives are designed to control and reduce the loss of drilling fluids into the formation during drilling operations. Drilling fluids, also known as drilling mud, are essential for various purposes during drilling, including lubrication, cooling, and carrying drilled cuttings to the surface. However, excessive fluid loss into the formation can lead to a range of issues, including wellbore instability, formation damage, and increased operational costs.

The global market for fluid loss control additives is essential to the oil and gas sector. These additives are added to drilling fluids to stop fluid loss into permeable rocks while drilling is taking place. By doing so, the risk of formation damage is decreased and wellbore stability is maintained. Rising drilling activity, increased demand for oil and gas, and improvements in drilling technology are all factors that affect market growth. The development of ecologically friendly additives is also being influenced by rigorous environmental restrictions and the necessity for sustainable drilling techniques. The market for fluid loss control additives is anticipated to be driven by regions with considerable oil and gas exploration, such as North America, the Middle East, and Asia-Pacific. There are several significant competitors in the market, and they are all working hard to innovate and create effective additives to satisfy the changing demands of the sector.

To know about the Research Methodology :- Request Free Sample Report

Fluid Loss Control Additives Market Dynamics

Fluid Loss Control Additives Market Drivers

Global demand for oil and gas drilling additives is a major factor driving the market for fluid loss control additives. Effective drilling fluids that guarantee wellbore stability are increasingly important as exploration and production activities which move towards unconventional deposits. Drilling Fluid Additives play a pivotal role in the global oil and gas industry. The market for these additives is driven by the increasing demand for oil and gas worldwide. Effective drilling fluids, including High-Temperature Fluid Loss Control additives, are essential for ensuring wellbore stability, especially as exploration and production activities move towards unconventional deposits.

Improvements in drilling technology have produced deeper and more intricate wells, necessitating the employment of cutting-edge additives to reduce fluid loss and keep drilling efficiency. The sector is being compelled by strict environmental restrictions to use eco-friendly additives that lessen the impact of drilling operations on the environment. Environmental concerns are compelling the industry to adopt eco-friendly additives that minimize the environmental impact of drilling operations. The development of novel fluid loss control additives that improve overall drilling performance is also being sparked by the growing emphasis on improving drilling processes for increased productivity and decreased operational costs. The development and evolution of the fluid loss control additives market on a global basis are mostly influenced by these main factors.

Fluid Loss Control Additives Market Restraints

The growth and dynamics of the global market for fluid loss control polymers and other additives are impacted by a number of significant restrictions. The fluctuation in oil prices is one of the major problems. Drilling activity can be directly impacted by changes in oil prices since businesses may reduce exploration and production initiatives when prices are low. This in turn has an impact on the demand for fluid loss control additives, which causes the market to cycle. The market's growth is constrained by the strict regulatory environment. Governments and business organizations have tightened drilling laws as a result of environmental concerns. This has forced the industry to use additives that are both efficient and safe for the environment.

The adoption of advanced fluid loss control additives, such as Oil-Based Drilling Fluids, may be hampered by the oil and gas industry's capital-intensive nature, especially for smaller exploration and production businesses. Smaller exploration and production businesses might find it difficult to budget for pricey drilling fluid technology, which would restrict the market's potential.

Restraints come from technical difficulties as well. The demand for drilling additives that work well in high-pressure and temperature environments is increasing as drilling operations become more complicated. The industry's task is to create additives that satisfy these requirements while remaining affordable. Drilling activities can be impacted by local and global geopolitical instability, which in turn affects the demand for fluid loss control additives. Due to political or economic uncertainty, supply chain disruptions and project delays might impede market expansions.

Fluid Loss Control Additives Market Opportunities

Numerous significant chances for development and innovation exist in the global market for fluid loss control additives. The market has a sizable opportunity as a result of the increased attention being paid to unconventional oil and gas sources like deep water and shale reserves. The demand for customized fluid loss control additives is fuelled by the fact that these reserves frequently call for specialized drilling fluid solutions to deal with particular problems. The increased focus on sustainable and environmentally friendly drilling techniques creates opportunities for the creation of eco-friendly additives such as Water-Based Drilling Fluids. Businesses with the ability to produce efficient additives while reducing their environmental impact are likely to acquire a competitive advantage in the market. Polymer-Based Fluid Loss Control additives could undergo a revolution thanks to developments in nanotechnology and material science.

The performance, stability, and environmental impact of nano-based additives may all be improved. Opportunities for expansion are also created by the rising offshore exploration and production activities. The creation of specific chemicals was required since offshore drilling calls for additives that can survive abrasive sea environments and deeper whole depths. Joint development of custom solutions might result from partnerships between additive makers and oil and gas firms. Market traction may be possible for specialized additives that address certain drilling difficulties. There is an expanding market for additives that connect with smart drilling equipment as the sector progresses toward digitization and automation. There is a lot of potential for additives that can adjust to drilling circumstances in real-time and improve drilling efficiency.

