Europe UV LED Market Size, Share & Forecast (2025–2032): Technology Disruption, Regulatory Tailwinds & Structural Migration from Mercury to Solid-State UV

Overview

Overview — Europe UV LED Market Size & Forecast (2025–2032)

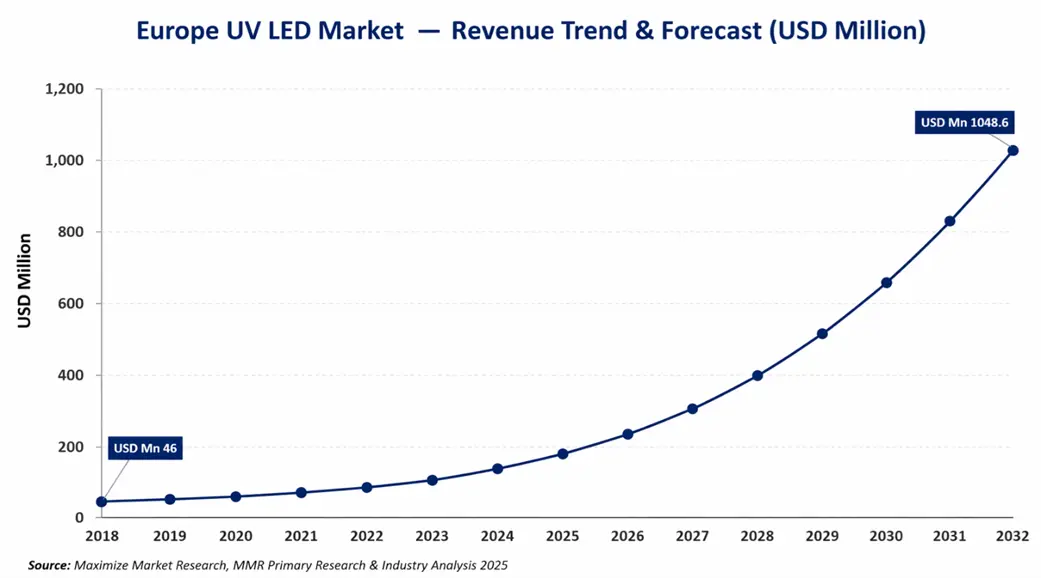

The Europe UV LED Market was valued at USD 215.3 Million in 2025 and is projected to reach USD 1,048.6 Million by 2032, growing at a CAGR of 25.4% during the forecast period 2025–2032. UV-C LEDs dominate with ~52% revenue share, driven by irreplaceable pathogen-elimination efficacy across healthcare, food processing, and water treatment verticals. The market is structurally propelled by the EU RoHS Directive mandating mercury phase-out, the European Green Deal energy efficiency targets, and post-COVID disinfection infrastructure investment — making UV LED adoption increasingly non-discretionary across European industrial sectors. Germany leads with ~27% regional revenue share, while Eastern Europe emerges as the fastest-growing sub-region at an estimated 28%+ CAGR, fuelled by EU compliance deadlines and industrial modernisation investment pulling mercury-era equipment replacement forward by 3–5 years.

Every hospital corridor has one quiet obligation — nothing harmful passes through. For a century, that obligation was discharged by mercury vapour lamps: toxic, fragile, energy-hungry, and impossible to miniaturise. They worked. And so no one replaced them — until they had to. The Europe UV LED Market is not a lighting story. It is a disinfection infrastructure revolution, quietly dismantling a century-old technology and replacing it with a solid-state photon engine that is safer, longer-lasting, and exponentially more precise. The paradox that defines this market is sharp: the technology that replaces mercury is not cleaner because it is newer — it is cleaner because it never contained poison to begin with.

That single fact is reshaping EU regulatory timelines, industrial procurement decisions, and capital allocation across Europe — and the inflection point arrived ahead of schedule. They worked. And so no one replaced them — until they had to. The Europe UV LED Market is not a lighting story. It is a disinfection infrastructure revolution, quietly dismantling a century-old technology and replacing it with a solid-state photon engine that is safer, longer-lasting, and exponentially more precise. The paradox that defines this market is sharp: the technology that replaces mercury is not cleaner because it is newer — it is cleaner because it never contained poison to begin with. That single fact is reshaping EU regulatory timelines, industrial procurement decisions, and capital allocation across Europe — and the inflection point arrived ahead of schedule.

