Ducted Heat Pump Market Size by Product Type, Application, End-User, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2032

Overview

The Global Ducted Heat Pump Market size was valued at USD 14.31 Billion in 2024 and the total Ducted Heat Pump revenue is expected to grow at a CAGR of 7.4% from 2025 to 2032, reaching nearly USD 25.34 Billion.

Ducted heat pumps, a highly efficient heating and cooling solution, have gained increasing demand due to their ability to provide year-round comfort in residential and commercial spaces. These systems, which use a network of ducts to distribute conditioned air, offer several advantages. They are energy-efficient, reduce greenhouse gas emissions, and offer precise temperature control. The demand for ducted heat pumps has risen as they contribute to cost savings on energy bills and create a more environmentally friendly heating and cooling solution. Additionally, their ability to be integrated with existing ductwork makes them appealing for retrofits and new construction projects. The growing awareness of energy-efficient and sustainable HVAC solutions, coupled with supportive government policies, has further accelerated the adoption of ducted heat pumps in the quest for energy efficiency and reduced carbon footprint.

As a result, the ducted heat pump market is experiencing significant growth, driven by the ever-increasing demand for energy-efficient and environmentally friendly heating and cooling solutions. As the world grapples with the challenges of climate change, ducted heat pumps have emerged as a crucial player in the effort to reduce greenhouse gas emissions. Their energy-efficient operation not only leads to substantial cost savings for consumers but also aligns with global efforts to combat climate change.

The key factor contributing to the growth of the ducted heat pump market is its adaptability for both residential and commercial use. These systems provide year-round comfort, offering precise temperature control, making them a versatile choice for a wide range of applications. Moreover, their compatibility with existing ductwork makes them an attractive option for retrofitting older buildings and incorporating them into new construction projects.

Supportive government policies and incentives have played a pivotal role in propelling the adoption of ducted heat pumps. Various countries have introduced regulations promoting energy-efficient HVAC systems, which have created a favorable environment for the market's expansion. The ongoing shift towards sustainability and energy efficiency is expected to further boost the ducted heat pump market as consumers increasingly seek greener alternatives for their heating and cooling needs. As a result, the ducted heat pump market is set to thrive, providing both economic and environmental benefits to users across the globe. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Ducted Heat Pump Market Dynamics:

25 States Agree To Quadruple Number of Heat Pumps in America

The increasing adoption of heat pumps, particularly in the United States, is expected to be the major factor driving the ducted heat pump market growth. The US Climate Alliance, a coalition of 25 states that collectively represent a substantial portion of the US economy and population, has recently committed to promoting policies aimed at expediting the installation of heat pumps. This commitment is expected to have a substantial impact, with the goal of increasing the number of heat pump installations from the current 4.7 million to an impressive 20 million by the end of the decade. Heat pumps are gathering attention due to their role in decarbonizing heating and cooling systems. They operate in a highly efficient manner, offering a cleaner and more sustainable alternative to traditional furnaces and heating equipment that rely on fossil fuels. Notably, they significantly reduce greenhouse gas emissions, thereby contributing to the fight against climate change.

Name of The States That Are Agreed

| California | Hawaii | Michigan | New Mexico | Vermont |

| New York | Illinois | Minnesota | North Carolina | Virginia |

| Washington | Maine | Nevada | Oregon | Wisconsin |

| Connecticut | Maryland | Colorado | Pennsylvania | New Hampshire |

| Delaware | Massachusetts | New Jersey | Rhode Island | District of Columbia (Washington, D.C.) |

The improved effectiveness of heat pumps compared to traditional heating and cooling techniques is one of the major factors for their increased popularity. Heat pumps efficiently extract heat from the outdoor environment or the ground and transfer it indoors, using electricity for this process rather than burning fossil fuels. This results in substantial energy savings and a notable reduction in heating and cooling costs. In addition to their economic advantages, heat pumps enhance air quality by reducing fine particulate emissions associated with traditional heating methods. The reduced presence of fine particulates has a positive impact on health, potentially reducing mortality rates associated with air pollution.

