Solar Bus Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2030

Overview

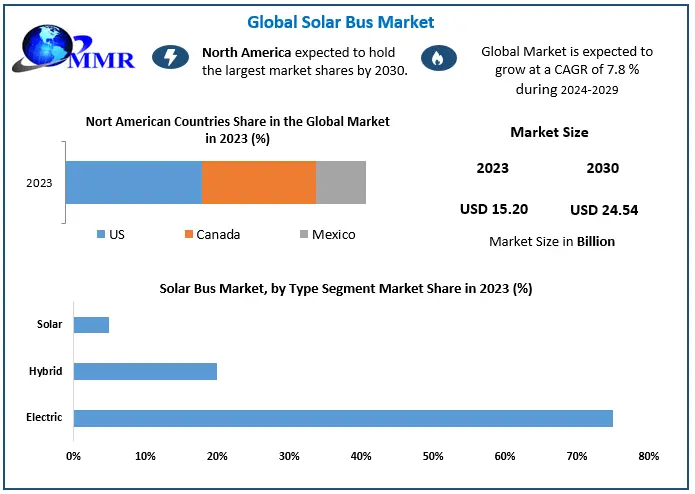

Solar Bus Market was valued at USD 15.20 Bn. in 2023 and is expected to reach USD 24.54 Bn. by 2030, at a CAGR of 7.8% during the forecast period (2024-2030).

Solar Bus Market Overview:

A solar bus is an electric bus in essence powered by solar energy. The buses have solar panels powered by PV (photovoltaic cells), mounted on their roof. The electricity generated is either used to power an electric motor for propulsion or is stored in batteries for later use. Solar-powered buses do not depend on conventional fuel sources like petrol or diesel and produce zero emissions when in use.

Although solar buses are a relatively new invention, they are swiftly gaining acceptance in towns and municipalities around the world as a means of lowering their carbon footprint and improving air quality. Thus, the global solar bus market is expected to grow rapidly during the forecast period. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Solar Bus Market Report scope

The objective of the report is to present a comprehensive analysis of the global solar bus market to the stakeholders in the industry. The report presents the past and current status of the industry with the forecasted market size and trends presented in the report with the analysis of complicated data in simplified language. This report covers all critical aspects of the industry with a dedicated study of key players that includes market leaders, followers, and new entrants.

PORTER, PESTLE analysis with the potential impact of micro-economic factors of the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The report also helps in understanding the global market dynamics, structure by analyzing the market segments and project the global solar bus market size. Clear representation of competitive analysis of key players by product, price, financial position, product portfolio, growth strategies, and regional presence in the global Market make the report investor’s guide.

Solar Bus Market Research methodology

The research methodology used has incorporated both primary and secondary sources. Secondary research is conducted to collect data from existing sources, such as industry reports, academic journals, and online databases. Secondary research aims to collect information about the solar bus market, including its size, growth potential, key participants, and other pertinent data. In addition, primary research is conducted to collect information directly from the market via surveys, interviews, and other techniques.

The research polls potential customers, industry experts, and other relevant stakeholders to determine their perspectives, preferences, and requirements regarding solar-powered buses. After collecting the data, it is analyzed by organizing, summarizing, and interpreting it to identify trends, patterns, and insights. Based on the research query and the data analysis, conclusions and recommendations are drawn from the data analysis. The conclusions are applicable and implementable. Overall, the Solar Bus Market research methodology used for analyzing the market for solar-powered buses includes secondary and primary research, data analysis, deriving conclusions, and making recommendations.

Solar Bus Market dynamics

The solar bus market is influenced by several factors:

Environmental issues: There is a higher demand for sustainable mobility solutions as people become more conscious of the repercussions of air pollution and climate change. Urban air quality can be improved and greenhouse gas emissions can be decreased with the usage of solar buses. Across the globe, numerous governments have put in place regulations and financial incentives to encourage the use of hybrid and electric vehicles, including buses. These regulations include tax breaks, financial aid, and financing for R&D. Solar technology's falling price. As solar technology costs have come down over time, solar-powered buses are now more affordable than conventional buses that are fueled by fossil fuels.

This is especially true in areas with abundant solar radiation, where solar energy can be effectively captured. Since solar-powered buses can produce their power from the sun, they can help cities and municipalities achieve some degree of energy independence. This lessens dependency on fossil fuels and power from the grid. The ability to store energy efficiently because of advancements in battery technology has allowed solar buses to travel farther and be more useful for public transportation systems. Reduced operating costs due to their decreased maintenance needs and lack of fuel expenses, solar buses may have lower running costs than conventional buses. They are thus a desirable alternative for public transport providers aiming to cut expenses.

Solar Bus Market Opportunities

The solar bus market is forecasted to grow in the coming years due to increasing awareness about the need for sustainable transportation, coupled with government policies and incentives promoting the adoption of electric and hybrid vehicles. This presents an opportunity for businesses to offer reliable and cost-effective solar-powered buses. There is space for innovation in solar and battery technology, which can improve the efficiency and reliability of solar-powered buses and provide a competitive edge for businesses.

