Global Remote Towers Market Size by Operation Type, Application, Offering, End User, and Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2029

Overview

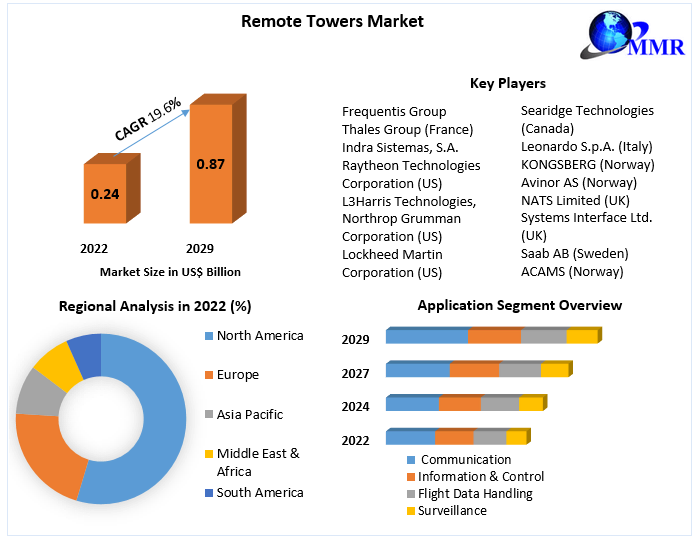

Remote Towers Market size was valued at US$ 0.24 Bn. in 2022 and the total revenue is expected to grow at 19.6% through 2023 to 2029, reaching nearly US$ 0.87 Bn.

Remote Towers Market Overview:

The Remote Towers Market was valued at USD 0.24 billion in 2022, and is predicted to grow at a CAGR of 19.6 percent to USD 0.87 billion by 2029. The Remote Towers Market is studied by segments like Operation Type (Single / Sequential, Multiple/ Simultaneous, Contingency), Application (Communication, Information & Control, Flight Data Handling, Surveillance) and Region (North America, Europe, Asia-Pacific, and Rest of the World). The report consists of the Trend, Forecast, Competitive Analysis, and Growth Opportunities of the market. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

For the forecast period of 2023 to 2029, the report provides a complete analysis that reflects today's Remote Towers Market realities and future market prospects. To provide a comprehensive perspective of the market, the research segments and analyses it in great detail. The key data and observations offered in the study can help market participants and investors identify low-hanging fruit in the market and build growth strategies.

Covid-19 Impact on Remote Towers Market:

The COVID-19 pandemic did have and will continue to have a severe impact on aviation traffic, which will have an indirect negative influence on the distant towers industry. Airports of all capacities have been affected, but smaller & regional airports have been particularly hard hit. Due to announced lockdowns and government prohibitions on public meetings, research and development (R&D) in several remote towers systems has been hampered as a result of the COVID-19 problem. Due to the global COVID-19 situation, major airports have been shut down, delaying ongoing upgrades to airports with several remote tower systems.

Maintaining the production has now become a challenge for remote tower manufacturers of all types, as businesses and supply chains have experienced temporary shutdowns or disruptions due to financial losses incurred as a result of strict lockdowns, international border closures, and a drop in import and export activity. Investors were hesitant to fund new businesses because of these issues. COVID-19's financial impact on airlines and the aviation supply chain forced many firms and organizations to slash costs. The majority of these initiatives include personnel reductions, whether through furloughs or early retirements. It has transformed the working atmosphere for crews, ATCOs, & dispatchers in the aviation industry, in addition to having a detrimental impact on employee morale.

Remote Towers Market Dynamics:

Cost Savings Increased: From a remote location, remote towers may manage both a single and several airports. Cost saving in civil infrastructure & ATM systems result from this. Due to high ATC tower expenditures that cannot be balanced with the volume of air traffic, small and medium-sized airports with low traffic operate at a loss. Multiple similar airports can be operated concurrently or sequentially based on a timetable from a single place via remote towers. When compared to constructing a high-end camera system that sends video clip to a remote tower for ATC operations, the cost of getting independent towers at such airports is just too costly.

The first remote tower in Norway was installed in 2021, and Avinor AS is working with the SESAR 2021 program to install three more towers in 2021. Through the end of 2022, the remote towers system will be deployed at 15 airports across Norway, all of which will be managed from the Bod centre. This is predicted to be much less expensive than building separate towers at each of these airports. The remote towers will accommodate the increased passenger traffic at a lower cost than updating and constructing existing air traffic control towers. The market for remote towers is projected to increase as ATM costs decrease.

ATM Digitalization: The aviation market is going through a digital revolution. Autonomous aircraft & drones, digital MRO, and digital airport technology, among other things, are propelling the industry forward. The digitalization of airports is led by remote towers. They use digital technology with highly automated processes to replace human OTW views. The aeronautical data received by distant towers, as well as the automated algorithms that create terrain mapping and anti-collision mapping for controllers, are all digital.

For example, ENAIRE (Spain) is working on the development of the Digital Control Tower project, with Indra Sistemas (Spain) as the technological partner, in a project that extends much beyond the mere provision of remote Tower Control Traffic Services. Based on the implementation of Augmented Reality and Artificial Intelligence, this revolutionary solution blends existing ATS surveillance data, Air Traffic Control, & Communications systems with such a panoramic visualization system equipped with unique information and alarm features. Moving from the "visual" concept of operational processes of the exit Towers to a new concept of operational processes based on the merger of a new digitalized visual with ATM system information, this progression from "remote concept" to a new "digital concept" is based on the goal of expanding human and ATMS system cooperation.