While the upfront costs of heat pump installation can be higher, various financial incentives and tax credits are available to alleviate this financial burden. The realization that heat pumps are not only a sustainable choice but also a cost-effective one is encouraging their adoption among homeowners and businesses. As a result, the ducted heat pump market is experiencing substantial growth, driven by the transition to energy-efficient and eco-friendly heating and cooling solutions. This trend aligns with the broader commitment to reducing carbon emissions and building a more sustainable future.

Supportive Government Regulations For Accelerating The Global Adoption Of Energy-Efficient And Climate-Friendly Air Conditioners

The supportive government regulations aimed at accelerating the global adoption of energy-efficient and climate-friendly air conditioners are expected to be a pivotal factor driving the demand for ducted heat pumps and shaping the ducted heat pump market. The Model Regulation Guidelines advocate for such rules, that emphasize the need to transition to more sustainable cooling and heating solutions to meet rising energy demand in emerging and developing countries. With the expected tripling of energy consumption for space cooling by 2050 and a substantial rise in the number of air conditioners in these regions, the focus on improving energy efficiency and refrigerant choices becomes paramount.

Energy efficiency measures, including Minimum Energy Performance Standards (MEPS) and energy labels, are recognized as highly effective approaches to enhance the efficiency of cooling devices. However, many countries lack up-to-date or enforced standards, making them vulnerable to the influx of less efficient products. The impending changes in China's MEPS and labels are expected to have a global impact on the availability and affordability of energy-efficient air conditioners. Furthermore, the transition to refrigerants with lower global warming potential aligns with the Kigali Amendment to the Montreal Protocol, which aims to reduce hydrofluorocarbons (HFCs) and combat climate change. This phasedown of HFCs complements the efforts to improve energy efficiency, creating a more sustainable and environmentally friendly approach to cooling and heating.

The impact of various government regulations on the global adoption of energy-efficient and climate-friendly ducted heat pumps

| Government Regulation | Description | Impact on Adoption of Ducted Heat Pumps |

| Minimum Energy Performance Standards (MEPS) | Set energy efficiency requirements for ducted heat pumps. Drive the adoption of more energy-efficient ducted heat pumps by limiting options in the market. | Accelerate adoption by making energy-efficient ducted heat pumps the sole consumer choice. |

| Energy Efficiency Labels | Provide consumers with energy efficiency information, promoting informed purchasing decisions. Effective in increasing awareness and encouraging the purchase of efficient ducted heat pumps. | Accelerate adoption by guiding consumers towards energy-efficient choices. |

| Public Procurement Programs | Mandate government agencies to purchase energy-efficient ducted heat pumps, creating a market and reducing costs. Proven effective in the public sector. | Accelerate adoption by establishing a market and lowering product costs. |

| Financial Incentives | Encourage consumers and businesses to buy energy-efficient ducted heat pumps through rebates, tax credits, and low-interest loans. Effective in boosting adoption. | Accelerate adoption by making energy-efficient ducted heat pumps more affordable. |

| Information and Education Campaigns | Raise awareness and promote the benefits of energy-efficient ducted heat pumps. Effective in increasing adoption. | Accelerate adoption by enhancing awareness of product benefits. |

The guidelines serve as a foundational framework for countries to develop comprehensive regulations addressing both energy efficiency and refrigerant choices, striking a balance between ambitious performance standards and product availability. The global movement towards sustainable cooling solutions not only mitigates environmental impacts but also contributes to cost savings, air quality improvement, and energy efficiency, ultimately driving the demand for ducted heat pumps as part of this broader transition. Thus, this factor driving the ducted heat pump market growth.

