Urban Air Mobility Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning / Landscape Review & Global Market Size Forecast to 2034

Overview

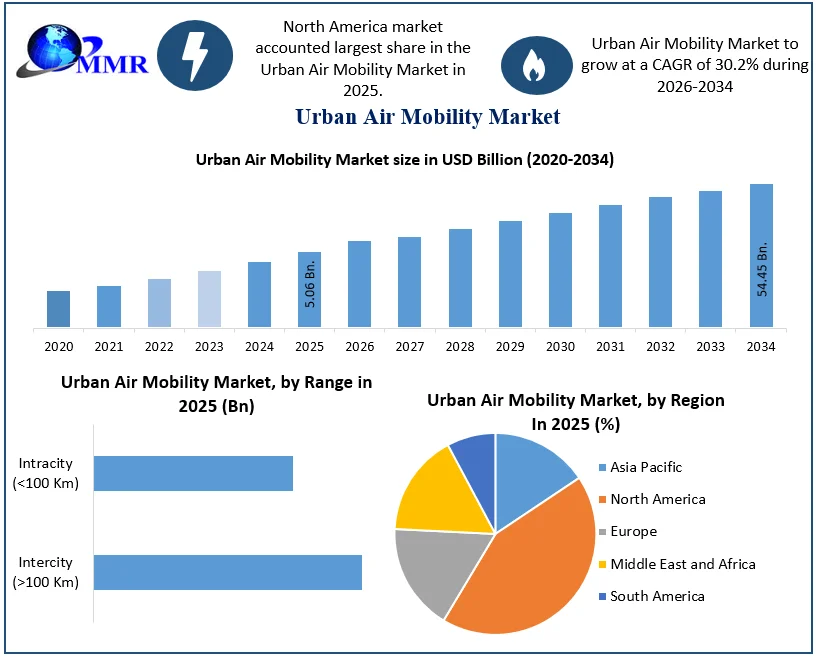

The Urban Air Mobility Market size was valued at USD 5.06 Billion in 2025 and the total Urban Air Mobility revenue is expected to grow at a CAGR of 30.2% from 2026 to 2034, reaching nearly USD 54.45 Billion.

Urban Air Mobility is the transportation of passengers, goods, or services using electric Vertical Take-Off and Landing (eVTOL) aircraft, drones, or other aerial vehicles within urban and suburban areas. UAM's primary goal is to address urban congestion challenges and provide efficient, faster, and eco-friendly transportation alternatives. Urban Air Mobility (UAM) aims to address urban congestion and limited ground infrastructure while providing safe, low-carbon, and convenient transportation options for city dwellers. It is estimated that 60% of the world's population will live in urban areas by 2030, making innovations in mobility solutions crucial. Urban Air Mobility offers a promising solution to overcome these challenges by utilizing the largely untapped airspace above cities. Recent advancements in technology have played a crucial role in enabling Urban Air Mobility.

Airbus a major aerospace manufacturer, has been actively involved in exploring and developing urban air mobility solutions since 2014. In May 2018, Airbus established Airbus Urban Mobility, a dedicated division focused on commercial urban air mobility services and solutions. Airbus Urban Mobility aims to bring safety, convenience, and the joy of flight to urban inhabitants by providing seamless and integrated urban air mobility services. The company takes a holistic approach to urban air mobility by combining various critical components, including cutting-edge aerial vehicles, infrastructure, and digital platforms. Urban Air Mobility represents a transformative concept that can revolutionize urban transportation by providing safe, low-carbon, and convenient aerial transportation options. As cities grow, investing in and developing urban air mobility solutions becomes imperative to meet urban populations' mobility needs efficiently. Successful implementation will require collaboration among industry stakeholders, policymakers, and the public to overcome regulatory, infrastructure, and social challenges.

Urban Air Mobility Market Scope and research methodology:

The scope and research methodology of Urban Air Mobility (UAM) typically covers various aspects, including market segmentation, technology assessment, the regulatory landscape, key player analysis, and future market projections. The research methodology used to study the UAM market involves a combination of primary and secondary research methods. The UAM market covers a wide range of aerial mobility solutions, including electric Vertical Take-Off and Landing (eVTOL) aircraft, passenger drones, cargo drones, and associated infrastructure. Research segments the market based on vehicle type, application (e.g., passenger transportation, cargo delivery, emergency services), and region. The research assesses the latest technologies and innovations related to eVTOL aircraft, propulsion systems, avionics, autonomous flight capabilities, battery technology, charging infrastructure, and enabling technologies. UAM research involves analyzing existing and proposed regulations governing urban air mobility operations.

