Cancer Pain Market – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2030

Overview

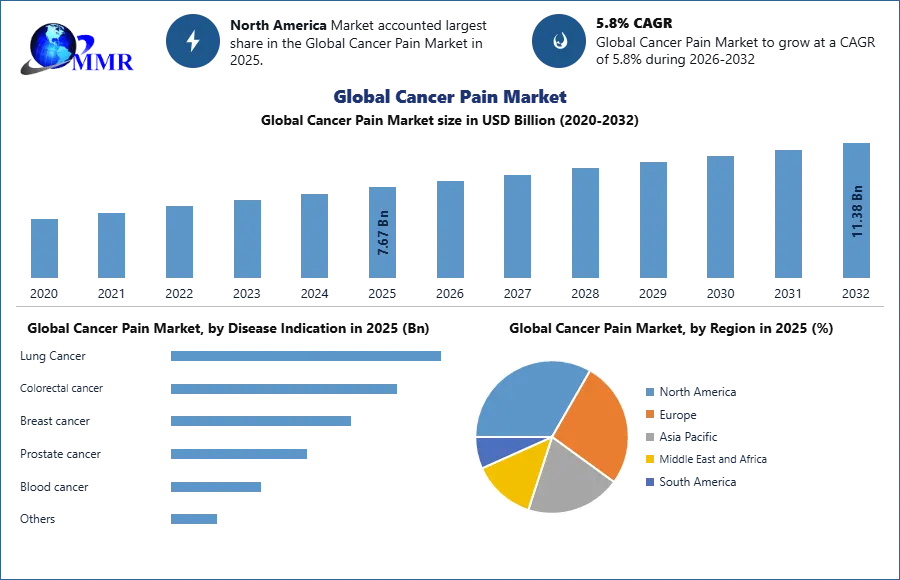

The Cancer Pain Market size was valued at USD 7.67 Billion in 2025 and the total Cancer Pain Revenue is expected to grow at a CAGR of 5.8% from 2024 to 2030, reaching nearly USD 11.38 Billion by 2032.

Cancer Pain Market Overview

Cancer pain arises from the disease itself or as a result of treatments such as surgery or chemotherapy. A range of medications are available to help ease cancer pain, with the choice of drug depending on the level of pain experienced.

The Cancer Pain Market encompasses the global landscape of pharmaceuticals and treatments aimed at managing pain associated with cancer. This market is largely driven by factors such as the increasing prevalence of cancer, a rise in the geriatric population, and investments in research and development activities by healthcare companies. The key players in the market include Aoxing Pharmaceutical Company, Inc., Teva Pharmaceutical Industries Limited, Pfizer, Inc., and Orexo AB, etc. The market is segmented based on drug type, disease indication, and region, with opioids, non-opioids, and nerve blockers being key drug categories used for pain management. The growth of the cancer pain market is influenced by factors like the aging population's susceptibility to various cancers and the surge in demand for monoclonal antibodies for cancer treatment. Regardless of its growth potential, challenges such as adverse effects associated with pain management drugs hinder market growth during the forecast period.

In the Asia-Pacific region, the Cancer Pain Market is witnessing significant growth, with a projected CAGR. This robust development is fueled by various factors reshaping the landscape of cancer pain management in the region. The rising prevalence of cancer in Asia-Pacific has underscored the need for more effective pain management solutions. Additionally, the region is experiencing a demographic shift towards an aging population, which correlates with a higher incidence of cancer and a greater demand for advanced pain management interventions. Also, there is a growing awareness regarding the importance of early cancer screening, leading to an increased need for effective pain management strategies. These combined factors are driving Asia-Pacific to the forefront of the Cancer Pain Market.

To know about the Research Methodology :- Request Free Sample Report

Cancer Pain Market Dynamics

Surge in Cancer Prevalence & Advancements Pain Management Therapies

Cancer remains a major health concern worldwide, with millions of new cases diagnosed each year. The development of novel drugs and treatment strategies has revolutionized the field of pain management, offering more targeted and effective solutions for alleviating cancer-related pain. Targeted therapy and immunotherapy have emerged as game-changers in cancer treatment, providing more nuanced approaches to controlling tumor growth and managing associated pain. These innovative treatment modalities have significantly improved patient outcomes and contributed to reducing the prevalence of severe cancer pain.

