Piping Spools and Process Pipes Market Size by Equipment Type, End-use Industry, Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2030

Overview

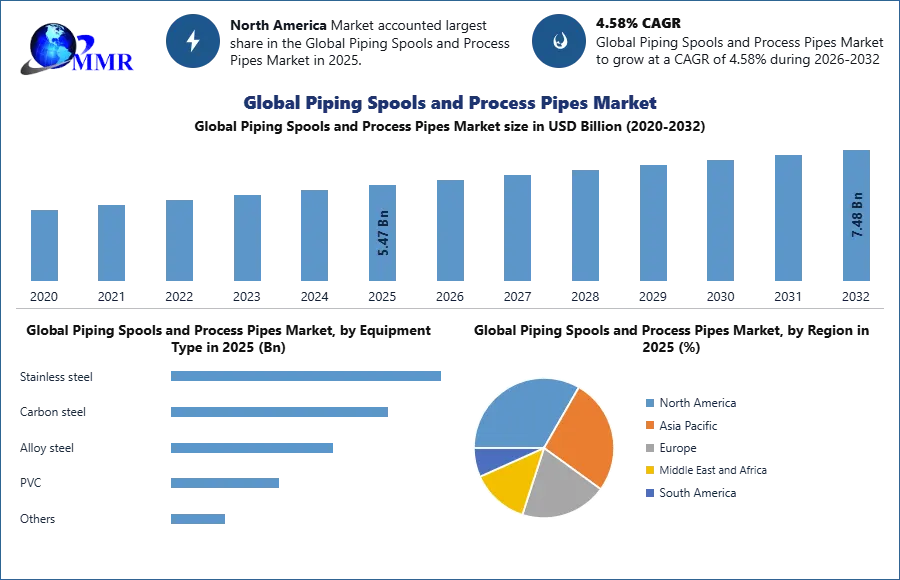

The Piping Spools and Process Pipes Market size was valued at USD 5.47 Billion in 2025 and the total Piping Spools and Process Pipes Market revenue is expected to grow at a CAGR of 4.58% from 2026 to 2032, reaching nearly USD 7.48 Billion by 2032.

Piping Spools and Process Pipes Market Overview:

Piping spools and process pipes are integral components in industries like oil and gas, power generation, chemical processing, and pharmaceuticals. These systems are designed to transport various fluids, gases, and chemicals safely and efficiently. Constructed using durable materials such as stainless steel, carbon steel, and alloy steel, these pipes are manufactured to withstand extreme conditions such as high pressure, temperature, and corrosive environments. Piping spools are pre-fabricated pipe sections that are customized for specific installations, streamlining the construction process while ensuring reliability and safety. With increasing industrial demands, the need for high-quality piping systems has surged, driving the growth of the market.

To know about the Research Methodology :- Request Free Sample Report

This comprehensive report delves into the dynamics of the piping spools and process pipes market, providing valuable insights for stakeholders across various industries. It covers key aspects including market size, growth projections, competitive landscape, material segmentation, and the latest technological trends like Industry 4.0 adoption and smart manufacturing techniques. Additionally, the report offers an in-depth analysis of regional and country-level market dynamics, with a focus on high-growth regions and sectors. Our findings will help manufacturers, investors, and industry leaders make informed decisions, assess market opportunities, and navigate challenges effectively in the rapidly evolving piping solutions market.

The market is driven by key factors such as rising industrial investments in the oil and gas, power generation, and chemical sectors. Technological advancements, including the integration of robotics and AI-driven design, are enhancing production efficiency, reducing costs, and ensuring higher precision in manufacturing. However, challenges like material costs and skilled labor shortages remain prevalent. The fastest-growing region for the piping spools and process pipes industry is North America, particularly the United States, which holds over 60% of the market share. Driven by the booming shale oil industry and significant investments in energy infrastructure, the U.S. is expected to maintain a strong market presence in the upcoming years.

