Coal to Liquid Fuel (CTL) Market by Product, Technology and Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

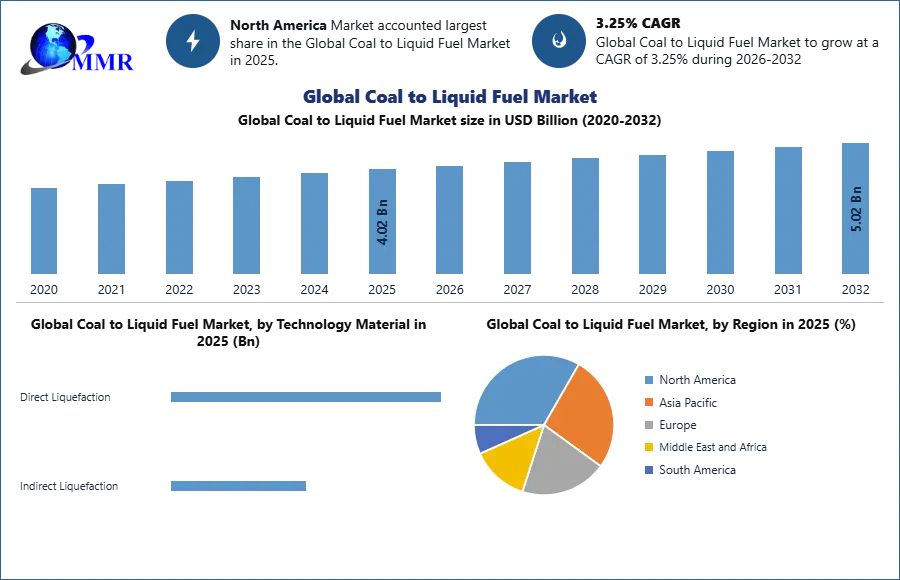

Coal to Liquid Fuel Market size is expected to reach USD 5.02 Bn. by 2032, at a CAGR of 3.25% during the forecast period.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Coal to Liquid Fuel Market Dynamics:

Rising reliability on natural gas and fossil fuel for the manufacturing of conveying powers along with stationary or steadily decreasing depository according to the present industry framework is the major factor accountable for the CTL automation execution. The increase in the prices of fossil fuel or crude oil gas refinement is additionally estimated to operate the need for the CTL procedure.

Various CTL activities will be money-oriented in the coming year with the expectation of inducement for an extended attempt to transform coal to low sulfur, ash-free conveying powers, and ultimately gaseous powers for domestic utilization. Technological development combined with encouraging the development of the liquid power needs for conveying is the major factor operating the worldwide CTL market. In the recent industry outline, there are twenty energetic CTL amenities around the world. With an increase in gas costs, the exchanges of natural gas from dry carbon, to be utilized in natural gas discharged energy creation provision, seems to be remarkably reasonable. Technologically promoted power cell and incorporated Cycle energy creations will also need the transformation of carbon to cleansed gaseous or fluid powers. Fluid products obtained from syngas are estimated to captivate a larger market portion in the upcoming years. Simple accessibility of developed and operation specified catalysts has authorized the manufacturing of larger hydrocarbons such as methanol. Combination gas obtained from power products are estimated to acquire higher significance in the coming year. These products are utilized for product chemicals and also observe execution as conveying powers. Furthermore, they can be utilized in the manufacturing of reserved additional powers for IGCC power plants. The Fischer Tropsch procedure is the highest utilized coal mixture procedure in the companies. Its responses and polymerization of syngas planning’s examined to be larger and modifiable according to the determined needs to manufacture a broad arrangement of products, like paraffin lubricates, hydrocarbon gasoline, and oxygenates.

Coal to Liquid Fuel Market Segment Analysis:

Based On Product : The diesel segment dominated the Coal-to-Liquid (CTL) fuel market in 2025, accounting for approximately 66.6% of the total market share. This dominance is primarily driven by the extensive use of diesel fuel across transportation, industrial, and commercial sectors. Diesel remains the preferred fuel for heavy-duty vehicles, including trucks, buses, mining equipment, and construction machinery, due to its higher energy efficiency and durability compared with other fuels. As global logistics, infrastructure development, and freight transportation activities expand, the demand for diesel continues to increase, supporting the growth of this segment.