The growth of the cancer pain market is further fueled by an aging population and increased healthcare expenditure globally. Older individuals are more susceptible to various types of cancers owing to age-related effects and genetic mutations. Additionally, the rise in investments in research and development activities by healthcare companies has led to the introduction of advanced pain therapeutics that offer enhanced efficacy and safety profiles for cancer patients. The market is witnessing a surge in demand for monoclonal antibodies and other cutting-edge treatments that target specific pathways involved in cancer-related pain, driving further growth in this sector. Even with these advancements, challenges such as adverse effects associated with pain medications and stigma around opioid use continue to pose restraints on market growth. Issues like drug tolerance, dependence, and cognitive impairment associated with certain pain medications highlight the importance of developing safer and more tolerable treatment options for cancer pain management. Addressing Healthcare Disparities and Financial Barriers

Addressing Healthcare Disparities and Financial Barriers

Unequal healthcare infrastructure and inflated healthcare expenses are major obstacles for the cancer pain market, affecting the availability of crucial pain management services and causing financial hardships for patients. Divergences in healthcare infrastructure, both locally and globally, contribute to uneven access to specialized pain management treatments for cancer patients. In regions with underdeveloped healthcare systems, patients often struggle to receive timely and effective pain relief, resulting in disparities in treatment outcomes and quality of care.

The uneven allocation of healthcare resources worsens these differences, limiting the accessibility of advanced pain management therapies for those in need. Additionally, the high costs associated with cancer care, including pain management treatments, create a barrier to receiving optimal care. The financial strain of cancer treatment, combined with the expenses of pain management medications and therapies, overwhelm healthcare systems and individuals, hampering the adoption of innovative pain management approaches and potentially compromising the quality of care for cancer patients. Overcoming these challenges necessitates a collaborative effort to enhance healthcare infrastructure, reduce inequalities in pain management service access, and implement strategies to alleviate the financial burden of cancer care.

Cancer Pain Market Segment Analysis

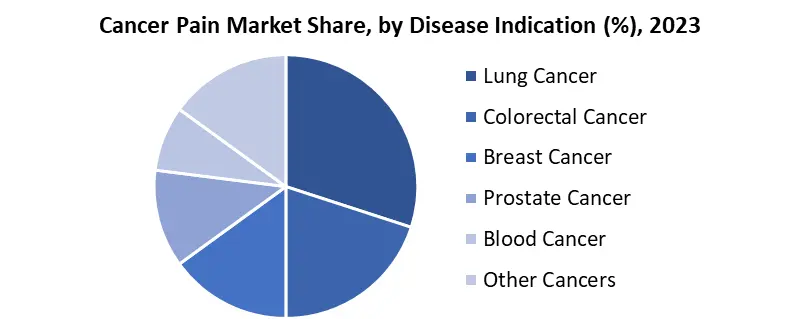

Based on Disease Indication, the Lung Cancer segment holds the largest market share of about 43% in the Global Cancer Pain Market. According to MMR analysis, the segment is further expected to grow during the forecast period. It stands out as the dominant segment within the Global Cancer Pain Market. Lung cancer stands as a prominent segment within the cancer pain market, fueled by its widespread occurrence and aggressive nature. This intensifies the demand for continuous pain management solutions, driving cancer pain market growth. The complexity of lung cancer pain arises from various sources, including nerve compression by tumors, bone involvement, and inflammation-related discomfort, necessitating a diverse array of pain management options. The limited remedial treatments available for advanced-stage lung cancer shift the focus towards pain easing and enhancing patient quality of life, sustaining the need for effective pain medications and creating a favorable market landscape.

Additionally, the evolving healthcare landscape emphasizes the importance of early and aggressive pain management practices to mitigate the adverse impact of untreated pain on patient outcomes and well-being. This shift translates to increased interventions for lung cancer patients at earlier stages, elongating treatment duration and subsequently bolstering cancer pain market demand for pain management solutions. Lung cancer's prevalence, diverse pain sources, limited treatment options in advanced stages, evolving therapeutic landscape, and growing emphasis on early pain management collectively position it as a dominant segment in the cancer pain market.

