Central Laboratory Market Size by Service Type, Application, End User, Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

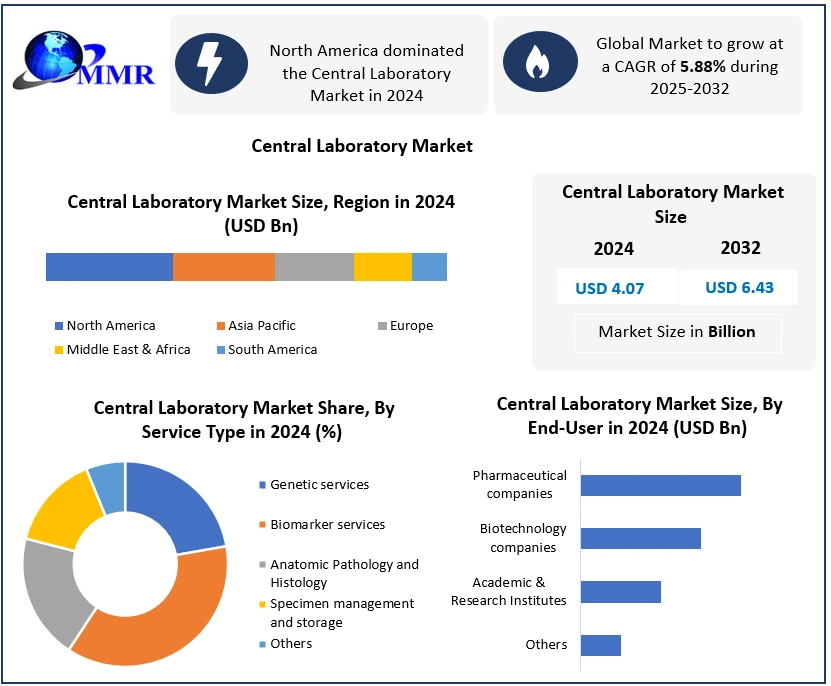

The Central Laboratory Market was valued at USD 4.07 Bn in 2024, and the total revenue of the Central Laboratory Market is expected to grow at a CAGR of 5.88% from 2025 to 2032, reaching USD 6.43 Bn by 2032.

The central laboratories are specialized facilities equipped to conduct various scientific analyses and experiments in a centralized location. It serves as a hub for processing and testing samples collected from multiple locations, often in the context of clinical trials, research studies, or industrial processes. The major factors driving the growth of the central laboratory market are increased funding, investments, and collaborative agreements related to clinical trials, research studies, or industrial processes. For instance, in February 2023, Cerba Research, a leading global clinical trial laboratory service provider announced a Memorandum of Understanding (MoU) with Teddy Clinical Research Laboratory, a preeminent central lab provider to lay the foundation for the creation of a Joint Venture (JV). This collaborative move emphasizes the key player's dedication to addressing the evolving demands of the central laboratory market and leveraging their collective expertise to contribute to the growth and advancement of global clinical trial services.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

In addition, increased funding provides central laboratories with the necessary resources to enhance their capabilities, adopt advanced technologies, and improve overall infrastructure. For instance, LabCentral Impact Report 2021, reported that the company raised $6.03 billion funding, with 21% of the total Series A funding. Such strategies have led to the development and implementation of innovative laboratory technologies, automation systems, and data management solutions, thereby contributing to the expansion of central laboratory market growth.

