Semiconductor Plating System Market Size by Technology, Application, Wafer Size, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2030

Overview

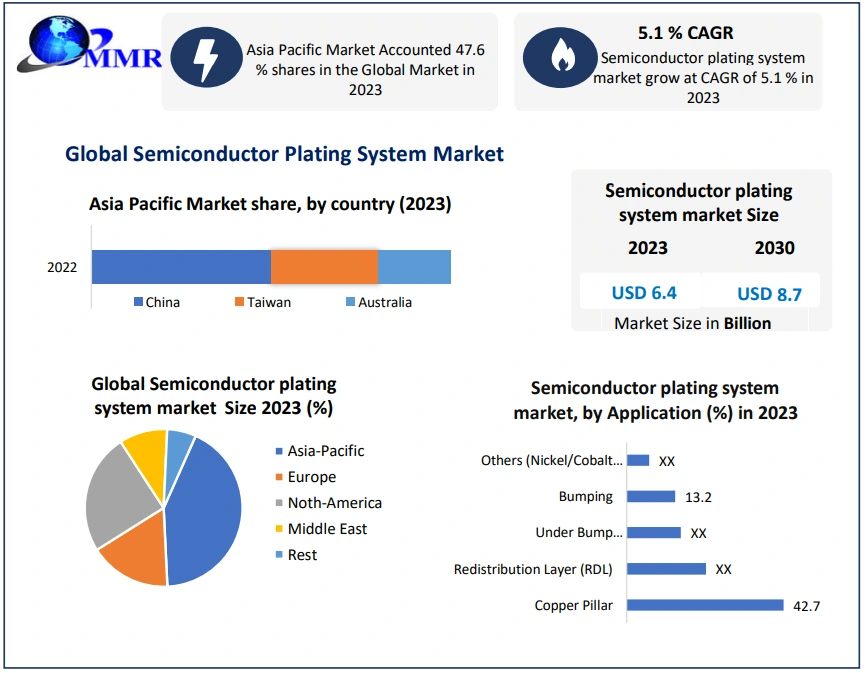

The Semiconductor plating system market size was valued at USD 6.4 Billion in 2023 and the total Semiconductor plating system market revenue is expected to grow at a CAGR of 5.1 % from 2024 to 2030, reaching nearly USD 8.7 Billion.

Semiconductor Plating System Market overview

Semiconductors are the foundation of the electronic industry these partially conductive products include transistors, chips and other electronic control parts, and are integral to electronic equipment from mobile phones to cars and robots. The companies create most semiconductor chips using a plate with another material. This outer coating protects the semiconductor from outside elements and connects it to the outside world. The semiconductor plating materials are anything from tin to gold, and each has a unique set of trains with different effects on the finished product. Chips, LED lights, and transistors are all made with semi-conductive materials like silicon. This means the material has characteristics of both conductors and insulators.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

They are crucial in creating protective and conductive layers, as well as interconnects and vital structures, that assist in the manufacturing of integrated circuits and various semiconductor devices. Serving the semiconductor industry's need for precise and efficient plating processes are a variety of tools, software, and chemical delivery systems that fall under the market for semiconductor plating systems. The semiconductor plating system market is essential for meeting the demands of advanced semiconductor device fabrication and ensuring uniformity throughout the plating process.

The market is influenced by factors such as cost, competition, and geographical trends, manufacturers strive to offer cost-effective plating systems. This semiconductor plating system provides high-quality results. Competition among suppliers drives innovation and improves the development of a more reliable and effective semiconductor plating market. Also the market dynamics are influenced by regional trends the global semiconductor plating industry demand for semiconductor plating systems varies across different regions based on the concentration of semiconductor manufacturing facilities and expected economic growth in these areas, during the forecast period.