In addition, the rapid expansion of the manufacturing and industrial sectors, particularly in emerging economies such as China and India, has significantly contributed to the consumption of diesel-based fuels. Diesel is widely used to power industrial generators, heavy machinery, and backup power systems, making it a critical fuel for continuous industrial operations.Technological advancements in indirect coal liquefaction processes, especially Fischer–Tropsch synthesis, have also improved the efficiency and yield of synthetic diesel production. These advancements enable companies to produce high-quality, low-sulfur diesel from coal resources. As a result, strong industrial demand, cost efficiency, and technological progress continue to drive the growth of the diesel segment in the CTL fuel market.

Coal to Liquid Fuel Market Regional Analysis:

North America emerged as a lucrative region in the coal-to-liquid (CTL) fuel market, accounting for nearly 18.0% of the global market share in 2025. The growth of the regional market is primarily driven by increasing fuel demand from the transportation and industrial sectors. The steady rise in the number of passenger vehicles, commercial trucks, and logistics fleets across the United States and Canada has significantly increased the need for reliable liquid fuels, creating opportunities for synthetic fuel technologies such as CTL.

In addition, the expansion of manufacturing facilities and heavy industries in North America has contributed to higher fuel consumption. Many industrial operations rely on diesel and other liquid fuels to power machinery, equipment, and backup generators, which indirectly supports demand for alternative fuel production technologies.

Another key factor supporting market growth is the growing awareness of energy security and alternative fuel sources. Governments and energy companies in the region are increasingly focusing on reducing dependence on imported crude oil by promoting domestic fuel production. Supportive regulatory frameworks, research funding, and pilot projects related to advanced fuel technologies are encouraging investments in CTL and other synthetic fuel solutions.

Together, rising fuel demand, industrial expansion, and supportive energy policies are strengthening the growth prospects of the coal-to-liquid fuel market in North America.

Coal to Liquid Fuel Market Recent Development:

-

Expansion of CTL capacity in China (2024–2026): China has significantly expanded its coal-to-liquid and coal-to-chemicals industries to enhance energy security and reduce dependence on imported oil and gas. Several new projects and plant expansions are being developed in coal-rich regions such as Inner Mongolia and Xinjiang, strengthening the country’s synthetic fuel production capacity.

-

China Shenhua Energy CTL expansion (2024): China Shenhua Energy expanded its CTL operations to increase the production of cleaner synthetic fuels. The company is investing in advanced liquefaction technologies to improve efficiency and meet rising transportation fuel demand in China.

-

Technological advancements in CTL production: In 2024, Linc Energy announced improvements in coal-to-liquid technologies aimed at increasing conversion efficiency and lowering environmental impact. The company is focusing on advanced gasification and liquefaction processes to produce cleaner diesel and jet fuel from coal resources.

-

Integration of hydrogen and cleaner fuel technologies (2025): China Datang Corporation launched a coal-to-chemicals project integrating green hydrogen, marking an important step toward lowering carbon emissions in coal-based fuel production systems.

-

New coal gasification and synthetic fuel initiatives in India (2026): New projects in Maharashtra aim to convert coal-derived syngas into alternative fuels such as dimethyl ether (DME), supporting India’s goal of reducing LPG and petroleum imports.

Coal to Liquid Fuel Market Scope: Inquiry Before Buying

| Global Coal to Liquid Fuel Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 4.02 USD Billion |

| Forecast Period 2026-2032 CAGR: | 3.25% | Market Size in 2032: | 5.02 USD Billion |

| Segments Covered: | by Technology Material | Direct Liquefaction Indirect Liquefaction |

|

| by Product Material | Diesel Gasoline Other Fuels |

||

| by Application | Transportation Fuel Cooking Fuel Others |

||

Coal to Liquid Fuel Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Coal to Liquid Fuel Market, Key Players:

- Sasol Limited

- China Shenhua Energy Company

- Yankuang Energy Group Company Limited

- Inner Mongolia Yitai Coal Co., Ltd.

- Linc Energy Ltd.

- DKRW Energy LLC

- Monash Energy

- Envidity Energy Inc.

- Altona Energy Plc

- Bumi plc

- TransGas Development Systems LLC

- Celanese Corporation

- Syntroleum Corporation

- Rentech Inc.

- Baard Energy LLC

- GreatPoint Energy Inc.

- Headwaters Incorporated

- Eastman Chemical Company

- Siemens Energy

- Shell plc

- Exxon Mobil Corporation

- Chevron Corporation

- Peabody Energy Corporation

- China National Petroleum Corporation

- Honeywell International Inc.

- Worley Limited