Bone Hammers Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2029

Overview

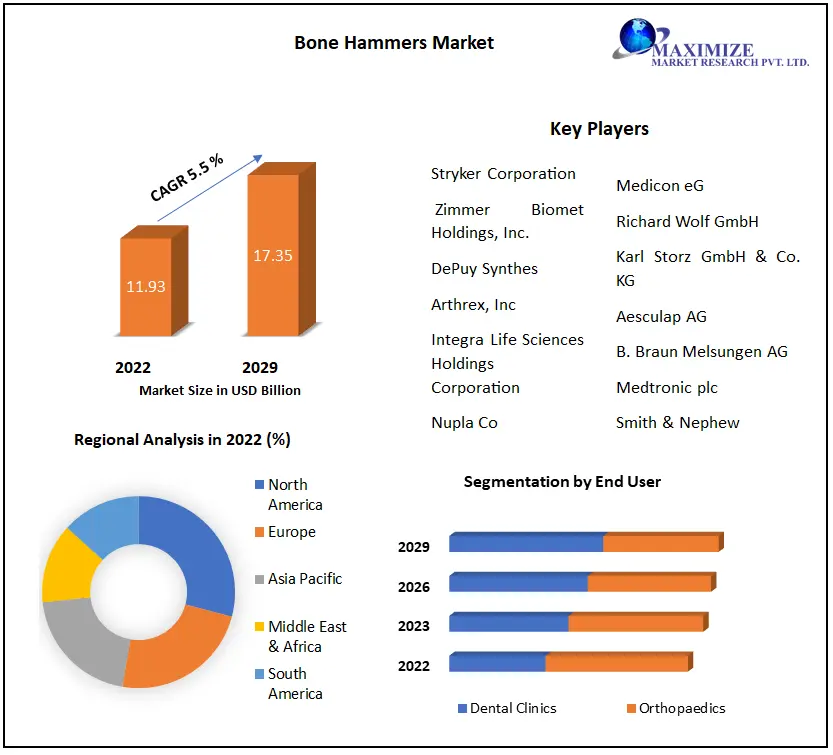

Bone Hammers Market is worth USD 11.93 Billion in 2022 and is estimated to grow at a CAGR of 5.5 % in the forecasted period. The forecasted revenue hints at a growth of around 17.35 billion USD by 2029.

The bone hammer is a solid head orthopaedic instrument utilized to apply force for bone and tissue abrade or resizing bones. In simpler words these hammers are specifically designed for use in orthopaedic surgeries and procedures. These specialized hammers are used by surgeons to manipulate, shape, and set bones during surgical interventions. The hammer's size and form dictate its surgical utility. Bone hammers are usually built of durable, strong, and corrosion-resistant materials. Factors like aging population, increased patients and advanced surgeries have helped the market flourish in many regions.

The bone hammer market is a tightly regulated market and is governed by stringent quality standards and certifications that ensures the safety of the product during orthopaedic surgeries. The bone hammer provides an advantage in the process of bone fixation, saving valuable operating time and improving patient outcomes. Another use of this bone hammer is when orthopaedic surgeons use bone hammers to shape, mold, and set bones according to the desired alignment which helps in correcting deformities, realigning fractures, and improving overall bone function. The Bone hammers are known for their versatilities which allows for a broader range of orthopaedic applications which in turn helps the market diversify into various sectors. In current scenario, the product has huge demand and is expected to grow even in future indicating a CAGR 5.5%.

North America leads the market share amongst the other regions. Osteoporosis, osteoarthritis, and other bone ailments are common in the region. Dental clinics are also driving the bone hammer industry. Some of the key players operating in the bone hammers market include Nupla Co., Uppea, Rockforge Co., Klein Tools Co., Ludell Pvt. Ltd., Husky Ltd., Estwing, TEKTON Inc., Hart Associates, and Razor-Back Co. Such companies have focused on innovation and technology to distinguish themselves from competition. Asia Pacific is the fastest growing market as the bone disorders have been increasing along with increase in production of such hammers. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Increasing Awareness Driving the Growth in Bone Hammers Market

The major driving factor for the growth has been the increasing cases of orthopaedic problems. The rising number of patients with orthopaedic conditions such as fractures, degenerative bone diseases, and musculoskeletal disorders has driven the demand for bone hammers. Also, the aging global population has helped market growth. Sports-related injuries often use bone hammers, so the market has grown in that segment as well. Fractures, dislocations, and ligament tears often require orthopaedic interventions, which rely on bone hammers for bone manipulation and fixation. The increasing economies, especially in developing countries, have helped companies establish well-developed infrastructure in such countries.