Increasing number of clinical trials

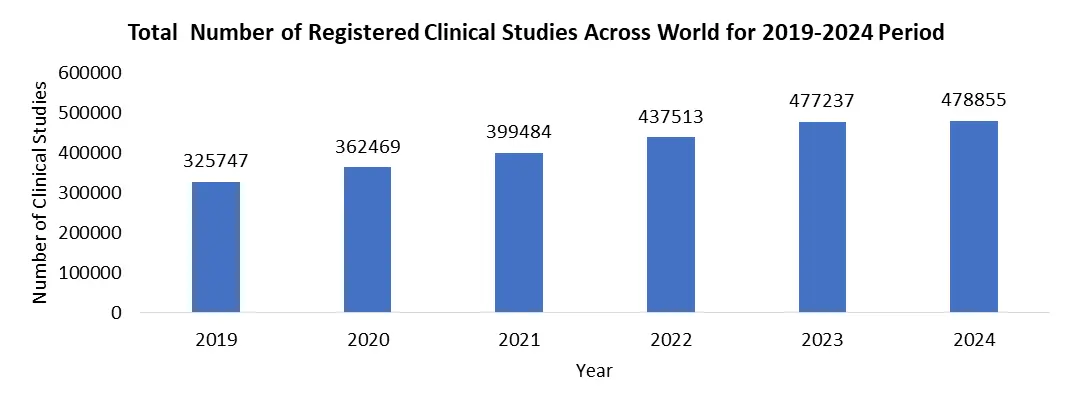

The increasing number of clinical trials, especially in the pharmaceutical and biotechnology sectors, demands centralized and standardized laboratory services for efficient sample processing, analysis, and data management, thereby propelling the growth of the central laboratory market. Clinical trials, which evaluate the safety and efficacy of new drugs, medical devices, and therapeutic interventions, have witnessed a substantial surge in numbers globally. For instance, the U.S. National Library of Medicine reported 485,377 clinical trial studies across 223 countries till March 2024. This surge is primarily driven by advancements in medical research, the need for novel treatments, and the growing emphasis on evidence-based medicine. Clinical trials serve as a crucial step in the development and approval of new healthcare interventions, making accurate and reliable laboratory testing an indispensable component of the process. Central laboratories play a pivotal role in this landscape by providing comprehensive testing services that ensure the collection of high-quality, standardized data across multiple trial sites. As the number and complexity of clinical trials continue to rise, several factors contribute to the growth of the central laboratory market. The below graph shows the number of registered clinical studies across the world.

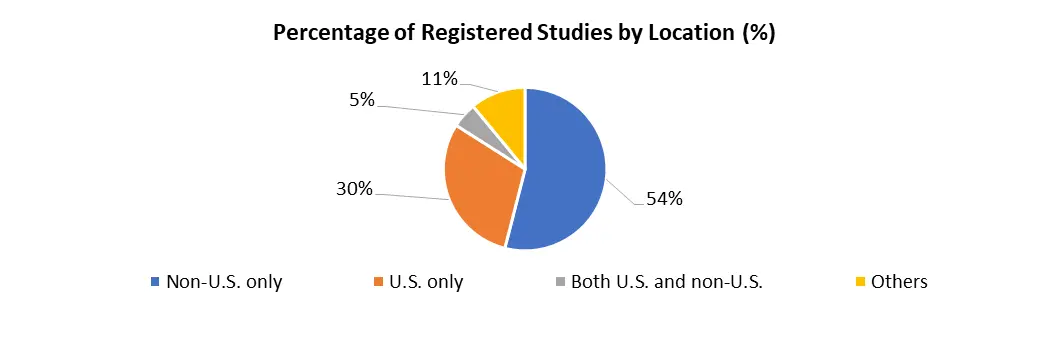

Further, the globalization of clinical trials is expected to fuel the central laboratory market revenue. With the expansion of research activities beyond traditional boundaries, central laboratories offer a standardized approach to sample processing and testing. This ensures consistency in data collection and analysis, regardless of the geographical locations of trial sites. Centralized testing facilitates the comparison of results, streamlines processes, and enhances the overall efficiency of clinical trials. The below graph shows the number of registered clinical studies across the world, thereby propelling the central laboratory market growth.

Moreover, regulatory compliance is a crucial factor influencing the central laboratory market. Regulatory authorities impose stringent requirements on the data generated during clinical trials to ensure its accuracy, reliability, and integrity. Central laboratories, often accredited and compliant with industry standards, play a vital role in meeting these regulatory demands. Their adherence to rigorous quality control measures instills confidence in the integrity of the data generated, making them a preferred choice for sponsors and researchers. Thus, the increasing number of clinical trials globally is a driving factor for the growth of the central laboratory market.

