Autoinjectors Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2030

Overview

Autoinjectors Market size was valued at USD 1.54 Billion in 2023 and the total Autoinjectors Market revenue is expected to grow at a CAGR of 14.20% from 2024 to 2030, reaching nearly USD 3.90 Billion by 2030.

Autoinjectors Market Overview:

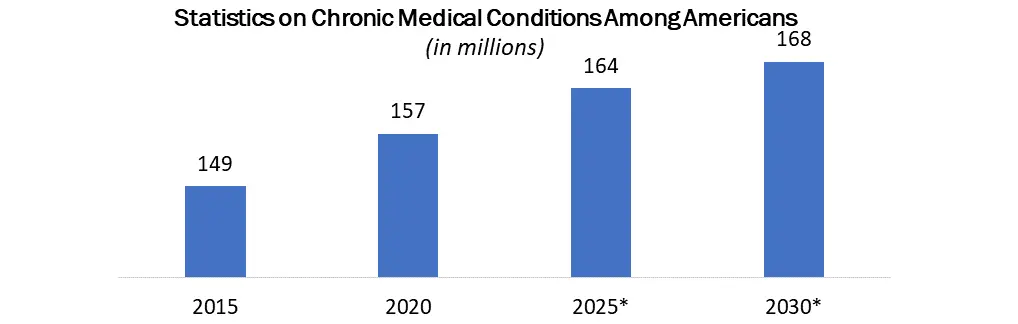

Autoinjectors are innovative medical devices that revolutionize allergy treatment. Unlike traditional syringes, autoinjectors deliver medication with precision and comfort, making them a preferred choice among patients and healthcare professionals. According to the National Health Interview Survey (NHIS), over half of the adult population in the US suffers from at least one chronic condition, such as asthma, diabetes, or hypertension. These conditions generate an annual cost burden of around USD 3.7 trillion, equivalent to nearly 20% of the country's GDP. A significant portion of this expense stems from the frequent need for medication, often requiring repeated visits to healthcare facilities. Patient adherence to treatment regimens also poses a challenge. To address these issues, a range of self-injectable drugs have been developed, offering patients greater independence and psychological benefits compared to traditional medication administration. Among these self-injection devices, autoinjectors have gained prominence, particularly for managing emergency and chronic conditions like anaphylactic shock and rheumatoid arthritis. Autoinjectors incorporate additional features like integrated needle safety, Bluetooth connectivity, and injection dose history tracking, effectively resolving several injection-related compliance concerns faced by patients.

The MMR reports also help in understanding the Autoinjectors Market dynamic, structure by analysing the market segments and projecting the Autoinjectors Market size. Clear representation of competitive analysis of key players by type, price, financial position, product portfolio, growth strategies, and regional presence in the Autoinjectors Market make the report investor’s guide.

Autoinjectors Market Dynamics-

The Rise of Chronic Diseases:

The increasing prevalence of chronic diseases is a major driver of the global Autoinjectors market. Autoinjectors offer a convenient and easy-to-use way to administer injectable medications, which is particularly beneficial for patients who require long-term treatment. The growth of the Autoinjectors market is expected to be driven by a number of factors, including the increasing prevalence of chronic diseases, the growing demand for home healthcare, the development of new and innovative autoinjector devices, the increasing adoption of biologics, and the growing awareness of the benefits of autoinjectors.

Some of the chronic diseases that are driving the demand for autoinjectors include:

| Disease | Prevalence |

| Diabetes | 463 million adults worldwide |

| Rheumatoid arthritis | 2.1 million adults in the United States |

| Multiple sclerosis | 2.3 million adults worldwide |

The prevalence of chronic diseases is increasing owing to a number of factors, including:

1. Aging populations: As the global population ages, there is an increased risk of developing chronic diseases such as diabetes and heart disease.

2. Unhealthy lifestyles: Unhealthy lifestyles, such as smoking, poor diet, and lack of physical activity, are major risk factors for chronic diseases.

3. Urbanization: People who live in cities are more likely to be exposed to environmental pollutants and have less access to healthy food and exercise.

Home Healthcare Trend Amplifies Demand for Autoinjectors:

The escalating demand for home healthcare services is a significant factor propelling the growth of the global autoinjectors market. The global home healthcare market is expected to reach a valuation of nearly USD 1.5 trillion by 2027. This surge in demand is primarily attributed to the aging population and the rising prevalence of chronic diseases. With the increasing number of individuals requiring ongoing medical care at home, there is a growing need for convenient and user-friendly drug delivery systems. Autoinjectors aptly fulfil this requirement, as they empower patients to self-administer injectable medications without the need for frequent healthcare professional visits.