Ducted Heat Pump Market Segment Analysis:

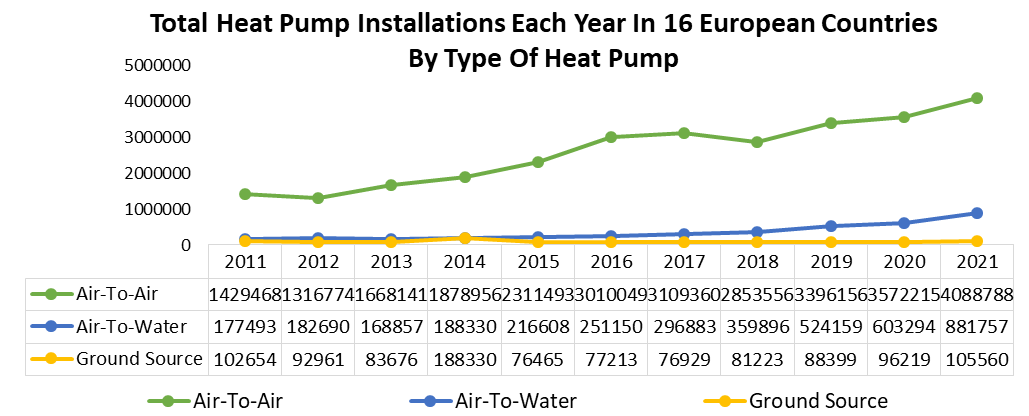

Based on the product type, the air source heat pump segment dominated the global ducted heat pump market with the highest revenue share of 43% in 2024. The segment is further expected to grow at a CAGR of 7.00% during the forecast period. The increasing demand for energy-efficient systems is expected to be the major factor driving the segment growth. The high demand for air-source heat pumps is significantly driving the growth of the ducted heat pump market. These air-source heat pumps, play a pivotal role in enhancing energy efficiency and sustainability in heating and cooling systems. Air-source heat pumps effectively collect heat from the external environment, often the outdoor air, and concentrate it for indoor use, making them a versatile and eco-friendly solution for climate control.

The unique energy efficiency of air-source heat pumps is one of the major factors leading to the increase in demand for products. In comparison to traditional electric resistance heating methods like furnaces and baseboard heaters, air-source heat pumps are expected to reduce electricity consumption for heating by approximately 50%. This substantial reduction in energy usage not only benefits homeowners and businesses by lowering utility bills but also aligns with the global push to reduce carbon emissions and combat climate change. Moreover, high-efficiency air-source heat pumps provide an additional advantage through improved dehumidification compared to standard central air conditioners. This leads to increased cooling comfort during the summer months while using less energy, further contributing to the overall energy efficiency of the system.

In the past, air-source heat pumps were primarily deployed in regions with milder climates, limiting their usage in areas prone to extended periods of subfreezing temperatures. However, recent advancements in air-source heat pump technology have expanded their capabilities. These innovations have transformed air-source heat pumps into a viable heating alternative even in colder regions, where they were previously underutilized.

This paradigm shift towards utilizing air-source heat pumps in colder climates has spurred their adoption and, by extension, drove the growth of the ducted heat pump market. As consumers and businesses increasingly recognize the benefits of these systems, the demand for ducted heat pump solutions, incorporating air-source technology, is on the rise. This trend is aligned with the broader mission of transitioning to more energy-efficient and environmentally sustainable heating and cooling solutions, ultimately contributing to the reduction of carbon footprints in the built environment. In light of these developments, the future of the ducted heat pump market, with a strong focus on air-source heat pumps, holds promise as a key player in the ongoing global effort to achieve greater energy efficiency and reduce the environmental impact of heating and cooling systems. However, Ground Source or Geothermal Heat Pump segment is expected to grow at a rapid CAGR of 7.84%. Geothermal heat pumps, also known as ground-source, have emerged as a highly attractive segment offering substantial growth opportunities for manufacturers in the ducted heat pump industry. These innovative systems are designed to achieve superior energy efficiency by facilitating the exchange of heat between a building and the stable, naturally occurring temperatures of the ground or nearby water sources. The exceptional efficiency of geothermal heat pumps, which results in significant energy savings, is expected to be the primary driver of this rising demand, thereby supporting the ducted heat pump market growth. While the initial installation costs may be higher compared to traditional heating and cooling systems, geothermal heat pumps offer lower operating costs. This is primarily due to their ability to tap into the consistent and relatively constant ground or water temperatures. By leveraging these stable thermal reservoirs, geothermal heat pumps effectively and efficiently heat and cool buildings, thereby significantly reducing energy consumption.

