Professional Service Automation Market Size by Type, Deployment, Organisational Size, End Use, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2032

Overview

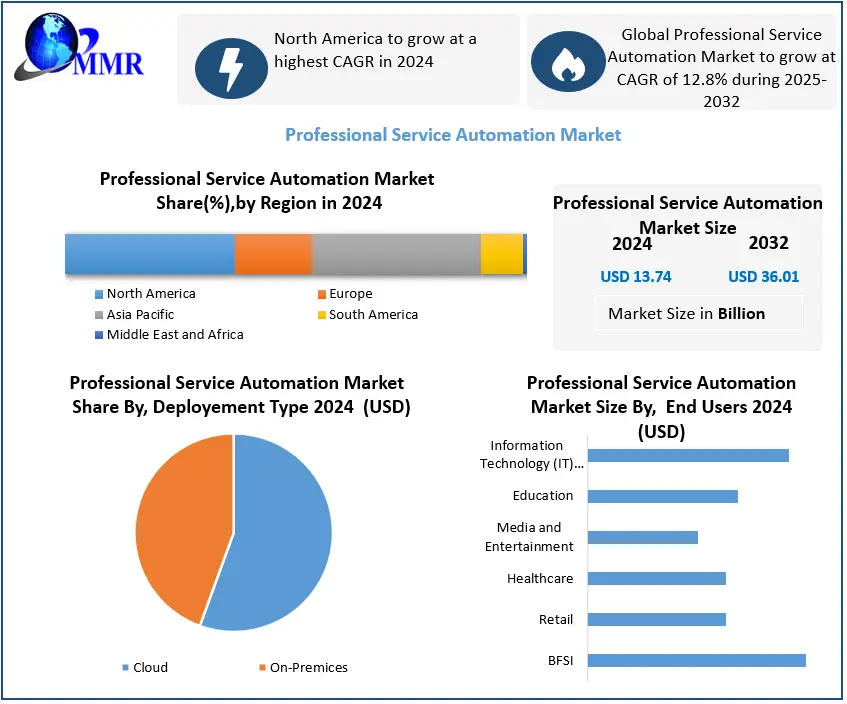

Professional Service Automation Market was valued at USD 13.74 Bn. in 2024 and the total Global Professional Service Automation Market revenue is Expected to grow at a CAGR of 12.8% from 2025 to 2032 reaching nearly USD 36.01 Bn. by 2032.

Professional Service Automation Market Overview:

Professional Services Automation (PSA) software streamlines project management, time tracking, invoicing, and resource planning into an integrated solution. It supports project lifecycles, starting from sales opportunities to final contract agreements, resource allocation, billing, and cash receipts. PSA ensures a standardized approach across project planning, management, and assessment, reducing manual tasks by centralizing operations and data. Often likened to Enterprise Resource Planning (ERP) for service-based firms, PSA is beneficial for organizations offering chargeable services. It offers visibility into crucial performance metrics like revenue, costs, utilization, and profit margins, particularly valuable as firms grow and their service-related expenses increase. Originally designed for professional service sectors (consultants, lawyers, specialized teams), PSA's benefits vary based on its capabilities but primarily allow monitoring and measuring service delivery at scale.

The Professional Service Automation market is experiencing significant growth globally due to the rising demand for integrated software solutions catering to service-based industries. This growth is primarily driven by the need for streamlined project management, resource allocation, and financial operations within these sectors. Businesses are increasingly seeking comprehensive tools that merge project management, time tracking, invoicing, and resource planning, aiming to improve operational efficiency. Automation plays a pivotal role in this expansion as PSA software reduces manual tasks, enhancing productivity and allowing businesses to focus on core activities.

Moreover, the scalability of PSA systems is particularly appealing to growing firms, providing standardized processes and metrics to manage escalating service-related expenses efficiently. Regions such as North America, Europe, and the Asia-Pacific are witnessing substantial growth in PSA adoption, thereby supporting the Professional Service Automation industry growth. North America's robust presence of service-based industries and tech-savvy approach, alongside Europe's adoption of digital solutions, contribute to their significant Professional Service Automation market growth. Meanwhile, emerging economies in the Asia-Pacific region are swiftly embracing digital transformation, contributing to the rising demand for PSA solutions in these markets.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Professional Service Automation Market Dynamics:

Organizational Benefits Associated With Professional Services Automation Developing the Performance Is A Key Driver For The Professional Service Automation Market

Professional Services adapts to organizations to help them better manage project teams, enhance staff productivity, improve service capabilities, and speed billings while minimizing costs through tighter integration of client and project-related data. It offers solutions to meet specific financial and project management requirements. Automation Professional Services provides Connect information about financial, resource, and intellectual capital. By linking diverse systems and information, organizations may save duplicated work, streamline procedures, enhance accuracy, and boost productivity.