The growing number of regulatory approvals and reimbursement policies for autoinjectors, coupled with government support, is fuelling the market's revenue growth. For instance, several Medicare prescription drug plans cover generic epinephrine autoinjectors, and some may also cover EpiPens, a brand-name autoinjector that administers epinephrine to individuals experiencing potentially life-threatening allergic reactions. Pfizer is also collaborating with the Food and Drug Administration (FDA) to extend the expiration dates of specific batches of EpiPen 0.3 mg Auto-Injectors and its authorized generic version to alleviate EpiPen shortages and enhance access to the medication. Prescription drug coverage under Medicare Part D is contingent upon the plan's terms and other factors. Autoinjectors represent the most effective first-line therapy for managing anaphylaxis in community settings. In anaphylactic emergencies, autoinjectors are crucial owing to their ability to deliver a precise dose, ensure consistent needle penetration and depth, facilitate rapid administration, and achieve a predictable dispersion pattern. Accurate and prompt self-administration of intramuscular adrenaline using an ampoule, needle, and syringe poses a greater challenge for patients and caregivers. Moreover, the rising prevalence of anaphylaxis is expected to further propel autoinjectors market revenue growth. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Regulatory Approvals: Fuelling Autoinjector Innovation and Autoinjectors market Growth

The growing number of regulatory approvals and reimbursement policies for autoinjectors, coupled with government support, is driving the autoinjectors market's revenue growth. For instance, several Medicare prescription drug plans cover generic epinephrine autoinjectors, and some may also cover EpiPens, a brand-name autoinjector that administers epinephrine to individuals experiencing potentially life-threatening allergic reactions. Pfizer is also collaborating with the Food and Drug Administration (FDA) to extend the expiration dates of specific batches of EpiPen 0.3 mg Auto-Injectors and its authorized generic version to alleviate EpiPen shortages and enhance access to the medication. Prescription drug coverage under Medicare Part D is contingent upon the plan's terms and other factors. Autoinjectors represent the most effective first-line therapy for managing anaphylaxis in community settings. In anaphylactic emergencies, autoinjectors are crucial due to their ability to deliver a precise dose, ensure consistent needle penetration and depth, facilitate rapid administration, and achieve a predictable dispersion pattern. Accurate and prompt self-administration of intramuscular adrenaline using an ampoule, needle, and syringe poses a greater challenge for patients and caregivers. Moreover, the rising prevalence of anaphylaxis is expected to further propel autoinjectors market revenue growth.

Lack of Knowledge and Abundance of Alternatives in Autoinjector Utilization:

The Autoinjectors Market growth hampered by a lack of knowledge about how to use them and the availability of alternative medical treatments, such as oral tablets. Many patients fail to properly mix insulin suspension pen injectors by tipping and rolling them, resulting in large clumps of accumulated insulin being expelled from the device during the first injection. This error can lead to the administration of subtherapeutic doses when using new cartridges, potentially causing hypoglycemia symptoms and hindering market revenue growth. Furthermore, autoinjectors may increase costs in healthcare settings compared to manual syringes and needles. Oral medication remains the most popular administration method due to its practicality, safety, and affordability. A wide range of drugs can be taken orally in the form of chewable tablets, liquids, capsules, or pills.

Threat of New Entrants in the Autoinjectors Market

The threat of new entrants in the autoinjectors market is moderate to high. While the market boasts high entry barriers, the growing demand for autoinjectors and the potential profitability of the market could attract new players.

High Entry Barriers:

1. Regulatory Requirements: Autoinjectors are classified as Class II medical devices by the FDA, requiring stringent regulatory approval processes. This can be a significant hurdle for new companies, particularly those without extensive experience in the medical device industry.

2. Technology and Manufacturing Expertise: Developing and manufacturing safe and effective autoinjectors requires advanced technology and expertise in precision engineering, material science, and drug delivery systems. New entrants may lack these capabilities, requiring significant investments in research and development.

3. Brand Recognition and Distribution Network: Established players in the autoinjectors market enjoy strong brand recognition and established distribution networks, making it difficult for new entrants to gain market share.

4. Intellectual Property: Existing players have a strong intellectual property portfolio, including patents and trademarks, that can further limit the entry of new competitors.

Drivers for New Entrants:

1. Growing Autoinjectors Market Demand: The rising prevalence of chronic diseases and increasing awareness about autoinjector benefits are driving significant market growth, attracting new players seeking lucrative opportunities.