This includes airspace management, safety standards, certification requirements, and integration with existing air traffic management systems. The research identifies and profiles key players, such as established aerospace companies, start-ups, technology firms, and government initiatives involved in the UAM market. Company profiles typically include information on their products, partnerships, funding, and development progress. Future market projections aim to provide insights into potential growth and revenue opportunities within the UAM industry.

These projections consider factors such as market trends, technological advancements, regulatory developments, and investment activities. Researchers analyze both primary and secondary research data to derive meaningful insights and draw conclusions about the UAM market's size, growth potential, challenges, and opportunities. This is based on historical data and identified market drivers. The research methodology should transparently state any limitations, assumptions, or potential biases that may influence the findings and conclusions. It is essential to acknowledge uncertainties and variables that may impact projection accuracy.

Urban Air Mobility Market Growth and Share Analysis

To know about the Research Methodology :- Request Free Sample Report

Urban Air Mobility Market Dynamics:

The Urban Air Mobility Revolution is the Sustainable Future for City Transportation:

The Urban Air Mobility market is urban congestion in major cities worldwide. As cities grow, traffic congestion becomes a significant challenge, leading to longer commuting times and decreased productivity. UAM offers a solution to this problem by providing an aerial alternative for short- to medium-distance travel, bypassing ground traffic. Commuters typically spend hours in traffic to reach their workplace in a densely populated city. With the growing focus on environmental sustainability, reducing carbon emissions from transportation has become a global priority. UAM, especially electric-powered eVTOL aircraft, and drones, present an eco-friendly option, decreasing emissions and contributing to cleaner urban air quality.

An eVTOL air taxi service powered by renewable energy sources significantly reduces greenhouse gas emissions compared to conventional fossil fuel-driven ground vehicles. Advances in battery technology, electric propulsion systems, lightweight materials, and autonomous flight capabilities have made UAM more feasible and reliable. These technological advancements have attracted investments and accelerated UAM vehicle development.

The development of lightweight composite materials and more efficient electric motors has enabled the creation of eVTOL aircraft with extended flight ranges and improved performance. The increasing interest from aerospace companies, technology giants, and startups in the UAM market has resulted in significant investments and research and development efforts. This has led to accelerated innovation and progress in the sector. Major aerospace manufacturers invest in developing and testing eVTOL prototypes, attracting venture capital funding and propelling the industry forward.

Mobility Apps Have a Long Road Ahead To Mass Adoption, In 2023 (% of people who have used an app for mobility service)

Safety Concerns and Public Trust are Critical Factors for Urban Air Mobility Adoption.

Safety is a paramount concern in the UAM market, given the risks associated with flying vehicles in densely populated urban areas. Robust safety standards and public trust are critical to widespread adoption. A highly publicized accident involving an eVTOL aircraft raises safety concerns and leads to increased scrutiny and regulatory challenges for the entire UAM industry. Integrating UAM into existing airspace and developing appropriate regulations pose significant challenges. Addressing airspace management, air traffic control, and ensuring compliance with existing aviation laws are complex tasks. Different cities or countries have varying regulations and airspace restrictions, making it challenging for UAM operators to navigate smoothly across borders.

Establishing a network of airports and charging infrastructure in urban areas requires substantial investment and coordination with urban planning authorities. Infrastructure lack hinders UAM services' growth. An absence of suitable transport and charging stations in a city may delay the launch of Urban Air Mobility services, affecting its feasibility and adoption. Convincing the general public that UAM is safe, reliable, and beneficial is a challenge. Public perception and acceptance play a crucial role in shaping UAM's operation success. Initial hesitancy by the public to use air taxis due to safety concerns or unfamiliarity with the technology impacts initial adoption rates. Integrating UAM into existing air traffic management systems poses challenges in efficiently managing multiple aerial vehicles in urban airspace to ensure safe operations. Without effective air traffic management, conflicts between UAM vehicles and traditional aircraft occur, leading to safety issues and airspace congestion.

Improving emergency patient transfers through urban air mobility.

Urban Air Mobility opens up new markets and revenue streams for various industries, including transportation, tourism, medical services, and emergency response. An on-demand medical transport service using UAM vehicles could provide faster and more efficient patient transfers between hospitals, saving critical time in emergency. UAM has the potential to significantly reduce emissions and contribute to sustainable urban mobility, aligning with cities' efforts to reduce their carbon footprint. A city with a successful UAM network can significantly decrease greenhouse gas emissions from ground transportation, progressing toward its environmental goals. The development of UAM will drive advancements in autonomous flight, electric propulsion, and air traffic management. Advancements in autonomous flight technology may lead to more reliable and safer UAM operations, promoting its wider adoption in the market.

