Bread Market by Product Type, Ingredient, Nutritional value, Distribution channel and Region - Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

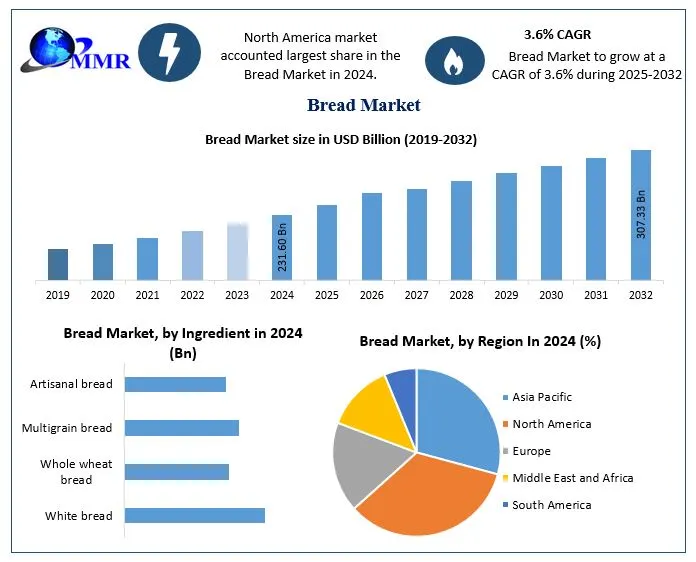

The Bread Market size was valued at USD 231.60 Billion in 2024 and the total Bread revenue is expected to grow at a CAGR of 3.6% from 2025 to 2032, reaching nearly USD 307.33 Billion.

The global bread market is a thriving industry, fueled by factors such as population growth, changing dietary habits, and the convenience and versatility of bread as a food item. With a market value of approximately USD 208.7 billion in and a compound annual growth rate of around 3.6%, the bread market continues to expand steadily. This growth is attributed to rising urbanization, increased disposable incomes, and the growing popularity of convenience foods.

While North America and Europe are the leading regions in terms of consumption and market growth, emerging economies in Asia Pacific, Southern America, the Middle East and Africa are also witnessing an increasing demand for bread. As consumers prioritize health and nutrition, there is a growing interest in whole wheat bread and speciality varieties. The rise of online retail and the opportunities presented by developing regions further contribute to the market's potential. To capitalize on these trends, industry players are focusing on innovation, product differentiation, and catering to specific consumer needs.

The report includes market analysis, forecasts, industry segmentation and competitive analysis of top Bread manufacturers. The report also emphasises sustainability, innovation and consumer preferences, offering a global outlook with trends, drivers, challenges and opportunities. It will help industry stakeholders (manufacturers, distributors, retailers, investors) make informed decisions and capitalise on Bread market opportunities. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Bread Market Dynamics

Market Drivers:

The bread market is primarily driven by several factors that contribute to its sustained growth. Firstly, the increasing global population, coupled with urbanization, has resulted in higher demand for convenient and readily available food options like bread. Rising disposable incomes, particularly in developing economies, have also boosted the consumption of bread as an affordable staple food. For instance, the Bread Price Index, which tracks the cost of a loaf of bread in various countries, has shown steady growth in recent years, reflecting increased consumption.

Furthermore, changing dietary patterns and preferences have influenced the demand for different types of bread. Consumers are becoming more health-conscious, leading to a shift towards whole wheat bread and specialty varieties. This trend is supported by government initiatives promoting healthier eating habits. For example, the Indian government launched the 'Eat Right India' campaign, which promotes the consumption of whole grain bread and encourages bakeries to use healthier ingredients.

Market Restraints:

Despite the positive growth trajectory, the bread market faces certain challenges and restraints. One of the primary concerns is the increasing prevalence of gluten intolerance and celiac disease, which has led to a rise in demand for gluten-free bread. The market has responded to this demand with the introduction of gluten-free options; however, production costs and limited availability of gluten-free ingredients impacts the pricing and accessibility of such bread.

Additionally, the competition from alternative food products, such as wraps, tortillas, and gluten-free substitutes like cauliflower bread, poses a challenge to the traditional bread market. Changing consumer preferences and the availability of various substitutes require bread manufacturers to innovate and adapt their product offerings to remain competitive.

Market Opportunities:

The bread market offers several opportunities for growth and expansion. With the increasing adoption of e-commerce and online retail, bread manufacturers can tap into the digital space to reach a wider consumer base. Online platforms enable convenient ordering and home delivery of bread, catering to busy lifestyles. For instance, during the COVID-19 pandemic, there was a significant surge in online bread sales as consumers sought contactless purchasing options.