2. Technological Advancements: Advancements in materials science, drug delivery systems, and digital technology are creating new opportunities for innovation and differentiation, potentially opening doors for new entrants with unique product offerings.

3. Focus on Cost-Effectiveness: As healthcare providers and payers strive for cost-effective solutions, new entrants may offer lower-priced autoinjectors, disrupting the autoinjectors market landscape.

4. Partnerships and Acquisitions: Collaborations between established companies and new entrants with specific expertise can accelerate entry and overcome some of the traditional barriers.

Overall, the threat of new entrants in the autoinjectors market is a dynamic factor influenced by market trends, technological advancements, and strategic decisions of established players. While entry barriers remain significant, the potential for growth and profitability could incentivize new entrants to overcome these challenges and reshape the autoinjectors market landscape.

Autoinjectors Market Segment Analysis:

Subcutaneous is the most popular route of administration of autoinjectors, accounting for an autoinjectors market share of nearly XX% in 2023. Subcutaneous autoinjectors play a pivotal role in the delivery of various medications, offering a convenient and effective way for patients to self-administer their medications. These autoinjectors are specifically designed for subcutaneous administration, ensuring reliable absorption and helping to maintain therapeutic drug levels over an extended period. This consistent and accurate medication delivery system empowers patients to manage their chronic conditions independently, enhancing treatment adherence and improving overall quality of life. Subcutaneous autoinjectors are particularly well-suited for home use, allowing patients to administer their medications in the comfort of their own homes, reducing the need for frequent healthcare provider visits. This not only enhances patient convenience but also alleviates the burden on healthcare systems. The growing prevalence of chronic diseases and the increasing demand for home healthcare are driving the adoption of subcutaneous autoinjectors. As the global autoinjectors market continues to expand, subcutaneous autoinjectors are expected to play an increasingly significant role in improving patient care and treatment outcomes.

Subcutaneous autoinjectors are particularly well-suited for home use, allowing patients to administer their medications in the comfort of their own homes, reducing the need for frequent healthcare provider visits. This not only enhances patient convenience but also alleviates the burden on healthcare systems. The growing prevalence of chronic diseases and the increasing demand for home healthcare are driving the adoption of subcutaneous autoinjectors. As the global autoinjectors market continues to expand, subcutaneous autoinjectors are expected to play an increasingly significant role in improving patient care and treatment outcomes.

Rheumatoid Arthritis Expected to Hold Significant Autoinjectors Market Share Over the Forecast Period:

Rheumatoid arthritis (RA), an autoimmune disorder characterized by the immune system attacking the joints, is a significant contributor to the growth of the autoinjectors market. The inflammation of the synovium and swelling and pain in and around the joints caused by RA primarily affects the elderly population, with females experiencing a higher prevalence than males. According to the United Nations World Population Prospects 2020 report, 727 million people aged 65 years or above currently reside worldwide, and this number is projected to more than double by 2050. The increased prevalence of RA among the aging population is expected to fuel the demand for autoinjectors, as these devices offer a convenient and effective method for self-administering medications for RA treatment.

Autoinjectors play a crucial role in managing RA, allowing patients to self-administer medications such as methotrexate, adalimumab, and etanercept with ease and accuracy. The ease of use of autoinjectors enhances patient compliance and adherence to treatment regimens, improving overall disease management and treatment outcomes. The rising prevalence of RA, coupled with the aging population and the growing demand for home healthcare, is expected to drive the autoinjectors market for RA treatment significantly over the forecast period. Autoinjectors are poised to revolutionize RA management, empowering patients to take control of their health and improve their quality of life.

Autoinjectors Market Regional Analysis:

North America Dominates the Autoinjectors market

The North American Autoinjectors Market held the largest revenue share in the global autoinjectors market in 2023. North American pharmaceutical companies are actively investing in research and development, leading to the introduction of innovative autoinjector devices. For instance, on April 12, 2020, Teva Pharmaceuticals USA, Inc., a subsidiary of Teva Pharmaceutical Industries Ltd., introduced AJOVY autoinjector devices. AJOVY is the only anti-calcitonin Gene-Related Peptide (CGRP) migraine medicine available with quarterly (675 mg) and monthly (225 mg) subcutaneous dose options. It is approved for the preventive treatment of migraine in adults.