With real-time access to information, users can better manage the business. Reporting and business intelligence (BI) technologies enable companies to swiftly acquire and evaluate customer and project information, allowing them to make educated choices. In addition, it provides corporate employees with integrated collaborative workspaces and centralized access to essential information via a simple web-based interface.

Increase productivity with closely integrated tools that cover everything from project planning and budgeting to resource use and analysis. Moreover, with the capacity to gather, evaluate, and analyze resource use to enable improved resource planning, allocation, scheduling, and predictions, organizations may assess employee productivity and plan more efficiently. These factors develop the interest of consumers and are aiding in increasing the global Professional Service Automation market growth.

Increased Inclination Of Organizations Toward Digitalization And Process Automation Drives The Global Professional Service Automation Market Growth

The increasing need for enhanced mobility among service consultants, growing adoption of automation, and improving internet infrastructure are anticipated to boost the Professional Service Automation market growth. The global professional services automation (PSA) software market is being driven by increased demand for PSA software, as a result of the availability of PSA solutions with enhanced functionality. With organizations' increasing inclination toward digitization and process automation, the need for process automation is increasing and this is expected to drive the Professional Service Automation market growth during the forecast period.

Several solution developments have taken place in the industry, aiding in the Professional Service Automation market growth. For example, VOGSY, the only PSA solution based on Google's G Suite, provides business process support and integration across professional services organizations' fundamental operations. It is based on a single, easily accessible platform that serves personnel from different departments. VOGSY's most distinguishing feature is that it created a simple yet sophisticated PSA solution that drives users to perform additional tasks.

Lack Of Skilled Professionals And High Deployment Cost Restraining The Professional Service Automation Market Size

Continuous professional development requirements incorporate both the skill and cost channels in terms of eligibility conditions. Professional qualifications may not give the skills needed to deploy digital automation systems, and they may impose higher financial and time spending. As a result, not only do they not guarantee a step forward in digital automation, but they may potentially redirect resources away from it. On the other hand, it may be claimed that any time the essential abilities are relevant to digital automation, it may have a beneficial influence on digital automation since it allows for the upkeep of skills.

Another unique constraint within this regulatory region is the category of certification requirements: skills and cost channels operate in this situation as well. Indeed, the certifications required for practice could not give the digital competencies required to apply digital technologies and new services. Additionally, this limitation may reflect a skill mismatch between the qualification standards and the real skills and knowledge necessary to use digital automation technologies, posing an obstruction to growing abilities, effort, and talents in digital transformation. This implies that focusing on specific activities and abilities essential to the regulated profession may divert resources and time away from digital automation training and development.

Professional Service Automation Market Segment Analysis:

Based on Component, Professional Service Automation Market segmented into solution and service. Service segment dominated the market in 2024 and held the largest market share of about 82.6% in 2024 for the Professional Service Automation market. The services segment is expected to grow at a faster CAGR during the forecast period because services enable organizations to easily deploy software on their premises or in the cloud and enable organizations to build successful customer relations through ongoing support throughout the business tenure. Through a broad collection of consulting services, Professional Services provides unique capabilities.

These services promote innovation by providing simplified and efficient solution delivery. Professional Services Conduct a discovery assessment session to investigate existing use cases, map them by complexity, pick a use case candidate for delivery, and create a roadmap for future use cases. In addition, it Conducts an architecture and design workshop to gather information for RPA platform deployment, covering components such as infrastructure, networking, security, access, and applications, and collaborates with customer SMEs to generate high-level architectural and use case design documentation.

Based on Deployment, the market is segmented into SMEs and Cloud. Cloud segment dominated the market in 2024 and is expected to hold largest share during the forecast period. End-to-end cloud services that incorporate creative strategy and design and allow the underlying cloud technology to become more important as the requirement for adopting cloud applications, cloud migration, and cloud-native development increases.

