Electronic navigational charts market- Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning / Landscape Review & Global Market Size Forecast to 2032

Overview

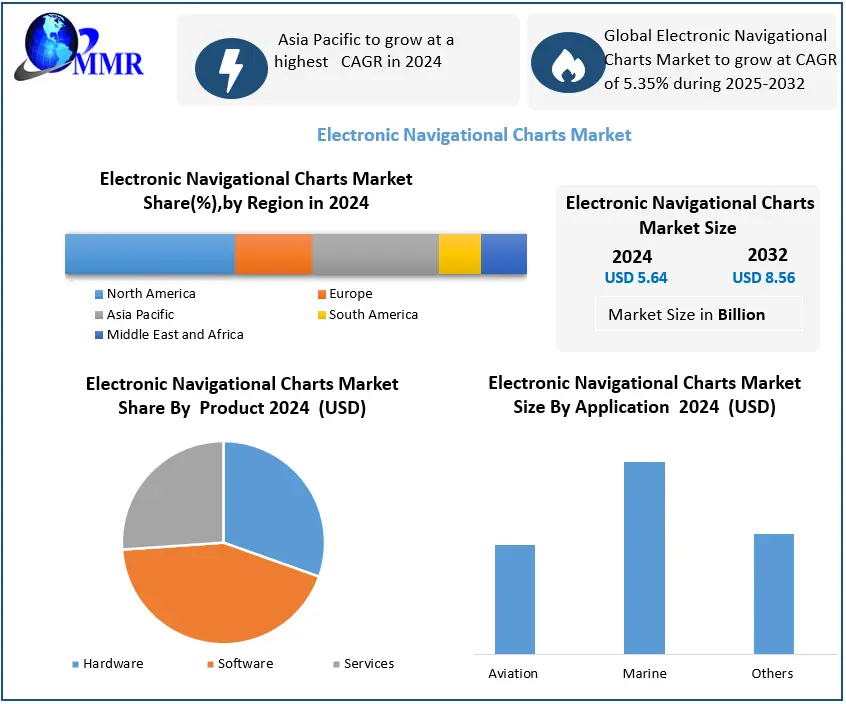

Electronic Navigational Charts Market was valued at USD 5.64 Bn. in 2024 and the total Global Electronic Navigational Charts Market revenue is Expected to grow at a CAGR of 5.35% from 2025 to 2032 reaching nearly USD 8.56 Bn. by 2032.

Electronic Navigational Charts Market Overview:

Electronic navigational maps are compliant with International Hydrographic Organization (IHO) S57 standards. ECDIS (Electronic Map Display and Information System) manufacturers use the IHO S57 standard to display navigational data on maps. Raster or paper maps are far preferable to computer navigational charts. Systems that use ENCs can be designed to provide information about an approaching danger in relation to mapped information and the movement and position of a ship.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Electronic Navigational Charts Market Dynamics:

The International Maritime Organization’s (IMO) safety criteria, the growth in the movement towards safe navigation systems & the expansion of the maritime and aircraft industries worldwide are expected to fuel the global demand for electronic navigation charts in forecast period. The paper catalogue is replaced by a digital catalogue (many of which are available), the order is sent by e-mail, & a license for the ENCs is sent by e-mail to the map distributor.

Rise in Maritime Safety System:

The increasing need to manage complicated supply chain operations, improve sustainability across the marine industry, increase trade & freight transport activities through the sea, increasing need to raise awareness about maritime safety & regulatory compliances & standards are the main factors propelling the growth of the maritime safety market. Additionally, the development of integrated solutions to reduce maritime terrorism & piracy, as well as emerging opportunities across untapped regional markets, are expected to present opportunities for businesses operating in the maritime safety market. These innovative technologies include RFID, GPS, AR, robotics, & Blockchain.

However, there are restraints that could impede the market's growth for marine safety. The marine industry is facing a number of challenges, such as strict environmental rules & compliance concerns, a lack of common standards for implementing security solutions, & an increase in criminal activity. In addition to these limitations, merchants are expected to face a number of other difficulties in the near future. These would include escalating piracy problems, rising maritime terrorism, a shortage of workers, & a suspension of production during the epidemic. A global health & economic catastrophe brought on by the COVID-19 coronavirus had far-reaching effects on marine trade & transportation. Ports, shipping, and supply chains have been affected by the pandemic-related restrictions, which were put in place. There were difficulties in many industries' supply chains.

Raw material limitations, lead-time issues, ocean blank sailings, port closures, shortened port hours, equipment and manpower shortages, and transportation capacity restrictions were a few of these difficulties. These impediments seriously damage transportation services and threaten the efficiency of supply chain operations and trade flows. Governments have circulated circulars and other types of communication regarding COVID-19 to both flag states and port states.

