Waste Heat to Power Market by Technology, End-User Industry, Geography and Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2029

Overview

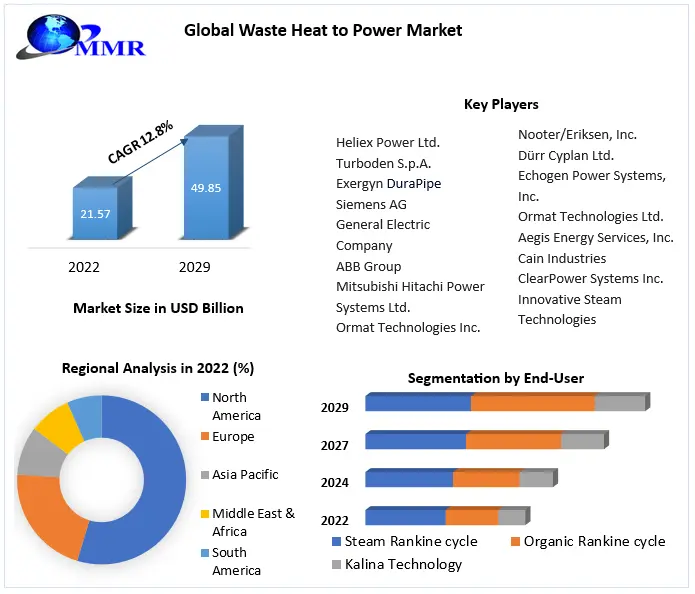

The Waste Heat to Power Market size is valued at USD 21.57 Billion and is forecast to grow at a CAGR of 12.8% from 2023 to 2029, reaching nearly USD 49.85 Billion.

The waste heat to power (WHP) market has emerged as a promising sector focused on capturing and converting waste heat into usable electricity or mechanical power. This form of energy recovery plays a crucial role in reducing energy consumption, improving efficiency, and mitigating greenhouse gas emissions. In recent years, the market has witnessed significant growth due to escalating environmental concerns, stringent regulations, and the increasing demand for sustainable energy solutions. Industries such as oil and gas, chemicals, cement, glass, metals, pulp and paper, among others, have become key adopters of waste heat to power systems. By effectively utilizing the waste heat generated during their operations, these industries can optimize their energy usage and decrease operational costs.

This report offers a comprehensive analysis of the evolving global market for Waste Heat to Power, featuring both qualitative and quantitative insights. The report is designed to provide valuable insights to help the companies already in the business develop effective growth strategies, analyze the competitive landscape, evaluate their position in the market, and make informed business decisions, as well as also help new entrants take strategic decisions regarding Waste Heat to Power Market. The report will further be valuable to other key stakeholders like suppliers, distributors, and industry participants, offering them insights into the market's revenue, production, and pricing trends and market share analysis across different segments and regions. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Waste Heat to Power Market dynamics

Market Drivers

The waste heat to power (WHP) market is experiencing significant growth driven by several market drivers. Stringent environmental regulations focused on reducing greenhouse gas emissions and improving energy efficiency are compelling industries to adopt waste heat recovery systems. These regulations, combined with the rising demand for sustainable energy solutions, are key drivers propelling the growth of waste heat to the power market. The market drivers are creating substantial opportunities for industries to achieve cost savings. Waste heat recovery enables industries to utilize the waste heat generated during their operations, reducing energy consumption and lowering operational costs. The ability to convert waste heat into usable electricity or mechanical power presents a viable solution for industries to optimize their energy usage and improve their bottom line.

Market Restraints and Challenges:

However, the waste heat to power market also faces certain restraints and challenges. High upfront costs associated with the installation of waste heat recovery systems is a restraint to market growth. The initial investment required to integrate these systems into existing industrial processes deter some industries from adopting waste heat to power technologies. Technological limitations, such as the efficiency and scalability of certain waste heat recovery technologies, pose challenges that need to be addressed to maximize the market potential. Moreover, the complexity of integrating waste heat recovery systems into existing industrial processes is another challenge faced by the market. Each industry has unique operational requirements, and retrofitting waste heat recovery technologies to suit these requirements can be complex and time-consuming. The customization and integration process requires careful planning, engineering expertise, and coordination with existing systems, which can pose challenges for industry players.

Opportunities

Despite the challenges, the waste heat to power market presents significant opportunities for growth. The increasing focus on sustainability and energy efficiency is driving the demand for waste heat recovery technologies. The market offers opportunities for technological advancements, such as the development of more efficient and scalable waste heat-to-power systems. Additionally, expanding industrial sectors in emerging economies provide a fertile ground for market expansion, as industries seek energy-efficient solutions to reduce costs and comply with environmental regulations.

Waste Heat to Power Market Segmentation:

The waste heat to power market is segmented based on various factors, including the end-user industry, technology, and geography. Each segment represents a distinct subset of the market, and understanding their dynamics is crucial for identifying growth opportunities and potential market leaders which is covered in detail in the report.

