Semiconductor Devices Market Size by Device Type, Material, End-User Vertical, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2032

Overview

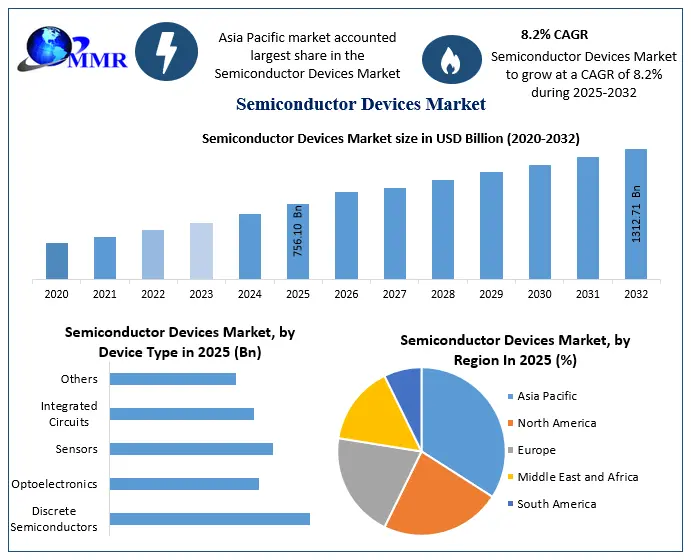

The Semiconductor Devices Market size was valued at USD 756.10 Billion in 2025 and the total Semiconductor Devices revenue is expected to grow at a CAGR of 8.2% from 2026 to 2032, reaching nearly USD 1312.71 Billion by 2032.

Semiconductor Devices Market Overview

Semiconductor devices are electronic components that exploit the electronic properties of semiconductor materials, like as silicon, germanium, and gallium arsenide, as well as organic semiconductors. Semiconductor devices have replaced vacuum tubes in many applications. They use electronic conduction in the solid state as opposed to the thermionic emission in a high vacuum. Semiconductor devices are manufactured for both discrete devices and integrated circuits, which consist of from a few to billions of devices manufactured and interconnected on a single semiconductor substrate or wafer.

Demand for semiconductors is growing due to increased digitization of the economy, growing demand for “smart” products, increased remote work, schooling, and shopping, and other factors, which is expected to boost the Semiconductor Devices Market growth. To meet this growing demand and counter the supply chain shock caused by the pandemic, the semiconductor industry has in the short term substantially expanded shipments by increasing the utilization of existing manufacturing capacity.

Semiconductor Devices Market Dynamics To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Rise in demand for Power Semiconductor Devices to boost Semiconductor Devices Market growth

Utilizing wide band gap (WBG) semiconductors results in power semiconductor devices that are smaller, faster, and more reliable and efficient compared to other available semiconductor materials. The benefits of wide band gap semiconductor materials, such as lightweight construction, extended lifespan, and larger energy band gap, make them the preferred choice for various types of power semiconductor devices worldwide, which significantly boosts the Semiconductor Devices Market growth. The widespread availability and decreasing prices of WBG semiconductor power devices, coupled with the growing demand for gallium nitride (GaN) and silicon carbide (SiC) power devices in applications spanning from telecom equipment and computers to military devices, electric vehicles, and photovoltaic inverters, are expected to propel the global wide band gap semiconductor market over the forecast period. The surge in investments in wide band gap semiconductor materials and their integration into the power semiconductor industry are poised to drive further growth in the global wide band gap semiconductor devices market throughout the forecast period.

Emerging technologies to boost Semiconductor Devices Market growth

The proliferation of emerging technologies such as artificial intelligence (AI), Internet of Things (IoT), 5G connectivity, augmented reality (AR), and virtual reality (VR) drives demand for advanced semiconductor devices. These technologies rely heavily on semiconductor components for processing, memory, connectivity, and sensor functionalities, fueling the need for specialized semiconductor solutions tailored to their requirements. The automotive industry represents another significant driver of the semiconductor devices market. The rise of electric vehicles (EVs), autonomous driving technologies, advanced driver-assistance systems (ADAS), and in-vehicle connectivity systems has led to a surge in semiconductor content per vehicle. Semiconductor devices enable key functionalities such as power management, sensing, processing, and communication within modern automotive systems, contributing to improved safety, efficiency, and performance.

The increasing adoption of renewable energy sources and energy-efficient technologies drives demand for power semiconductor devices, which significantly helps to increase the Semiconductor Devices Market share. Semiconductor devices such as insulated gate bipolar transistors (IGBTs), MOSFETs, and diodes are essential components in power electronics systems used for renewable energy generation, energy storage, electric grid management, and electric vehicle charging infrastructure.