The maritime industry has released a number of port marine circulars connected to COVID-19 in a number of nations and areas. Following feedback from the industry & unions, it established a prescribed process after initially announcing that crew changes were suspended. This process takes into account whether the seafarer has served the maximum amount of time on board and no further extensions of the employment contract are granted by the flag state. The long-term impact of the COVID-19 is yet to be fully understood. All signs point to the maritime industry facing major hurdles right away. Depending on the maritime transport sector, they vary (e.g., container, bulk, reefer, tanker). These indicators vary by geography, degree of development, & level of preceding shock and disruption preparedness. Globally, the COVID-19 epidemic has produced an unheard-of condition. Governments all across the world have imposed travel restrictions and closed borders to stop the disease's spread & diminish its effects. Ports and airports all over the world have closed, ships have been turned away, and planes have been grounded. Approximately 90% of world trade is transported by sea. One of the main sources of food in the globe is commercial fishing. There are many seamen aboard for extended periods of time. Crews must therefore frequently change in order to prevent tiredness. Every month, this affects some 100,000 mariners. Around 90,000 seamen are currently stranded aboard cruise ships without passengers and occasionally even without pay due to COVID-19-related regulations. Both sailors & ship owners have benefited from the Maritime Labor Convention of 2006, which has shown to be a reliable & useful tool during this pandemic.

Licensing practices:

The bonus of ENCs is that they are usually already on board the CDs that contain the ENCs. When the license is released, the ship will then load the charts from the CDs onto the ECDIS, removing the need to send physically any merchandise. Via M&A operations, several businesses are attempting to enter the domain of electronic navigational maps. In the year 2017, for example, Garmin Ltd. purchased Navionics S.P.A., the Italian electronic navigation charts firm. In addition, the demand for instruction in electronic navigational charts is likely to impede the development of the market for electronic navigational charts. Shipping businesses face difficulties in the use of ECDIS when teaching crew. There are choices for pursuing a general or type-specific ECDIS training plan.

In purchasing & licensing practices, though the crew still needs to be qualified. The management of a digital catalogue, the preparation of a trip, the assessment of license conditions and the loading of ECDIS licenses require training in their own right. Owing to the numerous distinct forms of catalogue applications in operation, all with their own user interface and peculiarities, this is particularly true. The IMO approves ENCs as a paper-chart counterpart. Furthermore, according to the IMO, as is usually necessary under the Protection of Life at Sea (SOLAS) Convention, warships and ships fitted with ENCs do not need to hold paper maps. The contract fee is calculated on the basis of the contract duration, the number of units and the forms of ENCs for electronic navigational charts.

Marine Technology Trends by the end of 2030:

The development of technology is accelerating & will do so in the future. There is no sign that it will slow down in the next 15 years, nor is there any indication that the trend toward more tightly related technology applications will change. Despite how widespread the technological revolution is, the commercial maritime, navy, & ocean space sectors will experience it differently.

In the marine industry, both individually & collectively, big data analytics, advanced materials, autonomous systems, advanced manufacturing, energy management, cyber & electronic warfare, human-computer interaction &human augmentation technologies are transformational. Utilizing these technologies will improve a navy's capacity to project military force, which is directly reliant on gaining access to the full spectrum of battle space, including cyberspace & on having the ability to coerce, deter, and intervene in its war fighting role to safeguard national interests. The ability of a navy to safeguard a country's population, territory, & trade against terrorism, crime, piracy, state-sponsored insurgency, & unlawful limitations on freedom of navigation will also be improved by these technology.

Big data analytics, cutting-edge materials, autonomous systems, sensors, & communication, sustainable energy production, carbon capture & storage, marine biotechnology, & deep ocean mining are all transformational in nature when used separately or in combination in the ocean space sector. These technologies will offer a thorough understanding of the ocean environment, which might be utilised to solve issues like climate change, the depletion of land-based resources, & population growth. These technologies can make it simple to defend residents of coastal areas against powerful natural forces like storms &s tsunamis.

Electronic Navigational Charts Market Segment Analysis

Based on Component Electronic Navigational Charts Market is segmented into Hardware, Software and Services. Software Segment Dominated the market in 2024 and is expected to hold largest share during the forecast period. Dominance due to software segment leads the ENC market as shipping companies increasingly adopt digital navigation, route optimization, and compliance solutions. Regulatory mandates like IMO’s ECDIS requirement accelerate demand for software-based chart systems over traditional hardware. Continuous updates, real-time data integration, and lower operational costs make software the most critical and revenue-generating component.

Based on Application Electronic Navigational Charts Market is segmented into Aviation, Marine and Others. Marine segment dominated the market in 2024 and is expected to hold largest share during the forecast period. Dominance due to IMO and SOLAS regulations mandate the use of ECDIS on commercial vessels, driving large-scale adoption in shipping and naval operations. Rising global seaborne trade, port expansion, and demand for safe, efficient navigation further strengthen Marine’s leading position over aviation and others.