The Colorectal Cancer Segment is the second largest with a market share of about 20.7% in the Cancer Pain Market. Colorectal cancer constitutes a sizeable segment of the cancer pain market. Tumors obstruct the colon, causing cramping and abdominal discomfort. In later stages, the cancer spreads to other organs or nerves, leading to more severe pain. Surgery and radiation for colorectal cancer also induce pain. This multifaceted pain experience necessitates a variety of pain management approaches, including medications, nerve blocks, and interventional procedures. As the focus on early pain management grows, the colorectal cancer segment is expected to see continued growth in the cancer pain market.

The Colorectal Cancer Segment is the second largest with a market share of about 20.7% in the Cancer Pain Market. Colorectal cancer constitutes a sizeable segment of the cancer pain market. Tumors obstruct the colon, causing cramping and abdominal discomfort. In later stages, the cancer spreads to other organs or nerves, leading to more severe pain. Surgery and radiation for colorectal cancer also induce pain. This multifaceted pain experience necessitates a variety of pain management approaches, including medications, nerve blocks, and interventional procedures. As the focus on early pain management grows, the colorectal cancer segment is expected to see continued growth in the cancer pain market.

Cancer Pain Market Regional Insights

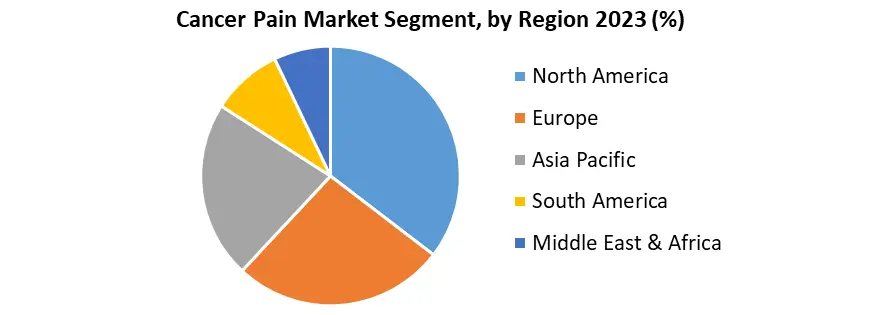

North America dominated the Global Cancer Pain Market with the highest share of over XX% in 2025. The region is expected to grow at a CAGR of 6.3% during the forecast period and maintain its dominance. With a high prevalence of cancer and a well-developed healthcare infrastructure, the region boasts a substantial patient population in need of pain management solutions, thus driving cancer pain market demand.

Additionally, North America's emphasis on pain management as a vital component of cancer care is reflected in extensive protection coverage for pain medications and procedures, encouraging healthcare providers to explore diverse pain management options and fostering research and development in the field. The region's willingness to embrace innovative technologies further boosts the cancer pain market growth, with a strong inclination towards adopting new drug delivery systems, minimally invasive procedures, and advanced radiotherapy techniques aimed at minimizing pain. Supported by a flourishing pharmaceutical industry dedicated to pain management research, North America consistently introduces new medications and treatment modalities into the market, catering to the varied pain experiences of cancer patients. Even with challenges such as high healthcare costs and stringent regulatory frameworks, the region's focus on advanced cancer care, prioritization of pain management, and culture of innovation solidify its position as a global leader in the cancer pain market. The European market for cancer pain commands a substantial share, accounting for approximately 25-30% of the global market. Europe's large and aging population, coupled with a high cancer prevalence, drives demand for pain management solutions. The presence of universal healthcare systems in certain European countries ensures widespread patient access to pain management medications and procedures. The increasing adoption of palliative care further accentuates the need for effective pain management options. Nevertheless, economic disparities across the region and bureaucratic hurdles in some countries pose challenges, potentially limiting access to advanced pain management therapies and delaying the adoption of new medications. Despite these obstacles, Europe's well-established healthcare infrastructure, growing emphasis on palliative care, and continuous advancements in pain management technologies solidify its significance in the global cancer pain market.

The European market for cancer pain commands a substantial share, accounting for approximately 25-30% of the global market. Europe's large and aging population, coupled with a high cancer prevalence, drives demand for pain management solutions. The presence of universal healthcare systems in certain European countries ensures widespread patient access to pain management medications and procedures. The increasing adoption of palliative care further accentuates the need for effective pain management options. Nevertheless, economic disparities across the region and bureaucratic hurdles in some countries pose challenges, potentially limiting access to advanced pain management therapies and delaying the adoption of new medications. Despite these obstacles, Europe's well-established healthcare infrastructure, growing emphasis on palliative care, and continuous advancements in pain management technologies solidify its significance in the global cancer pain market.