Key Market Highlights Of Europe Uv Led Market — 2025

• Market Value (2025): USD 215.3 Million → USD 1,048.6 Million by 2032 — CAGR of 25.4%

• UV-C dominates: ~52% revenue share driven by irreplaceable pathogen-elimination efficacy

• EU RoHS Directive + Green Deal mandate mercury phase-out — UV LED is the only fully compliant, scalable commercial alternative

• Total cost of ownership over 5 years favours UV LED by 40–60% — primary barrier is buyer education and capex financing, not economics

• Germany leads with ~27% regional share; Eastern Europe fastest-growing at ~28%+ CAGR

• Residential and agriculture remain near-zero penetration — combined EUR 160–210 Mn white space by 2032

Report Coverage & Market Scope_ Europe UV LED Market

| Report Coverage | Details |

| Base Year | 2025 |

| Forecast Period | 2026–2032 |

| Historical Data | 2019–2025 |

| Market Size — Base Year (2025) | USD 215.3 Million |

| Market Size — Forecast Year (2032) | USD 1,048.6 Million |

| CAGR (2025–2032) | 25.4% |

| Dominant Technology Segment | UV-C (~X2% revenue share) |

| Dominant Application Segment | UV Curing (~X8% revenue share) |

| Fastest-Growing Application | Disinfection & Sterilisation (~26.2% CAGR) |

| Leading Country | Germany (~27% market share) |

| Fastest-Growing Sub-Region | Eastern Europe (~28%+ CAGR) |

| Key Players Covered | 38 Companies Profiled |

| Segments Covered | Technology · Application · Industry Vertical · Country |

Europe UV LED Market _ Size & Growth Trajectory

Fig:Europe UV LED Market — Revenue Trend & Forecast (USD Million)

To know about the Research Methodology :- Request Free Sample Report

The growth trajectory is not linear — it is accelerating. The 2022–2024 period represents an inflection: post-COVID procurement normalisation, EU regulatory deadlines crystallising, and UV LED system costs crossing the economic parity threshold with mercury alternatives. The market does not need further technology proof. It needs financing architecture and buyer education. Both are arriving.

Europe UV LED Market Volume Economics & Demand Analysis: Why Demand Is Structurally Inelastic

| Application Revenue Distribution — Europe UV LED Market (2025, % Share) | ||

| UV Curing | ■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■ | 38% |

| Disinfection/Steril. | ■■■■■■■■■■■■■■■■■■■■■■■■ | X8% |

| Medical Light Therapy | ■■■■■■■■■■■■ | X4% |

| Optical Sensing | ■■■■■■■■■ | X1% |

| Counterfeit Detection | ■■■■■ | X% |

| Others | ■■■ | X% |

UV curing commands the largest revenue share today — but the market's growth engine is disinfection. Curing is a volume-mature vertical with predictable replacement cycles and moderate margin expansion. Disinfection is structurally different: it is compliance-driven, non-deferrable, and expanding into new verticals with every regulatory update. The two segments are diverging — and the investor with curing exposure today needs disinfection exposure by 2025. Despite a 40–60% lower total cost of ownership, UV LED adoption remains below 40% across several industrial segments — highlighting a structural gap between economic viability and buyer awareness.

The demand logic is inelastic for a simple reason: UV LED adoption is no longer a choice in most European industrial contexts — it is a compliance trajectory. EU RoHS restrictions on mercury in new equipment, combined with Green Deal energy efficiency targets, mean that every product refresh, facility upgrade, or new construction that includes UV functionality defaults to LED. Volume is structurally locked in.

Kry Economic Insight

UV LED total cost of ownership over 5 years beats mercury by 40–60% when energy savings (50–70% lower consumption), replacement cycle differential (10–20× longer lifespan), and hazardous waste disposal costs are included. The adoption barrier is not economic — it is a capex financing gap and a buyer education deficit.

Europe UV LED Market Segmentation & Profit Pool Analysis: Where the Profit Pools Concentrate

By Technology — Revenue & Growth Profile

| Technology | Wavelength | 2025 Share | Primary Application | Growth Driver | Margin |

| UV-C | 200–280 nm | ~52% | Disinfection & sterilisation | Regulatory mandate + post-COVID | Highest |

| UV-A | 315–400 nm | ~X6% | UV curing — printing, coatings, adhesives | Volume base — industrial replacement | Medium |

| UV-B | 280–315 nm | ~X2% | Medical phototherapy, agriculture | Underpenetrated — early stage growth | Medium–High |

UV-C is not merely the dominant segment — it is the structurally protected segment. No alternative technology matches UV-C LED's pathogen elimination efficacy without chemicals, heat, or residue. This is not a competitive moat built on product design. It is physics. Competing against UV-C LED in disinfection requires replicating the technology itself — which means competitors must become UV-C LED manufacturers. There is no substitution path.

By Industry Vertical — Adoption Stage & Opportunity

| Industry Vertical — 2022 Revenue Share (%) & Adoption Stage | ||

| Healthcare & Medical | ■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■ | %31 |

| Industrial | ■■■■■■■■■■■■■■■■■■■■■■■■■■■■■ | %28 |

| Commercial | ■■■■■■■■■■■■■■■■■■■ | %18 |

| Agriculture | ■■■■■■■■■■■■■ | %13 |

| Residential | ■■■■■■■■■■ | %10 |

Structural Opportunity

Residential UV LED — 10% of revenue today — is approaching its consumer inflection point. Smart home air purifiers, under-sink water sterilisers, and portable UV wands are creating a mass-market demand curve that industrial-focused suppliers are entirely unprepared for. The company that designs a consumer-grade UV-C product for EUR XX0–X50 retail price will access a buyer segment three times larger than the current industrial base.

