Steel Long Products Market by Connection Type, Application and Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2034

Overview

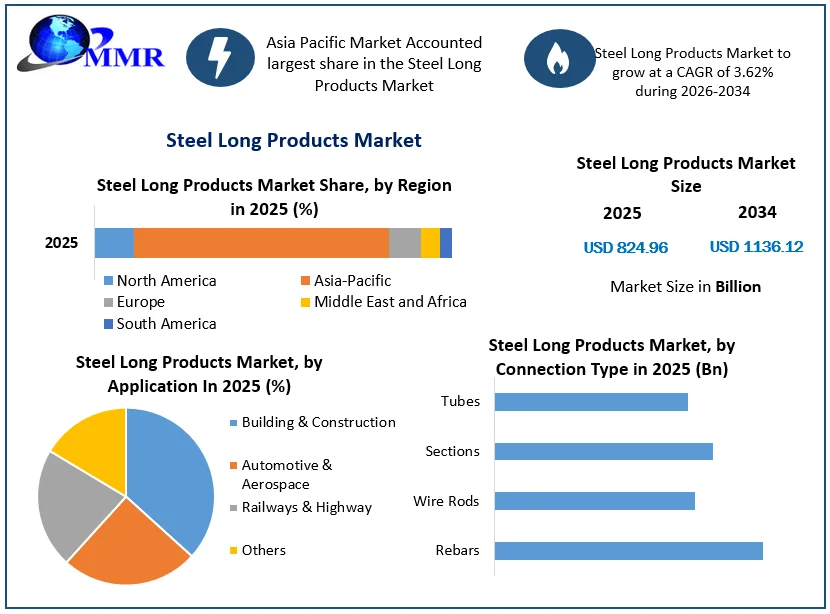

The Steel Long Products Market size was valued at USD 824.96 Billion in 2025 and the total Steel Long Products revenue is expected to grow at a CAGR of 3.62% from 2026 to 2034, reaching nearly USD 1136.12 Billion.

Steel Long Products Definition:

In steel industry, steel long products are products, which includes wire, rod, rail and bars and types of steel structural sections and girders. It also includes hot rolled bar, cold rolled or drawn bar, rebar, railway rails, wire, rope (stranded wire), woven cloth of steel wire, shapes (sections) such as U, I, or H sections. Generally, steel long products find in construction industries, and in capital goods sectors. The steel long products have a capability to absorb the massive amount of heat energy and offer efficient stability in extreme weather condition.

Steel Long Products Market Overview:

Steel industry is the heart of global end-user industries development. It is crucial factor for the development of economy and the backbone of the human civilization. The steel is essential material, which is used in a very wide range of construction applications and products like steel framing, structural steel (beams, channels, angles, etc), reinforcing bar (rebar), wire, roofing and cladding, decking, doors, sashes, windows, ductwork, pipe, fixtures, hardware (hinges, handles, braces, screws, nails, etc), culverts, storm water drains and manhole covers.

The steel long products market growth is driven by factors such as global economic growth, construction activities, infrastructure development, and industrial production. The demand for steel long products is mainly driven by the construction and infrastructure sectors, that account for a substantial share of steel consumption. Rapid urbanization, population growth across developing economies, and the requirement for modern infrastructure are some of the key driving factors behind the steel long products market growth.

Steel Long Products Market Snapshot

To know about the Research Methodology :- Request Free Sample Report

China is a dominant country in both steel production and consumption, followed by other emerging economies. Despite the high demand for steel long products, key players operating in the market faces challenges like fluctuating raw material prices, environmental regulations, and intense competition. Price instability in iron ore and other key raw materials are expected to impact negatively on the profitability of steel manufacturers. Steel manufacturers are focusing on the advanced technologies and processes to enhance production efficiency, reduce costs, and improve product quality.

High adoption of electric arc furnaces, continuous casting, and automation in manufacturing processes are some of the factors that encouraging key players to introduce the innovative products. The steel industry is progressively focusing on sustainability and reducing its environmental footprint. The steel long products market growth is also driven by international trade dynamics, including tariffs, trade policies, and trade disputes. Steel products used in construction account for slightly more than half of Chinese apparent steel consumption. In terms of infrastructure, steel products most typically used are rebar, but sections, plates and rail track are also important inputs

Key Findings of Global Steel Long Products Industry:

World GDP growth is expected to slow down to 3.0% in 2024: Ukraine and Russia are large exporters of key minerals and energy which are dynamic countries for steel production and also for economic growth. A continuation of Russia’s large-scale war against Ukraine, downturn in the Chinese real estate sector, and high inflation pressures that erode household’s purchasing power are some of the key factors behind the slowdown of World GDP growth.

