Smart Home Devices Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

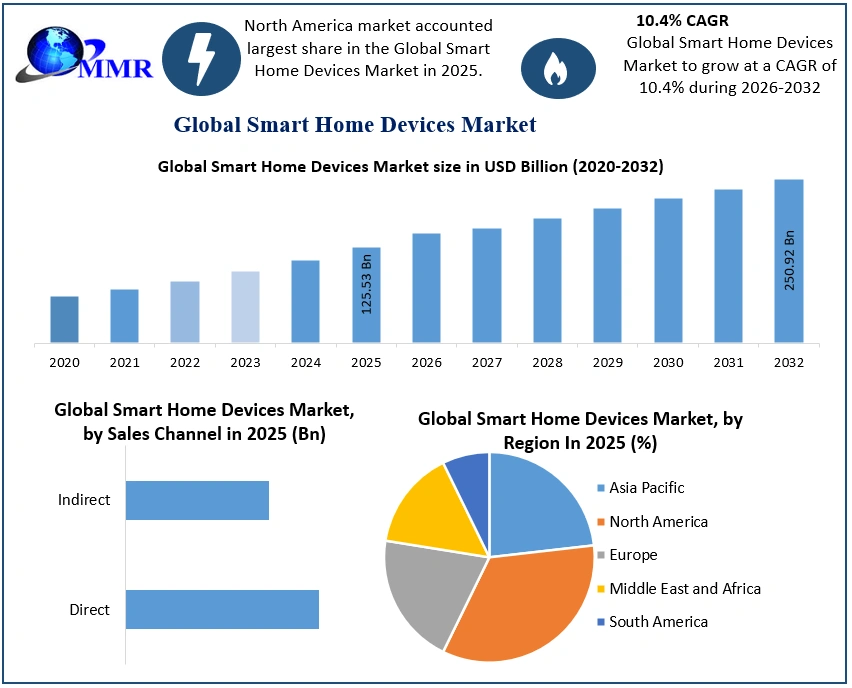

The Smart Home Devices Market size was valued at USD 125.53 Billion in 2025 and the total Smart Home Devices revenue is expected to grow at a CAGR of 10.4% from 2026 to 2032, reaching nearly USD 250.92 Billion by 2032.

Smart Home Devices Market Overview:

The increasing importance of home monitoring in remote locations, as well as growing concern about safety, security, and and convenience among the general population, as well as the growing number of internet usersand and rising acceptance of smart devices, as well as the increasing need for energy-saving and low carbon emission-oriented solutions, have all contributed to increased demand for smart home systems.

To know about the Research Methodology:- Request Free Sample Report

Smart Home Devices Market Dynamics

Increased internet usage and smart device adoption are driving factors:

The internet of things (IoT), has gained popularity among residential customers because of the advantage of connecting common household items to the internet. and It simply connects electronic items, software, algorithm and the end user allowing data to flow freely in real-time to make convenient choices in day to day activity.

It has proven to be effective in improving the quality and consistency of automation systems. Several large, mid-size and small businesses are heavily investing in the Internet of Things. With most organizations transitioning to IoT, it is likely to reach a wide range of application sectors, including lighting, HVAC, security, healthcare, and entertainment.

The increasing customer preference for video doorbells, voice-assisted technology (such as Alexa and Google Home), and surveillance systems is likely to propel the smart home market forward. The expanding penetration of the internet, the growing use of smartphones, and the expansion of social network platforms are all factors driving consumer IoT adoption. Because of the increased usage of internet-enabled smart devices like radio frequency identification (RFID), barcode scanners, and mobile computers, the entire market for IoT is expected to grow. In the last 10–15 years, the internet penetration rate has risen dramatically, particularly in industrialized nations such as North America and Europe. According to Internet World Stats, North America and Europe had penetration rates of 93.9 % and 88.2 % in March 2022, respectively; Asia and Africa had penetration rates of 63.8 % and 43.2 %, respectively.

Restraint: Concerns about security and privacy violations:

A smart house collects data on energy use, bills, purchases, movements, and music preferences, among other things, so that its systems may be tailored to best support the residents' lifestyle. Common hacking tools may be vulnerable to smart home devices. Because personal information, physical safety, medical care, and houses are all stored virtually on the cloud, the risk of hackers misusing this information is high. A hacked monitor could provide hackers access to other personal data and information, which could then be utilised to harm a user or a household.