Cancer Pain Market Competitive Landscapes

The market for Cancer Pain is competitive for both well-established and emerging companies. The key players such as Johnson & Johnson Services Inc., F. Hoffmann, La Roche Ltd., Pfizer Inc., Abbott Laboratories, Novartis AG, Eli Lilly and Company, Gilead Sciences, Bristol Myers Squibb, AbbVie Inc., Zydus Pharmaceuticals Inc. have been concentrating on adopting new technology, product innovations, mergers & acquisitions, joint venture, alliances, and partnerships to improve their market position in the global liver disease treatment industry.

1. In 2023, Pfizer partnered with Seagen to reimagine the future of cancer treatment. This collaboration aimed to develop innovative medicines and vaccines that benefit patients globally, demonstrating Pfizer's commitment to addressing the challenges of cancer and improving healthcare outcomes.

2. In 2023, Novartis collaborated with MorphoSys AG, which aimed at strengthening its oncology pipeline with innovative treatments for cancer, including pelabresib and tulmimetostat. This acquisition aligns with Novartis' strategic focus on oncology and underscores its commitment to developing next-generation treatment options for cancer patients.

3. Johnson & Johnson's acquisition of Ambrx Biopharma in 2023 for approximately $2 billion marked a strategic move to strengthen its oncology pipeline with promising cancer therapies, particularly focusing on antibody-drug conjugates (ADCs) for targeted cancer treatment

Cancer Pain Market Scope: Inquiry Before Buying

| Global Cancer Pain Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 7.67 USD Billion |

| Forecast Period 2026-2032 CAGR: | 5.8% | Market Size in 2032: | 11.38 USD Billion |

| Segments Covered: | by Drug Type | Opioids Non-steroidal anti-inflammatory Drugs (NSAIDs) Adjuvants Local Anesthetics Other Analgesics |

|

| by Disease Indication | Lung Cancer Colorectal cancer Breast cancer Prostate cancer Blood cancer Others |

||

| by End-Users | Hospitals Homecare Specialty Clinics Others |

||

Cancer Pain Market by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Cancer Pain Market Key Players

1. North America

Pfizer Inc (USA)

Johnson & Johnson (United States)

CK Life Science (WEX Pharma) (Canada)

Collegium Pharmaceutical (USA),

Abbott (USA)

Sorrento Therapeutics (USA)

Galena Biopharma (USA)

AbbVie Inc. (USA)

Talphera Inc (USA)

Merck & Co., Inc. (USA)

2. Europe

Orexo AB (Sweden)

Mallinckrodt Pharmaceuticals plc (Ireland)

AstraZeneca PLC (England)

MundiPharma International Ltd (United Kingdom)

Roche Holding AG (Switzerland)

Grünenthal Pharma GmbH & Co. KG (Germany)

3. Asia Pacific

Daiichi Sankyo Co., Ltd. (Japan)

Hisamitsu Pharmaceutical Co., Inc. (Japan)

Kalbe Farma (Indonesia)

Livzon Pharmaceutical Group (China)

Sun Pharmaceutical Industries Ltd (India)

Zydus Lifesciences (Indai)

4. Middle East & Africa

Teva Pharma Industries Ltd (Israel)

FAQs:

1. What are the growth drivers for the Cancer Pain market?

Ans. Rising cancer prevalence, aging population and focus on pain management are the drivers of the Global Cancer Pain Market.

2. What are the major challenges for the Cancer Pain market growth?

Ans. Limited access to specialists and uneven healthcare infrastructure are the major challenges for the Cancer Pain Market.

3. Which region is expected to lead the global Cancer Pain market during the forecast period?

Ans. North America is expected to lead the global Cancer Pain market during the forecast period.

4. What is the projected market size & and growth rate of the Cancer Pain Market?

Ans. The Cancer Pain Market size was valued at USD 7.67 Billion in 2025 and the total Cancer Pain revenue is expected to grow at a CAGR of 5.8% from 2026 to 2032, reaching nearly USD 11.38 Billion by 2032.

5. What segments are covered in the Cancer Pain Market report?

Ans. The segments covered in the Cancer Pain market report are drug type, disease indication, end-user, and region.