Semiconductor Plating System Market Dynamics

Semiconductor manufacturing is the electrochemical deposition of metallic interconnects from electrical circuits. Plating is a fast and cost-effective way for metallic connections in devices manufacturing and advanced packaging. The semiconductor plating system Market offers high-quality manual and automated semiconductor plating systems for a wide variety of plating applications, such as Damascene, Barrier diffusion layer, under bump metallization (UBM), Bumping, Pillars, through silicon vias (TSVs) and through glass vias (TGVs). The semiconductor plating system industry is a manual and automated electroplating platform that delivers superior process results in device fabrication and packaging to manufacture MEMS sensors, CMOS image sensors, LEDs, RF, and photonic devices. The semiconductor plating system market is advanced fountain technology that guarantees optimal flow dynamics and precise electronic field control. This features provides customers with an optimal electrolyte exchange rate at the surface as well as outstanding uniformity and high plating rates.

Consumer expectations for smaller, more powerful, and feature-rich electronic devices has been increasing the demand in the semiconductor plating system market. Semiconductor plating system manufacturers are developed advanced devices with high performance and increased functionality. In the semiconductor plating industry developing new technologies such as artificial intelligence, machine learning, 5G, and autonomous vehicles are driving the demand for advanced semiconductor plating system devices. This technology are required high-performance chips and components to support their complex functionalities. The semiconductor plating market is increasing the demand for semiconductor devices for their operation in the automobile, aerospace, healthcare, and telecommunications industries to boost market growth. The demand for advanced semiconductor devices is rapidly increasing in various industries such as automotive, healthcare, aerospace, and telecommunications. The rising demand, semiconductor manufacturers are under pressure to create high-Performance and multifunctional components for smartphones, tablets, wearables, IoT devices, and other emerging technologies. This demand for advanced chips is fuelled by the need to support complex functionalities of AI, machine learning systems, 5G networks, and autonomous vehicles. In the automotive sector specifically, semiconductor components are critical in ADAS tech and electric vehicles. With IoT gaining popularity through smart home applications and connected devices we have seen a surge in demand for these vital semiconductors. The increasing demand for advanced semiconductor devices is fuelled by consumer expectations, emerging technologies, industry requirements, and the growing IoT ecosystem.

The sector that designs, manufactures, and sells semiconductor plating devices, which are the building blocks of modern electronic devices in the semiconductor plating system industry. This industry experiencing significant growth due to electronic devices becoming an integral part of daily lives, ranging from smartphones and laptops to household appliances and automobiles. The increasing adoption and reliance in these devices are driving the demand for semiconductor components, such as wireless communications, the internet of things, and autonomous vehicles are driving the growth of the semiconductor plating system industry. Businesses strive to enhance their efficiency, connectivity, and data processing capabilities, they increasingly rely on semiconductor chips and components. Governments and organizations are investing to develop domestic semiconductor plating systems manufacturing capabilities and reduce reliance on foreign suppliers. The growing semiconductor industry is driven by the increasing adoption of electronic devices. Emerging technologies, and digital transformation. Technological advancements drive the growth of the semiconductor plating system market pushing the boundaries of performance, functionality, and innovation.

The development of the semiconductor planting system market is due to increasing demand for semiconductor devices, computer power, higher speeds and improved energy efficiency. This leads to the production of more powerful and capable electronic devices. Technological advancement plays an important role in driving the growth of Internet of Things ecosystem. The Internet of Things is strongly dependent on semiconductors, particularly on communication chips and sensors. The development of the Semiconductor Plating System market is fueled by technological breakthroughs in process improvements and cost reduction. Cost savings, increased production efficiency, and higher chip yields result from advancements in semiconductor manufacturing processes, such as advanced lithography techniques, materials research, and yield optimisation. Consequently, this makes it possible for semiconductor producers to provide more competitive goods, grow their clientele, and promote market expansion. The semiconductor industry is growing as a result of technological developments that make it possible to create more potent and effective devices, facilitate miniaturisation and integration, support emerging technologies, develop the IoT ecosystem, and spur process innovations for lower costs and greater efficiency.