Consumers' personal information must be kept secure and secret, which is a challenge for the smart home business. It is critical to protect the secrecy of the information saved while remotely controlling security services; the control of a network's security systems cannot be compromised. This is projected to limit market expansion in several ways. Furthermore, data created by unsecured wearables and smart appliances provides cyber attackers with a large amount of targeted personal data that can be used for fraudulent transactions and identity theft. The theft of a smart gadget has the ability to jeopardise the safety of an entire home.

An attacker can take control of a device by hijacking it. As the attacker does not change the device's vital functionality, these attacks are difficult to detect. Furthermore, one gadget has the potential to infect all smart devices in the home. An attacker who compromises a regulator, for example, might hypothetically get access to a whole network and remotely unlock a door or change the keypad PIN code to prevent entry.

Incorporation of lighting controllers with built-in data connectivity:

Over the last few years, the lighting control market has grown significantly. Dimmers, timers, occupancy sensors, daylight sensors, and relays are among the goods available in this sector. These products can be used separately or in conjunction with each another. Through wired and wireless technologies, they can be integrated with home automation systems. Lighting controllers must be externally integrated with communication protocols to enable automated operations. Lighting control makers, on the other hand, are increasingly producing solutions with built-in data communication. Without the use of external communication protocols or connectivity, these controllers can be functioned directly. This is expected to result in a significant increase in demand for such items, providing potential for smart home market participants.

The use of the Internet of Things (IoT) as the backbone for connected lighting systems enables seamless communication, contextual services, and data exchange across devices, resulting in significant changes in the sectors as a result of the convergence of numerous vertical markets. Increased control capabilities (e.g., switching and dimming) and lower operational expenses and energy usage are possible with LED-based systems. Incorporating IoT and connectivity into lighting systems ushers in a new era with a slew of new prospects and value propositions. The Internet of Things is rapidly maturing, making it economically feasible to link each luminaire to the Internet. As a result, now is a great time to launch the Internet of Lights, which is an improved lighting system with IoT at its heart.

Device failure is a possibility:

Device inter connectivity standards, communication protocols, and network technologies are all critical components of smart home systems. The interoperability of all devices is critical to the operation of smart home goods. The hardware, software, and service components make up the smart home ecosystem. The smooth and cooperative operation of all three segments is critical for the efficient and reliable operation of every single product. Any of these three failing or becoming disconnected can cause a slew of problems for homes in terms of expense and technical complexity. As a result, eliminating the risks of device malfunction and ensuring their seamless operation is a key task for smart home solution suppliers.

Despite the wide range of gadgets that enable Alexa, Google Assistant, and, to a lesser extent, Apple, Microsoft, and Samsung's voice assistants, the promised land of whole-home automation remains elusive for the majority of customers. Smart home device manufacturers, on the other hand, are entering into collaboration or partnership agreements with software and connectivity technology providers to develop innovative offerings tailored to the market, which could help them overcome the challenge of interoperability and reduce the likelihood of device failure. Vivint and Ring are two security-focused smart home solutions that are frequently paired with subscription plans for monitoring and video storage. These systems offer a well-integrated experience, but their capacity to add devices from other brands is usually limited.

In 2024, the major market for smart homes was entertainment and other controls:

During the forecast period, the entertainment and other controls sector is likely to hold the greatest share of the smart home market. The ease afforded by these controllers for managing and controlling entertainment systems within a house is driving the expansion of the audio, volume, and multimedia room control industry. Wireless communication technology improvements are a crucial component driving the home theatre system control business, and hence the smart home market for entertainment control. The increasing demand for smart meters and smoke detectors, as well as the rising popularity of smart plugs, smart hubs, and smart locks, are driving the market expansion of the other control sector.