The development of healthcare globally has had a positive impact on the bone hammer market. Growing awareness has definitely helped in increasing patients, which has caused an increase in bone hammer production. Minimally invasive surgical techniques have gained popularity due to their benefits, such as reduced scarring, shorter recovery times, and decreased post-operative complications. Bone hammers play a crucial role in these procedures by enabling precise bone manipulation through small incisions. The increasing awareness and adoption of minimally invasive surgeries contribute to the demand for bone hammers. NIAMS launched a campaign called "Joint Pain: Know Your Risks". This campaign was aimed at educating people about the risk factors for joint pain, such as obesity, smoking, and a lack of exercise.

The campaign also provided information regarding joint pain. The CDC also launched a campaign called "Bone Health: It's Not Just for Seniors". This campaign was aimed at educating people about the importance of bone health at all ages. Thus, such government campaigns have helped increase awareness, which has been a huge driving factor in the bone hammer market.

Replacement is a Major Challenge for Bone Hammer Market

One of the major challenges the bone hammer market faces is increasing competition. As demand increases, many companies have entered the market, making it difficult for existing users to compete. Also, hospitals and clinics tend to prefer cost-effective solutions, and thus they tend to negotiate lower prices or demand discounts from bone hammer manufacturers, putting pressure on profit margins. Bone hammers are basic instruments, making differentiation difficult for producers. To compete, companies must provide distinctive features or value-added services. The fragmentation in the product sizes increases price volatility and competitiveness, which affects the bone hammer market negatively. Also, issues regarding compliance and guidelines become a challenge, as ensuring compliance can be a complex and costly process, especially for smaller companies.

Product maintenance and feature integration have cost both manufacturers and customers, which has resulted in lower sales. Also, new-age equipment and technological advancements can reduce the demand for traditional bone hammers, as alternative tools or procedures may be preferred. Thus, the fear of substitution is a huge concern for the bone hammer market. Some healthcare professionals are unaware of the benefits of bone hammers or prefer alternative tools or techniques; thus, initiating awareness among them is also a difficult challenge for the bone hammer market.

Comfort and Feasibility are Major Factors influencing Trends in Bone Hammer Market

The trends regarding the bone hammer market have been revolving around its application and future use. One such application has been in minimally invasive surgeries. Orthopaedics is moving towards less invasive surgery to mitigate complications. Surgeons are increasingly using less invasive procedures that require bone hammers that can allow accurate bone manipulation through tiny entry sites. Thus, the increasing trend of non-invasive surgeries has an impact directly on bone hammer, helping the market sustain itself in the future. Also, the customization of designs has been seen as an early trend in the bone hammer industry.

Nowadays, surgeons prefer customized bone hammers, which ease surgeries. Adjustable handles, replaceable heads, and ergonomic designs are becoming more common. Bone hammers are made from more sophisticated materials. Titanium alloys and carbon fiber composites increase surgeon maneuverability and fatigue, and thus the trend to use such alloys rather than steel has been an upcoming trend.

Orthopaedic surgery is moving towards disposable and single-use equipment. Single-use bone hammers are convenient, cost-effective, and infection-free. Patient safety, cross-contamination prevention, and instrument control fuel this movement. As a result, the emphasis on patient safety, lowering the risk of cross-contamination, and streamlining instrument management are driving this trend. With increasing environmental concerns, the healthcare sector is also embracing sustainability. Recyclable or biodegradable bone hammers are in demand. Manufacturers are also considering eco-friendly production and packaging. Thus, technology, comfort, and feasibility have been driving the trends in the bone hammer market.

Bone Hammers Market Segmentation

Bone Hammers Market Segmentation, by Product

All Stainless Steel and Plastic Wood Handle Stainless Steel are the two main products in the bone hammer market. All stainless-steel bone hammers are expected to continue to have the highest market share, as they are the most durable and versatile type of bone hammer. They are also lightweight, which increases their application in many healthcare processes. However, plastic wood handle stainless steel may provide a cost advantage but lack durability and tenacity, which results in a lower market share than all stainless steel.