Moreover, expanding into emerging markets presents opportunities for bread manufacturers. Rapid urbanization, changing consumer habits, and rising disposable incomes in countries like India, China, and Brazil offer untapped potential for market growth. Companies can customize their product offerings to cater to specific regional tastes and preferences.

Market Challenges:

The bread market also faces specific challenges that require strategic approaches. One major challenge is the need to address sustainability and environmental concerns. The production and distribution of bread involve significant energy consumption and carbon emissions, and companies should look forward to mitigating those.

Furthermore, fluctuating raw material prices, especially for wheat and other grains, can affect the profitability of bread manufacturers. Volatile commodity markets and weather conditions, such as droughts or floods, influence crop yields leading to price fluctuations.

Bread Market Segmentation:

Based on Product type, the bread market is segmented into loaves, baguettes, rolls, burger buns, sandwich slices, ciabatta, frozen bread, and other product types. Among these, loaves hold the largest market share, being the most popular type of bread consumed worldwide. Baguettes have gained significant popularity in Europe, while rolls are commonly consumed in North America. Burger buns and sandwich slices cater to the sandwich market, offering convenient options for quick meals. Ciabatta, known for its airy texture and chewy crust, appeals to those seeking a unique dining experience. Additionally, frozen bread emerges as a convenient option for consumers with time constraints. Among these segments, rolls have the potential to grow in the future due to their versatility and adaptability in various cuisines, particularly as demand for fast and convenient food options continues to rise.

Based on ingredient, The bread market is segmented into white bread, whole wheat bread, multigrain bread, and artisanal bread.

White bread, a traditional and widely consumed variety, is made from refined wheat flour and is often fortified with nutrients. Whole wheat bread has gained popularity due to the growing emphasis on health and wellness. Made from whole grain flour, it retains the fiber and nutrients present in the wheat kernel. Multigrain bread appeals to health-conscious consumers as it contains a combination of different grains, providing a diverse nutritional profile and texture. Artisanal bread, handcrafted using traditional techniques and premium ingredients, offers unique flavors and textures, catering to consumers seeking high-quality and distinctive bread products.

Among these segments, whole wheat bread holds significant potential for growth in the future, driven by increasing consumer awareness of the benefits of whole grains and their preference for healthier options. The emphasis on wellness and nutritional value positions whole wheat bread as a favorable choice in the evolving bread market.

Based on nutritional value, The bread market is segmented into high-fiber bread, low-carb bread, gluten-free bread, functional bread, and other nutritional values. High-fiber bread, rich in dietary fiber, plays a crucial role in regulating digestion and promoting heart health, making it a popular choice among health-conscious consumers. Low-carb bread caters to individuals following a low-carbohydrate diet, providing an alternative option with reduced carbohydrate content.

Gluten-free bread addresses the needs of people with gluten intolerance or celiac disease, allowing them to enjoy bread without adverse effects. Additionally, bread can offer various other nutritional values such as protein, iron, and calcium, contributing to a well-rounded diet. Functional bread stands out by being fortified with additional nutrients or ingredients, offering specific health benefits like added vitamins, minerals, omega-3 fatty acids, or probiotics. Among these segments, high-fiber bread is widely used and has significant growth potential in the future due to increasing awareness of the importance of dietary fiber in maintaining overall health and wellness.

Based on Distribution Channel, The bread market is segmented into supermarkets and hypermarkets, convenience stores, specialist retailers, online retail, and other distribution channels. Among these segments, supermarkets and hypermarkets dominate the market, holding the largest market share. These retail giants provide a wide range of bread products, catering to the diverse preferences of consumers. Convenience stores serve as a popular distribution channel, offering a convenient option for consumers looking for quick and easy meals on the go. Specialist retailers, such as bakeries and bread shops, provide a unique and specialized selection of bread varieties, attracting consumers seeking premium and artisanal options.

Online retail is an emerging distribution channel for bread, with growing consumer interest in purchasing groceries online. This channel offers convenience and a wider product selection, allowing consumers to access a range of bread options from the comfort of their homes. Among these segments, online retail has the potential to witness significant growth in the future as e-commerce continues to gain traction and consumers seek more convenient ways to purchase bread and other grocery items.

Bread Regional Analysis:

The bread market exhibits diverse dynamics across different regions. In North America, the market holds the largest share, driven by well-established bakery industries and consumer demand for convenient food options. The region experiences a growing trend toward healthier bread choices, with an increased consumption of whole wheat and specialty breads.