Behavioral software will have the biggest market share during the forecast period;

Energy-related data is analysed and forwarded to end users using behavioral software and services. End users receive direct feedback from behavioral solutions, which include basic information on real-time energy consumption statistics as well as historical data on energy usage. Behavioral type software and services are rapidly being used in smart homes because they help improve energy efficiency and lower energy bills by analyzing behavioral type data. Behavioral software and services have the ability to learn user behaviour and, as a result, provide smarter appliance control, resulting in a rise in demand. Due to its initial popularity and low cost, this form of software and algorithm is likely to account for a higher part of the smart home market during the forecast period.

In 2024, the indirect sales channel will have the biggest market share for smart homes:

The indirect sales channel sector is likely to take the lead in the smart home market. Smart home devices are sold in both online and offline ways through indirect sales channels. Third-party cellular network carriers, wholesalers, retailers, and value-added resellers are examples of offline sales channels. E-commerce systems are used for online sales channels. In the smart home industry, the COVID-19 epidemic has led to an increase in the use of indirect sales channels.

People have begun to use online mode more regularly as a result of lockdowns in many places throughout the world. During the pandemic, demand for internet outlets has skyrocketed. Companies provide product setup and installation services, allowing customers to buy things online with confidence. Furthermore, third-party delivery companies have begun to take extra steps in order to encourage customers to buy without fear of becoming infected. As a result, during the forecast period, the internet sales channel segment is expected to rise.

In 2024, North America will have the biggest market share for smart homes:

The high per capita income in North America, the growing demand for reliable home energy management systems, improved home security levels, improved device standards, and the growing popularity of integrating smart devices like tablets, smartphones, and standalone voice assistants in homes are all driving the growth of the North American smart home market. Furthermore, the US government's different awards for green energy projects are propelling the smart home market in this region forward.

The objective of the report is to present a comprehensive analysis of the Smart Home Devices Market to the stakeholders in the sales channel. The past and current status of the sales channel with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the sales channel with a dedicated study of key players which include Market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the Market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the Sales Channel to the decision-makers.

The report also helps in understanding the Smart Home Devices Market dynamics and structure by analyzing the market segments and projecting the Smart Home Devices Market size. A clear representation of competitive analysis of key players by product type, price, financial position, Product Type portfolio, growth strategies, and regional presence in the Smart Home Devices Market make the report investor’s guide.

Smart Home Devices Market Scope: Inquire before buying

| Smart Home Devices Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 125.53 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 10.4% | Market Size in 2032: | USD 250.92 Bn. |

| Segments Covered: | by Product Type | Lighting Control Security & Access Control HVAC Control Smart Speaker Smart Kitchen Smart Furniture |

|

| by Sales Channel | Direct Indirect |

||

| by Software & Services | Behavioral Proactive |

||

Smart Home Devices Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Smart Home Devices Market, Key Players:

1. Honeywell (US)

2. Siemens (Germany)

3. Johnson Controls (Ireland)

4. Schneider Electric (France)

5. ASSA ABLOY (Sweden)

6. Amazon (US)

7. Apple (US)

8. ADT (US)

9. ABB (Switzerland)

10. Robert Bosch (Germany

11. Sony (Japan)

12. Samsung Electronics (South Korea)

13. Crestron Electronics (US)

14. Legrand (France)

15. Others

FAQ’S:

1. Which region has the largest share in Global Smart Home Devices Market?

Ans: North America region holds the highest share in 2025.

2. What is the growth rate of Global Smart Home Devices Market?

Ans: The Global Smart Home Devices Market is growing at a CAGR of 10.4% during forecasting period 2026-2032.

3. What is scope of the Global Smart Home Devices market report?

Ans: Global Smart Home Devices Market report helps with the PESTEL, PORTER, COVID-19 Impact analysis, Recommendations for Investors & Leaders, and market estimation of the forecast period.

4. Who are the key players in Global Smart Home Devices market?

Ans: The important key players in the Global Smart Home Devices Market are – Honeywell (US), Siemens (Germany), Johnson Controls (Ireland), Schneider Electric (France), ASSA ABLOY (Sweden), Amazon (US), Apple (US), ADT (US), ABB (Switzerland), Robert Bosch (Germany, Sony (Japan), Samsung Electronics (South Korea), Crestron Electronics (US), Legrand (France) and Others.

5. What is the study period of this market?

Ans: The Global Smart Home Devices Market is studied from 2025 to 2032.