Restraints Impacting the Semiconductor Plating System Market

Implementing semiconductor plating systems requires significant capital investment. The cost of acquiring the plating equipment, chemical delivery systems, and process control software can be substantial. The ongoing operational costs, including the purchase of plating chemicals and maintenance of the equipment, add to the financial burden The higher cost is a barrier for small and medium-sized enterprises or new entrants, limiting their ability to upgrade semiconductor planting systems. The semiconductor industry’s cyclical nature and fluctuating demand patterns make it challenging for manufacturers to justify the substantial investment in plating systems during the forecast period. The semiconductor plating system market is the cost associated with implementing the electrochemical system. This technology requires substantial investment, including equipment, infrastructure, and skilled labor. The cost of setting up and maintaining semiconductor plating system barriers for smaller businesses or industries with limited biggest. ongoing operational costs, such as the procurement of raw material and energy consumption adds a financial burden. The high capital expenditure and operational cost involved in semiconductor plating systems has been hindering adoption, for businesses that are unable to justify or afford such investment.

Technological Complexity and Expertise: Semiconductor plating systems involve complex technologies and processes that require technical expertise for operation, maintenance, and optimization. Proper calibration, monitoring, and adjustment of the plating equipment and chemical parameters are essential to achieve precise and uniform plating results. The complexity of these systems and processes can present challenges, particularly for companies with limited technical resources or access to skilled personnel. The shortage of skilled technicians with the necessary knowledge and experience in semiconductor plating systems can pose a constraint on the efficient adoption and operation of these systems. Companies may face difficulties in optimizing plating processes, troubleshooting issues, and staying updated with the latest technological advancements.

Semiconductor Plating System Market Trends

Process control and automation are becoming increasingly important in the semiconductor plating system market. The industry demands tight control over plating parameters to ensure consistent results and minimize defects. Automation and real-time monitoring systems are being integrated into plating systems to enable precise control, reduce human error, and improve overall process efficiency. The trend toward the adoption of advanced packaging technologies In the semiconductor plating system markets technologies such as fan-out wafer-level packaging, system-in-package, and heterogeneous integration, offer higher devices integration, improved performance, and miniaturization This trend drives the demand for advanced semiconductor plating systems that can meet the specific requirements of these packaging technologies. The emergence of 3D packaging and advanced packaging technologies is driving the need for specialized plating systems. These technologies, including through-silicon via (TSV) and wafer-level packaging (WLP), require precise and reliable plating processes to create interconnects and build stacked chip structures. The demand for high-speed plating processes is driven by the need for increased productivity and throughput in semiconductor manufacturing.

Semiconductor plating system market Segment Analysis

By Technology,

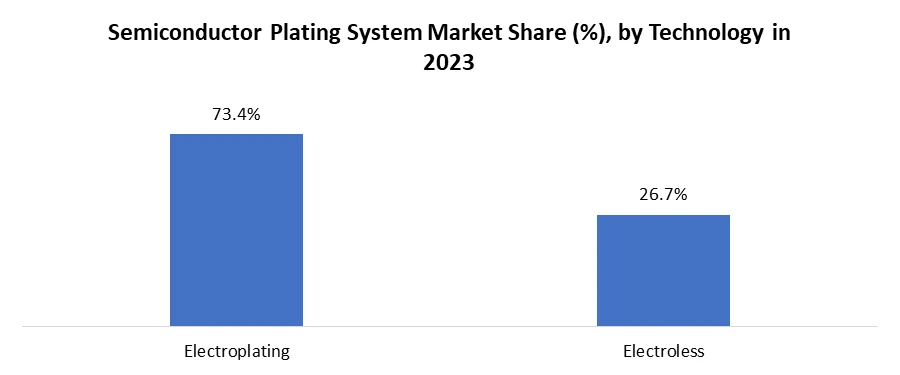

In the landscape of the Semiconductor Plating System Market in 2023, Electroplating takes center stage, commanding an impressive 73.4% market share. This dominance is attributed to its versatility and precise control, offering superior deposition thickness and uniformity crucial for high-performance chips with intricate geometries. Leveraging decades of development, electroplating systems boast mature technology, ensuring reliable operations, scalability, and cost-effectiveness. Further enhancing its appeal is the ability to handle a diverse array of metals, including copper, nickel, gold, and tin, catering to various functional requirements in chip fabrication.