The rise in investments to expand central lab services drives the central laboratory market growth

The central laboratory market is experiencing a substantial boost from the increasing trend of investments in central lab services. This surge in financial support is emerging as a key driver, propelling the growth and evolution of the central laboratory market. The expanding investments are driven by various factors that collectively contribute to the enhancement of infrastructure, technology, and capabilities within the central laboratory industry, thereby fostering innovation and meeting the growing demands of the clinical research landscape. For instance, in October 2022, Thermo Fisher Scientific Inc.'s PPD clinical research business announced an investment of $59 million for the expansion of its laboratory operations in Highland Heights, Kentucky. As a world leader in serving the scientific community, the company aims to fortify its existing facility, including central lab and biomarker operations, to enhance its capacity to deliver high-quality laboratory services to biopharmaceutical customers. The investment focuses on expanding sample management and testing capabilities, particularly to support the development of new therapeutics such as vaccines, cell therapies, and gene therapy products.

Further, the primary focus behind the escalating investments in central lab services is the exponential rise in clinical trials across diverse industries such as pharmaceuticals, biotechnology, and medical research. As the demand for robust, standardized, and high-quality data from clinical trials continues to rise, organizations are recognizing the pivotal role of central laboratories in delivering reliable and consistent results. Thus, increased investments are directed towards expanding the capacity and capabilities of central laboratories to cater to the rising number and complexity of clinical trials, thereby propelling the central laboratory market revenue.

Logistics and sample handling issues hamper the growth of the central laboratory market

The central laboratory market faces a notable restraint due to challenges associated with logistics and sample handling. Efficient management of logistics and the proper handling of samples are critical for the seamless execution of clinical trials, but they often present significant hurdles. In trials conducted across diverse geographic locations, coordinating the collection, transportation, and storage of samples becomes a complex process. The need for standardized procedures across various environments with distinct infrastructural and regulatory landscapes is crucial to maintaining data consistency. Additionally, stringent requirements for specific storage conditions, particularly maintaining the cold chain for certain samples, pose significant challenges. Any deviation from these conditions during transportation can compromise the integrity of samples, thereby impacting the accuracy of central lab results. These issues not only risk setbacks in clinical trial timelines but also necessitate meticulous planning and investments in advanced tracking systems to ensure compliance with regulatory standards. Thus, addressing these logistics and sample handling issues is crucial in enhancing the efficiency and reliability of central laboratory services, contributing to the overall growth and effectiveness of the central laboratory market.

Central Laboratory Market Segment Analysis

Based on Service type, the biomarker services segment dominated the central laboratory market and is expected to exhibit the fastest growth during the forecast period. This dominance is attributed to the escalating utilisation of biomarkers in both drug development and clinical research. Biomarkers play a pivotal role in measuring physiological or disease-related processes, including responses to treatment, disease progression, and patient prognosis. The increasing integration of biomarker services in these critical aspects of medical research is driving its prominence within the central laboratory market, reflecting a sustained demand for precision and personalized approaches in healthcare.

Based on the End-User, the pharmaceutical companies segment accounted for the largest central laboratory market share in 2024, owing to its pivotal role in clinical trials for new drugs, substantial investments in R&D activities, and the escalating prevalence of chronic diseases. As pharmaceutical companies continue to drive innovation in the healthcare sector, central laboratories stand as indispensable partners, facilitating the generation of high-quality data that is crucial for the development and approval of novel therapeutic interventions. Moreover, the increase in investments in research and development (R&D) activities by pharmaceutical companies further solidifies their influence in the central laboratory market. Robust R&D investments are essential for fostering innovation, exploring new therapeutic avenues, and advancing the drug development pipeline. Central laboratories become integral partners in these processes, offering a spectrum of services ranging from sample management to specialized testing, thereby aiding pharmaceutical companies in their novel treatments and therapies.