Europe UV LED Market Trends, Drivers, Restraints & Opportunities (DROCT Framework): Strategic Market Forces

| Dimension | Key Forces | Impact |

| Drivers | EU mercury phase-out (RoHS); post-COVID disinfection mandates; Green Deal energy targets; UV curing adoption in printing, packaging & electronics | Very High |

| Restraints | High initial capex vs mercury; output power limits at specific wavelengths; technology maturity concerns among conservative buyers | High — structural |

| Opportunities | Residential consumer market; agriculture & food processing; smart building HVAC; municipal water treatment; pharma cleanrooms | Very High |

| Challenges | Buyer TCO education; supply chain concentration in Asia; limited European fab base; wavelength standardisation across applications | Medium–High |

| Trends | Mercury regulation tightening; miniaturisation enabling wearable UV; AI-driven dosimetry optimisation; UV-C IoT sensor integration; precision agriculture photobiology | Transformative |

Europe UV LED Market Value Chain Transformation & Value Migration Analysis

The Europe UV LED landscape looks like a lighting industry listing. It is not. The companies winning are not those with the largest lighting portfolios. They are the companies that understood — earliest — that UV LED is a life-sciences and industrial process business wearing a photonics product disguise. Competitive advantage is concentrating fast around three capabilities: wavelength precision IP, system integration depth, and application-specific dosimetry expertise. Component-price competition is a race to margin zero.

| Value Migration Map — Europe UV LED Market 2023 | ||

| Mercury Vapour Lamps | → RoHS + Green Deal | UV LED Solid-State Systems |

| Component-Price Competition | → Margin compression | System Integration IP |

| Single-Application Products | → Customer consolidation | Multi-Application UV Platforms |

| Manual Dosimetry Control | → IoT + AI automation | Smart Adaptive UV Management |

| Asian OEM Dependency | → Supply chain risk | European Local Manufacturing |

The Central Structural Shift

Value is migrating from hardware to intelligence. The UV LED company of 2027 will not sell luminaires — it will sell sterilisation certainty. The transaction will be a service contract: guaranteed log-reduction of pathogens, measured by IoT sensors, reported to compliance dashboards, billed per square metre per month. That model does not yet exist at scale. That is the opportunity.

Analyst View

Rucha Deshpande| Research Manager, MMR — Photonics & Advanced Materials | Maximize Market Research

"The mercury-to-UV-LED transition is not a technology upgrade cycle — it is a regulatory-enforced market transfer. By 2027, any European industrial buyer still specifying mercury UV systems will face procurement compliance risk, not just operational inefficiency. Players that build dosimetry IP and service architectures now will capture disproportionate margin when the demand wave breaks. The window is 24 months."

Impact — UV LED suppliers must reframe the value proposition from component performance to system-level outcome delivery. Buyers are not purchasing lumens — they are purchasing sterilisation certainty and regulatory compliance.

Europe UV LED Market Regional Analysis & Growth Opportunities: Where Volume vs Value Plays Out

| Country Revenue Contribution — Europe UV LED Market (2025, Estimated %) | ||

| Germany | ■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■ | %X7 |

| United Kingdom | ■■■■■■■■■■■■■■■■■■■■■■■ | %X9 |

| France | ■■■■■■■■■■■■■■■■■ | %X4 |

| Italy | ■■■■■■■■■■■■■ | %X1 |

| Netherlands | ■■■■■■■■■■■■ | %X0 |

| Spain | ■■■■■■■■■■■ | %X |

| Rest of Europe | ■■■■■■■■■■■■ | %X0 |

| Country | Strategic Narrative | Primary Driver | Watch Signal |

| Germany | Europe's UV LED anchor. Automotive curing lines (BMW, Mercedes), precision electronics, and hospital sterilisation converge to create the continent's highest UV LED intensity per sq km of industrial floor space. | Auto + healthcare + electronics | ISO sterilisation mandates expanding to non-medical buildings |

| United Kingdom | Post-Brexit regulatory divergence creates unique dynamics. NHS UV-C procurement accelerating. Thames Water and Anglian Water UV infrastructure upgrades among Europe's largest municipal UV LED deployments. | Healthcare + water treatment | UK REACH post-Brexit — potential to diverge from EU mercury timeline |

| Netherlands | Outsized UV LED demand relative to country size: Port of Rotterdam water treatment, 10,000+ ha of greenhouse agriculture, and Philips/ASML supply chain create a uniquely dense UV LED ecosystem. | Water treatment + AgriTech | Greenhouse UV-B integration for crop yield — largest EU white space per hectare |

| Eastern Europe | Fastest-growing sub-region at estimated 28%+ CAGR. EU accession compliance deadlines and industrial modernisation investment are pulling mercury-era equipment replacement forward by 3–5 years. | EU compliance + industrial upgrades | Poland and Czech Republic pharmaceutical sector — major procurement cycle imminent |

