Refinery Catalyst Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

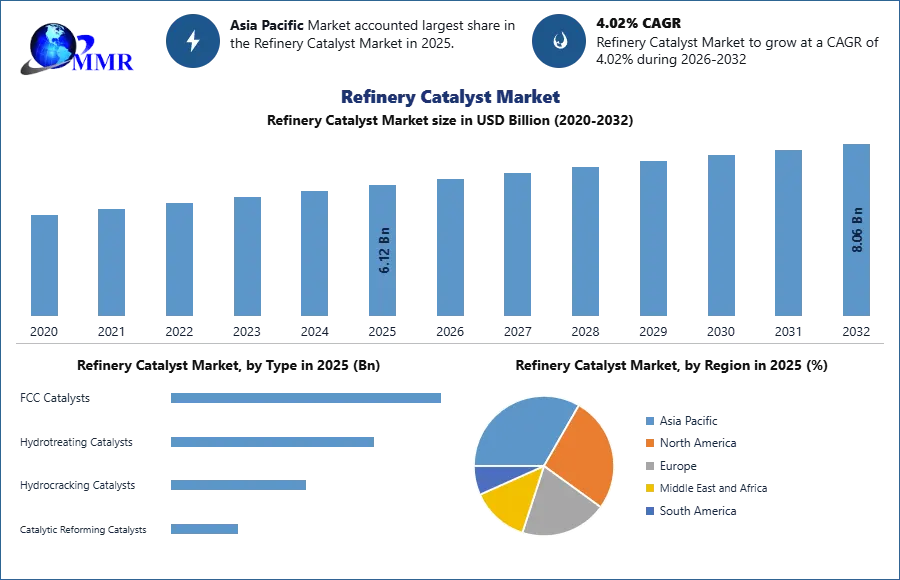

The Refinery Catalyst Market size was valued at USD 6.12 Billion in 2025 and the total Refinery Catalyst revenue is expected to grow at a CAGR of 4.02% from 2025 to 2032, reaching nearly USD 8.06 Billion.

Global Refinery Catalyst Market Overview:

Refinery Catalyst Market is expected to reach USD 8.06 Bn. by 2032. The Refinery catalysts are chemical compounds that are used to remove undesired impurities such as nitrogen, metal contamination, and sulphur during the refining process. This report focuses on the different segments of the Refinery Catalyst market (Type, Ingredient, and Region). This report examines the top industry players and regions in depth (North America, Asia Pacific, Europe, Middle East & Africa, and South America). It's a comprehensive look at today's rapid advancements in a range of fields. Facts and figures, visualisations, and presentations are used to highlight the primary data analysis from 2020 to 2025.

The market drivers, restraints, opportunities, and challenges for Refinery Catalyst are examined in this report. The MMR report's investment suggestions are based on a thorough examination of the current competitive environment in the Refinery Catalyst market. To Know About The Research Methodology :- Request Free Sample Report

To Know About The Research Methodology :- Request Free Sample Report

Refinery Catalyst Market Dynamics:

The Refinery Catalyst market is expected to grow due to rising global demand for transportation fuel. Refinery Catalyst Market growth is expected to be driven by strict regulations along with rising demand for petroleum and petroleum-derived products/chemicals. Refinery catalysts are used to improve the operational efficiency of the petroleum refining sector. Furthermore, rising demand for high-octane fuel, particularly in countries such as the United States, Japan, Germany, the United Kingdom, and India, is expected to favourably influence the growth of the refinery catalyst market.

Metal contamination and the thermal balance effect in tight oil processing are common problems that refinery catalysts are employed to solve. During the forecast period, growing tight oil production in the United States, Russia, China, and Argentina is expected to drive market growth. Government laws, such as those governing Ultra-low Sulfur Diesel (ULSD) and severe emission standards in developed nations, are expected to continue to drive demand for refinery catalysts in the petroleum refining industry. The availability of alternative fuels like biofuel, as well as the implementation of "Go Green" campaigns and environmental legislation by various countries, is expected to limit the growth of the refinery catalysts market.

Zeolites, chemical compounds, and metals are among the materials utilised in the production of refinery catalysts. Manufacturers can make fluid catalytic cracking refinery catalysts, alkylation refinery catalysts, hydrotreating refinery catalysts, and hydrocracking refinery catalysts using these compounds in various compositions or in conjunction with other chemicals.

Producers of refinery catalysts are focusing their efforts on producing catalysts that can handle a wide range of feedstocks while also providing stable, predictable, easy, and profitable hydrotreating and hydrocracking applications. Superior process designs, proprietary equipment, and performance refinery catalyst innovation have all aided businesses in gaining a competitive advantage over their rivals. Furthermore, corporations are increasingly combining technical expertise with environmentally friendly production processes.

Refinery Catalyst Market Segment Analysis:

The Refinery Catalyst Market is segmented by Type, and Ingredient.

Based on the Type, the market is segmented into FCC Catalysts, Hydrotreating Catalysts, Hydrocracking Catalysts, and Catalytic Reforming Catalysts. FCC Catalysts segment is expected to hold the largest market share by 2032. The increased demand for gasoline as a fuel for use in automobiles around the world is responsible for this segment's growth. Fluid catalytic cracking (FCC) catalysts, hydro treating catalysts, hydrocracking catalysts, and catalytic reforming are some of the other application-based segments.

The most common method used by refineries to transform heavy and high boiling hydrocarbons to lower value fractions is fluid catalytic cracking. The principal product of the process is gasoline, along with other fractions such as diesel and C3 and C4 gaseous fractions. This procedure aids in the production of more gasoline in order to meet the rising demand for automobiles. The lighter fractions are supplied to the alkylation plant, which produces a high-octane gasoline component known as alkylate, while the heavier portions are utilised as a diesel blender and additive.

