Smart Contracts Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2030

Overview

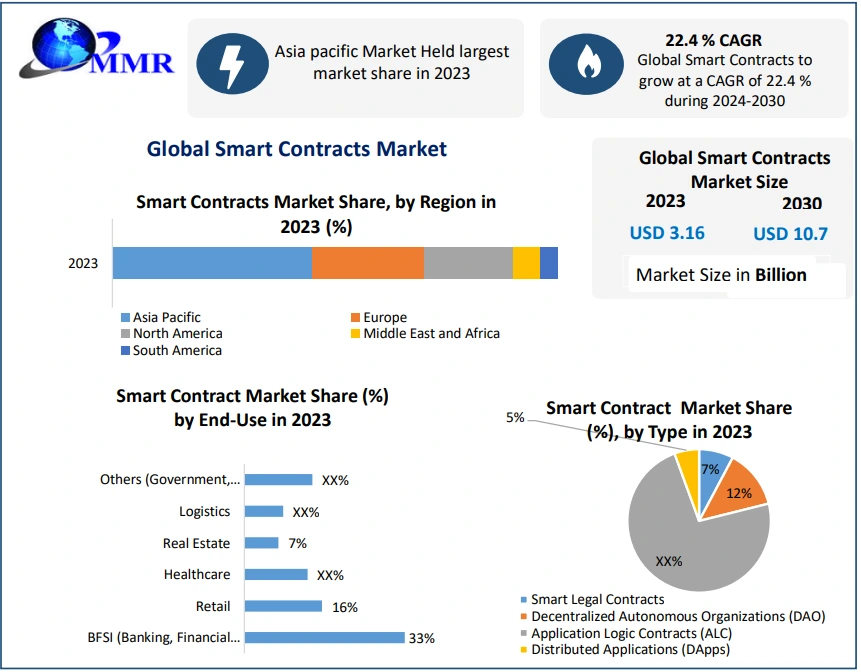

The Global Smart Contracts Market size was valued at USD 3.16 Bn in 2023 and is expected to reach USD 10.7 Bn by 2030, at a CAGR of 22.4%.

Smart Contracts Market: Overview

A smart contract is a digital contract that is self-executed and operated on a block chain platform. They are mainly formed to facilitate, verify and enforce the performance of the contract in a secure and transparent manner. The Smart Contracts Market is experiencing significant growth majorly because of increasing adoption across various industries. The report includes a detailed analysis of the technological developments that are contributing to the growth of the market. It also includes an in-depth analysis of market trends with market size, market share, regional insights, competitive landscape and market segments.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Smart Contracts Market Drivers and Opportunities

Smart Contracts operate on blockchain technology. This provides a decentralized and transparent ledger. The audibility and immutability of blockchain ensure that the terms and execution of smart contracts are visible to everyone, which foster thrust and reduce dispute. By eliminating the need for intermediaries, manual processing and paper workflow, the smart contracts automate contract execution. This automation reduces human error, improves efficiency and streamlines processes, which leads to cost savings and increase in productivity. They also eliminate the need for intermediaries such as brokers, lawyers or escrow agents.

This helps to reduce costs associated with their services. Smart contracts reduce transaction costs by automating contract enforcement and reducing administrative overhead. They execute actions automatically once predefined conditions are met. This eliminates the need for manual intervention and reduces the time required to complete contractual processes, which makes transactions faster and more efficient. All these factors are majorly driving the growth of the market. The increasing advancements in blockchain technology such as interoperability solutions, scalability improvements and smart contract platforms are mainly contributing to the smart contracts market growth.

The increasing demand for smart contract experts is creating an opportunity for educational institutions and training programs to offer courses and certifications focusing on smart contracts. Developing a skilled workforce that understands smart contract development, auditing and implementation is expected to drive the global market growth during the forecast period. The combination of smart contracts with Internet of Things (IoT) devices also offer new opportunities for the Smart Contracts Market growth. Smart contracts automate and facilitate transactions, agreements and data exchanges between interconnected devices. This enables autonomous and secure interactions within IoT ecosystems. This convergence creates various possibilities in areas such as logistics, supply chain management and smart cities.