Europe UV LED Market Technology Trends & Innovation Landscape: The Disruption Architecture

UV LED technology has crossed its performance credibility threshold. The historical objections — insufficient output power, wavelength limitations, premature failure under thermal stress — have been systematically resolved at the engineering layer since 2020. What persists is not a technology problem. It is a market architecture problem. The next competitive battle will not be won in the fab. It will be won in the application engineering lab, the hospital procurement office, and the IoT platform integration team.

| Technology Layer | Innovation | 2025 Status | Value Created |

| UV-C Wavelength Precision | Sub-265nm LEDs with >5mW output now commercial | Scaling | Pathogen-specific dosimetry — no mercury equivalent |

| Thermal Management | Advanced heat-sink integration extending operational life | Mature | 40% longer system lifespan vs gen-1 UV LED |

| Smart Dosimetry (AI/IoT) | Real-time UV dose optimisation — ensures compliance, eliminates over-dose waste | Emerging | Compliance reporting + service contract architecture |

| Miniaturisation | Chip-scale UV LED packages enabling wearable and portable form factors | Advancing | Consumer market access + new application verticals |

| Multi-Wavelength Arrays | Single device spanning UV-A/B/C — application flexibility | Early stage | Eliminates application-specific hardware fragmentation |

The Next Inflection

Smart dosimetry — AI-driven real-time UV dose management — will convert UV LED from a hardware sale into a subscription service. The company that packages UV-C hardware + IoT sensors + compliance reporting into a Sterilisation-as-a-Service model unlocks hospital and food processing procurement budgets that capex models cannot reach. That company does not yet exist in Europe. It will by 2026.

Europe UV LED Market White Spaces & Untapped Growth Opportunities

White Spaces & Uncontested Growth Opportunities

| White Space | 2032 EUR Opportunity | Current Status | First-Mover Window |

| Residential air & water UV-C | EUR 100–130 Mn | Fragmented; near-zero UV LED penetration | 2025–2027 |

| Agriculture UV-B (greenhouse) | EUR 60–80 Mn | Near-zero commercial adoption; no dominant product | ~18 months remaining |

| Smart building HVAC UV-C | EUR 80–100 Mn | Pilot stage; no scaled EU solution | 2025–2026 |

| Municipal water treatment | EUR 60–80 Mn | Mercury dominant; compliance gap widening | 2025–2026 tender cycle |

| Pharma cleanroom validated swap | EUR 40–50 Mn | Mercury legacy; reluctant to revalidate | 2026–2028 |

| Sterilisation-as-a-Service (SaaS) | EUR 120–150 Mn recurring | Does not exist at commercial scale in Europe | 2025–2027 |

The Blind Spot — Agriculture UV

UV-B LED application in controlled-environment agriculture is the most underpublicised opportunity in Europe's UV LED market. Studies confirm 15–30% yield improvement in tomatoes, lettuce, and leafy vegetables with precise UV-B dosing. The Netherlands alone has over 10,000 hectares of commercial greenhouse capacity. No single supplier has built a purpose-designed product for this vertical. The market is free — for approximately 18 more months.

Europe UV LED Market Pricing & Cost Structure Analysis

The pricing architecture of UV LED systems in Europe is undergoing structural compression driven by scale economics, semiconductor yield improvements, and increasing competition from Asian component manufacturers. However, system-level pricing remains resilient due to integration complexity and application-specific validation requirements.

Average Pricing Benchmarks (2025):

• UV-C LED Component Price: EUR 8–15 per unit (mid-power range)

• UV System Integration Cost: EUR 120–350 per module depending on application

• Industrial UV Curing Systems: EUR 8,000–25,000 per installation

• Municipal UV LED Reactor Systems: EUR 50,000–300,000 depending on flow capacity

Cost Structure Breakdown:

• Semiconductor Materials (GaN, AlGaN): 35–45%

• Manufacturing & Packaging: 20–25%

• Thermal Management Systems: 10–15%

• Electronics & Drivers: 10–12%

• Integration & Validation: 10–18%

Pricing Insights

While component-level pricing is declining at ~8–12% annually, system-level pricing remains stable due to regulatory validation requirements and application engineering complexity. This creates a margin shift from component manufacturers to system integrators.