Europe boasts a rich bread culture and is a significant market for traditional and artisanal bread varieties. Strong brand recognition and a wide range of bread products contribute to the market's growth in the region. Governments in Europe have implemented initiatives to safeguard and promote traditional bread-making methods and ingredients, fostering the expansion of specialty bread segments.

The Asia Pacific region is emerging as a key player in the bread market. Factors such as population growth, urbanization, and changing dietary habits contribute to the region's potential for significant growth. As disposable incomes rise and lifestyles become more fast-paced, there is a growing demand for convenient and ready-to-eat food options, including bread.

Governments in the Asia Pacific region are actively implementing initiatives to support the bakery sector and ensure food security. Urban development plans and food security programs are being put in place to accommodate the expanding urban population and guarantee the availability and affordability of bread products.

Latin America, the Middle East, and Africa are also witnessing an increasing demand for bread. Factors such as changing lifestyles, urbanization, and rising disposable incomes contribute to this growth. Governments in these regions are focused on improving food security, expanding distribution networks, and supporting local agricultural production to meet the growing demand for bread.

Bread Industry, Competitive Landscape

The bread market is characterized by intense competition, with established players and new entrants vying for market share. Grupo Bimbo, one of the world's largest baking companies, holds a prominent position in the industry, operating in numerous countries and owning renowned brands like Bimbo, Arnold, and Sara Lee. Another key player is Associated British Foods Plc, with its brand Kingsmill, which enjoys a strong presence in the United Kingdom. The competitive landscape of the bread market is shaped not only by established players but also by smaller-scale artisanal bakeries. These artisanal bakeries have gained popularity, particularly in urban areas, by offering handcrafted bread made with premium ingredients and unique flavors. They cater to consumers seeking high-quality and distinctive products, challenging the market dominance of larger players.

Mergers and acquisitions play a significant role in shaping the competitive landscape. A notable example is Grupo Bimbo's acquisition of Grupo Mankattan, a leading bakery company in Colombia. This strategic move expanded Grupo Bimbo's presence in the Latin American market, reinforcing its position as a global industry leader.

Technological advancements have also influenced the competitive dynamics of the bread market. Companies have embraced smart packaging solutions to enhance product freshness and improve the consumer experience. Bühler Group, for instance, has developed packaging technologies that utilize sensors to monitor temperature, humidity, and gas levels, ensuring optimal product quality and longer shelf life. Moreover, clean label ingredients have gained prominence, with bread manufacturers focusing on natural, additive-free alternatives. Puratos, a global baking and confectionery company, has introduced clean label solutions that cater to health-conscious consumers by offering bread products made from wholesome ingredients without compromising on taste or texture.

Bread Market Scope: Inquire before buying

| Bread Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 231.60 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 3.6% | Market Size in 2032: | USD 307.33 Bn. |

| Segments Covered: | by Product Type | Loaves Baguettes Rolls Burger buns Sandwich slices Ciabatta Frozen bread Other |

|

| by Ingredient | White bread Whole wheat bread Multigrain bread Artisanal bread |

||

| by Nutritional value | High-fiber bread Low-carb bread Gluten-free bread Functional bread Other nutritional values |

||

| by Distribution channel | Supermarkets and hypermarkets Convenience stores Online retail channel Speciality stores |

||

Bread Market by Region:

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Bread Key Players

The following Bread Companies are the key players in the market and are selected based on criteria for further evaluation. The strategies followed by the companies to sustain and grow in the market are discussed in detail in the report

1. Grupo Bimbo

2. Associated British Foods plc

3. Yamazaki Baking Co., Ltd.

4. Finsbury Food Group plc

5. Flowers Foods, Inc.

6. George Weston Limited

7. Premier Foods plc

8. Britannia Industries Limited

9. Warburtons Ltd.

10. Aryzta AG

11. Weston Foods

12. Barilla Group

13. Hostess Brands, Inc.

14. Grupo Lala

15. Almarai Company

FAQs

1. What was the Global Bread Market size in 2024?

Ans: The Global Bread Market size was USD 231.60 Billion in 2024.

2. What is the growth rate of the Bread Market?

Ans: The CAGR of the Bread Market 3.6%.

3. What are the segments of the Bread Market?

Ans: There are primarily five segments are product type, ingredient, nutritional value, distribution channel and geography for the bread market.

4. Which region has the highest market share in the Bread Market sector?

Ans: North America has the highest market share in the Bread Market sector.

5. Is it profitable to invest in the Bread Market?

Ans: There is a fair growth rate in this market and there are various factors to be analyzed like the driving forces and opportunities of the market which have been discussed extensively in Maximize’s full report. That would help in understanding the profitability of the market.