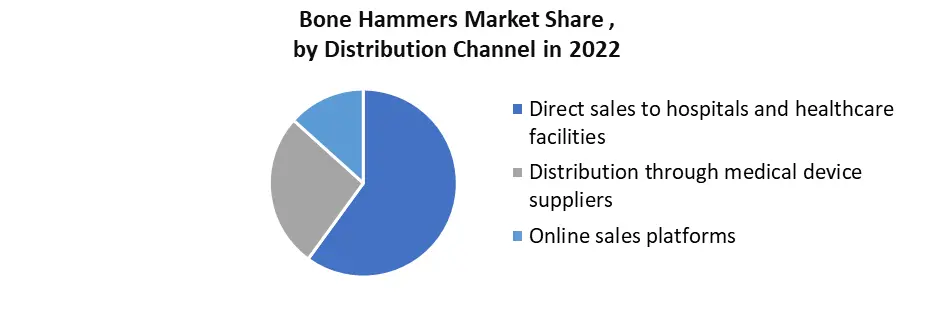

Bone Hammers Market Segmentation, by Distribution Channel Direct sales to hospitals and healthcare facilities, Distribution through medical device suppliers, and Online sales platforms have been the 3 dominant distribution channels in the market. The major market has been dominated by direct sales to hospitals, mainly because hospitals have been the primary customers of these hammers. Also, hospitals require bone hammers for a variety of procedures, such as bone surgery, dental extractions, and orthopaedic procedures. The online distribution channel is still in its early stages but has huge potential growth in the future.

Bone Hammers Market Segmentation, by Application

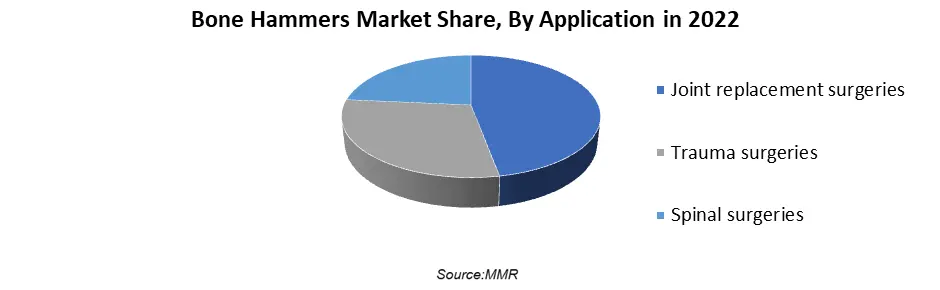

Joint replacement surgeries, Trauma surgeries and Spinal surgeries are the three major applications in bone hammer market. Most bone procedures come under joint replacements making it one of the most dominant segments in this application The replacement procedure helps in replacing hip, knee, and shoulder joints. These processes require bone hammers which makes it a huge part of all these join replacement surgeries. Spinal procedures cure scoliosis, stenosis, and ruptured discs. Bone hammers remove bone spurs and open the spinal canal in spinal procedures. Spinal surgeries also have huge potential in future as spinal problems are becoming more common.

Bone Hammers Market Segmentation, by End User

Orthopaedics and Dental Clinics have been the two prominent users in bone hammer market. Orthopaedics have been the dominant user amongst the two. Orthopaedics helps in musculoskeletal system, which includes the bones, joints, muscles, and tendons. The aging population plays a huge role in increased demand for this segment. Dental clinics use bone hammers for a variety of procedures like root canal. However, the use of bone hammers in dental clinics is not as widespread as the use of bone hammers in orthopaedics. But dental clinics still have huge opportunity in future to earn a larger market share

Bone Hammers Market Segmentation, by Region

North America leads the market with the highest percent of market share, which nearly equals around 40% of the total market. A high rise in demand, increasing cases, and advanced mechanisms have played a crucial role in this region. The US enjoys a well-established healthcare infrastructure and advanced surgical practices, which require a bone hammer. Thus, many investors have invested a huge amount to gain a competitive advantage in this cluttered market. Asia Pacific is the fastest growing market, as countries like India, China, Japan, Singapore, and South Korea have been revolutionizing their healthcare industries.

Also, the Asia-Pacific region sees an increase in orthopaedic cases, which acts as a further boost to the market. Europe has been a dominant player in this market. Factors such as a rising geriatric population, sports injuries, and an emphasis on advanced medical technology contribute to the growth of the bone hammer market in this region. Germany, France, and the UK have been at the forefront of this growth. The Middle East region has shown huge investments in recent years, thus indicating a future marketplace for many established companies in the market.