Increasing complexity and cost of semiconductor design and verification to limit the Semiconductor Devices Market growth

As semiconductor devices become more sophisticated and integrate complex functionalities, the design process becomes more intricate and time-consuming. Designing and verifying complex semiconductor systems require extensive simulation, modeling, and validation efforts, leading to longer time-to-market and higher development costs. The shortage of skilled semiconductor engineers and designers exacerbates these challenges, hindering innovation and productivity in the Semiconductor Devices industry. Supply chain disruptions and semiconductor shortages have emerged as critical restraints in recent years, driven by factors such as geopolitical tensions, natural disasters, and unexpected demand spikes. These disruptions disrupt semiconductor devices production and distribution, leading to delays in product launches, increased lead times, and supply chain inefficiencies.

Geopolitical tensions and trade disputes further complicate the semiconductor devices market, leading to uncertainties surrounding tariffs, export controls, and trade restrictions. Trade conflicts between major economies disrupt global semiconductor devices supply chains, fragment markets, and impede technology transfer and collaboration. Moreover, restrictions on the export of critical semiconductor equipment and materials can hinder innovation and R&D collaboration among international partners, limiting the industry's growth potential.

Semiconductor Devices Market Segment Analysis

By Product Type Segment-wise, the semiconductor devices market is increasingly shaped by the diverse functionality and technological advancements across key product categories. Integrated circuits (ICs) lead the landscape, contributing over 65% of global market revenue in 2025, fueled by sustained demand in data centers, consumer electronics, and automotive applications. Discrete semiconductors remain vital for switching, rectification, and power amplification, especially in high-reliability environments such as EVs and industrial automation.

The optoelectronics segment is experiencing accelerated growth, supported by the surging use of LEDs, laser diodes, and image sensors in displays, communication, and renewable energy systems. Sensors are gaining prominence, driven by their critical role in smart infrastructure, wearables, and industrial IoT applications, with CMOS and MEMS-based sensors leading innovation. The others segment, comprising niche and emerging technologies, is poised for long-term potential as neuromorphic and photonic components begin to commercialize and expand beyond R&D environments.

By Material Segment, Materials are at the heart of how semiconductor devices perform, and each type brings its own strengths to different applications. Silicon (Si) continues to be the industry’s workhorse, making up more than 80% of the market share in 2025. It is affordable, well-understood, and versatile—used everywhere from smartphones to industrial machinery. But as demand rises for faster, smaller, and more energy-efficient devices, alternative materials are gaining ground.

Silicon Carbide (SiC) is a standout in high-voltage and high-temperature environments, especially in electric vehicles, solar inverters, and smart grids, thanks to its wide bandgap, high thermal conductivity, and ability to handle power with minimal loss. Then there's Gallium Nitride (GaN), which is making waves in 5G, RF communication, and fast-charging technologies. Its high electron mobility and power density allow for more compact and efficient devices. Gallium Arsenide (GaAs), on the other hand, is ideal for high-frequency and optoelectronic applications—think satellite systems, laser diodes, and photodetectors—due to its strong photon absorption and electron velocity. Meanwhile, the ‘Others’ category—covering materials like Indium Phosphide (InP), Germanium, and even Graphene—is still emerging but holds promise for future innovations in quantum computing, terahertz electronics, and photonic integrated circuits.

Semiconductor Devices Market Regional Insight

Asia Pacific dominated the market in 2025 and is expected to hold the largest Semiconductor Devices Market share over the forecast period. Among the world's leading Semiconductor devices manufacturing hubs, China stands as a prominent player undergoing significant expansion in semiconductor manufacturing capacity. With its vast manufacturing sector, China holds the title of the largest semiconductor market globally with largest semiconductor devices exporter. Yet, the Chinese government is actively pursuing a path to bolster the country's manufacturing prowess, aiming for self-sufficiency by domestically producing the necessary volume of semiconductors without reliance on imports. Projections suggest that by 2032, China is expected account for as much as 25% of the world's semiconductor production.

In 2021, the United States claimed roughly 12% of the global chip manufacturing capacity, a marked decrease from its position a few decades earlier when it held 37% in 1990. This decline is attributed to the rise of semiconductor production capabilities in countries like Taiwan and China. The semiconductor industry remains highly profitable within the US. According to the Semiconductor Industry Association (SIA), semiconductor exports contributed $62 billion (USD) to the US economy in 2021, surpassing all other products except refined oil, aircraft, crude oil, and natural gas. A significant portion of these imported chips ultimately return to the US as finished consumer electronics.