Service providers with significant sector knowledge, industry-specific cloud offerings, and a variety of technological services ranging from consultancy to managed services are also going to be in high demand. Accenture possesses all of these characteristics, which helps to explain why Accenture is a global IDC markets cape Cloud Professional Services Leader. Accenture has a great possibility for success if it can overcome the problems, especially maintaining relevance with its major clients and creating revenue growth.

Based on End-users, the BFSI segment held the largest revenue share of about 32% in 2024 and is expected to hold largest market share during the forecast period. its dominance at the end of the forecast period. By automating the repetitive and time-consuming backend procedures in the banking business, financial institutions may streamline their operations, save operational expenses, and optimize their credit collection process. It also benefits the sector in evolving and eliminating unnecessary procedures, as well as improving financial institutions' legitimacy. It also enables institutions to devote their valuable resources to a variety of other critical value-added initiatives and tasks that require the engagement of individuals.

Service automation is extensively used in the BFSI industry since it automates transactional processes at scales, such as invoice processing, data input, reporting, cash collection, credit collection, vendor payment, and many others. HSBC has launched Treasury APIs, allowing treasurers to rapidly initiate, manage, and finish transactions while increasing visibility. The connection improves corporate payment transparency and enables finance managers to make educated and dynamic cash and credit management decisions. Additionally, some Fintech companies are also creating block chain-based accounts receivable automation solutions to improve their accounts receivable cycle.

Professional Service Automation Market Regional Insights:

North America held the largest revenue share of about 42.8% in 2023 for the Professional Service Automation market and is expected to dominate the market at the end of the forecast period. The major portion of industrial-technological innovators is situated in the North American regional market. These leaders are actively working to advance existing technology as well as expand unique market opportunities. Greater demand is being felt as a result of the region's rapidly aging workforce; automation aids seamless management and appropriate allocation of available resources.

North America's regional development may also be linked to the service industry's explosive growth and technological advancements. Regional corporations have also adopted inorganic development techniques to strengthen their global presence. Oracle, for example, chose collaboration and partnership to launch new market solutions.

Likewise, the region's major advanced economies, the United States and Canada, are investing in developing technologies and building IT infrastructure. Because of the existence of key market participants providing professional service automation products and services, such as Microsoft Corporation, Autotask Corporation, FinancialForce.com, and others, the United States is a big stakeholder in this area. The system integrates automated accounts payable and receivables processes, as well as mechanisms for paying bills and sending invoices within NetSuite.

These regional advancements would increase the regional market throughout the forecast period. The United States is home to a wide number of PSA software suppliers, including Salesforce.com, Inc., Microsoft Corporation, SolarWinds, and Oracle Corporation, which projects well for regional market growth. Salesforce.com, Inc., for example, released AI-powered marketing cloud advancements in September 2021 to help firms better every engagement and maximize marketing effect through unified data.

The Asia-Pacific market is expected to grow rapidly during the forecast period. With the increasing use of smartphones and the growing trend of digital culture, the demand for cloud services is developing throughout the Asia-Pacific region. Additionally, with the introduction of 5G networks, businesses are rapidly shifting to cloud computing to deliver better services.

The Japanese cloud computing company flourished substantially as a result of the COVID-19 outbreak. As the Japanese government imposed social distancing rules and lockdowns, there was a quick shift toward remote working, which could only be accomplished through cloud computing. As the volume of data rose and the requirement for remote access emerged, the region's need for cloud-based solutions increased substantially.

Scope of the Professional Service Automation Market Report:

The report covers the overall structure of the Professional Service Automation Market and provides premium insights that can assist software vendors, network operators, telecom service providers, equipment manufacturers, third-party providers, and managed service providers in identifying the needs of large and small organizations (end users), as well as displaying the gaps for telecom service providers and network operators. The report investigated the growth rate and penetration in the key regions and the report analyses global adoption patterns, future growth potentials, major drivers, limitations, prospects, Challenges, and best practices in the Professional Service Automation Market. It also investigates future demand sizes and revenue estimates across various geographies and user groups.

The report further includes a PORTER and PESTEL analysis, as well as the possible influence of market microeconomic aspects. External and internal elements that are expected to affect the organization positively or adversely have been studied, providing decision-makers with a clear future vision of the Professional Service Automation industry. The report also helps in the comprehension of the market trends and structure by studying market segments and projecting the Professional Service Automation market size. The study is an investor's guide because of its clear depiction of competitive analysis of key competitors in the Professional Service Automation market by service, price, financial situation, product portfolio, growth plans, and geographical presence.