Piping Spools and Process Pipes Market Dynamics:

Rising Investments in Oil & Gas and Power Generation Sectors Driving Market Expansion

The piping spools and process pipes market is experiencing significant growth, largely driven by the rising investments in the oil & gas and power generation sectors. These industries require reliable, durable, and corrosion-resistant piping systems to support their critical infrastructure needs, driving the demand for high-quality piping spools and process pipes. In the oil & gas sector, the demand for piping solutions has grown substantially due to ongoing exploration and production activities, especially in offshore and deep-water drilling projects. As per recent reports, global investments in the oil and gas sector are expected to exceed USD xx trillion by 2026, with a major portion allocated to pipeline infrastructure. This surge in investment is leading to an increase in the procurement of specialized piping materials like stainless steel and carbon steel. As a result, the demand for process pipes and spools used in upstream, midstream, and downstream operations is set to rise sharply. In the power generation sector, the push towards renewable energy and nuclear power plants has further accelerated the need for robust piping solutions. Countries worldwide are investing heavily in upgrading power grids and building new power plants, especially in Asia Pacific and North America. According to MMR report, investments in power generation are expected to surpass USD 2 trillion annually by 2032. This includes investments in both traditional and renewable energy sources, increasing the requirement for process pipes used in high-temperature and high-pressure environments.

The energy transition projects and the rise of smart grids are expected to further amplify the demand for advanced piping systems. Overall, the combination of rising investments, technological advancements, and the growing need for energy infrastructure is creating a highly favourable environment for the growth of the piping spools and process pipes market.

Increasing Need for Durable and Corrosion-Resistant Materials in Critical Industries

The increasing need for durable and corrosion-resistant materials in critical industries, especially in oil & gas, power generation, and chemical processing, is a major driver for the growing demand for piping spools and process pipes. Industries that operate in extreme environments, such as high-pressure systems, offshore drilling, and high-temperature power plants, require materials that withstand harsh conditions and offer long-lasting performance. As a result, materials such as stainless steel, alloy steel, and duplex stainless steel are in high demand. These materials offer excellent corrosion resistance, strength, and durability, making them ideal for handling aggressive chemicals and corrosive environments.

The pricing dynamics in the piping spools market are influenced by raw material costs, which have seen a steady rise due to global supply chain disruptions and increasing demand for specialized alloys. For instance, the price of stainless steel has increased by approximately 10-12% in the past two years, primarily due to fluctuations in raw material availability and rising manufacturing costs. This price increase directly impacts the overall cost of process piping systems, making the demand for durable and corrosion-resistant materials even more critical. In oil & gas and power generation, the demand for such materials is projected to increase by 15-18% over the next five years, with key regions such as Asia Pacific and North America leading the charge. Advanced coatings and composite materials are also emerging trends, further enhancing the longevity and performance of piping systems. As industries prioritize sustainability and safety, the need for reliable, durable materials will continue to shape the piping spools and process pipes market.

Cost Pressures and Labor Shortages: Barriers to Growth in the Piping Spools and Process Pipes Market

A significant obstacle hindering the expansion of the piping spools and process pipes market is the escalating cost of specialized materials, which are essential for demanding applications in industries such as oil & gas, power generation, and chemical processing. These industries demand materials that offer high corrosion resistance, strength, and durability, which often come at a premium price. The rising costs of stainless steel, alloy steel, and high-performance alloys have made the procurement of these materials a significant burden for manufacturers, particularly in regions with constrained budgets or fluctuating raw material prices. Additionally, the complex manufacturing processes involved in producing custom piping spools further increase costs, limiting the ability of small and medium-sized companies to compete in the market. Another restraint is the lack of skilled labor required to handle and fabricate these materials accurately, especially in highly regulated sectors. The growing emphasis on environmental regulations and sustainability goals in various countries also adds complexity to the production and disposal processes of piping systems. These factors contribute to the market's slow adoption in certain regions, particularly where cost-effectiveness and operational efficiency are top priorities for companies, impacting overall growth in the sector.

Leveraging Technology and Material Innovation for Growth in the Piping Spools and Process Pipes Market

A game-changing opportunity for growth in the piping spools and process pipes market is unfolding through the rapid technological advancements and material innovation reshaping the industry. Emerging smart manufacturing techniques, such as additive manufacturing (3D printing) and robotics, are set to transform production, driving precision, efficiency, and cost reductions. AI-driven design software and machine learning are empowering manufacturers to optimize custom piping spool designs, minimizing errors and waste. Furthermore, the development of new composite materials with superior corrosion resistance and lightweight properties presents a tremendous opportunity for industries to meet the rigorous demands of corrosive environments like offshore oil rigs and chemical plants. These advancements not only enhance the performance and durability of piping systems but also align with global sustainability efforts by reducing material waste and energy consumption. With the integration of IoT-based monitoring, the future of piping solutions looks poised for enhanced predictive maintenance and eco-friendly outcomes.