By technology, the market is segmented into steam Rankine cycle, organic Rankine cycle (ORC), and Kalina technology. While all these technologies have their applications and advantages, the ORC segment is expected to witness the highest growth. ORC technology enables the conversion of waste heat into electricity using organic working fluids with lower boiling points. This makes it suitable for applications with lower waste heat temperatures, which are prevalent in various industries.

The ORC segment's growth is fuelled by ongoing advancements in ORC systems, including the development of new and more efficient working fluids, improved heat exchangers, and system optimization. These advancements enhance the overall efficiency and performance of ORC systems, making them increasingly attractive for waste heat recovery applications. However, for high-temperature heat recovery, SRC technology is expected to remain the dominating one in the market.

By end-user industry, the WHP market caters to sectors such as oil and gas, chemicals, cement, heavy metal production, pipeline transportation and others. The chemicals industry is expected to experience the highest growth among the mentioned end-user industries in the waste heat to power market. Firstly, the chemicals industry is known for its energy-intensive processes, which often involve high-temperature reactions. Secondly, the chemicals sector is subject to stringent environmental regulations aimed at reducing greenhouse gas emissions and promoting sustainable practices.

Waste heat recovery systems offer a viable solution for the industry to meet these regulations by utilizing waste heat, reducing its carbon footprint, and achieving sustainability goals. The integration of waste heat to power technologies aligns well with the sector's commitment to environmental stewardship, making it an attractive option for industry players. The cement industry segment is also expected to remain the largest segment by application type over the forecast period. The growing prominence of ORC-based systems and the huge potential for heat recovery offered by the cement industry are driving the waste heat to the power market for cement industry applications.

Waste Heat to Power Market Regional Analysis:

The waste heat to power market has witnessed significant growth globally, with regional factors and government initiatives playing a crucial role in driving its expansion. Several regions have emerged as key players in this market, with varying degrees of market share and growth potential.

One region that currently holds the highest market share in the waste heat to power sector is North America. This can be attributed to several factors. Firstly, the region has a well-developed industrial sector, which generates substantial waste heat that can be harnessed for power generation. Additionally, North America has a favorable regulatory environment and strong government support for renewable energy technologies. Initiatives such as tax incentives, grants, and favorable policies have encouraged the adoption of waste heat to power systems, boosting the market growth in the region.

Furthermore, the presence of key market players and technological advancements in waste heat recovery systems have contributed to North America's leading market position.Looking towards the future, it is anticipated that the Asia-Pacific region will lead the waste heat to power market. Several factors support this prediction. Firstly, the region has a massive industrial base, particularly in countries like China, India, and Japan. This vast industrial sector generates significant amounts of waste heat, creating immense potential for waste heat to power conversion.

Moreover, the rising demand for electricity, coupled with increasing environmental concerns, has prompted governments in the Asia-Pacific region to focus on sustainable energy solutions. Governments are implementing various initiatives and regulations to promote waste heat recovery and power generation. Additionally, rapid industrialization, urbanization, and increasing investments in renewable energy infrastructure further contribute to the region's growth prospects in the waste heat to power market.

Competitive Landscape

The waste heat to power market is characterized by a competitive landscape with a mix of established players and emerging entrants. According to market research, the top players in the market, including Siemens AG, General Electric Company, ABB Ltd, Mitsubishi Hitachi Power Systems Ltd, and Ormat Technologies Inc., hold significant market shares and have a wide range of waste heat to power solutions.

These companies leverage their expertise, global presence, and extensive research and development capabilities to cater to various industries and applications. In addition to the established players, there has been a notable rise in the number of emerging companies and startups entering the market. These entrants bring innovative technologies and solutions to the table, driving competition and pushing for advancements in waste heat recovery. Notable emerging players include ElectraTherm and Heat Power, which offer compact and cost-effective waste heat to power systems.

Thus, competitive landscape is shaped by various strategies employed by market players. Technological advancements remain a key focus, with companies investing in research and development to improve the efficiency, performance, and reliability of their waste heat to power systems. Strategic partnerships and collaborations are also prominent, allowing companies to leverage complementary expertise, expand their product offerings, and access new markets.

Mergers, acquisitions, and consolidations play a significant role in the competitive landscape, enabling established players to expand their product portfolios, access new technologies, and consolidate their market position. These activities facilitate synergies, cost savings, and market expansion. In 2021, Heat Recovery Solutions (HRS) merged with Enginuity Power Systems to create a stronger presence in the waste heat-to-power market. The merger combined HRS’ expertise in organic Rankine cycle systems with Enginuity's capabilities in waste heat capture and utilization.