However, Ground Source or Geothermal Heat Pump segment is expected to grow at a rapid CAGR of 7.84%. Geothermal heat pumps, also known as ground-source, have emerged as a highly attractive segment offering substantial growth opportunities for manufacturers in the ducted heat pump industry. These innovative systems are designed to achieve superior energy efficiency by facilitating the exchange of heat between a building and the stable, naturally occurring temperatures of the ground or nearby water sources. The exceptional efficiency of geothermal heat pumps, which results in significant energy savings, is expected to be the primary driver of this rising demand, thereby supporting the ducted heat pump market growth. While the initial installation costs may be higher compared to traditional heating and cooling systems, geothermal heat pumps offer lower operating costs. This is primarily due to their ability to tap into the consistent and relatively constant ground or water temperatures. By leveraging these stable thermal reservoirs, geothermal heat pumps effectively and efficiently heat and cool buildings, thereby significantly reducing energy consumption.

Moreover, geothermal heat pumps bring an array of advantages to the table. They are known to reduce energy usage by an impressive 30% to 60%, making them a compelling choice for homeowners and businesses looking to cut down on utility bills and minimize their environmental footprint. Additionally, these systems excel in humidity control, ensuring a comfortable and healthy indoor environment. Their reputation for sturdiness and reliability further enhances their appeal, providing long-term cost-effective solutions for climate control. Geothermal heat pumps offer versatility, as they are integrated into a wide range of residential and commercial settings. However, the suitability of a geothermal system for a specific location depends on factors such as the size of the property, subsoil conditions, and the landscape.

An intriguing feature of geothermal heat pumps is their ability to operate effectively in a broader range of climates, including those with more extreme weather conditions. This adaptability makes them an attractive choice for regions that experience temperature extremes including the United States, Canada, Sweden, Norway, Finland, Iceland, Switzerland, New Zealand, Japan, etc. In addition, customer satisfaction with geothermal heat pump systems is notably high, reflecting their efficiency and reliability. As consumers become more environmentally conscious and look for ways to reduce energy consumption, the demand for geothermal heat pumps is on the rise. This escalating interest in geothermal technology is a driving force behind the growth of the ducted heat pump market, and manufacturers are well-positioned to capitalize on the lucrative opportunities it presents. The adoption of geothermal heat pumps aligns with the broader objective of promoting energy-efficient and eco-friendly heating and cooling solutions, ultimately contributing to a greener and more sustainable future in the built environment.

Ducted Heat Pump Market Regional Insights:

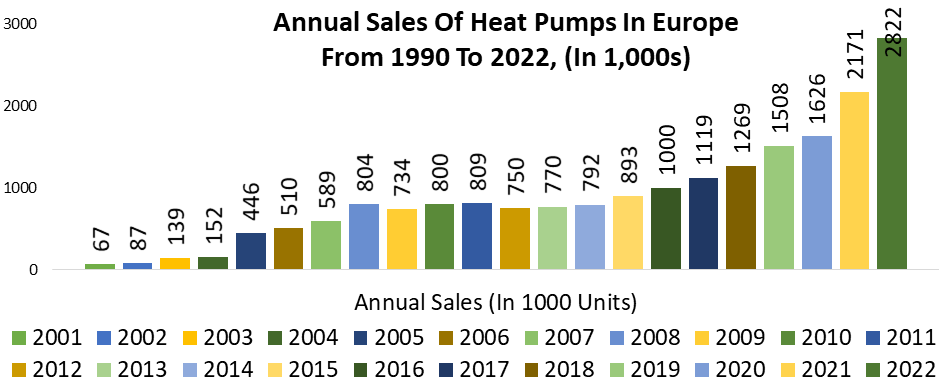

Europe held the highest market share of over 40% and led the global ducted heat pump market in 2024. The region is further expected to grow at a significant rate and maintain its dominance throughout the forecast period. In addition, Europe has emerged as a global leader in the transition to energy-efficient and sustainable heating systems. Ducted heat pumps have played a pivotal role in this transformation, with organizations like the International Energy Agency acknowledging their significance in decarbonizing heating and achieving net-zero emissions. According to the MMR analysis, the year 2024 witnessed a remarkable surge in heat pump adoption in Europe, with multiple factors contributing to this unprecedented growth.