Streamlining Global Piping Spool Supply Chains for Competitive Advantage

The supply chain in the piping spools and process pipes market is a complex network that involves multiple stages from raw material procurement to the final product delivery to end-users in industries such as oil & gas, power generation, and chemical processing. The supply chain starts with the procurement of high-quality materials, such as stainless steel, alloy steels, and composite materials, which are essential for producing corrosion-resistant, durable pipes and spools. Manufacturers then work with specialized fabricators and welders to process these materials into custom piping spools, adhering to strict industry standards for safety and performance. Logistics providers play a crucial role in transporting the finished products to end-user facilities, often across global supply chains. This stage is sensitive to fluctuating shipping costs, customs regulations, and inventory management practices, which impacts lead times and overall costs. Also, the increasing demand for just-in-time inventory systems is pushing companies to optimize their supply chains and reduce unnecessary stockpiles, enhancing efficiency and cost-effectiveness. Technological advancements such as IoT-enabled tracking systems and AI-based analytics are transforming supply chain operations by providing real-time visibility, helping identify potential disruptions and improving forecasting accuracy. However, the lack of skilled labor and geopolitical tensions in certain regions pose risks to supply chain stability, resulting in potential delays or price increases. Ultimately, a well-managed supply chain is critical to maintaining a steady flow of high-performance piping systems to meet the growing needs of industries demanding durable, corrosion-resistant, and cost-effective solutions.

Piping Spools and Process Pipes Market Segment Analysis:

Based on Equipment Type: In the piping spools and process pipes market, stainless steel continues to dominate, accounting for over 40% of the market share in 2025. Its exceptional resistance to corrosion, strength, and high-temperature endurance makes it the material of choice for critical applications in industries like oil & gas, power generation, and chemical processing. The demand for stainless steel is driven by its ability to provide long-term performance and reliability, contributing to a steady market growth rate of 5-7% annually. The carbon steel segment follows closely, holding around 30% of the market share, primarily due to its affordability and suitability for lower-cost projects. Alloy steel, with its superior wear and tear resistance, captures approximately 15% of the market, particularly in high-performance applications where strength is a priority. While PVC and other materials like composites are gaining traction in specific regions, they represent a smaller share, accounting for about 10-15% of the market. PVC is especially popular in non-corrosive environments, offering cost advantages but with lower performance in demanding applications. The market for alloy steels and carbon steels is expected to see growth of 6-8% annually, driven by the increasing adoption of advanced materials in process-intensive industries. Companies focusing on stainless steel and alloy steel production are experiencing higher profit margins due to the premium pricing of these materials. Overall, the market's growth is driven by the demand for durable, corrosion-resistant, and high-performance piping solutions.

Piping Spools and Process Pipes Market Regional Analysis:

North America stands as the dominant region in the global piping spools and process pipes market, with the United States leading the charge due to its robust investments in oil & gas, power generation, and chemical processing industries. The region accounts for the largest share of market demand, driven by infrastructure development projects, including shale oil and gas exploration. The U.S. is projected to maintain its market leadership with a strong compound annual growth rate of around 5-6% over the next few years. The demand for high-performance materials, such as stainless steel and alloy steel, remains strong, especially in critical applications like offshore rigs and chemical plants.

The United States dominates North America's piping spools and process pipes market, with over 60% of the regional share in 2025. Key drivers include substantial investments in oil & gas, power generation, and chemical processing industries. The country leads in adopting advanced technologies, such as smart manufacturing and composite materials, to meet stringent regulatory standards and growing demand for high-performance materials like stainless steel.

Canada's market is driven by oil sands projects in Alberta and the growing need for eco-friendly, corrosion-resistant piping materials. Projected to grow at 5-7% annually, Canada is embracing innovative material technologies, including composite systems for challenging environments like offshore oil rigs, contributing to steady market growth.