World crude steel long products production declined: The world crude steel production declined sharply falling to 158.1 million metric tonnes in , a 5.9% decrease compared to . Africa and the European Union have experienced sharp double-digit declines in production, with more moderate contractions in South America, Asia and North America

Steelmaking capacity is expected to increase: Despite the steelmaking capacity is expected to increase during the forecast period capacity utilisation is expected to shrink. Global steelmaking capacity are expected to increase to 2 460.8 mmt in while capacity utilisation is expected to decrease from 78.5% in to 77.1% in .

Steel consumption is expected to decline by 2.3% in 2024:

Despite the Energy and commodity price are increasing, inflationary pressure, lower demand from China and political instability are expected to impact negatively on steel demand across the globe.

Steel Long Products Market Competitive Landscapes:

The steel long products market is highly competitive, with several major players operating globally. ArcelorMittal is the largest steel producer globally and has a significant presence in the long products market. The company offers a wide range of long steel products and has a strong distribution network across various regions. POSCO is a leading steel producer based in South Korea and has a notable presence in the long products segment. The company manufactures and sells wire rods, bars, and other long steel products and caters to diverse industries such as automotive, construction, and energy. Nucor Corporation is a prominent steel producer in the United States and has a substantial presence in the long products market.

The company delivers a diverse range of long steel products and is known for its focus on technological innovation and operational efficiency. In India, Tata Steel Long Products Ltd (TSLP), who is a subsidiary of Tata Steel has increased its stake in Neelachal Ispat Nigam Ltd (NINL) for Rs 300 crore. The proposed funding is expected to utilise towards the initial working capital and capex requirement of the company. The company has been focusing on debt reduction for the current financial year. The Narendra Modi government has completed the strategic disinvestment of Odisha-based Neelachal Ispat Nigam Ltd (NINL) to Tata Steel Long Products Ltd (TSLP).

Steel Long Products Market Dynamics:

Global Economic Conditions are expected to drive the demand for Steel Long Products

Global economic conditions play a vital role in driving the demand for steel long products. In the euro area, GDP is expected to grow by 3.3% in and by 0.5% in 2024. In the United States, GDP is projected to grow by 1.8% in and by 0.5% in . Supply disruptions may take some time to fully ease, especially given the impacts of Russia’s war against Ukraine and COVID-related lockdowns in China. The global economy is experiencing growth because of high construction and infrastructure projects. Economic conditions also impact the manufacturing sector, which is a major consumer of steel long products. An industrial production and manufacturing activities are expected to increase. In India, after a strong GDP rebound in , the economy is progressively losing momentum as inflation expectations remain elevated, monetary policy normalises and global conditions deteriorate. According to the research,

Global steelmaking capacity would increase to 2 460.8 mmt in , i.e., by 1.2% (29.5 mmt) from its level that is expected to drive the demand for steel long products. In , crude steelmaking capacity would increase mainly in the Middle East, where an additional 8.6 mmt of capacity is expected to grow that drive the production of the steel long products. The global trade dynamics and government policies also impact the demand for steel long products.

Trade tensions, tariffs, or protective measures have imposed on steel imports are expected to influence the demand for domestically produced steel long products market. The government spending on infrastructure projects, stimulus packages, or industrial policies are also affecting positively the demand for steel long products. The demand for steel long products is closely tied to global economic conditions, including factors such as economic growth, construction activity, infrastructure investment, manufacturing output, and government policies.

Ongoing Construction and Infrastructure Development projects are expected to boost the demand for steel long products.

Many construction and infrastructure development projects can drive the demand for steel long products. Steel long products like bars, rods, beams, and sections, are vital components in many construction applications because of their strength, durability, and versatility. The construction of tall buildings and skyscrapers relies heavily on steel long products. Structural steel beams and columns provide the framework and support for construction structures. Steel long products are widely used in industrial plants like power plants, refineries, and manufacturing facilities and also utilized in the construction of steel structures, platforms, and supports for equipment, offering a robust and reliable infrastructure for industrial operations. ongoing construction and infrastructure development projects have a significant impact on the demand for steel long products.

Merdeka 118, Buffalo Bills Stadium, The Grand Ethiopian Renaissance Dam, Jansen Potash Project, Laguardia International Airport, Samsung Semiconductor Factory, Intel Arizona Semiconductor Plants, Plant Vogtle, Units 3 & 4, Dubailand and California High Speed Rail are top 10 biggest construction projects in across the globe that is expected to drive the demand and production of the steel long products. India is one of the fastest-growing economies across the globe. The infrastructure sector is one of the economic key drivers in India. It is largely responsible for driving the overall economic growth by developing innovative infrastructure projects and upgradation of the old infrastructure projects. The government has also implemented a great deal that is expected to increase the demand of steel long products.