Central Laboratory Market Regional Insights

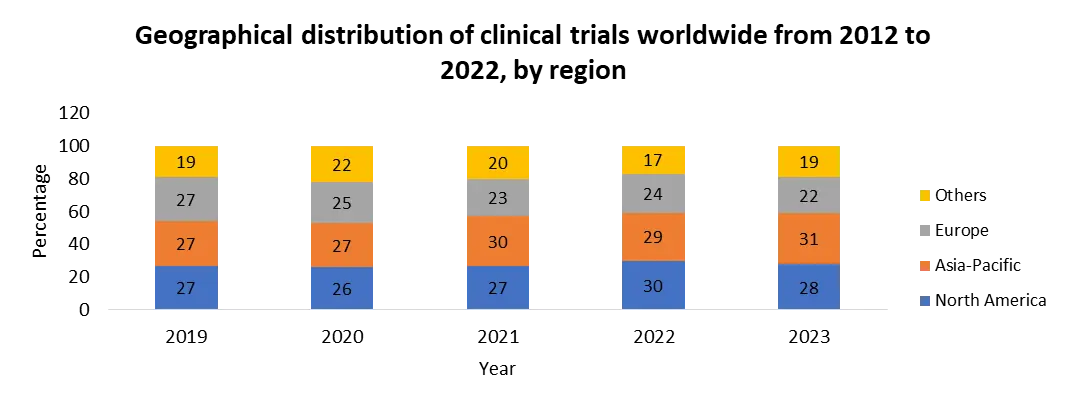

Region-wise analysis, North America was a major contributor to the central laboratory market and is expected to remain dominant during the forecast period, owing to factors such as the strong presence of key players along with the availability of advanced technologies, the large presence of pharmaceutical and biotech companies, and rise in government initiatives promoting research activities for the development of novel drugs. The presence of several major players, such as Laboratory Corporation of America, IQVIA Inc (Q2 Solutions), Eurofins Scientific, and Rochester Regional Health (ACM Global Laboratories), and the wide availability of service offerings in the region drives the growth of the central laboratory market. Furthermore, the presence of a well-established healthcare infrastructure and the rise in the adoption rate of sequencing services for disease detection is expected to drive the central laboratory market growth. The below graph shows region-wise clinical trials for the 2019-2023 period.

Moreover, the rise in the adoption of strategies such as the expansion of central laboratories, collaboration, acquisition, and agreement in this region further boost the growth of the central laboratory market revenue. For instance, in October 2021, IQVIA announced the opening of a state-of-the-art, 160,000-square-foot lab facility for its Q2 Solutions subsidiary. The new facility has an innovative suite of laboratory capabilities, including novel bioanalytical, vaccine, biomarker, and genomics laboratories.

Central Laboratory Market Scope: Inquire before buying

| Global Central Laboratory Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 4.07 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 5.88% | Market Size in 2032: | USD 6.43 Bn. |

| Segments Covered: | by Service Type | Genetic services Biomarker services Anatomic Pathology and Histology Specimen management and storage Others |

|

| by Application | Oncology Infectious Diseases Cardiology Neurology Others |

||

| by End User | Pharmaceutical companies Biotechnology companies Academic & Research Institutes Others |

||

Central Laboratory Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Central Laboratory Market Key Players

Global

1. Laboratory Corporation of America Holdings (United States)

2. Medpace (United States)

3. ACM Global Central Lab (United States)

4. Frontage Labs (United States)

5. IQVIA Inc. (United States)

6. LabConnect (United States)

7. Thermo Fisher Scientific (United States)

8. MLM Medical Labs (Germany)

North America

1. Rochester Regional Health (United States)

Europe

1. Cerba Healthcare (France)

2. ICON Plc (Ireland)

3. Eurofins Scientific (Luxembourg)

4. Medicover Integrated Clinical Services (Poland)

Frequently Asked Questions

1] What segments are covered in the Central Laboratory Market report?

Ans. The segments covered in the Central Laboratory Market report are based on Service Type, End User, Application, and Region.

2] Which region is expected to hold the highest share in the Market?

Ans. The North American region is expected to hold the largest share of the Market.

3] What is the market size of the Central Laboratory Market by 2032?

Ans. The Central Laboratory Market is expected to reach USD 6.43 Bn in 2032.

4] What is the forecast period for the Central Laboratory Market?

Ans. The forecast period for the Central Laboratory Market is 2025-2032.

5] What was the market size of the Global Central Laboratory Market in 2024?

Ans. The market size of the Central Laboratory Market in 2024 was valued at USD 4.07 Bn.