US ENT Devices Market Size by Product Type, Diagnostic Devices, Surgical Device, End User - Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2030

Overview

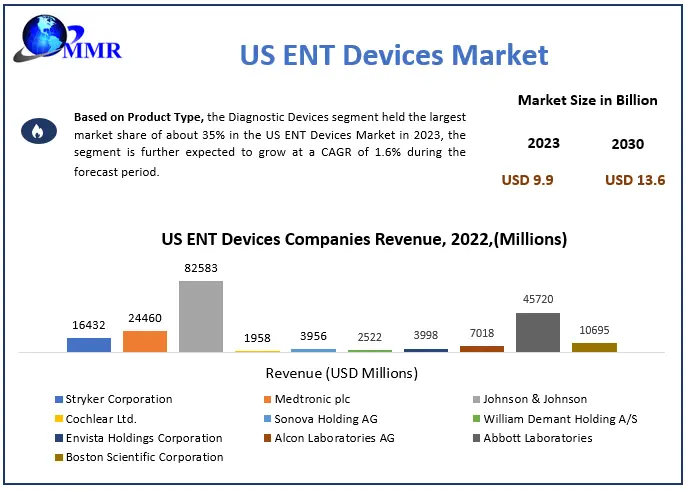

The US ENT Devices Market size was valued at USD 9.9 Billion in 2023 and the total US ENT Devices revenue is expected to grow at a CAGR of 4.64% from 2024 to 2030, reaching nearly USD 13.6 Billion.

US ENT Devices Market Overview:

ENT devices, including otoscopes, nasal endoscopes, and audiometers, are crucial in diagnosing and treating ear, nose, and throat issues that are covered in US ENT Devices market. They are essential tools for comprehensive care and addressing various conditions with specialized equipment such as,

1. Otoscopes are tools for examining the ear canal and eardrum, equipped with a light, magnifying lens, and optional camera.

2. Audiometers assess hearing by emitting sounds of varying frequencies and volume.

3. Laryngoscopes are employed to inspect the larynx (voice box).

4. Rhinoscopes are instruments for nasal examination, featuring a small, flexible tube inserted into the nostril.

5. Nasal sprays and drops effectively alleviate allergies, congestion, and sinusitis

In the US, ENT disorders affect 65.30% of the population. The highest prevalence, 52.8%, occurs across all age groups, with individuals aged 0-19 years following at 12.5%. The 2023 showed a remarkable surge in demand increase in the utilization of ENT Devices, depicting a growing reliance on these technologies for health management.

The report offers an inclusive view of the US ENT Devices market, capturing its current landscape and future projections. The complete report researches the intricate dynamics defining the market, exploring trends, technological breakthroughs, and potential disruptions. It meticulously examines regulatory framework, competitive landscapes, patient demographics, and market positioning to comprehensively understand the sector. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Growing Demand for home-based ENT Monitoring and Treatment Devices to Impact the US ENT Devices Market

The rising demand for home-based ENT monitoring and treatment devices has been composed to significantly impact the US ENT devices market. The increased accessibility allows for broader patient reach and fosters earlier diagnoses and treatment adherence. The cost-effectiveness compared to hospital care attracts a wider consumer base, as well as technological advancements, increasing device sophistication, accuracy, and user-friendliness, bolstering trust and acceptance.

The increasing demand for home-based ENT devices opens avenues for new entrants and prompts established companies to innovate. These fosters increased competition and product diversification, offering consumers a wider array of choices. Also, the existing ENT device manufacturers need to adjust strategies, such as creating new product lines, acquiring startups, or forming strategic partnerships, to meet the rising demand for home-based solutions.

Additionally, navigating the regulatory landscape is crucial to maintaining trust and US ENT Devices market stability, focusing on data privacy, security, and device efficacy. Securing wider insurance coverage and favourable reimbursement policies is essential for the broader adoption of home-based ENT devices. Implementing effective patient education and training programs is necessary to ensure the proper use and interpretation of these devices.

The rising demand for home-based ENT devices is a promising opportunity for the US ENT devices industry. Also, navigating challenges and ensuring responsible development are crucial for maximizing benefits for patients, healthcare providers, and the market.