Based on the Ingredient, the market is segmented into Zeolites, Metals, and Chemical Compounds. Zeolites segment is expected to grow rapidly during the forecast period 2026-2032. Zeolites are hydrated aluminosilicate minerals that are part of the microporous solids family. Because of their porosity and huge surface area, they are commonly employed as adsorbents and catalysts. Potassium (K+), sodium (Na+), calcium (Ca2+), and magnesium (Mg2+) are all accommodated by the porous structure of zeolites. Zeolites are generated naturally when volcanic rocks and ash layers combine with alkaline water. Because of the inclusion of various minerals, metals, and quartz in natural zeolites, they are impure. Zeolites, on the other hand, are commercially produced from the slow crystallisation of silica-alumina gel with a variety of additional atoms added to boost activity and performance in a certain process.

Metals segment is expected to grow rapidly during the forecast period 2026-2032. The type of feedstock, required cycle length, and final product are all factors in deciding which metal catalyst to utilise in the process. Clariant and BASF SE are two of the largest makers and providers of FCC and hydrocracking catalysts in the world. The rising demand for noble and other metals in growing economies such as Chile, China, and South Africa, as a result of favourable governmental support for FDI in mineral extraction, is expected to ensure the availability of raw materials for metal catalyst makers. The rising demand for these metals in other applications, on the other hand, is expected to restrain raw material availability, limiting the refinery catalyst market's growth during the forecast period.

Refinery Catalyst Market Regional Insights:

Asia Pacific region is expected to dominate the Refinery Catalyst Market during the forecast period 2026-2032. Asia Pacific region is expected to hold the largest market share by 2032. The fastest-growing refinery catalyst market is in Asia Pacific, owing to rising population, developing industrialization, rigorous regulatory requirements, and environmental restrictions, which are all contributing to the region's overall growth. The growing capacity of oil production in oil refineries in emerging countries in the region is generating significant potential prospects for the refinery catalyst market. During the forecast period, these factors are expected to drive up demand for refinery catalysts in the region.

Europe region is expected to grow rapidly during the forecast period 2026-2032. Due to high manufacturing costs and severe environmental laws, European refineries are experiencing low profitability. This legislative change in Russia is expected to boost catalyst demand in refining applications. Furthermore, technological advancements in enhanced oil recovery and hydraulic fracturing activities in countries such as Russia and Ukraine are expected to increase the availability of tight oil and shale gas. Increased shale gas production and tight oil supply are expected to make raw materials more accessible to refineries in Germany, France, and Italy, boosting the demand for refinery catalysts.

Recent Industry Developments (2025–2026)

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 14 January 2025 | Honeywell UOP | Launched the UOP Unity™ Hydrocracking Catalyst series, specifically engineered to maximize diesel yield from heavy vacuum gas oils. | The innovation enhances refinery profitability by increasing high-value distillate yields while reducing hydrogen consumption. |

| 05 February 2025 | Albemarle Corporation | Announced a strategic collaboration with a major Asian refinery to implement Action™ FCC Catalysts for improved plastic-to-fuel conversion. | This partnership drives the circular economy by enabling refineries to process recycled feedstock more efficiently. |

| 19 February 2025 | BASF SE | Introduced Altrium™, a new Fluid Catalytic Cracking (FCC) catalyst designed to improve gasoline octane while processing heavy metal-laden bottoms. | The product addresses the challenge of contaminant metals, allowing refiners to utilize cheaper, heavier crude slates. |

| 12 March 2025 | Clariant International Ltd. | Commissioned a state-of-the-art R&D center in Germany focused exclusively on sustainable refinery catalysts and hydrotreating technology. | The expansion accelerates the development of next-generation catalysts that support cleaner fuel production and lower emissions. |

| 27 March 2025 | Axens SA | Secured a major contract to provide its Impulse™ hydrotreating catalysts for a multi-billion dollar refinery expansion project in the Middle East. | The deployment ensures compliance with stringent Euro VI fuel standards and optimizes the desulfurization process for the regional market. |

The objective of the report is to present a comprehensive analysis of the Global Refinery Catalyst Market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market has been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The reports also help in understanding the Global Refinery Catalyst Market dynamic and structure by analyzing the market segments and projecting the Global Refinery Catalyst Market size. Clear representation of competitive analysis of key players by Distribution Channel, price, financial position, product portfolio, growth strategies, and regional presence in the Refinery Catalyst Market make the report investor’s guide.

Refinery Catalyst Market Scope: Inquire before buying

| Refinery Catalyst Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 6.12 USD Billion |

| Forecast Period 2026-2032 CAGR: | 4.02% | Market Size in 2032: | 8.06 USD Billion |

| Segments Covered: | by Type | FCC Catalysts Hydrotreating Catalysts Hydrocracking Catalysts Catalytic Reforming Catalysts |

|

| by Ingredient | Zeolites Metals Chemical Compounds |

||

| by Catalyst Material | Zeolites Metals Chemical Compounds |

||

Refinery Catalyst Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key players/ competitors profile covered in brief in Refinery Catalyst Market report in strategic perspective

- Albemarle Corporation

- W.R. Grace & Co.

- Axens SA

- Haldor Topsoe A/S

- BASF SE

- Johnson Matthey

- Honeywell UOP

- Clariant International Ltd.

- Criterion Catalysts & Technologies L.P.

- Air Products and Chemicals

- Arkema Group

- Chevron

- Eka Chemicals AB

- Exxon Mobil Corporation

- Evonic Industries AG

- Sinopec

- Anten Chemical

- Hebei Jinhong Chemical

- Ineos

- KNT Group

- Porocel Corporation

- Neste

- Shell

- Taiyo Koko

- Zibo Huaya