The market is still relatively untapped in emerging markets, creating an opportunity for businesses to expand their customer base. Moreover, there is an opportunity for businesses to partner with public transportation operators and other stakeholders in the transportation industry to develop sustainable transportation solutions. This can help to build brand recognition and reputation in the market, ultimately driving growth and profitability for businesses operating in the solar bus market.

Renewable energy and EV charging have significant potential synergy. At the level of bulk energy, changing the load of EV charging to more advantageous times of the day might boost consumption and lessen the need to limit transmission-connected renewables, improving the business case.

Restraints:

High upfront costs: Solar buses cost more than fossil fuel-powered buses, which may deter purchasers. This is the key restraint for the solar bus market. Smaller and developing-country enterprises are especially affected. Range limitations: Solar buses generate electricity from sunlight, which limits their range on overcast or rainy days. This makes them unsuitable for extended treks or low-light conditions. Battery technology constraints: Despite recent advances, battery technology still has inherent limitations. Batteries are bulky and expensive to replace. Solar-powered buses may not have charging outlets or maintenance facilities in some places. Operators may find solar bus adoption harder. Tax rebates and R&D funding drive the solar bus business. These policies and political will might affect market growth.

Global Solar Bus Market Regional Analysis

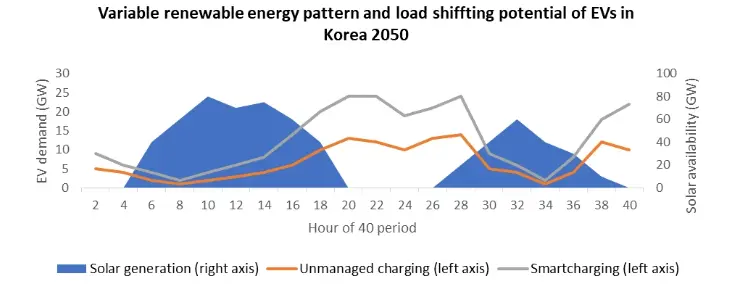

In Korea, the utilization of flexible EV charging methods may lead to a decline in peak prices by USD 18/MWh and operating expenses by USD 21/MWh for the estimated 30% EV fleet in 2035. This equates to a decrease of 30% and 21%, respectively. Furthermore, if all vehicles were electric and flexible charging practices were implemented, emissions could be slashed by 63%. Additionally, renewable energy producers could see an enhancement in their business case by syncing EV charging with renewable energy availability to lessen curtailment. Synergies could also be found at the distribution level. There are areas that have experienced high local voltage because of their rooftop solar PV usage. This happens because energy is injected without the demand matching. Currently, this tends to occur on sunny weekends where there is strong PV generation but low consumption.

Conversely, charging EVs concurrently during evenings when consumption is high could produce low voltage (undervoltage) instead. Within the voltage restrictions, there is the opportunity to enhance mutual hosting capacity within distribution grids by coordinating the delivery of solar PV and EV charging. A recent study conducted in Sweden showed that coordinating the operation between distributed PVs and EVs with the help of a management system could further increase their combined penetration into the grid. This is expected to drive the solar bus market in Sweden during the forecast period. Essentially, this means that working within these voltage restrictions can help maximize the potential of these two systems working together.

Electric vehicle (EV) charging integration could be a potential advantage for policymakers who seek to speed up renewable energy adoption and electric mobility. By planning the marginal load, clean power can be generated to meet the needs of the EVs. This strategy ensures that as people transition from internal combustion engine vehicles (ICEVs) to EVs, the decarbonization of transportation activity occurs more effectively. Coordinated efforts are necessary to make this happen.

Solar Bus Market Segmentation

Solar Bus Market Segmentation

Sunny areas such as tropical or subtropical regions are more likely to send solar buses. The Solar Belt in the United States, South Asia, Southeast Asia, and South America are examples of areas with great potential to use solar energy for transportation. Demographic Segmentation: Environmentally conscious consumers, such as environmentally conscious youth, may find solar-powered buses attractive. Demographic factors such as age, income level, education level and safety attitudes can be used to segment businesses. Psychological Segmentation: A person's values or lifestyle will be what motivates them to drive a solar bus. For example, someone who prefers to live in a fixed location or who prefers public transport rather than owning a car could be a possible group.

Classifying people according to their values, interests, and perceptions of transportation can create psychological segmentation. Segmentation based on usage: solar powered buses can be used for a variety of purposes, including public transportation, airport shuttles and passenger transportation. The use of buses and the specific needs and requirements of each group can form the basis of Solar Bus market segmentation. Behavioural Segmentation: Consumer confidence, bus usage frequency, and willingness to pay for a solar bus can be used to construct behavioural segmentation. This can make it easier for companies to target specific customers with their marketing plans and products.