Urban Air Mobility Market Segmental Insights:

Based on the Platform, In the Urban Air Mobility Market, Air Shuttles and Air Metro dominate the market in 2025 and are expected to grow during the forecast period. Air Shuttles and Air Metro platforms are large-scale aerial vehicles capable of transporting more passengers within urban areas. Air shuttles operate on predefined routes and schedules, while air metros provide more frequent services, similar to traditional mass transit systems. Personal air vehicles are compact aerial vehicles designed for individual use, allowing users to commute between various locations efficiently and independently. Cargo air vehicles are specifically designed for transporting goods and packages, offering faster delivery options for businesses and e-commerce companies.

These specialized aerial vehicles are equipped to provide medical assistance and transportation to patients in emergency, enabling quicker response times and critical care. Last-mile delivery vehicles operate in urban areas and provide efficient delivery of goods to their final destinations, reducing ground-based transportation dependency for last-mile logistics. Air taxis are aerial vehicles designed to transport passengers within urban areas, offering a faster and more convenient alternative to ground transportation. They cater to individuals or small groups, offering point-to-point travel.

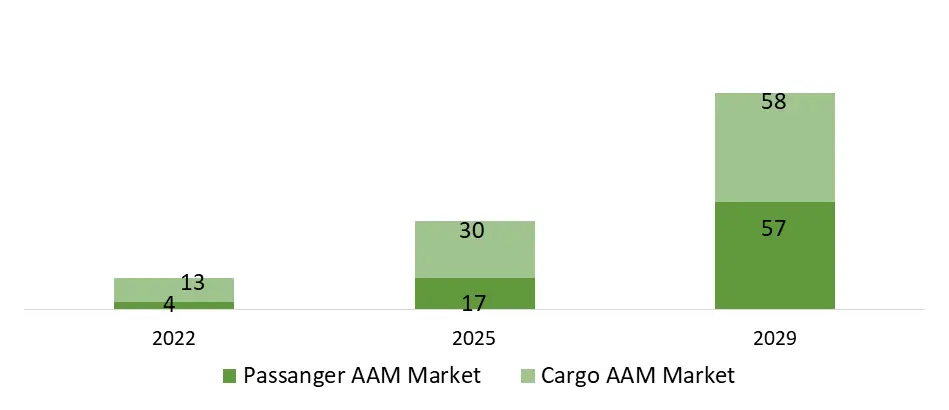

Advanced Air Mobility Market Poised to grow Sevenfold Between 2024- 2030 (US$ billion)

Urban Air Mobility Market Regional Insights:

The Urban Air Mobility (UAM) market is expected to vary significantly across different regions, influenced by factors such as the regulatory environment, infrastructure development, technological adoption, population density, and market demand. North America is one of the leading regions in the UAM market in the year 2025. This is driven by strong government support, technological advancements, and substantial investments from both established aerospace companies and startups. The region has a high concentration of major urban centers with significant traffic congestion, making it an attractive market for UAM services.

Companies like Uber Air pilot air taxi services in cities like Los Angeles and Dallas. This demonstrates the potential for aerial ridesharing in congested urban areas. Delivery companies in the U.S., such as Amazon Prime Air, have been actively exploring the use of UAM platforms for faster and more efficient last-mile delivery of packages to customers. Urbanization and demand for efficient transportation options make personal air vehicles attractive for urban commuters in North America. North America has been at the forefront of developing autonomous technology, making piloted autonomous platforms a critical segment for testing and deployment.

Europe is another significant region in the UAM market, driven by strong regulatory efforts and support from the European Union. The region has a dense network of cities, providing ample opportunities to develop UAM applications. European countries like Germany and France have been actively exploring UAM for medical emergency transportation. This is aimed at reducing response times and improving patient outcomes. Several European cities are exploring the use of UAM air shuttles to connect urban centers and offer efficient transportation for daily commuters. Europe's robust e-commerce industry and emphasis on sustainable logistics create significant potential for cargo air vehicles, addressing the need for fast and eco-friendly last-mile deliveries. Europe is a leader in autonomous technology development, making autonomous platforms a prominent segment of regional UAM deployments.