Europe UV LED Market Competitive Landscape & Strategic Positioning

Market Concentration & Competitive Structure

The Europe UV LED market in 2025 operates as a moderately fragmented competitive landscape, transitioning rapidly toward consolidation. The top 5 players — Heraeus Holding, Signify (Philips UV-C), OSRAM Opto Semiconductors, Seoul Viosys, and Nichia Corporation — collectively account for an estimated 42–47% of European market revenue, with the remaining share distributed across 30+ regional specialists, Asian component OEMs, and application-specific niche players. This fragmentation is not structural permanence — it is a consolidation window. Analysts project the competitive field will narrow to 5–7 dominant full-stack players by 2028, as the market's centre of gravity shifts from component supply to system integration, dosimetry IP, and service-contract architecture. Companies that fail to verticalise before 2027 will face binary outcomes: acquisition or margin compression below viable operating thresholds.

Europe UV LED Market Scope: Inquire before buying

Competitive Risk Matrix

| Company | Core Strength | Primary Risk | Strategic Outlook (2025–2028) |

| Heraeus Holding | Vertical integration + UV chemistry IP | SME and residential market reach limited | Strong — most defensible European position in premium UV-C |

| Signify (Philips UV-C) | Scale + brand + distribution | Execution lag; mercury cannibilisation trough | Cautiously positive — distribution advantage durable if execution improves |

| OSRAM Opto Semiconductors | Fab depth + automotive-grade process | Component margin compression from Asian cost pressure | Positive if licensing and partnerships deepen; exposed if pure component |

| Seoul Viosys | UV-C performance + aggressive pricing | Margin sustainability at scale; brand perception in premium healthcare | Strong momentum — will reach ~15% EU UV-C share by 2027 |

| Nichia Corporation | Patent portfolio depth | Limited system integration; premium-only positioning | Stable — IP moat durable but upside constrained to component tier |

| sglux GmbH | UV measurement precision | Scale limitations; acquisition target | Highly defensible niche — probable acquisition by 2027 at significant premium |

| Xylem (Wedeco) | Municipal water treatment installed base | Mercury transition pace slower than hospital sector | Positive — EU Water Directive compliance will accelerate tender flow |

Likely Winners:

• Companies with system integration + dosimetry IP

• Players building service-based UV models (SaaS — Sterilisation-as-a-Service)

• Firms with strong healthcare and municipal validation

At Risk:

• Pure component manufacturers without integration capability

• Players dependent on price-led competition

• Companies without regulatory alignment strategy

The competitive battlefield is no longer component efficiency — it is outcome certainty and compliance delivery.

M&A Activity & Consolidation Signals

The European UV LED competitive landscape is entering its consolidation phase, marked by several structural signals visible in 2024–2025:

• Heraeus's 2022 system integration acquisition established the vertical integration playbook that competitors are now compelled to follow or partner around

• EU Horizon Europe directing EUR 45 Million+ toward UV LED water treatment R&D is shaping the next generation of IP ownership — companies participating in consortium R&D are building licensing positions that will matter commercially by 2027–2028

• Baldwin Technology + Phoseon strategic partnership confirmed that the industrial curing market has accepted that UV LED systems are sold at the press-line integration level, not as lamp replacements — a business model shift with permanent margin implications

• AMS-OSRAM merger integration is creating a broader UV sensor and emitter portfolio that positions the combined entity to compete in application segments neither company could address independently

The acquisition targets most likely to transact before 2028 are companies with unique dosimetry IP, validated healthcare procurement positions, or category-defining positions in underpenetrated verticals — sglux GmbH, UV-Technik, and any early mover establishing the Agriculture UV-B category are considered the most probable targets by MMR analysts.

Europe UV LED Market Recent Developments

The Europe UV LED market witnessed an accelerated pace of strategic activity between 2024 and 2025 — spanning product launches, technology breakthroughs, cross-sector partnerships, regulatory updates, and manufacturing capacity expansions. The overarching pattern is clear: the industry is moving decisively from component-level competition toward system-integration, application-validation, and service-architecture models. The developments catalogued below represent the competitive signals shaping the market through 2032.

Summary Table — Key Recent Developments (2024–2025)

| Date | Company | Development Type | Detail | European Impact |

| March 2024 | Nichia Corporation | Product Launch | UV-B 308 nm + UV-A 330 nm LEDs — mass production, 434 Series | Phototherapy + agriculture UV-B markets opened |

| April 2024 | Crystal IS × Amway | Partnership | eSpring Water System — UVC LED point-of-use water treatment | Consumer residential UV-C market proof point |

| May 2024 | Luminus Inc. | Product Launch | SST-08-UV High-Power UV-A LED (365/385/395/405 nm) | Multi-application OEM component supply for EU manufacturers |

| May–Jun 2024 | Silanna UV | Product Launch | 235 nm Far-UVC Quad High-Power LED — ICFUST 2024, Scotland | Far-UVC occupied-space disinfection technology advance |

| October 2024 | ams-OSRAM | Product Launch | OSLON UV 3535 — 115 mW at 265 nm, 20,000-hr life | Healthcare + municipal water reliability milestone |