Cyber Threats to ATM: The use of ICT in remote tower systems to construct a network between both the airport & CWPs could put ATC operations at risk of cyber attack. The digitalization of such complicated instruments has raised significant cybersecurity concerns. Traditional ATC towers operate in a secure environment that is free of cyber threats. Remote towers & their components, on the other hand, are connected to the web or a network, making them hackable. The risk to remote towers has escalated as a result of the interaction and interdependence inherent in ICT.

Non-state actors, such as terrorists, hacktivists, and cybercriminals, represent the most direct threat to ATM systems. Information theft, general aviation disruption, and probable loss of life are all possible consequences of such threats. The coordinated attack by Iranian hackers on computer systems in over sixteen countries, including attacks on systems in Pakistan, South Korea, Saudi Arabia, and also the United States, is one example of recent cyberattacks on the ATM system. By hacking the system that creates flight plans, a cyberattack on the networks of Polskie Linie Lotnicze, the Polish National Airline in June 2021 grounded 10 aircraft to Poland, Germany, and Denmark and caused delays for another ten.

Remote Towers Market Segment Analysis:

Based on Operation type, the remote towers market is classified into Single / Sequential, Multiple/ Simultaneous, Contingency. Due to the necessary monitoring of all parameters before to every flight boarding, the single sector is predicted to grow at a significant rate in the remote towers market. The growing number of air passengers, combined with the need for quick and secure solutions, is allowing industry participants to offer improved facilities for them.

Due to the number of systems deployed at various airports throughout the globe, the multiple sector is expected to account for a large market share during the forecast period. They work on numerous parameters at the same time to improve performance. As the systems are utilized for emergencies and also a backup remote tower, the contingency category dominated the market in 2022 and is predicted to expand at the highest CAGR throughout the forecast period.

Based on Application, the remote towers market is classified into Communication, Information & Control, Flight Data Handling, and Surveillance.

Communication: During the forecast period, this category is predicted to grow at the fastest rate. Remote towers help to connect ground-based equipment with air traffic, ensuring that the aircraft and airport run well. Such factors are projected to propel the industry forward.

Information & Control: Remote towers help gather weather data, acquire intelligence information, and take overhead images. The global market for information and control is predicted to develop due to its increasing uses.

Flight Data Handling: The market is predicted to grow due to the increased development of various systems and services such as flight operations quality assurance as well as flight data analysis.

Surveillance: Due to the expanding use of unmanned aerial vehicles (UAVs) and increased air passenger traffic, the surveillance segment led the global market in 2022. The global market for remote towers is rising since they provide increased monitoring capabilities for pilots and aid in air traffic management.

Regional Insights:

In 2022, Europe is expected to lead the remote tower market, with the United Kingdom and Sweden accounting for a large portion of the regional market. The market in Europe is being driven by the increasing demand for remote towers in the region, as well as the development of new & technologically advanced remote tower components such as high resolution cameras, panoramic displays, and communication systems.

Objective:

To understand the Remote Towers industry and study the market trends.

Focusing on the regional market and other segmentations, knowing the drivers and challenges of the same.

Understanding the market segment geographically to gauge the growth potential.

The report includes analytical models like the Porter’s Five Forces, which helps in understanding the operating environment of the competition in the Remote Towers Market and thereby study the stakeholders to derive an efficient strategy; and PESTLE Analysis to gain a macro perspective of the Remote Towers Industry in terms of political aspects like Government stability, policies, trade regulation and economic aspects like market trends, taxes and inflation. It also provides the effect of environmental factors and influence of social and legal aspects on the Remote Towers Market.

Remote Towers Market Scope: Inquire before buying

| Remote Towers Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2022 | Forecast Period: | 2023-2029 |

| Historical Data: | 2018 to 2022 | Market Size in 2022: | US $ 0.24 Bn. |

| Forecast Period 2023 to 2029 CAGR: | 19.6% | Market Size in 2029: | US $ 0.87 Bn. |

| Segments Covered: | by Operation Type | Single / Sequential Multiple/ Simultaneous Contingency |

|

| by Application | Communication Information & Control Flight Data Handling Surveillance |

||

| by Offering | Hardware Software and solutions Services |

||

| by End User | Military Airport Commercial Airport |

||

Key Players are :

1. Saab AB (Sweden)

2. Frequentis Group (Austria)

3. Thales Group (France)

4. Indra Sistemas, S.A. (Spain)

5. Raytheon Technologies Corporation (US)

6. L3Harris Technologies, Inc. (US)

7. Northrop Grumman Corporation (US)

8. Lockheed Martin Corporation (US)

9. Searidge Technologies (Canada)

10.Leonardo S.p.A. (Italy)

11.KONGSBERG (Norway)

12.Avinor AS (Norway)

13.NATS Limited (UK)

14.Systems Interface Ltd. (UK)

15.ACAMS (Norway)

Frequently Asked Questions:

1] What segments are covered in the Remote Towers Market report?

Ans. The segments of Application, Operation Type and Region are covered in the Remote Towers Market report.

2] Which Region is expected to hold the highest share in the Remote Towers Market?

Ans. The North America region is expected to hold the highest share in the Remote Towers Market.

3] What is the market size of the Remote Towers Market by 2029?

Ans. The market size of the Remote Towers Market is expected to reach USD 0.87 Bn by 2029.

4] What is the forecast period for the Remote Towers Market?

Ans. The forecast period for the Remote Towers Market is 2023-2029.

5] What was the market size of the Remote Towers Market in 2022?

Ans. The market size of the Remote Towers Market in 2022 was USD 0.24 Bn.