In contrast, Electroless plating plays a vital role, holding an estimated 26.7% market share. Excelling in seed layer formation on non-conductive surfaces, it proves essential for subsequent electroplating steps. Additionally, its capability to deposit materials like palladium and platinum holds promise for future chip technologies. Despite these advantages,

electroless. plating encounters limitations, such as slower deposition rates impacting wafer throughput and potential cost considerations.

Looking ahead, the Semiconductor Plating System Market is poised for a balanced approach. Electroplating is expected to maintain dominance due to its versatility, efficiency, and cost-effectiveness in high-volume production. Concurrently, advancements in electroless plating technology, focusing on speed and cost reduction, may broaden its application scope. The choice between these technologies will hinge on specific chip design requirements, striking a delicate balance between performance, cost, and complexity. Continuous innovation in both electroplating and electroless plating ensures optimal plating solutions, addressing the evolving needs of the dynamic chip industry.

By Application,

In the dynamic landscape of the Semiconductor Plating System market in 2023, Copper Pillar plating emerges as the frontrunner, commanding an estimated 42.7% market share. This dominance is underpinned by the widespread application of copper pillars as foundational structures for interconnects in advanced logic devices, memory chips, and critical components, showcasing their indispensability across various chip types. Copper pillars gain further traction due to the ongoing trend of miniaturization, where their superior electrical conductivity and smaller dimensions, compared to traditional aluminum alternatives, make them essential for the development of high-performance chips. The mature technology associated with copper pillar systems, characterized by established processes and reliable equipment, contributes to their cost-effectiveness and widespread adoption, setting them apart from emerging plating technologies.

While Copper Pillar takes the lead, other segments in the Semiconductor Plating System market exhibit promise, albeit with smaller market shares. Redistribution Layer (RDL) plating, constituting approximately 20-25% of the market, facilitates signal routing within advanced packages, contingent on the overall demand for complex chip packaging. Under Bump Metallization (UBM) and Bumping, with shares ranging from 15-20% and 10-15%, respectively, play vital roles in facilitating connections between chips and packages, but their growth is linked to the adoption of advanced packaging technologies. The "Others" segment, encompassing emerging technologies like nickel and cobalt plating, holds a 5-10% share, representing a nascent stage of development and adoption. While Copper Pillar plating is anticipated to maintain its lead in the short term, the Semiconductor Plating System market may undergo further diversification driven by advancements in other segments, especially those aligned with the demands of miniaturization and 3D chip integration, shaping the industry's evolution in response to the dynamic needs of the chip market.

Semiconductor plating system market regional analysis

The Asia Pacific held the largest market share of 47.6% of the global semiconductor planting system market in 2023. The region is expected to dominate the market during the forecast period due to the strong presence of semiconductor manufacturers. The region's semiconductor sector is largely supported by Taiwan, Japan, South Korea, and China, where demand for semiconductor seeding systems is rising. A sizeable share of the revenue from the global semiconductor market was generated in the Asia Pacific area. Manufacturers of semiconductor plating systems find the region to be appealing due to its emphasis on technological breakthroughs, adoption of cutting-edge packaging techniques, and presence of semiconductor production facilities.

North America is another prominent region in the semiconductor plating system market, known for its advanced technology, strong semiconductor industry, and high demand for electronic devices. With its considerable presence of semiconductor manufacturers and technological advancements, the United States is a major participant in the region. Major players and research institutions that fuel technical developments are present in the semiconductor sector in the US. Silicon Valley, in California, is a well-known centre for semiconductor research and is home to numerous semiconductor start-ups and enterprises. The region has a market opportunity for suppliers of plating systems due to the existence of significant semiconductor industries, a strong supply chain, and a highly skilled workforce.