Smart Contracts Market Restraints and Challenges

The scalability of smart contracts is a major challenge for market growth. As blockchain networks are increasing in size and transaction volume, scalability issues are expected to arise, which leads to an increase in transaction costs and slower processing times. It is very important to solve scalability challenges for the huge adoption of smart contracts in high-volume industries. Even though blockchain technology provides inherent security features, smart contracts still can be vulnerable to coding errors, hacking and security breaches. Vulnerabilities in smart contracts lead to financial loss or exploitation. To mitigate risks, it is important to ensure security measures and auditing of smart contracts. The lack of standards that are widely adopted and best practices for the development of smart contracts is expected to hinder interoperability and increase the risk of inconsistent implementations in the future.

Smart Contracts Market Regional Insights

The North American Smart Contracts Market held the major share of the global market in 2023. The United States and Canada are the hubs for blockchain technology and smart contract development. It has a well-established ecosystem of blockchain startups and research institutions with the presence of Smart Contracts key players. New York City, San Francisco and Toronto are the main cities known for their high focus on blockchain and cryptocurrency companies. In the region, the adoption of smart contracts is rising in many industries such as finance, healthcare, supply chain management, real estate and others. The robust tech ecosystem with a highly skilled workforce is also driving regional market growth.

The Asia Pacific Smart Contracts Market has emerged as a major region with China, Japan, Singapore and South Korea contributing largely to the regional market growth. China has made significant strides in blockchain technology. It has an ecosystem of blockchain startups and projects exploring smart contracts. The Chinese government has launched initiatives such as the Blockchain Service Network (BSN) to facilitate the adoption of blockchain technology including smart contracts in various industries, which is expected to largely contribute to the growth of the market in the future. Singapore is a global blockchain hub that is promoting the adoption of smart contracts through initiatives like Project Ubin. The Monetary Authority of Singapore (MAS) is continuously exploring the use of blockchain technology including the blockchain-based payment system development that incorporates smart contracts.

European Smart Contracts Market has been growing rapidly in the past few years. It is also expected to continue growing during the forecast period. This growth of the regional market is majorly because of the rising adoption of smart contracts in the countries such as Germany, the UK, Switzerland and Estonia. The initiatives taken by European Union such as European Blockchain Partnership aim to create a unified approach to blockchain adoption including smart contracts. The cities like Zug in Switzerland, often referred to as “Crypto Valley” are home to the ecosystem of blockchain companies working on the development of smart contracts.

Smart Contracts Market Segment Analysis

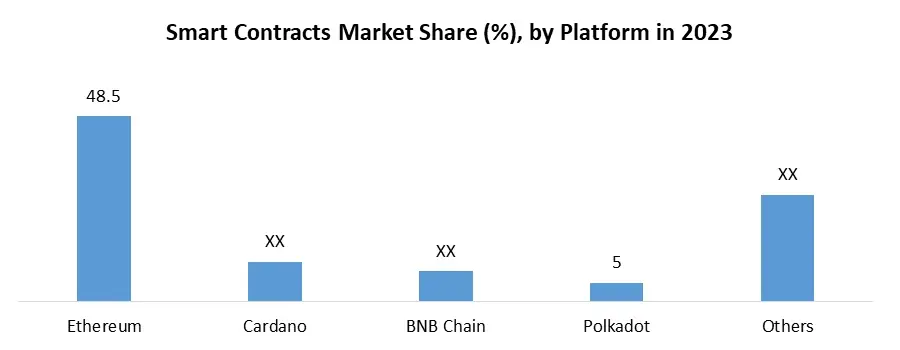

Based on Platform,

In 2023, Ethereum dominates the Smart Contracts Market with a 48.5% global share. Its first-mover advantage, established smart contract functionality, and a robust developer community contribute significantly to its leadership. Ethereum's maturity, stability, and extensive track record instill user confidence, while the diversity of decentralized applications (dApps) across sectors like DeFi, NFTs, DAOs, and gaming further solidify its position. The Solidity programming language tailored for Ethereum enhances accessibility for developers. Despite emerging platforms like Cardano, BNB Chain, and Polkadot gaining traction, they face challenges such as being newer entrants, technical limitations, and niche-focused functionalities, preventing them from surpassing Ethereum's dominance. The dynamic landscape, shaped by technological advancements and evolving use cases, underscores the potential for market share shifts in the future.