General Economic Downturn is expected to limit the steel long products market growth

Most of the consumer base from the steel industry includes the end user industries like automotive, construction, appliance, machinery, equipment and transportation industries. These industries are negatively affected by the general economic downturn. Many key players are facing some problems like market slowdown in key customers segments in particular the automotive industry and steel industry. The economic environment of the steel business has characterized by persisting economic and geopolitical risk and decline in the demand from automotive industries.

Steel Long Products Market Segment Insights:

Steel Long Products Market Segment Analysis by Product:

Based on the product, the steel long products market is segmented into rebars, wire rods, sections and tubes. Wire rods are long, thin metal rods with a round cross-section, which are mainly used as a raw material in the production of various wire products like fencing, nails, wire mesh, springs, and electrical wires. Steel sections are a variety of structural shapes made from steel like beams, channels, angles, and tees, that sections have specific cross-sectional profiles, which provide strength and stability to structures. Steel sections are widely used in construction, infrastructure development, and engineering projects. Beams are used to support heavy loads in buildings and bridges and angles are used for framing and support structures. Steel tubes are steel pipes, which are forming in cylindrical structures and made from steel. They are commonly used for transporting fluids and gases, and for structural applications.

Steel tubes are available in various shapes and sizes like round, square, and rectangular, depending on the intended and widely utilized in industries like oil and gas, construction, automotive, and manufacturing. Rebars are reinforcing bars, which are usually used in construction projects to offer strength and stability to concrete structures. They are typically entrenched in concrete to enhance its tensile strength and avoid cracking. Rebars are widely used in the construction industry for building foundations, columns, beams, and other structural components. High infrastructure development, smart city development projects across the developing economies are expected to increase the demand for rebars during the forecast period. Rebars held the more than 33% share in the steel long products market in .

By application, steel long products market is segmented into Building & Construction, Automotive & Aerospace, Railways & Highway and Others. In the automotive industry, Steel long products are used in the automotive and aerospace sectors for manufacturing components like engine parts, suspension systems, chassis, axles, drive shafts, and structural frames. High-strength steels are also used to enhance the safety and performance of vehicles and aircraft. The automotive industry also depends on on steel wire rods for tire reinforcement and steel bars for the production of crankshafts, camshafts, and other engine parts. The Automotive & Aerospace segment held the second dominant position in the steel long products product by the analysis of the application segment. Steel long products are vital for the railway and highway sectors, which are used for the construction of railway tracks like rails, sleepers, and fishplates. In the highway industry, steel long products are used for guardrails, barriers, bridge components, and road signposts.

Building & construction segment held the more than 70% share in the global steel long products market Mandatory Road crash barriers on national highway, concretisation, usages of pre-engineered buildings, design changes in urban housing are some of the driving factors that are increasing the demand for the steel long products. The steel industry is one of the bulwarks of rapid infrastructure development. The share of construction in steel long products industry is high at 60-65% in India. Similarly, China and United States have strong share of the construction sector in steel demand, at 50-55% and 40-45% respectively. Japan has low share, which is at 25-30% share in the construction sector. As a manufacturing hub, Japan has witnessed high demand from automotive manufacturing and engineering sector. The steel long products demand from building and construction sector is expected to account for more than 35% share. A global population, urbanization, concretisation projects under the various central and state government are some of the key drivers for the market growth.

Steel Long Products Market Regional Insights:

The European Steel Long Products Industry:

The European steel industry is a world leader in innovation and environmental sustainability. The sector produces on average 160 million tonnes of steel per year at more than 500 steel production sites across 22 EU member states. The steel is the backbone for development, growth and employment in Europe. Steel is the most versatile industrial material in the world. The European steel long products sector is a significant part of the region's steel industry. In March , the EU has imposed sanctions on the Russian steel industry as European countries banned imports of Russian steel that seriously affects its performance as the Russian steel industry is an export-oriented industry. According to the World Steel Association, Russia's steel production fell by 6.6% to 60.4 million tons in that affect the European Steel Long Products.