Semiconductor plating system market Competitive Landscape

The semiconductor plating system market is fiercely competitive, with numerous key players striving to establish their dominance. Among them, Applied Materials Inc. stands out as a leading player in the industry. The company offers a comprehensive portfolio of plating systems that cater to various semiconductor applications, including advanced packaging and interconnects. Applied Materials' plating systems are renowned for their precision, reliability, and compatibility with cutting-edge manufacturing processes.

Another prominent player is Lam Research Corporation, a global leader in semiconductor equipment and services. Lam Research's plating solutions are designed to deliver high-quality, uniform plating results, ensuring optimal performance in advanced packaging and interconnect applications. The company places a strong emphasis on process optimization and control, incorporating real-time monitoring, automation, and data analytics features to enhance productivity and yield. Tokyo Electron Limited (TEL), a renowned semiconductor equipment manufacturer, is also a significant player in the plating system market. TEL's plating systems are highly regarded for their advanced process control capabilities, high throughput, and compatibility with diverse plating materials. The company focuses on continuous technological advancements and collaborates closely with customers to develop tailored plating solutions that meet specific requirements. Kulicke & Soffa Industries, Inc., a prominent player in the semiconductor packaging and electronics assembly market, offers a wide range of plating systems. Known for their reliability, scalability, and flexibility, Kulicke & Soffa's plating solutions enable efficient and cost-effective production of semiconductor components across various industries such as automotive, consumer electronics, and telecommunications.

Semiconductor Plating System Market Scope: Inquire before buying

| Global Semiconductor Plating System Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 6.4 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 5.1% | Market Size in 2030: | US $ 8.7 Bn. |

| Segments Covered: | by Technology | Electroplating Electroless |

|

| by Application | TSV Copper Pillar Redistribution Layer (RDL) Under Bump Metallization (UBM) Bumping Others |

||

| by Wafer Size | Up to 100 mm 100 mm-200 mm Above 200 mm |

||

Semiconductor Plating System Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Semiconductor plating system market Key players

1. RENA Technologies

2. ACM Research

3. Mitomo Semicon Engineering

4. Heraeus

5. XiLong Scientific

6. Atotech

7. Yamato Denki

8. Meltex

9. Ishihara Chemical

10. Raschig GmbH

11. Japan Pure Chemical

12.Coatech

13. MAGNETO special anodes

14. Vopelius Chemie

15. Moses Lake Industries

16. JCU International

17. Applied Materials, Inc.

18. Lam Research Corporation

19. Tokyo Electron Limited

20. Hitachi High-Tech Corporation

21. Semsysco GmbH

22. JBT Corporation

23. ULVAC, Inc.

24. ClassOne Technology, Inc.

25. Strasbaugh Inc.

26. Naura Akrion Inc.

27. Applied Materials, Inc.

28. Tokyo Electron Limited:

29. KLA Corporation:

30. Advanced Process Systems Corporation:

31. Technic Inc

32. Solvay SA

33. TEL Nexx, Inc

Frequently Asked Questions:

1] What is the growth rate of the Global Semiconductor plating system market?

Ans. The Global Semiconductor plating system market is growing at a significant rate of 5.1 % during the forecast period.

2] Which region is expected to dominate the Global Semiconductor plating system market?

Ans. Asia Pacific is expected to dominate the Semiconductor plating system market during the forecast period.

3] What is the expected Global Semiconductor plating system market size by 2030?

Ans. The Semiconductor plating system market size is expected to reach USD 8.7 Bn by 2030.

4] Which are the top players in the Global Semiconductor plating system market?

Ans. Some of the top players operating in the Semiconductor plating system market are RENA Technologies, ACM Research, Mitomo Semicon Engineering, Heraeus.

5] Which sector is the key driver in the Semiconductor plating system market?

Ans. Increasing Demand for advanced technologies boost the market growth in Semiconductor plating system market.