Mexico is witnessing a surge in industrial activity, driven by investments in oil & gas and power generation sectors. Although its market share is smaller, it is expected to grow at a CAGR of xx %, thanks to its expanding energy infrastructure and cost-effective manufacturing, making it an emerging player in the market.

Piping Spools and Process Pipes Market Scope: Inquire Before Buying

| Global Piping Spools and Process Pipes Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 5.47 USD Billion |

| Forecast Period 2026-2032 CAGR: | 4.58% | Market Size in 2032: | 7.48 USD Billion |

| Segments Covered: | by Equipment Type | Stainless steel Carbon steel Alloy steel PVC Others |

|

| by End-use Industry | Power plant Petroleum refineries Offshore, shipbuilding, and marine Chemical and fertilizers Pharmaceuticals Others |

||

Piping Spools and Process Pipes Market Competitive Landscape

• In 2023, Vallourec successfully delivered a comprehensive range of line pipe products for LLOG Exploration's deepwater Salamanca project off the U.S. Gulf Coast. This project underscores Vallourec's capability in providing high-quality piping solutions for complex offshore developments.

• In 2024, Federal Steel Supply highlighted emerging technologies and materials reshaping pipe manufacturing. The company emphasized the industry's shift towards sustainability and innovation, positioning itself at the forefront of these transformative trends.

• In 2024, HGG Group launched PypeServer and ProCam, software tools designed to transform pipe fabrication workflows. These tools enable CAD designers to import pipe designs and spools, streamlining the fabrication process.

Piping Spools and Process Pipes Market by Region

North America (United States, Canada, and Mexico)

Europe (United Kingdom, France, Germany, Italy, Spain, Sweden, Russia, Rest of Europe)

Asia Pacific (China, Japan, South Korea, India, Australia, Malaysia, Thailand, Vietnam

Indonesia, Philippines, and Rest of Asia Pacific)

Middle East and Africa (South Africa, GCC, Nigeria, Egypt, Turkey, and Rest of ME&A)

South America (Brazil, Argentina, Colombia, Chile, Peru, and Rest of South America)

Key Players/Competitors Profiles Covered in the Piping Spools and Process Pipes Market Report in Strategic Perspective

1. DEE Development Engineers Limited (DEE Piping Systems)

2. Prosaic Steel and Alloys

3. Larsen & Toubro Limited (L&T Piping Center)

4. CHELPIPE Group

5. Cogbill Construction, LLC

6. YENA Engineering B.V.

7. CCI Leidingsystemen BV

8. Metal Forge India

9. Arabian International Co. for Steel Structures (AIC)

10. Forterra Inc. (U.S. Pipe)

11. ENKA Insaat ve Sanayi (Cimtas Pipe Fabrication and Trading Co. Ltd.)

12. SUNG IL SIM CO LTD.

13. SEONGHWA Industrial Co., Ltd.

14. Creative Piping Solution

15. DEE Development Engineers Limited (DEE Piping Systems)

16. Shree Sarjan Industries Pvt. Ltd.

17. Emcor Engineering India LLP

18. United Engineers And Consultants (Piping Spools)

19. Saanvika Corporation

20. RELI ENGINEERING

21. Shashwat Stainless Inc

Frequently Asked Questions:

1] What is the projected market size & and growth rate of the Piping Spools and Process Pipes Market?

Ans. The Piping Spools and Process Pipes Market size was valued at USD 5.47 Billion in 2025 and the total Piping Spools and Process Pipes revenue is expected to grow at a CAGR of 4.58% from 2026 to 2032, reaching nearly USD 7.48 Billion By 2032.

2] What segments are covered in the Global Piping Spools and Process Pipes Market report?

Ans. The segments covered in the Piping Spools and Process Pipes Market report are based on Equipment Type, End-use Industry, and region.

3] Which region is expected to hold the highest share in the Global Piping Spools and Process Pipes Market?

Ans. The North American region is expected to hold the highest share of the Piping Spools and Process Pipes Market.

4] What is the forecast period for the Global Piping Spools and Process Pipes Market?

Ans. The forecast period for the Piping Spools and Process Pipes Market is 2026-2032.