| October 2024 | NS Nanotech | Technology | First solid-state far-UVC semiconductor — human-safe disinfection | Occupied-space disinfection roadmap advance |

| February 2025 | ams-OSRAM | Financial | Q4 2024: EUR 882 Mn revenue; FCF guidance >EUR 100 Mn 2025 | Confirms UV LED capital commitment at Regensburg fab |

| March 2025 | AquiSense Technologies | Partnership/Pilot | Norwegian municipal water UV-C LED reactor validation pilot | EUR 50–70 Mn municipal water market — reference data building |

| May 2025 | Kyocera | Product Launch | G7A Series Air-Cooled UV LED — 300 mJ/cm², industrial curing | Industrial curing competition intensifies against Phoseon, ITL |

| 2024 (full year) | Seoul Viosys | Market Share | Global No.1 UV LED for 6th consecutive year (TrendForce 2025) | European UV-C mid-market share estimated ~11–13% |

| 2025 | Seoul Semiconductor | Legal/IP | UPC Europe patent win — WICOP No-Wire technology | Strengthens Seoul Viosys commercial position in EU OEM supply |

| 2024–2025 | EU Regulatory | Policy | RoHS mercury phase-out post-2027 confirmed; Minamata alignment | Structural demand floor — mercury replacement non-deferrable |

| 2024–2025 | EU Regulatory | Policy | EU Drinking Water Directive 2021/2115 — implementation accelerating | Eastern Europe tender wave 2025–2027 |

| 2024–2025 | EU Horizon Europe | R&D Funding | EUR 45 Mn+ UV LED water treatment R&D — active 2024–2028 | IP landscape shaping; consortium participants gain procurement advantage |

| 2025 | Multiple | Technology | GaN-on-SiC 100 mW prototypes; EQE 9.19% milestone | High-power UV-C reactor retrofit unlocked for mercury bank replacement |

Analyst View

Gaurav Deshmukh | Lead Analyst — Industrial Technology & Energy Transition | Maximize Market Research

"The UV LED competitive landscape will consolidate to 5–7 dominant players by 2027. The filter is simple: those who deliver application-validated, dosimetry-certified, service-backed UV systems will win healthcare and municipal procurement. Those who supply only components will be marginalised to Asian OEM supply chains where margin is already below 8%. European players have a 24-month window to verticalise before that window closes permanently."

Impact — Investors should weight European UV LED exposure toward system integrators and wavelength-IP holders — the component margin compression is structural, not cyclical, and is already underway.

Strategic Takeaway of Europe UV LED Market

• Demand is regulation-locked — EU mercury phase-out makes UV LED adoption mandatory on every industrial refresh cycle, not merely desirable

• UV-C is the structurally protected segment — irreplaceable disinfection physics creates a permanent moat against substitution

• The TCO argument is already won — the 40–60% 5-year cost advantage is documented; the remaining barrier is capex financing architecture

• Residential and agriculture are the largest undercaptured markets — combined EUR 120–160 Mn opportunity with near-zero current UV LED penetration

• Competitive advantage is migrating from component performance to system integration depth, dosimetry IP, and service contract architecture

• Eastern Europe at 28%+ CAGR is the highest-velocity emerging theatre — critically underindexed in current supplier strategies

The Central Thesis

The Europe UV LED market is not a lighting upgrade. It is the systematic dismantling of a toxic, non-compliant, energy-inefficient technology and its replacement by a solid-state photon system that is safer, more precise, and cheaper to operate over any meaningful time horizon. The only variable is speed of adoption — and in Europe, that speed is now determined by regulation, not buyer preference. The market will grow. The only question worth asking is: who owns the margin when it does?

Frequently Asked Questions for Europe UV LED Market

Q1. What is the Europe UV LED Market size in 2025?

The Europe UV LED Market is valued at USD 215.3 Million in 2025 and is projected to reach USD 1,048.6 Million by 2032, at a CAGR of 25.4%.

Q2. What is the CAGR of the Europe UV LED Market (2025–2032)?

The market grows at a CAGR of 25.4% from 2025 to 2032 — one of Europe's highest-growth industrial technology sectors.

Q3. Which technology segment dominates?

UV-C (200–280 nm) dominates with ~52% revenue share (USD 111.9 Mn in 2025), projected USD 558.2 Mn by 2032.

Q4. Which application has the highest growth rate?

Disinfection & Sterilisation is the fastest-growing application at ~26.2% CAGR, driven by healthcare mandates, EU water compliance, and Sterilisation-as-a-Service (SaaS) models.

Q5. Which country leads and which is growing fastest?

Germany leads with ~27% share (USD 58.1 Mn, 2025). Eastern Europe is fastest-growing at ~28%+ CAGR driven by EU compliance deadlines and industrial modernisation.

Q6. What is the TCO advantage of UV LED?