Professional Service Automation Market Research Methodology:

The report analysis begins with the data collection and analysis of key vendor product offerings and business strategies from secondary sources. The vendor offerings were also considered while determining market segmentation. The entire market size of the Professional Service Automation Market was calculated using the bottom-up approach. Primary and secondary research is used to create the Professional Service Automation Market report. Secondary data sources include nationalized and global data sources, OneSource Business Browser, D&B Hoovers, 10K Wizard, Bloomberg, Thomson Street Events, Factiva, IT service providers, technology providers' annual and financial reports from major market participants, news announcements, and so on. Interviews, surveys, expert and trained professional opinions, and other methods were used to collect primary data.

The research also includes information on current developments, trade regulations, import-export analysis, production analysis, value chain optimization, market share, the effect of domestic and major & and localized market players, changes in market regulations, and strategic market growth analysis. The data gives a comprehensive study of the present rapid advances in all industry sectors. The report investigates the drivers, constraints, possibilities, and challenges in the Professional Service Automation Market. The report includes recommendations for all sectors based on a detailed study of the current competitive environment in the Professional Service Automation Market. Key data analysis for the historical period from 2018 to 2023 is provided using facts and figures, pictures, and presentations.

Professional Service Automation Market Scope: Inquire before buying

| Global Professional Service Automation Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 13.74 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 12.8% | Market Size in 2032: | USD 36.01Bn. |

| Segments Covered: | By Type | Solutions Project Management Project Accounting Time and Expense Management Project Analytics Billing and Invoice Management Resource Management Contract Management Opportunity and Lead Management Others Services Training and Support Integration and Implementation |

|

| By Deployment | Cloud On-Premises |

||

| By Organisational Size | SMEs Large Enterprises |

||

| By End Use | BFSI Retail Healthcare Media and Entertainment Education Information Technology (IT) and Telecom Government Legal Services Audit and Accountancy Scientific Research and Development Services Others |

||

Professional Service Automation Market by Region:

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Professional Service Automation Market Key Players:

Global Professional Service Automation Market Key Players:

1. SAP S/4HANA Cloud

2. Replicon PSA

3. Scoro

4. Avaza

North America Professional Service Automation Market Prominent Providers:

1. Changepoint Corporation (US)

2. Microsoft (US)

3. ConnectWise (US)

4. Mavenlink, Inc. (US)

5. Kaseya Limited (US)

6. BigTime

7. Planview Clarizen

8. Autotask Corporation (Datto Inc.)

9. Deltek Inc.

10. Financialforce Inc.

11. NetSuite Inc. (Oracle Corporation)

12. Upland Software Ltd.

13. Projector PSA Inc.

14. Workfront, Inc.

Europe Professional Service Automation Market Top Contributors:

1. Kimble Applications (UK)

2. SAP (Germany)

3. Project Open Business Solutions S.L (Spain)

4. Infor Inc.

5. Unanet Technologies

Asia Pacific Professional Service Automation Market Leading Companies:

1. Atlassian (Australia)

FAQs:

1. What are the growth drivers for the Professional Service Automation market?

Ans. The increased demand for integrated software solutions, the necessity for operational efficiency and automation, the scalability needs of growing firms, the rise of service-based industries, and the importance of data-driven decision-making are expected to be the major drivers for the Professional Service Automation market.

2. What is the major restraint for the Professional Service Automation market growth?

Ans. The high operational costs associated with implementing and maintaining PSA systems, which can limit adoption, particularly for smaller organizations are expected to be the major restraining factor for the Professional Service Automation market growth.

3. Which region is expected to lead the global Professional Service Automation market during the forecast period?

Ans. North America is expected to lead the global Professional Service Automation market during the forecast period.

4. What is the projected market size and growth rate of the Professional Service Automation Market?

Ans. The Professional Service Automation Market size was valued at USD 13.74 Billion in 2024 and the total Professional Service Automation revenue is expected to grow at a CAGR of 12.8% from 2025 to 2032, reaching nearly USD 36.01 Billion by 2032.

5. What segments are covered in the Professional Service Automation Market report?

Ans. The segments covered in the Professional Service Automation market report are Component, Deployment, Organization Size, End-user, and Region.