Despite possessing only 12% of the world's semiconductor manufacturing capacity in 2021, US-based companies commanded approximately 46.3% of the total semiconductor devices market share. This apparent incongruity is justified by both the significant dollar value of imported US semiconductors, as mentioned earlier, and the fact that many US-based companies operate semiconductor fabrication plants abroad, such as in Japan. In such instances, the manufacturing capacity is attributed to the host country rather than the US, but the profits are typically counted within the US economy.

In May 2023, South Korea unveiled the “K-Semiconductor Belt” strategy aimed at building the world’s largest semiconductor supply chain by 2030. The initiative offers investment tax credits for semiconductor R&D to attract more private-sector investment. South K`orea's K-semiconductor strategy outlines an ambitious plan to establish the world's premier semiconductor devices supply chain by 2030, backed by a substantial $450 billion investment initiative. The government has unveiled tax deductions totaling nearly $260 billion for semiconductor facilities and research and development endeavors. Efforts to expedite and streamline the approval process for semiconductor manufacturing facility expansions are underway, alongside subsidies covering up to 50% of the construction expenses for power infrastructure within these facilities, which significantly boost the Semiconductor devices market growth.

Strategic investments are earmarked for crucial semiconductor sectors like power, automotive, and AI, as part of a comprehensive long-term research and development roadmap. With robust financial incentives and regulatory support, the government aims to double semiconductor production to $245 billion, with an export target of $200 billion, by the year 2030.

Semiconductor Devices Market Scope: Inquire Before Buying

| Global Semiconductor Devices Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 756.10 Billion |

| Forecast Period 2026 to 2032 CAGR: | 8.2% | Market Size in 2032: | USD 1312.71 Billion |

| Segments Covered: | by Device Type | Discrete Semiconductors Optoelectronics Sensors Integrated Circuits Others |

|

| by Material | Silicon (Si) Silicon Carbide (SiC) Gallium Nitride (GaN) Gallium Arsenide (GaAs) Others |

||

| by End-User Vertical | Electronics & Consumer Goods Aerospace & Defense Telecommunication Automotive Others |

||

Semiconductor Devices Market, by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, ASEAN and Rest of APAC)

South America (Brazil, Argentina Rest of South America)

Leading Semiconductor Devices Manufacturers include:

1. TSMC

2. Samsung Electronics

3. Intel Corporation

4. NVIDIA Corporation

5. Broadcom Inc.

6. SK hynix

7. Micron Technology

8. Texas Instruments

9. AMD

10. Qualcomm

11. Infineon Technologies

12. STMicroelectronics

13. NXP Semiconductors

14. MediaTek

15. Analog Devices, Inc.

16. ON Semiconductor

17. Sony Semiconductor Solutions

18. Renesas Electronics

19. GlobalFoundries

20. UMC (United Microelectronics Corporation)

21. SMIC (Semiconductor Manufacturing International Corp.)

22. Rohm Semiconductor

23. Toshiba Electronic Devices & Storage

24. Murata Manufacturing

25. Tower Semiconductor

26. HiSilicon

27. GigaDevice Semiconductor

28. Melexis

29. Nuvoton Technology

30. CEVA Inc

Frequently asked Questions:

1. What are semiconductor devices?

Ans: Semiconductor devices are electronic components that utilize the electronic properties of semiconductor materials like silicon, germanium, and gallium arsenide.

2. What is driving the growth of power semiconductor devices?

Ans: The utilization of wide band gap (WBG) semiconductors results in power semiconductor devices that are smaller, faster, more reliable, and more efficient. This is driving their adoption in various applications such as telecom equipment, computers, military devices, electric vehicles, and photovoltaic inverters.

3. What are the key factors boosting the semiconductor devices market growth?

Ans: The proliferation of emerging technologies such as AI, IoT, 5G connectivity, AR, and VR is driving demand for advanced semiconductor devices.

4. Which regions dominate the semiconductor devices market?

Ans: Asia-Pacific dominates the semiconductor devices market, with countries like China, South Korea, and Japan playing significant roles. However, North America and Europe also have prominent semiconductor industries and contribute to market growth.

5. What initiatives are countries taking to strengthen their semiconductor industries?

Ans: Countries like South Korea have unveiled strategies such as the "K-Semiconductor Belt" to build robust semiconductor supply chains by investing in R&D, offering tax incentives, and streamlining regulatory processes to attract private-sector investment.