Asia Pacific Market Poised for Rapid Growth:

The Asia Pacific Autoinjectors Market is expected to register the fastest revenue growth rate in the global autoinjectors market during the forecast period. Pharmaceutical companies are expanding their presence in the Asia Pacific region, bringing innovative autoinjector technologies to the market. For instance, on July 30, 2021, ALK and China Grand Pharmaceutical and Healthcare Holdings Limited announced an exclusive licensing agreement to bring ALK's AAI Jext to the Chinese market. This collaboration aims to address the growing demand for effective and convenient allergy treatment options in the region.

The prevalence of chronic diseases, such as diabetes and rheumatoid arthritis, is rising in the Asia Pacific region. Autoinjectors offer a convenient and effective method for self-administering medications for these chronic conditions, driving the demand for these devices.

Recent Development News in the Global Autoinjectors market:

The global autoinjectors market is witnessing a surge of innovation and development, driven by the increasing demand for convenient and user-friendly drug delivery solutions. Several recent advancements underscore the market's growth trajectory and highlight the continued focus on enhancing patient care and treatment outcomes.

• Qfinity Autoinjector Platform: A Cost-Effective Solution for Subcutaneous Drug Delivery: In May 2022, Jabil Healthcare, a division of Jabil Inc., introduced the Qfinity autoinjector platform. Designed for subcutaneous (SC) drug self-administration, Qfinity stands out as a simple, reusable, and modular solution that offers enhanced affordability compared to existing market alternatives. This cost-effective platform is expected to expand access to autoinjector technology and improve patient adherence to treatment regimens.

• Aidaptus Auto-Injector: A Collaboration for Enhanced Patient Experience: In May 2022, Stevanato Group S.p.A. and Owen Mumford Ltd., a leading medical device developer and manufacturer, entered into an exclusive agreement for the development and commercialization of the Aidaptus auto-injector. This collaboration aims to bring forth an innovative autoinjector device that prioritizes patient comfort, ease of use, and safety.

Key Company Strategies:

Key players in autoinjectors market have adopted various strategies to expand their global presence and increase their market shares. Partnerships, agreements, mergers and acquisitions, and new product developments are some of the major strategies adopted by the market players, to achieve growth in the autoinjectors market. For example,

In May 2023, MoonLake initiated a partnership with SHL Medical to jointly work on the development of an autoinjector intended for the clinical and commercial distribution of MoonLake's Nanobody® sonelokimab.

Autoinjectors Industry Ecosystem

Autoinjectors Market Scope: Inquiry Before Buying

| Autoinjectors Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | USD 1.54 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 14.2% | Market Size in 2030: | USD 3.90 Bn. |

| Segments Covered: | by Type | Reusable Autoinjectors Disposable Autoinjectors |

|

| by Route of Administration | Intramuscular Subcutaneous |

||

| by Indication | Multiple Sclerosis Rheumatoid Arthritis Diabetes Anaphylaxis Others |

||

| by End-User | Homecare Settings Hospitals & Clinics Ambulatory Surgical Centers |

||

Autoinjectors Market, by Region:

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Autoinjectors Market Key Players:

1. Becton, Dickinson, and Company

2. Sanofi

3. Pfizer, Inc

4. Mylan N.V.

5. Novartis AG

6. Bayer AG

7. Janssen Global Services, LLC

8. Antares Pharma, Inc.

9. Amgen Inc

10. Eli Lilly and Company

11. Teva Pharmaceutical

12. Merck KgaA

13. GlaxoSmithKline plc

14. Ypsomed

15. SHL Medical

16. Gerresheimer AG

17. Midas Pharma GmbH

18. Aptar Pharma

19. Solteam Medical

20. Stevanato Group

21. E3D

22. West Pharmaceutical Services, Inc

FAQs:

1. What are the growth drivers for the Autoinjectors Market?

Ans. The increasing prevalence of chronic diseases is the major driver for the Autoinjectors Market.

2. What is the major restraint for the Autoinjectors Market growth?

Ans. Lack of Knowledge and Abundance of Alternatives in Autoinjector Utilization is expected to be the major restraining factor for the Autoinjectors Market growth.

3. Which Region is expected to lead the global Autoinjectors Market during the forecast period?

Ans. North America is expected to lead the global Autoinjectors Market during the forecast period.

4. What is the projected Autoinjectors Market size & growth rate of the Autoinjectors Market?

Ans. The Autoinjectors Market size was valued at USD 1.54 Billion in 2023 and the total Autoinjectors Market revenue is expected to grow at a CAGR of 14.20 % from 2024 to 2030, reaching nearly USD 3.90 Billion.

5. What segments are covered in the Autoinjectors Market report?

Ans. The segments covered in the Autoinjectors Market report are Route of Administration, Indication, Type, End-Use, and Region.