Europe witnessed heat pump sales surpassing 3 million units for the first time, marking a notable 38% increase from the previous year in 2024. This surge is expected to be propelled by various factors, including an increased focus on energy efficiency, sustainability, and the mounting urgency to reduce carbon emissions. Government incentives and regulations, promoting the adoption of energy-efficient heating and cooling solutions, further fueled this demand for ducted heat pumps across the continent, thereby supporting the ducted heat pump market growth.

The economy of energy sources is one of the key drivers of Europe's ducted heat pump market’s rapid growth. Gas and oil prices experienced unprecedented spikes in 2024, tipping the balance in favor of heat pumps, which are known for their energy efficiency. Although electricity prices also saw an increase in various countries, the overall cost-effectiveness of heat pumps became evident to consumers and businesses alike. This cost advantage has been a pivotal factor in the accelerating adoption of ducted heat pump technology. Europe's commitment to energy-efficient solutions is highlighted by a rapid expansion of heat pump markets. The continent can be categorized into three segments: mature, emerging, and dormant heat pump markets. Mature markets, including the Nordic countries, Switzerland, and France, have long embraced heat pump technology, with steady growth patterns. Emerging markets, on the other hand, have experienced more recent and rapid adoption, with countries like Germany, Poland, and the Netherlands witnessing substantial increases in heat pump sales. Dormant markets, such as the UK, have shown signs of reawakening, further highlighting the region's overall momentum.

Europe's commitment to energy-efficient solutions is highlighted by a rapid expansion of heat pump markets. The continent can be categorized into three segments: mature, emerging, and dormant heat pump markets. Mature markets, including the Nordic countries, Switzerland, and France, have long embraced heat pump technology, with steady growth patterns. Emerging markets, on the other hand, have experienced more recent and rapid adoption, with countries like Germany, Poland, and the Netherlands witnessing substantial increases in heat pump sales. Dormant markets, such as the UK, have shown signs of reawakening, further highlighting the region's overall momentum.

Notably, 2022 saw robust growth across all these segments. Even in mature markets like Finland, heat pump sales surged by 50%, driven by government grants encouraging the replacement of oil-fired heating systems. Norway, already a leader in heat pump adoption, recorded a 25% increase in sales. Switzerland, with its carbon tax on heating fuels, saw a 23% growth rate. Sweden, which has maintained a carbon tax for decades, experienced an astonishing 61% growth in 2022. However, the most remarkable growth was observed in emerging markets. Belgium, the Czech Republic, and Poland led the way, with their heat pump markets doubling in a single year. Poland's impressive 120% growth is particularly noteworthy, surpassing even larger economies with more established markets.