The Asia-Pacific region presents unique opportunities and challenges for the UAM market. The region's fast-growing urban centers, traffic congestion, and increasing urbanization demand innovative mobility solutions. Countries like Japan and South Korea are exploring the use of UAM platforms for inter-city air shuttles, offering faster and more efficient travel options between major metropolitan areas. High population density and urban congestion in several Asian cities present significant opportunities for air taxis as a feasible transportation solution. The vast distances between major urban centers in the Asia-Pacific region demand UAM platforms capable of efficient inter-city travel.

Urban Air Mobility Market Recent Development

| Date | Company | Development | Impact |

|---|---|---|---|

| 08 January 2025 | Atlantic Aviation | Atlantic Aviation acquired Ferrovial Vertiports from global infrastructure operator Ferrovial to expand its advanced air mobility infrastructure footprint across the United States. | The acquisition accelerates the deployment of dedicated vertiport networks and e-mobility landing hubs required to scale urban air taxi operations. |

| 05 November 2025 | Joby Aviation | Joby Aviation initiated power-on testing for its first FAA-conforming aircraft after entering the final Type Inspection Authorization (TIA) stage of certification. | This milestone enables FAA test pilot flights, moving the company closer to commercial air taxi launch readiness and regulatory type approval. |

| 02 March 2026 | Archer Aviation | Archer Aviation achieved 100% FAA-accepted Means of Compliance for its flagship Midnight eVTOL aircraft. | The full regulatory acceptance clears the pathway for formal compliance testing and supports planned commercial passenger operations. |

| 15 March 2026 | EHang Holdings | EHang Holdings reported full-year 2025 deliveries of 221 autonomous eVTOL aircraft and expanded annual manufacturing capacity to 1,000 units at its Yunfu facility. | The scaled production capabilities significantly enhance commercial availability for unmanned urban air mobility and passenger transport services. |

| 28 March 2026 | Federal Aviation Administration (FAA) | The U.S. government and aviation regulator officially launched the national eVTOL Integration Pilot Program (eIPP) to facilitate pre-certification demonstration flights in controlled airspace. | The initiative accelerates the safe operational integration of urban air mobility platforms into existing national air traffic management systems. |

Urban Air Mobility Market Competitive Landscape

Key Players of the Urban Air Mobility Market profiled in the report include Airbus, Airspacex, Aurora Flight Sciences, Carter Aviation, Embraer SA, Guangzhou EHang Intelligent Technology Co. Ltd, Jaunt Air Mobility Corporation, Joby Aviation Inc., Kitty Hawk, Lilium, Neva Aerospace, Opener, Pipistrel Group, Safran SA, Textron Inc., The Boeing Company, Volocopter GmbH, Wisk Aero LLC, Workhorse Group Inc. This provides huge opportunities to serve many End-uses & customers and expand the Urban Air Mobility Market.

In April 2023, Joby Aviation, Inc., a leading eVTOL aircraft manufacturer, announced the third extension of its contract with the United States Air Force under the Agility Prime program. The contract extension, valued at $55 million, brings Joby's existing contract to $131 million. Joby will continue to provide and operate up to nine of its five-seat aircraft, known for their low noise levels and zero operating emissions.

In March 2023, Lilium Aviation GmbH, a leader in all-electric vertical take-off and landing (eVTOL) jets, forged a strategic partnership with Air-Dynamic SA, a prominent private jet and helicopter company based in Switzerland. Under the definitive agreement, Air-Dynamic SA committed to purchasing up to five Lilium Jets and secured the orders by depositing.

In March 2023, Kakao Mobility, a prominent South Korean mobility technology business, placed a significant preorder for up to 50 units of Vertical's VX4 aircraft. This move expands the number of customer launch regions for Vertical, showcasing the growing interest in electric vertical take-off and landing (eVTOL) technology.

In March 2023, Eve Holding, Inc., an innovator in urban air mobility solutions, signed a Letter of Intent (LOI) with Ferrovial Vertiports, a subsidiary of the world's largest infrastructure operator, Ferrovial. The collaboration aims to explore the implementation of Eve Air Mobility's Urban Air Traffic Management (Urban ATM) software solution. This software will play a crucial role in ensuring the safe and reliable operation of vertiports and electric vertical take-off and landing (eVTOL) aircraft.