US ENT Devices Market Segment Analysis

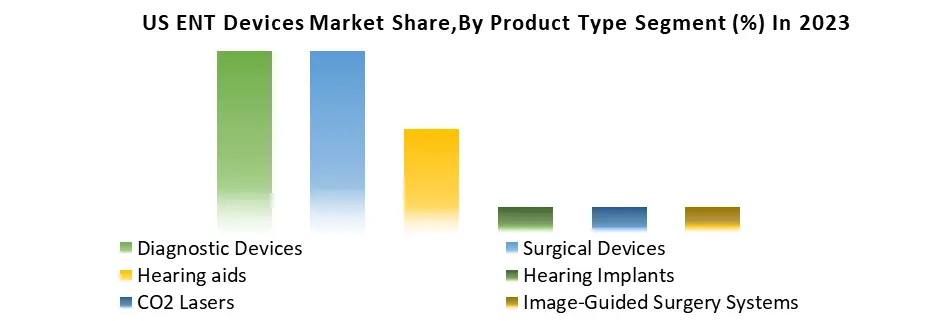

Based on Product Type, the Diagnostic Devices segment held the largest market share of about 35% in the US ENT Devices Market in 2023. According to the MMR analysis, the segment is further expected to grow at a CAGR of 1.6% during the forecast period. It stands out as the dominant segment within the US ENT Devices Market thanks to its rapid technological advancement and growing adoption of smart devices with data connectivity and integration.  The US ENT diagnostic devices market is booming and driven by factors including the rising incidence of ENT disorders such as hearing loss, sinusitis, and allergies. This rise is attributed to factors such as an aging population, environmental pollution, and lifestyle choices. Additionally, technological progress in imaging tools like endoscopes and audiometers allows for quicker and more precise diagnoses, enhancing patient outcomes. There's a growing awareness of ENT conditions, fostering demand for early intervention and diagnostic tools.

The US ENT diagnostic devices market is booming and driven by factors including the rising incidence of ENT disorders such as hearing loss, sinusitis, and allergies. This rise is attributed to factors such as an aging population, environmental pollution, and lifestyle choices. Additionally, technological progress in imaging tools like endoscopes and audiometers allows for quicker and more precise diagnoses, enhancing patient outcomes. There's a growing awareness of ENT conditions, fostering demand for early intervention and diagnostic tools.

Also, the trend toward minimally invasive procedures drives demand for compact diagnostic devices. Telemedicine's ascent opens avenues for remote ENT diagnosis through portable, connected tools. Integration of artificial intelligence enhances diagnosis, test result interpretation, and personalized treatment recommendations in the ENT field, reflecting ongoing advancements in healthcare technology.

The US ENT diagnostic devices Industry faces challenges, including the high cost of equipment limiting patient access. Stringent regulations and prolonged approval processes impede innovation and market entry. The diverse US ENT diagnostic devices reimbursement policies tied to insurance plans pose challenges as well as affecting patient accessibility to specific diagnostic tests and shaping the future landscape of the industry.

US ENT Devices Market Scope: Inquiry Before Buying

| US ENT Devices Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 9.9 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 4.64% | Market Size in 2030: | US $ 13.6 Bn. |

| Segments Covered: | by Product Type | Diagnostic Devices Surgical Devices Hearing Aids Hearing Implants Co2 Lasers Image-Guided Surgery Systems |

|

| by Diagnostic Devices | Endoscopes Hearing Screening Devices |

||

| by Surgical Device | Powered Surgical Instruments Radiofrequency (RF) Handpieces Handheld Instruments Balloon Sinus Dilation Devices ENT Supplies Ear Tubes Voice Prosthesis Devices |

||

| by End User | Hospitals and Ambulatory Settings Home Use ENT Clinics |

||

Leading Key Players in the US ENT Devices Market

1. Medtronic PLC

2. Stryker Corporation

3. Smith & Nephew plc

4. Olympus Corporation

5. Johnson & Johnson

6. Cochlear Limited

7. Sonova Holding AG

8. GN Store Nord A/S

9. William Demant Holding A/S

10. Starkey Hearing Technologies

FAQs:

1. What are the growth drivers for the US ENT Devices market?

Ans. Growing Demand for home-based ENT Monitoring and Treatment Devices etc. are expected to be the major drivers for the US ENT Devices market.

2. What is the major restraint for the US ENT Devices market growth?

Ans. High device costs and limited insurance coverage are expected to be the major restraining factors for the US ENT devices market growth.

3. What is the projected market size & and growth rate of the US ENT Devices Market?

Ans. The US ENT Devices Market size was valued at USD 9.9 Billion in 2023 and the total US ENT Devices revenue is expected to grow at a CAGR of 4.64 % from 2024 to 2030, reaching nearly USD 13.6 Billion By 2030.