Based on Contract Type,

Based on Contract Type,

Determining the single largest market share segment in smart contracts based on specific contract types, such as Smart Legal Contracts, DAOs, Application Logic Contracts (ALC), and Distributed Applications (DApps), proves challenging due to various factors. Data scarcity remains a primary hurdle, as market research reports typically focus on broader categorizations like platforms or application categories, rarely delving into specific functionalities. Overlapping functionalities further complicate the issue, as contract types often blend aspects, making clear market share divisions elusive. The rapidly evolving landscape, especially with emerging contract types like DAOs, adds another layer of complexity, rendering historical data less reliable.

Despite these challenges, insights into each category offer a glimpse into their potential market impact. Smart Legal Contracts, although facing regulatory hurdles, hold promise for automating legal processes. DAOs, gaining traction in governance and fundraising, exhibit considerable growth potential. ALC, integral to many decentralized applications (dApps), likely hold a substantial, albeit challenging to quantify, market share. DApps, encompassing various contract functionalities, present a nuanced understanding when analyzed within specific categories like DeFi or NFTs. While pinpointing the exact leader based on specific contract types is challenging, DAOs and ALC show high-growth potential. As the smart contract market evolves and data becomes more granular, a clearer picture of market share distribution based on contract functionalities is anticipated. The dynamic nature of the smart contract landscape promises continual evolution, with exciting developments shaping the future of blockchain technology applications.

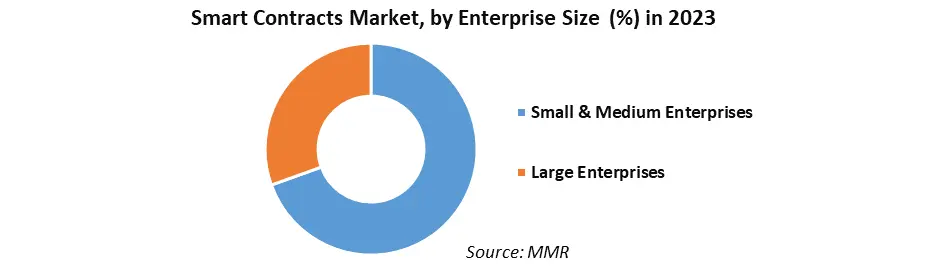

Based on Enterprise Size: The market is segmented into Small & Medium Enterprises and Large Enterprises. The Large Enterprises segment held the largest Smart Contracts Market share in 2023. Large enterprises possess the financial resources necessary to invest in blockchain technology and smart contracts. They can enlist experts to develop and implement smart contract solutions, while also providing training for their employees. Moreover, operating within heavily regulated sectors like finance and healthcare underscores the importance of compliance, where smart contracts play a pivotal role in automating processes and mitigating human error risks.

Conversely, the small and medium enterprises (SMEs) sector is projected to experience substantial growth in the foreseeable future. This growth is fueled by the cost-effectiveness and efficiency enhancements facilitated by smart contracts. By automating numerous processes, smart contracts enable SMEs to streamline operations and cut expenses. Given their typically limited resources, the affordability of smart contracts presents a significant advantage for SMEs. Additionally, smart contracts bolster efficiency by automating manual tasks, minimizing error occurrences, and expediting transaction processing times.

Based on End-User: The market is divided into Banking, Government, Management, Supply Chain, Automobile, Real Estate, Insurance and Healthcare. The Banking and Government segments held the major Smart Contracts Market share in 2023. Large banks mainly use smart contracts for various applications such as asset tokenization, cross-border payments, decentralized lending and insurance. Governments employ smart contracts for various purposes such as land registration, identity verification, social welfare distribution, voting systems and public procurement. The healthcare segment is expected to grow at a high CAGR during the forecast period because smart contracts enable the secure and efficient sharing of patient data, automated insurance claims processing, medical records management and supply chain tracking for pharmaceuticals and medical devices, which is expected to increase its demand in the healthcare sector.