Asia-Pacific Aviation Sector Set To Boom:

The market's growth is ascribed to a number of factors, including rising disposable incomes, more air travel, the growth of the tourism sector, & growing global trade. Players in the aerospace avionics industry are being further encouraged to expand their avionics portfolios by the growth in aircraft deliveries to address the accelerating air passenger traffic. The industry share will be supported by the implementation of cutting-edge technologies like the Internet of Things (IoT) and connected cabin technologies, which will provide clients with individualized travel experiences. In the year 2018, the flight management system accounted for a significant 19% of the market for aerospace avionics. Numerous advantages of the flight management system include shorter flight routes that result in less fuel being consumed & more operating capabilities. The development of new open architecture for avionics, which will support the industry scale over the future years, is a top priority for major producers of avionics systems. A surge in air passenger traffic is being caused by a number of regional government laws that assist the improvement of passenger safety.

By the end of 2025, it is expected that the commercial aviation segment would hold a significant share of the Aerospace Avionics market, accounting for more than 55% of total market revenue, as a result of the increased need for commercial aircraft to serve the region's growing business travel & international tourist sectors. Government agencies in the area are putting their efforts into building infrastructure, initiating helpful initiatives, and collaborating with private airlines to provide customers with sustainable & inexpensive air connectivity, helping the commercial aviation market. For instance, in order to make flying more accessible to citizens, the Ministry of Civil Aviation, Government of India, announced the National Civil Aviation Policy (NCAP) in June 2016. The Indian ministry also released updated RDG route categorization, which went into effect at the end of 2017.

In the year 2023, China held a market share of over 30%. The fastest developing economy in the area is to blame for the country's rising industry. In order to meet the growing need for avionics, the region's aircraft operators are calling for improved avionics and communication systems. For instance, in December 2019, Boeing established its first 737 assembly factory in China, putting an end to the trade spat between the two countries and creating new market opportunities.

Electronic Navigational Charts Market Regional Overview:

Due to the growth of the marine industry, an improvement in the safety of navigational systems, & the existence of well-established businesses offering electronic navigational charts, North America and Europe are anticipated to dominate the market for electronic navigational charts. Additionally, the market for electronic navigational charts in Asia Pacific is expected to grow over the projected period of 2023 to 2029 due to an increase in demand for electronic navigational charts for ships & aircraft.

The report's objective is to provide industry stakeholders with a thorough insight of the global IPTV Market. The research analyses complex data in plain terms & shows the historical & current state of the industry together with predicted market size & trends. The analysis analyses important companies, including market leaders, followers, and new entries, in detail and covers all areas of the industry. The research includes a PORTER, PESTEL analysis with the probable influence of market micro-economic aspects. Analysis of both internal & external variables that are thought to have an impact on the company either favourably or unfavorably has been done in order to provide decision-makers with a clear futuristic vision of the sector.

The reports also help in understanding the Electronic Navigational Charts Market dynamic, and structure by analyzing the market segments and projecting the Electronic Navigational Charts Market size. Clear representation of competitive analysis of key players by Design, price, financial position, Component portfolio, growth strategies, and regional presence in the Electronic Navigational Charts Market make the report investor’s guide.

Electronic Navigational Charts Market Scope: Inquire before buying

| Global Electronic Navigational Charts Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 5.64 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 5.35% | Market Size in 2032: | USD 8.56 Bn. |

| Segments Covered: | by Component | Hardware Software Services |

|

| by Chart Form | Raster Navigational Charts (RNCs) Vector Navigational Charts (VNCs) |

||

| by Application | Aviation Marine Others |

||

| by Distribution Channel | Commercial Shipping Defence/ Military Recreational Boating |

||

Electronic Navigational Charts Market, by Region:

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America

Electronic Navigational Charts Market, Key Players:

1. Electronic Charts Company, Inc.

2. ChartCo Limited

3. Japan Hydrographic Charts & Publications Co., Ltd.

4. OceanWise

5. Poseidon Navigation Services Ltd

6. Maritime Services Ltd.

7. Sirm SPA

8. Jeppesen

9. SRH Marine Electronics S.A.

10. Maryland Nautical

11. American Nautical Services, Inc.

12. Fontanski Marine Supply

13. Nautisk Forlag AS.

14. Others.

Frequently Asked Questions:

1. What is the study period of the market?

Ans. The Global Electronic Navigational Charts Market is studied from 2025-2032.

2. What is the growth rate of Electronic Navigational Charts Market?

Ans. The Global Electronic Navigational Charts Market is growing at a CAGR of 5.35 % over forecast period.

3. Which region has largest share in The Global Electronic Navigational Charts Market?

Ans. North America holds the largest share.

4. What is the Global Electronic Navigational Charts Market segment based on Application?

Ans. Aviation, Marine, Others

5. Who are the key players in the Global Electronic Navigational Charts Market?

Ans. The key players in the Global Electronic Navigational Charts Market Are Electronic Charts Company, Inc., ChartCo Limited, Japan Hydrographic Charts & Publications Co., Ltd., OceanWise, Poseidon Navigation Services Ltd, Maritime Services Ltd., Sirm SPA, Jeppesen, SRH Marine Electronics S.A.,