40–60% lower total cost of ownership over 5 years vs mercury — including energy savings (50–70% reduction), extended replacement cycles (10–20× longer lifespan), and hazardous waste disposal costs.

Q7. Who are the 38 key players profiled?

Heraeus Holding, Signify (Philips UV-C), OSRAM Opto Semiconductors, AMS-OSRAM, Lumileds, Seoul Viosys, Nichia Corporation, LG Innotek, Crystal IS, Nikkiso, SETi, sglux, Schott, Halma, Thorlabs, Ushio Europe, Phoseon Technology, Baldwin Technology, ITL, Nordson, Miltec UV, Xylem (Wedeco), Trojan Technologies, Atlantic Ultraviolet, ProMinent, Steril-Aire, Aquisense, Daavlin, Schulze & Böhm, Herbert Waldmann, Kernel, RayVio, Violumas, Excelitas, Würth Elektronik, UV-Technik, Stanley Electric, Luminus Devices.

Q8. What is the most underpenetrated opportunity?

Agriculture UV-B — Netherlands greenhouse sector (10,500+ ha); 15–30% documented crop yield uplift; no purpose-designed commercial product exists; EUR 60–80 Mn opportunity with ~18-month first-mover window.

Q9. What is Sterilisation-as-a-Service?

UV-C hardware + IoT dosimetry sensors + real-time compliance reporting bundled as a subscription (billed per m²/month). Unlocks hospital and food processing procurement budgets unreachable by capex models. No dominant European provider as of 2025. Commercial-scale deployment expected 2026–2027

Europe UV LED Market Key Players

Tier 1 — European System Integrators & Full-Stack UV LED Leaders

| Sr. No. | Company | HQ | Primary Segment | Core Strength |

| 1 | Heraeus Holding GmbH | Hanau, Germany | Healthcare + Industrial curing | Precision UV chemistry, vertical integration, quartz glass IP |

| 2 | Signify N.V. (Philips UV-C) | Eindhoven, Netherlands | Healthcare + Commercial disinfection | Scale, brand trust, Trulifi UV-C platform, EU distribution |

| 3 | OSRAM Opto Semiconductors GmbH | Regensburg, Germany | Industrial + Automotive + Sensing | Regensburg fab depth, component IP, automotive-grade UV LED |

| 4 | Lumileds Holding B.V. | San Jose CA / EU | Industrial curing + Automotive | High-power UV LED modules, automotive heritage, global OEM supply |

| 5 | AMS-OSRAM AG | Premstätten, Austria | Sensing + Industrial | UV sensor and emitter portfolio; spectral precision |

Tier 2 — Asian Component Manufacturers with Strong EU Presence

| Sr. No. | Company | HQ | Primary Segment | Core Strength |

| 6 | Nichia Corporation | Tokushima, Japan | UV-A + UV-C premium | World's deepest UV LED patent portfolio; blue and UV pioneer |

| 7 | Seoul Viosys Co., Ltd. | Ansan, South Korea | Disinfection + Water treatment | Violeds® UV-C technology; aggressive EU pricing |

| 8 | LG Innotek Co., Ltd. | Seoul, South Korea | Mid-market curing + Disinfection | Cost leadership, module volume, supply chain scale |

| 9 | Stanley Electric Co., Ltd. | Tokyo, Japan | Automotive + Industrial | UV LED components; automotive lighting crossover |

| 10 | Nikkiso Co., Ltd. | Tokyo, Japan | Pharma + Water treatment + Research | Deep UV LED precision (222–280 nm) |

| 11 | Crystal IS (Asahi Kasei) | Green Island NY / EU | Water treatment + Pharma cleanrooms | AlN-substrate UV-C LEDs — highest output below 265 nm commercially |

| 12 | SETi — Sensor Electronic Technology | Columbia SC / EU OEM | Disinfection components | Pioneer deep UV-C LED; OEM supply backbone for EU system integrators |

| 13 | Luminus Devices Inc. | Sunnyvale CA / EU | OEM component supply | High-power UV LED chips for curing and disinfection OEMs |

Tier 3 — European Niche Technology & Application Specialists

| Sr. No. | Company | HQ | Primary Segment | Core Strength |

| 14 | sglux GmbH | Berlin, Germany | Sensing + Dosimetry + Compliance | Ultra-precise UV photodetectors; indispensable for SaaS dosimetry |

| 15 | UV-Technik Speziallampen GmbH | Wörth am Rhein, Germany | Industrial + Water treatment | UV system engineering; mercury replacement consultancy |

| 16 | Schott AG | Mainz, Germany | Component — optical elements | UV-transmitting specialty glass and quartz optics for UV systems |

| 17 | Halma Plc | Amersham, UK | Healthcare + Industrial safety | UV sensing + safety systems portfolio; UV-C compliance dosimetry |

| 18 | Thorlabs, Inc. | Newton NJ / EU | Research + Sensing + Metrology | Precision photonics instruments; UV LED light sources for R&D |

| 19 | Ushio Europe B.V. | Tilburg, Netherlands | Industrial curing + Medical | UV lamp + LED transition products for printing and medical verticals |

| 20 | Excelitas Technologies | Waltham MA / Rosenheim, Germany | Sensing + Curing + Medical | UV lamp and LED hybrid solutions for industrial and medical applications |

| 21 | Würth Elektronik GmbH | Waldenburg, Germany | Industrial OEM supply | UV LED component distribution + application engineering for German Mittelstand |