| Country | Sales Of Heating Heat Pumps 2022 | Growth In Sales From 2021 To 2022

(% Of Additional Heat Pump Units Sold) |

Growth In Sales From 2021 To 2022

(No. Of Additional Heat Pump Units Sold) |

| Austria | 49,204 | +59% | 18,227 |

| Belgium | 32,965 | +66% | 13,121 |

| Czech | 60,065 | +99% | 29,886 |

| Denmark | 88,833 | +20% | +14,892 |

| Finland | 196,359 | +52% | +66,984 |

| France | 462,672 | +20% | +76,176 |

| Germany | 236,000 | +53% | +82,000 |

| Italy | 502,349 | +37% | +134,429 |

| Netherlands | 123,208 | +80% | +54,796 |

| Norway | 156,295 | +25% | +31,267 |

| Poland | 195,480 | +102% | +98,540 |

| Portugal | 29,969 | +17% | +4,357 |

| Sweden | 215,373 | +60% | +81,875 |

| Switzerland | 41,209 | +22% | +7,505 |

| Spain | 161,800 | +21% | +28,129 |

| UK | 59,862 | +40% | +17,103 |

The shift towards heat pumps is not confined to warmer regions; it is a continent-wide phenomenon. Finland, Norway, Sweden, and Estonia, with some of Europe's coldest winters, have some of the highest penetration rates for heat pumps. This dispels the myth that heat pumps are unsuitable for cold climates, as data shows that they continue to perform efficiently even in sub-zero temperatures. Looking ahead, high fossil fuel prices have made heat pumps an economically attractive choice, offering a cleaner and cost-effective alternative to traditional heating methods. The EU's Emission Trading System will further incentivize heat pump adoption, beginning in 2027. Many countries have announced plans to phase out fossil fuel heating, with potential EU-wide phaseout dates on the horizon. Novel policy instruments, like clean heat standards, are being discussed, which may play a pivotal role in scaling up Europe's heat pump market. Additionally, reforms to the EU Renewable Energy Directive are expected to provide further incentives for heat pump deployment, eventually supporting the ducted heat pump market during the forecast period.

Ducted Heat Pump Market Scope: Inquiry Before Buying

| Ducted Heat Pump Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 14.31 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 7.4% | Market Size in 2032: | USD 25.34 Bn. |

| Segments Covered: | by Product Type | Air Source Heat Pumps Ground Source/Geothermal Heat Pumps Water Source Heat Pumps |

|

| by Application | Heating Cooling Both heating and cooling |

||

| by End-User | Residential Commercial Others |

||

Ducted Heat Pump Market by Region:

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Ducted Heat Pump Market Key Players:

1. Carrier Global Corporation

2. Daikin Industries, Ltd.

3. Johnson Controls International Plc

4. United Technologies Corporation

5. Lennox International Inc.

6. Rheem Manufacturing Company

7. Goodman Global, Inc.

8. Amana Corporation

9. Bosch Thermotechnology GmbH

10. LG Electronics Inc.

11. Changhong Group

12. Skyworth Group Co., Ltd.

13. TCL Corporation

14. Haier Smart Home Co., Ltd.

15. Panasonic Corporation

16. Fujitsu General Limited

17. Hitachi Global Life Solutions, Inc.

18. Samsung Electronics Co., Ltd.

19. Mitsubishi Electric Corporation

20. Gree Electric Appliances, Inc. of Zhuhai

21. Midea Group Co., Ltd.

22. Hisense Group

23. Haier Group Corporation

24. Chigo Air Conditioning Co., Ltd.

25. AUX Group Co., Ltd.

FAQs:

1. What are the growth drivers for the Ducted Heat Pump Market?

Ans. The Increasing demand for energy-efficient heating and cooling solutions, Government incentives and regulations promoting energy-efficient HVAC systems, Rising awareness of sustainability and reduced carbon footprint, etc. are expected to be the major driver for the Ducted Heat Pump market.

2. What is the major restraint on the Ducted Heat Pump market growth?

Ans. The initial high installation cost of ducted heat pumps can deter some potential customers from adopting these systems and this is expected to be the major restraining factor for the Ducted Heat Pump market growth.

3. Which region is expected to lead the global Ducted Heat Pump market during the forecast period?

Ans. Europe is expected to lead the global Ducted Heat Pump market during the forecast period.

4. What is the projected market size & and growth rate of the Ducted Heat Pump Market?

Ans. The Global Ducted Heat Pump Market size was valued at USD 14.31 Billion in 2024 and the total Ducted Heat Pump revenue is expected to grow at a CAGR of 7.4% from 2025 to 2032, reaching nearly USD 25.34 Billion.

5. What segments are covered in the Ducted Heat Pump Market report?

Ans. The segments covered in the Ducted Heat Pump market report are Product Type, Application, End-User, and Region.