Recent Advancements in Waste Heat to Power Market:

The waste heat to power (WHP) market has witnessed significant advancements in technologies, further enhancing its potential for energy recovery and efficiency. These recent developments have addressed some of the challenges faced by the market and opened up new opportunities for growth.

One notable advancement is the improvement in thermoelectric systems. Thermoelectric technology involves converting temperature differences into electrical voltage, enabling the direct conversion of waste heat into electricity. Recent developments in thermoelectric materials, such as advanced alloys and nanomaterials, have significantly enhanced the efficiency and performance of thermoelectric generators. These advancements have increased the feasibility of thermoelectric systems in a wider range of applications, making them more attractive for waste heat recovery.

Furthermore, the integration of waste heat to power technologies with other renewable energy systems has gained attention. Hybrid systems that combine waste heat recovery with solar, geothermal, or biomass energy sources have emerged as a promising approach. These integrated systems maximize energy utilization, improve overall efficiency, and provide a more sustainable and reliable power generation solution.

Additionally, digitalization and the Internet of Things (IoT) have contributed to the advancement of waste heat to power technologies. IoT-enabled sensors and connectivity enable remote monitoring and control of waste heat recovery systems, providing real-time insights into system performance and energy savings. This digital transformation enhances operational efficiency, facilitates predictive maintenance, and enables data-driven decision-making.

In September 2022, Mitsubishi Heavy Industries proclaimed the development of a binary power generation system based on ORC technology. The system retrieves waste heat from the sulfur-free-fuel-burning engines and later converts it into usable technology

In February 2022, A lead-free material called Cadmium (Cd) doped Silver Antimony Telluride (AgSbTe2) that can efficiently recover electricity from waste heat has been discovered by researchers at the Jawaharlal Nehru Centre for Advanced Scientific Research (JNCASR), an autonomous institution of the Department of Science and Technology (DST), Government of India. This discovery marks a paradigm shift in the thermoelectric puzzle.

In February 2022, An unspecified sum was agreed upon between TC Energy Corporation and Siemens Energy AG, a German energy business, to commission a waste heat-to-power plant installation in Alberta, Canada. As part of the agreement, Siemens Energy will construct and manage the facility, with TC Energy having the option to retake ownership in the future. The facility would collect waste heat from a gas-fired turbine at a pipeline compression station and transform it into emissions-free power. A projected 44,000 tonnes of greenhouse gas emissions will be reduced annually due to the electricity generated being sent back into the grid.

Waste Heat to Power Market Scope: Inquire before buying

| Waste Heat to Power Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2022 | Forecast Period: | 2023-2029 |

| Historical Data: | 2018 to 2022 | Market Size in 2022: | US $ 21.57 Bn. |

| Forecast Period 2023 to 2029 CAGR: | 12.8% | Market Size in 2029: | US $ 49.85 Bn. |

| Segments Covered: | by Technology | Steam Rankine cycle Organic Rankine cycle Kalina Technology |

|

| by End-User Industry | Chemical Oil and Gas Heavy Metals Pipeline Transportation Cement Others |

||

Waste Heat to Power Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Waste Heat to Power Market Key players

The following Waste Heat to Power Companies are the key players in the market and are selected based on criteria for further evaluation. The strategies followed by the companies to sustain and grow in the market are discussed in detail in the report.

1. Siemens AG

2. General Electric Company

3. ABB Group

4. Mitsubishi Hitachi Power Systems Ltd.

5. Ormat Technologies Inc.

6. Thermax Limited

7. Calnetix Technologies LLC

8. Exergy International

9. ElectraTherm Inc.

10. Toshiba Corporation

11. Bharat Heavy Electricals Limited

12. General Electric Power Conversion

13. Hangzhou Steam Turbine Co., Ltd.

14. Nooter/Eriksen, Inc.

15. Dürr Cyplan Ltd.

16. Echogen Power Systems,

17. Aegis Energy Services, Inc.

18. Cain Industries

19. ClearPower Systems Inc.

20. Innovative Steam Technologies

21. Triogen BV

22. Heliex Power Ltd.

23. Turboden S.p.A.

24. Exergyn

FAQs

1. How big is the Waste Heat to Power Market?

Ans: Waste Heat to Power Market was valued at USD 21.5 billion in 2022.

2. What is the growth rate of the Waste Heat to Power Market?

Ans: The CAGR of the Waste Heat to Power Market is 12.8%.

3. What are the segments of the Waste Heat to Power Market?

Ans: There are primarily 3 segments – Technology, End-user, and Geography for the Waste Heat to Power Market

4. Which region has the highest market share in the Waste Heat to Power Market sector?

Ans: North America has the highest market share in the Waste Heat to Power Market sector.

5. Is it profitable to invest in the Waste Heat to Power Market?

Ans: There is a fair growth rate in this market and there are various factors to be analyzed like the driving forces and opportunities of the market which have been discussed extensively in Maximize’s full report. That would help in understanding the profitability of the market