Tier 4 — UV Curing Systems Specialists

| Sr. No. | Company | HQ | Primary Segment | Core Strength |

| 22 | Phoseon Technology | Hillsboro OR / EU | Industrial UV curing | UV LED curing systems — printing, coating, converting |

| 23 | Baldwin Technology Company, Inc. | Shelton CT / EU | Commercial printing + Packaging | UV LED printing press integration; strategic partnership with Phoseon |

| 24 | Integration Technology Ltd. (ITL) | Oxfordshire, UK | Industrial curing | UV LED curing lamp systems for web printing, coatings, and converting |

| 25 | Nordson Corporation | Westlake OH / EU | Electronics + Medical devices | UV curing dispensing and adhesive assembly systems |

| 26 | Miltec UV International | Millersville MD / EU | Industrial UV curing | High-intensity UV LED curing systems for web-converting applications |

Tier 5 — Water Treatment & Environmental UV Specialists

| Sr. No. | Company | HQ | Primary Segment | Core Strength |

| 27 | Xylem Inc. — Wedeco brand | Herford, Germany | Municipal water + Wastewater | Europe's largest UV water treatment installed base; mercury→LED transition |

| 28 | Trojan Technologies (Danaher) | London, Ontario / EU | Municipal water treatment | High-capacity UV flow-through reactors; dominant UK and Benelux municipal tenders |

| 29 | Atlantic Ultraviolet Corporation | Hauppauge NY / EU | Food processing + Water | UV water and air purification for food and beverage industry |

| 30 | Steril-Aire Inc. | Burbank CA / EU | Commercial HVAC + Hospitals | UV-C HVAC coil disinfection — building air quality and energy efficiency |

| 31 | ProMinent GmbH | Heidelberg, Germany | Industrial water + Municipal | UV disinfection integrated into dosing and water treatment systems |

| 32 | Aquisense Technologies | Lexington KY / EU | Water treatment OEM | PearlAqua UV-C LED reactor — compact point-of-use water disinfection |

Tier 6 — Medical Phototherapy Companies

| Sr. No. | Company | HQ | Primary Segment | Core Strength |

| 33 | Daavlin Company | Bryan OH / EU distribution | Dermatology + NHS | Narrowband UV-B phototherapy systems (311 nm); NHS and GKV approved |

| 34 | Schulze & Böhm GmbH | Germany | Dermatology clinics | UV phototherapy equipment; strong German clinical network |

| 35 | Herbert Waldmann GmbH & Co. KG | Villingen-Schwenningen, Germany | Medical + Workplace | Medical UV phototherapy + workplace light therapy; CE-marked under EU MDR |

| 36 | Kernel (formerly Lifelight) | Netherlands | Dermatology wearable | Next-generation UV-B wearable phototherapy — emerging segment pioneer |

Tier 7 — Emerging & Regional Challengers

| Sr. No. | Company | HQ | Primary Segment | Core Strength |

| 37 | RayVio Corporation | Fremont CA / EU OEM | Disinfection modules | UV-C LED arrays for water and surface disinfection OEM integration |

| 38 | Violumas | USA / EU | UV-C air + HVAC | UV-C LED modules targeting HVAC OEM embedded supply agreements |

Lead Analyst — Europe UV LED & Advanced Photonics Markets

This research is authored by analysts with deep expertise in UV LED photonics economics, European regulatory compliance architecture (RoHS, EU Green Deal, REACH), semiconductor technology market modelling, and application-specific industrial market dynamics — advising UV LED manufacturers, system integrators, healthcare procurement divisions, and institutional investors across Germany, UK, France, and Benelux.

Core competencies: UV photobiology · Semiconductor market modelling · European compliance architecture · Industrial disinfection economics · Technology substitution forecasting · Wavelength-application mapping

Segmentation Coverage — Europe UV LED Market

| Segment | Sub-segments |

| By Technology | UV-A (315–400 nm) · UV-B (280–315 nm) · UV-C (200–280 nm) |

| By Industry Vertical | Healthcare & Medical · Industrial · Commercial · Agriculture · Residential |

| By Application | UV Curing · Disinfection & Sterilisation · Medical Light Therapy · Optical Sensing · Counterfeit Detection · Others |

| By Region | NA | Europe | APAC | MEA | LATAM |