Asia Pacific region held more than 60% share in the Steel Long Products Market

China Steel Long Products Industry Overview:

In 2025, China's crude steel production was 935 million tons, decreasing by 1.4% YOY according to the

National Bureau of Statistics of China (NBS). China’s steel production is expected to reach at USD xx billion tons in 2025, which will down by 10 million tons. China has a massive production capacity for steel long products. Some of the dominant manufacturers are contributing to the steel long product industry's overall output. The domestic demand for steel long products in China is significant, which is driven by the country's construction boom, infrastructure projects, and industrial growth. An expansion of middle class and urbanization is expected to increase the demand for residential and commercial construction. China is a major exporter of steel long products.

The country's competitive pricing, large-scale production, and extensive manufacturing capabilities are encouraging key players operating in the steel long products market to supply steel long products to various international markets. The Chinese government has implemented numerous policies and regulations to manage the steel long products industry that policies aim to promote energy efficiency, environmental sustainability, and capacity optimization.Chinese steel long product key players are investing in technological advancements and process developments to enhance production efficiency, quality control, and product development and also focusing on innovation to remain competitive in the domestic market.

India Steel Long Products Market:

Steel has contributed immensely towards India’s economic growth. Economic activities have witnessed a sustained recovery in India. As of , India was the world’s second-largest producer of crude steel, with an output of 124.5 MT of crude steel and finished steel production of 117.6 MT. The steel long products industry is witnessing consolidation of key players, which has led to investment by entities from other sectors. The ongoing consolidation also presents an opportunity to global players to enter the Indian steel long products market. In , the government has announced guidelines for the approved specialty steel production-linked incentive (PLI) scheme.

In , the production of crude steel in India stood at 81.96 MT. The India Steel Long Products Market growth is driven by easy availability of low-cost manpower and presence of abundant raw material. The annual production of steel is projected to exceed 300 million tonnes by 2030–2031. In India, more than 67 applications from 30 companies have selected under the Production Linked Incentive (PLI) Scheme for Specialty Steel that will attract committed investment of Rs. 42,500 crore (US$ 5.19 billion) with a downstream capacity addition of 26 million tonnes and also expected to boost the demand for steel long products in India.

In India, the steel industry is a vital part of the country's economic development. The demand for steel long products are steadily growing because of factors like rapid urbanization, industrialization, and infrastructure development. Long steel products are playing a vital role in construction projects like buildings, bridges, railways, and highways. Some of the major key players are operating in the Indian Steel Long Products Market include Tata Steel, JSW Steel, Steel Authority of India Limited (SAIL), Jindal Steel & Power Ltd. (JSPL), and Rashtriya Ispat Nigam Limited (RINL), which have a significant market share and are involved in the production, distribution, and export of steel long products.According to the analysis, the government’s push on infrastructure, primarily in the rural markets, at a distance from the pickup in the local small ticket construction activity are expected to lead to increased offtake from smaller manufacturers during the forecast period.

Steel Long Products Market Scope: Inquire before buying

| Steel Long Products Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 824.96 Bn |

| Forecast Period 2026 to 2034 CAGR: | 3.62% | Market Size in 2034: | USD 1136.12 Bn |

| Segments Covered: | by Connection Type | Rebars Wire Rods Sections Tubes |

|

| by Application | Building & Construction Automotive & Aerospace Railways & Highway Others |

||

Steel Long Products Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Steel Long Products Market Key Players:

1. Baosteel Group

2.Evraz Plc

3. Hyundai Steel

4.JFE Steel Corporation

5.Nucor Corp

6. POSCO

7.Tata Steel

8. United States Steel

9. Emirates Steel Arkan

10. Al-Rasheed Steel

11.Arabian Gulf Steel Industries (AGCI)

12.ArcelorMittal

13. Emirates Rebar Limited

14.Emirates Steel Arkan

15. Hamriyah Steel

16.Jindal Shadeed Steel

17.Rajhi Steel Industries

18. RAK Steel

19.Star International Steel

20.Union Iron and Steel

21. United Gulf Steel

22. Watania Steel Factory

FAQs:

1] What segments are covered in the Global Steel Long Products Market report?

Ans. The segments covered in the Linear Lighting report are based on Connection Type, application and Region.

2] Which region is expected to hold the highest share in the Global Steel Long Products Market during the forecast period?

Ans. The Asia Pacific region is expected to hold the highest share of the Steel Long Products Market during the forecast period.

3] What is the market size of the Global Linear Lighting by 2034?

Ans. The market size of the Linear Lighting by 2034 is expected to reach USD 1136.12 Bn.

4] What is the forecast period for the Global Steel Long Products Market?

Ans. The forecast period for the Steel Long Products Market is 2026-2034.

5] What was the Global Steel Long Products Market size in 2025?

Ans: The Global Steel Long Products Market size was USD 824.96 Billion in 2025.