Fluid Loss Control Additives Market Challenge

Numerous significant obstacles that affect the market's trajectory exist for fluid loss control additives globally. The unpredictability of oil prices, which might affect drilling activity and therefore have an impact on additive demand, is one of the main challenges. The creation of additives that are efficient and ecologically benign is mandated by the strict environmental laws placed on the oil and gas industry, which presents a technical and regulatory difficulty. The adoption of modern additives may be hampered by the industry's capital-intensive nature, especially by smaller exploration and production businesses. Technical challenges are also brought about by the industry's shift toward unconventional reserves and complicated drilling sites, which call for additives that can operate under conditions of high pressure and temperature.

Fluid Loss Control Additives Market Trends

The global market for Fluid Loss Control Additives, including Polymer-Based Fluid Loss Control, is being shaped by a number of key trends. Due to increased environmental concerns, there is a growing demand for environmentally friendly additives. Manufacturers are putting their efforts into creating additives that lessen drilling operations' negative effects on the environment while keeping their efficacy. The development of unconventional drilling techniques like hydraulic fracturing has increased the demand for additives that can handle the particular difficulties these techniques present.

The industry is seeing a rise in demand for additives that are tailored to the needs of unconventional reserves as they become more prevalent. The market is being impacted by the integration of cutting-edge technology, such as automation and digitization. Gaining popularity are drilling additives that can communicate with intelligent drilling systems to enhance fluid performance and drilling parameters. The exploration of deeper and more intricate wells in offshore and deep water environments is driving the development of additives able to tolerate extremely high temperatures and pressures.

Collaborations between additive producers and oil and gas firms are also expanding, resulting in the co-development of solutions that are specifically customized to each drilling difficulty. To improve the effectiveness of fluid loss control additives, research and development activities are concentrating on nanotechnology and new materials. Better stability and efficiency under diverse drilling situations are the goals of these developments. Globally, the market for fluid loss control additives is changing as a result of environmental issues, technical breakthroughs, and altered drilling techniques, opening the way for more effective and environmentally friendly drilling operations.

Fluid Loss Control Additives Market Segment Analysis

By Type of Additives: The type of additives used in drilling operations can be used to segment the global market for fluid loss control additives. Organic substances that are used as natural additions for their ability to reduce fluid loss include starch and lignite. Synthetic additives include a variety of polymeric chemicals designed to improve drilling fluid performance and efficiently manage fluid loss. For different drilling circumstances, this category includes polymers that are anionic, cationic, and non-ionic. Modified natural polymers improve stability and control by combining the advantages of natural and synthetic additives. Specialty additives like lost circulation materials are made to solve serious fluid loss issues by sealing formation fissures and fractures. According to their unique drilling requirements and geological conditions, drilling operators can choose from a variety of additive solutions thanks to this segmentation, which reflects the many ways used to manage fluid loss issues.

By Fluid Types: The market for fluid loss control additives can be divided into several groups depending on the Fluid Types. These additives are crucial in the oil and gas industry's drilling operations to limit fluid loss into formations, ensure wellbore stability, and reduce formation damage. Fluid loss control additives are added to cement slurries in the construction sector to optimize cementing operations by lowering fluid loss and increasing cement bond strength. These additives also help to maintain wellbore integrity and maximize drilling efficiency in geothermal drilling. Fluid loss control additives are used in mining, especially in drilling operations where they aid in preventing fluid loss and guarantee efficient mineral extraction. The industry also includes civil engineering, where additives help build sturdy subsurface buildings and foundations. The versatility and importance of fluid loss control additives across a range of industrial Fluid Types around the world are highlighted by this multi-sectorial segmentation.

Regional Insights for Fluid Loss Control Additives Market

North America dominated the largest market share in 2025. The oil and gas operations in this region, particularly in the United States and Canada, are what drive the market for fluid loss control additives. The demand for sophisticated drilling technologies, particularly efficient fluid loss control additives, has expanded as the region's concentration on shale gas and tight oil deposits has grown. Environmentally friendly additives are increasingly popular as a result of stricter environmental restrictions. The market's growth is further aided by the existence of numerous significant oil and gas corporations and a focus on technological innovation. The region's need for fluid loss control additives is still being shaped by North America's changing energy landscape and ongoing exploration operations.

Asia-Pacific: Oil and gas exploration and production operations have increased significantly in the Asia Pacific area, which has an impact on the market for fluid loss control additives. Rapid industrialization and urbanization are occurring in nations like China and India, increasing the need for energy. Effective drilling solutions, such as fluid loss control additives, are therefore increasingly required to support these expanding activities. In addition, the region's trend towards offshore exploration and unconventional resources increases the need for specific additives. The adoption of sophisticated additives is encouraged by regulatory actions to enhance drilling safety and environmental effects. As a result of these factors, the Asia Pacific market is expected to rise steadily.

Fluid Loss Control Additives Market: Competitive Landscape

The presence of major competitors working to innovate and seize a sizeable portion of this crucial business characterizes the competitive landscape for fluid loss control additives globally. In order to meet the changing needs of oil and gas, construction, mining, and other key industries, companies active in this market concentrate on research and development to produce sophisticated additives. The market is dominated by well-known companies with wide product portfolios and a global presence like Halliburton, Schlumberger, and Baker Hughes, a GE Company (now Baker Hughes). Utilizing their technological know-how and in-depth industry knowledge, these industry titans provide a comprehensive selection of fluid loss control additives.