Solar Bus Market Competitive Landscape

Mainland China dominates the global e-bus market

In 2030, it is estimated that there will be 1.9 Billion electric buses worldwide, according to a report by Maximize, of which Mainland China will be holding a share of more than 95%. About 30.1% of the entire Chinese bus fleet comprises of E buses as of 2023, with pure electric buses decisively dominating plug-in hybrid buses. There are 5 primary factors that contribute to China’s market dominance:

1. Financial support: Strong government support in the form of subsidies, led to a rise in adoption E- Vehicles as it was cheaper in comparison with a traditional vehicle.

2. International trade: The Chinese government's fervent backing for the sector also results from its ambition to build domestic businesses that can lead their respective markets abroad.

3. Big urban population and the associated pollution: Population the primary factor in the rising pollution levels in the nation. The politicization of this problem led to prompt government intervention and the adoption of regulations in favour of electrifying the whole network of public transit.

4. Lack of legacy transportation infrastructure: Many Chinese cities have the luxury of building entirely new public transportation networks, which makes the task much easier. This contrasts with Europe and the U.S., which are attempting to integrate electric buses into their complex existing public transportation infrastructure.

5. Greater public awareness: While mainland China has been taking action to reduce air pollution for several years, the Volkswagen diesel emissions crisis was the catalyst for a significant increase in public awareness of air pollution in Europe.

Solar Bus Market Scope: Inquire before buying

| Global Solar Bus Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 15.20 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 7.8% | Market Size in 2030: | US $ 24.54 Bn. |

| Segments Covered: | By Type | Electric Hybrid Solar |

|

| By Drive Mechanism | Hub motor Mid-drive Others |

||

| By Battery | Lead-acid Lithium-ion Nickel-metal hydride (NiMH) Other |

||

Global Solar Bus Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Solar Bus Market Key Players are

1. Solaris (Poland)

2. VDL Bus & Coach (Netherlands)

3. Mercedes-Benz (Germany)

4. Iveco Bus (Italy)

5. Ebusco (Netherlands)

6. Van Hool (Belgium)

7. Volvo (Sweden)

8. Hyundai Motor Company (South Korea)

9. Mitsubishi Fuso Truck and Bus Corporation (Japan)

10. King Long United Automotive Industry Co., Ltd. (China)

11. Ankai Bus (China)

12. BYD (China)

13. Zhongtong Bus (China)

14. Yutong (China)

15. Tata Motors (India)

16. Lion Electric Company (Canada)

17. Blue Bird Corporation (USA)

18. GreenPower Motor Company Inc. (Canada)

19. Nova Bus (Canada)

20. Proterra (United States of America)

21. Volare (Brazil)

22. Agrale (Brazil)

23. Abu Dhabi National Oil Company (ADNOC) (UAE)

24. Al Naboodah Group Enterprises (UAE)

25. Ashok Leyland (UAE)

26. Yutong Bus Middle East FZE (UAE)

27. Foton (UAE)

28. Golden Dragon (South Africa)

29. China FAW Group Corporation (South Africa)

30. Yutong (South Africa)

31. MAN Truck & Bus (South Africa)

32. Scania AB (South Africa)

FAQs:

1. What is the current state of the market for photovoltaic buses?

Answer: The current state of the solar bus market varies by region, but it is expanding overall. The largest market is in the Asia-Pacific region, with China being the largest contributor, followed by Europe and North America.

2. What are the primary growth drivers for the solar bus market?

Answer: Increasing concerns about climate change and air pollution, government incentives for renewable energy and green transportation, and technological advancements that have made solar-powered buses more efficient and affordable are the primary growth drivers.

3. What are the most significant obstacles confronting the solar bus market?

Answer: Among the most significant obstacles are the high initial costs of solar-powered buses, the limited availability of charging infrastructure, and concerns about solar-powered buses' dependability in extreme weather conditions.

4. What are the most common varieties of solar-powered buses on the market?

Answer: There are two primary varieties of solar buses: fully electric buses with a solar charging system and hybrid buses that combine a conventional combustion engine with solar charging.

5. What is the nature of competition on the photovoltaic bus market?

Answer: The competitive landscape is diverse, with both established bus manufacturers and emerging companies specialising in solar-powered buses. BYD, Proterra, Solaris, and Yutong are some of the major participants on the market.

6. What pricing and financial models apply to solar-powered buses?

Answer: Solar buses are priced differently based on factors such as bus dimensions, battery capacity, and charging infrastructure. The available financing options include outright purchase, leasing, and power purchase agreements (PPAs), which enable customers to pay for the solar energy generated by the bus rather than the bus itself.

7. What are the possible environmental advantages of solar-powered buses?

Answer: Solar-powered buses have the potential to reduce greenhouse gas emissions and air pollution significantly when compared to conventional diesel buses. In addition, they can reduce dependence on fossil fuels and encourage the use of renewable energy.

8. What are the most important factors to consider when entering the photovoltaic bus market?

Answer: Key considerations include understanding the regulatory environment and government incentives in various regions, identifying potential manufacturing and distribution partners, and ensuring adequate funding for initial costs.