Competitive Landscape

The bone hammer market is mainly based on its distribution. Extensive distribution has resulted in increased sales, which in turn have helped companies earn a higher market share. Thus, established companies like Stryker Corporation, Zimmer Biomet Holdings, Inc., DePuy Synthes (a subsidiary of Johnson & Johnson), Medtronic plc, and B. Braun Melsungen AG have shown a strong presence in the bone hammer market. Some companies have formed tie-ups with the government, which has helped them create a reputation for themselves in the market. One such example is Nupla Co., a US-based company that manufactures a variety of hand tools, including bone hammers.

The company has tie-ups with the US military and the US Department of Defence. Also, Ludell Pvt. Ltd. has tie-ups with the Indian government. Such collaborations ensure that these companies maintain their standards and provide quality along with durability and efficiency. Partnerships have a huge role in these markets as they add an added dimension to the existing product, improving its quality. Example: Husky Ltd. and Estwing have a distribution partnership to distribute bone hammers in Canada, and Tekton Inc. and Hart Associates have a technology sharing agreement to improve their bone hammer manufacturing processes.

Mergers have been a consistent thing in the market, and some prime examples have been Husky Ltd. acquiring Tekton, which gave Husky a stronger position in the DIY market. Another case has been of Klein Tools Co. acquiring Ludell Pvt. Ltd. and establishing a strong base in the Indian market. These mergers have not only helped strategically but have also shown changes in dynamics, positioning, and the overall market.

Bone Hammers Market Scope : Inquire Before Buying

| Global Bone Hammers Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2022 | Forecast Period: | 2023-2029 |

| Historical Data: | 2017 to 2022 | Market Size in 2022: | US $ 11.93 Bn. |

| Forecast Period 2023 to 2029 CAGR: | 5.5% | Market Size in 2029: | US $ 17.35 Bn. |

| Segments Covered: | by Product | All Stainless Steel Plastic Wood Handle Stainless Steel |

|

| by Distribution Channel | Direct sales to hospitals and healthcare facilities Distribution through medical device suppliers Online sales platforms |

||

| by Application | Joint replacement surgeries Trauma surgeries Spinal surgeries |

||

| by End-User | Orthopaedics Dental Clinics |

||

Bone Hammers Market by Region:

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Bone Hammers Market , Key Players are

1. Stryker Corporation (United States)

2. Zimmer Biomet Holdings, Inc. (United States)

3. DePuy Synthes (United States)

4. CONMED Corporation (United States)

5. Arthrex, Inc. (United States)

6. Integra LifeSciences Holdings Corporation (United States)

7. W. Lorenz Surgical, Inc. (United States)

8. Wright Medical Group N.V. (United States)

9. MicroAire Surgical Instruments LLC (United States)

10. Accurate Surgical & Scientific Instruments Corporation (United States)

11. AESCULAP USA (United States)

12. Arthrotek, Inc. (United States)

13. OsteoMed (United States)

14. Precision Medical Devices, Inc. (United States)

15. Synthes (United States)

16. Medicon eG (Germany)

17. Richard Wolf GmbH (Germany)

18. Karl Storz GmbH & Co. KG (Germany)

19. Aesculap AG (Germany)

20. B. Braun Melsungen AG (Germany)

21. Medtronic plc (Ireland)

22. Smith & Nephew plc (United Kingdom)

23. Maxtown Medical Corp. (Taiwan)

24. Narang Medical Limited (India)

25. Olympus Corporation (Japan)

FAQ

Q.1) What is the CAGR of the Bone Hammers Market?

Ans: The CAGR for Bone Hammers Market is 5.5%.

Q.2) Which are the leading companies in Bone Hammers Market?

Ans: Nupla Co., Uppea, Rockforge Co., Klein Tools Co, are some of the leading companies in the Bone Hammers Market.

Q.3) Which region shows maximum potential in Bone Hammers Market?

Ans: North America is expected to grow exponentially and is likely to dominate Bone Hammers Market in the future.

Q,4) Which is the leading region in Bone Hammers Market?

Ans: Asia Pacific leads the market in Bone Hammers Market significantly.

Q.5) What was the forecasted period of this report?

Ans: The forecasted period for the Bone Hammers Market research was 2023 – 2029.