Companies such as Clariant, Kemira, and Solvay are important market participants as well, providing specialty additives that address certain drilling difficulties. The wellbore stability, drilling effectiveness, and environmental sustainability of their novel formulations are all goals. With the introduction of cutting-edge additives and methods for fluid loss control, start-ups and niche companies also play a significant role in the competitive environment. In order to address particular drilling conditions, these players frequently concentrate on developing individualized, ecologically friendly solutions. Oil and gas corporations and additive manufacturers collaborating on projects further sculpt the market environment.

Through these agreements, difficulties related to fluid loss in particular drilling operations can be successfully addressed by co-developing unique solutions. Companies are investing in research to create eco-friendly additives that go by strict environmental standards as sustainability becomes more and more important.

Recent Key Development:

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 02 January 2026 | SNF Group | The company successfully completed the €135 million acquisition of Syensqo’s Oil & Gas division, incorporating a major portfolio of fluid loss control agents. | This acquisition consolidates SNF's leadership in water-soluble polymers and strengthens its technical expertise in HPHT filtration control. |

| 15 January 2025 | Clariant AG | Clariant launched a new series of sulphonated polymer additives specifically designed for industrial filtration and harsh oilfield environments. | The high-performance polymers provide superior thermal stability, meeting the growing demand for additives that maintain rheological integrity in deepwater wells. |

| 22 October 2025 | SLB (Schlumberger) | SLB received the Best Oilfield Fluids and Chemicals award for its OpenPath Flex service, which optimizes fluid management in carbonate reservoirs. | The technology enhances treatment efficiency and reduces environmental impact by using customizable chemical formulations for better leak-off control. |

| 12 February 2026 | Halliburton | Halliburton advanced its carbon sequestration capabilities with the launch of the XTR CS injection system for extreme temperature conditions. | The system integrates specialty fluid additives to ensure wellbore integrity during the injection and storage of CO2 in offshore formations. |

| 25 January 2026 | A*STAR / Halliburton | A*STAR and Halliburton officially launched the NEX Lab to pioneer innovations in well completion and specialty chemical additives. | This collaboration focuses on developing next-generation fluid loss agents to reduce formation damage and improve the rate of penetration in complex drilling projects. |

Global Fluid Loss Control Additives Market Scope: Inquire before buying

| Global Fluid Loss Control Additives Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 386.03 USD Million |

| Forecast Period 2026-2032 CAGR: | 3.2% | Market Size in 2032: | 481.26 USD Million |

| Segments Covered: | by Type of Additives | Natural Polymers Synthetic Polymers Specialized Additives Modified Natural Polymers |

|

| by Fluid Types | Water-Based Fluids Oil-Based Fluids Synthetic-Based Fluids |

||

| by Application | Oil and Gas Industry Construction Industry Mining Industry Geothermal Industry Civil Engineering Others |

||

Fluid Loss Control Additives Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Fluid Loss Control Additives Key Players

1. Halliburton

2. Baker Hughes, a GE Company (now Baker Hughes)

3. Clariant

4. Kemira

5. Solvay

6. Croda International

7. Chevron Phillips Chemical Company

8. The Dow Chemical Company

9. BASF SE

10. Lubrizol Corporation

11. Ecolab Inc.

12. CP Kelco

13. Drilling Specialties Company

14. Newpark Resources Inc.

15. National Oilwell Varco (NOV)

16. Nouryon

17. Croda International

18. Innospec Inc.

19. Croda International

20. TETRA Technologies, Inc.

21. Parchem Fine & Specialty Chemicals

22. Stepan Company

23. AkzoNobel

24. Wyo-Ben, Inc.

25. Schlumberger Limited

Frequently Asked Questions:

1] What is the growth rate of the Fluid Loss Control Additives Market?

Ans. The Global Fluid Loss Control Additives Market is growing at a significant rate of 3.2% over the forecast period.

2] Which region is expected to dominate the Fluid Loss Control Additives Market?

Ans. Asia Pacific region is expected to dominate the Fluid Loss Control Additives Market over the forecast period.

3] What is the expected Global Fluid Loss Control Additives Market size by 2032?

Ans. The market size of the Fluid Loss Control Additives Market is expected to reach USD 481.26 Millon by 2032.

4] Who are the top players in the Fluid Loss Control Additives Market?

Ans. The major key players in the Global Fluid Loss Control Additives Market are Halliburton, Baker Hughes, Clariant, Kemira, Solvay.

5] Which factors are expected to drive the Fluid Loss Control Additives Market growth by 2032?

Ans. An increase in the production and exploration of shale gas and increasing investments in the latest and unconventional drilling technologies are the factors expected to drive the Fluid Loss Control Additives Market growth over the forecast period (2026-2032).

6] Which countries dominate the fluid loss control additives market?

Ans. In 2025, the United States, Canada, China, and some Middle Eastern countries were significant players in this market.