Based on End-User: The market is divided into Banking, Government, Management, Supply Chain, Automobile, Real Estate, Insurance and Healthcare. The Banking and Government segments held the major Smart Contracts Market share in 2023. Large banks mainly use smart contracts for various applications such as asset tokenization, cross-border payments, decentralized lending and insurance. Governments employ smart contracts for various purposes such as land registration, identity verification, social welfare distribution, voting systems and public procurement. The healthcare segment is expected to grow at a high CAGR during the forecast period because smart contracts enable the secure and efficient sharing of patient data, automated insurance claims processing, medical records management and supply chain tracking for pharmaceuticals and medical devices, which is expected to increase its demand in the healthcare sector.

Smart Contracts Market Competitive Landscape

This section of the report includes various activities by Smart Contracts key competitors to increase their presence in the Smart Contracts Industry. These activities include mergers, acquisitions, joint ventures, collaborations, recent developments, technological advancements, innovations, etc. Several Smart Contracts Companies and blockchain platforms are actively involved in providing smart contract solutions.

Chainlink, which is an oracle network connects smart contracts with real-world data and external APIs. It provides reliable and secure data feeds to smart contracts that enable them to access and interact with off-chain information. Polkadot is a multichain platform. It enables interoperability between different blockchains. Simultaneously, it deploys and executes smart contracts on multiple chains. Polkadot and Chainlink are majorly working on providing interoperability frameworks and oracle solutions to facilitate cross-chain communication and data integration for smart contracts.

Smart Contracts Market Scope:Inquire Before Buying

| Global Smart Contracts Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 3.16 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 22.4% | Market Size in 2030: | US $ 10.7 Bn. |

| Segments Covered: | By Platform | Ethereum Cardano BNB Chain Polkadot Others |

|

| By Contract Type | Smart Legal Contracts Decentralized Autonomous Organizations (DAO) Application Logic Contracts (ALC) Distributed Applications (DApps) |

||

| By Blockchain Type | Public Private Hybrid |

||

| By Enterprise Size | Small & Medium Enterprises Large Enterprises |

||

| By End Use | BFSI Retail Healthcare Real Estate Logistics Others |

||

Smart Contracts Market, by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Smart Contracts Market Key Players are:

1. Monax Industries Limited (UK)

2. Monetas (Switzerland)

3. Blockchain Corporation (US)

4. Coinbase Inc (US)

5. Bitfinex (China)

6. BlockCypher Inc (US)

7. Chain Inc (US)

8. Coinify ApS (Denmark)

9. BitPay Inc (US)

10. GoCoin Pre Ltd (Singapore)

11. ScienceSoft USA Corporation (US)

12. Innowise Group (Warsaw)

13. iTechArt (New York)

14. 4soft (Poland)

15. IBM (New York)

16. TATA Consultancy Services Limited (India)

17. Chainlink (US)

18. ELEKS (Estonia)

19. Waves Technologies (UK)

20. Algorand (US)

21. Shardeum Foundation (Switzerland)

22. Oracle (US)

FAQs

1] What is the growth rate of the Smart Contracts Market?

Ans. The Global Smart Contracts Market is growing at a significant rate of 22.4 % over the forecast period.

2] Which region is expected to dominate the Smart Contracts Market?

Ans. North America region is expected to dominate the Smart Contracts Market over the forecast period.

3] What is the expected Global Smart Contracts Market size by 2030?

Ans. The market size of the Smart Contracts Market is expected to reach USD 10.7 Billion by 2030.

4] Who are the top players in the Smart Contracts Market?

Ans. The major key players in the Global Smart Contracts Market are Archer Daniels Midland Company, Arla Foods Amba, Kerry Group PLC, Saputo, Inc., Fonterra Co-operative Group Limited, and Royal Frieslandcampina N.V., Schreiber Foods, Inc.

5] Which factors are expected to drive the Smart Contracts Market growth by 2029?

Ans. A major driver for the global Smart Contracts market is the need for infant formula for newborns and babies who are in the pre or early weaning age.