Urban Air Mobility Industry Ecosystem

Urban Air Mobility Market Scope: Inquire Before Buying

| Urban Air Mobility Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 5.06 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 30.2% | Market Size in 2034: | USD 54.45 Bn. |

| Segments Covered: | by Platform | Air Taxis Air Shuttles and & Air Metro Personal Air Vehicles Cargo Air Vehicles Air Ambulance & Medical Emergency Vehicles Last-mile Delivery Vehicles |

|

| by Platform Operation | Piloted Autonomous |

||

| by Range | Intercity (>100 Km) Intracity (<100 Km) |

||

| by Platform Architecture | Rotary Wing Fixed Wing Hybrid Fixed Wing |

||

| by End User | Ridesharing Companies Scheduled Operators E-Commerce Companies Hospitals and Medical Agencies Private Operators |

||

Urban Air Mobility Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Urban Air Mobility Market, Key Players

Urban Air Mobility is an industry that involves an efficient and clean transportation system, both passenger and cargo, utilizing electric and hybrid-electric Vertical Take-Off and Landing (eVTOL) aircrafts, through which people can commute between cities. This market covers aircraft production, infrastructure on the ground, and air traffic management systems.

| Company Name | Headquarters | Core Competencies |

| Airbus | Leiden, Netherlands | eVTOL aircraft, urban air mobility, aerospace engineering |

| Archer Aviation Inc. | San Jose, California, USA | Electric air taxis, eVTOL aircraft, commercial UAM solutions |

| Aurora Flight Sciences | Manassas, Virginia, USA | Autonomous aircraft, advanced aviation systems, aerospace R&D |

| AutoFlight | Shanghai, China | eVTOL aircraft, autonomous flight, passenger and cargo air mobility |

| BETA Technologies | South Burlington, Vermont, USA | Electric aircraft, charging infrastructure, aerospace battery systems |

| Embraer S.A. | São José dos Campos, Brazil | Commercial aircraft, advanced air mobility, aerospace manufacturing |

| EHang Holdings Limited | Guangzhou, China | Autonomous eVTOL aircraft, urban air mobility, aerial logistics |

| Eve Air Mobility | São José dos Campos, Brazil | eVTOL aircraft, UAM ecosystem, fleet management solutions |

| Jaunt Air Mobility | Dallas, Texas, USA | Slowed-rotor eVTOL aircraft, advanced air mobility technologies |

| Joby Aviation Inc. | Santa Cruz, California, USA | Electric air taxis, eVTOL aircraft, integrated air mobility services |

| Lilium GmbH | Wessling, Germany | Electric jet aircraft, regional air mobility, eVTOL propulsion |

| Pipistrel | Ajdovščina, Slovenia | Electric aircraft, light aviation, sustainable aviation technologies |

| Safran S.A. | Paris, France | Aircraft propulsion systems, electric propulsion, aerospace equipment |

| Supernal | Fremont, California, USA | Advanced air mobility, eVTOL development, integrated mobility solutions |

| Textron Inc. | Providence, Rhode Island, USA | Rotorcraft, business aviation, advanced aerospace systems |

| The Boeing Company | Arlington, Virginia, USA | Advanced air mobility, autonomous aircraft, aerospace systems |

| Vertical Aerospace | Bristol, England, United Kingdom | eVTOL aircraft, zero-emission aviation, electric flight technologies |

| Volocopter GmbH | Bruchsal, Germany | eVTOL air taxis, urban air mobility platforms, flight services |

| Wisk Aero LLC | Mountain View, California, USA | Autonomous eVTOL aircraft, AI-enabled flight systems, urban air mobility |

| Bell Textron Inc. | Fort Worth, Texas, USA | eVTOL aircraft, rotorcraft, advanced air mobility platforms |

Frequently Asked Questions:

1. What are the growth drivers for the Urban Air Mobility Market?

Ans. The Urban Air Mobility Revolution is the Sustainable Future for City Transportation and is expected to be the major driver for the Urban Air Mobility Market.

2. What is the major restraint for the Urban Air Mobility Market growth?

Ans. Safety Concerns and Public Trust are Critical Factors for Urban Air Mobility Adoption and are expected to be the major restraining factor for the Urban Air Mobility Market growth.

3. Which region is expected to lead the global Urban Air Mobility Market during the forecast period?

Ans. North America is expected to lead the global Urban Air Mobility Market during the forecast period.

4. What is the projected market size & growth rate of the Urban Air Mobility Market?

Ans. The Urban Air Mobility Market size was valued at USD 5.06 Billion in 2025 and the total Urban Air Mobility revenue is expected to grow at a CAGR of 30.2% from 2026 to 2034, reaching nearly USD 54.45 Billion.

5. What segments are covered in the Urban Air Mobility Market report?

Ans. The segments covered in the Urban Air Mobility Market report are Platform, Platform Operations, Range, Platform Architecture, End User and Region.